by Shareholdersunite

by Shareholdersunite

Summary

- OPEC is supposedly out to beat, or at least curtail the growth of American shale oil production.

- For a host of reasons, especially the much shorter capex cycle for shale, they will not succeed unless they are willing to accept permanent low oil prices.

- But, permanent low oil prices will do too much damage to OPEC economies for this to be a credible threat.

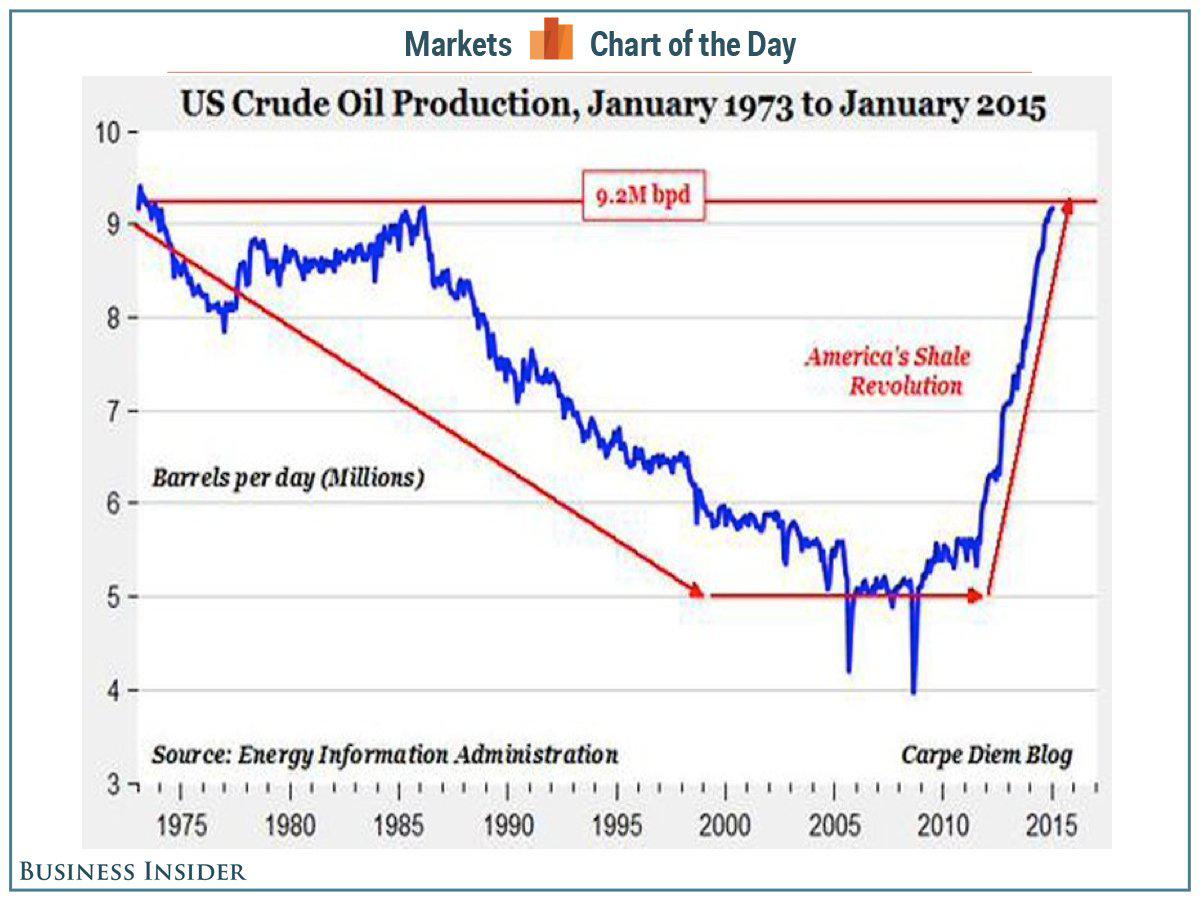

We’re sure by now you are familiar with the main narrative behind the oil price crash. First, while oil production outside of North America is basically stagnant since 2005.

The shale revolution has dramatically increased supply in America.

(click to enlarge)

The resulting oversupply has threatened OPEC and the de-facto leader Saudi Arabia has chosen a confrontational strategy not to make way for the new kid on the block, but instead trying to crush, or at least contain it. Can they achieve this aim, provided it indeed is their aim?

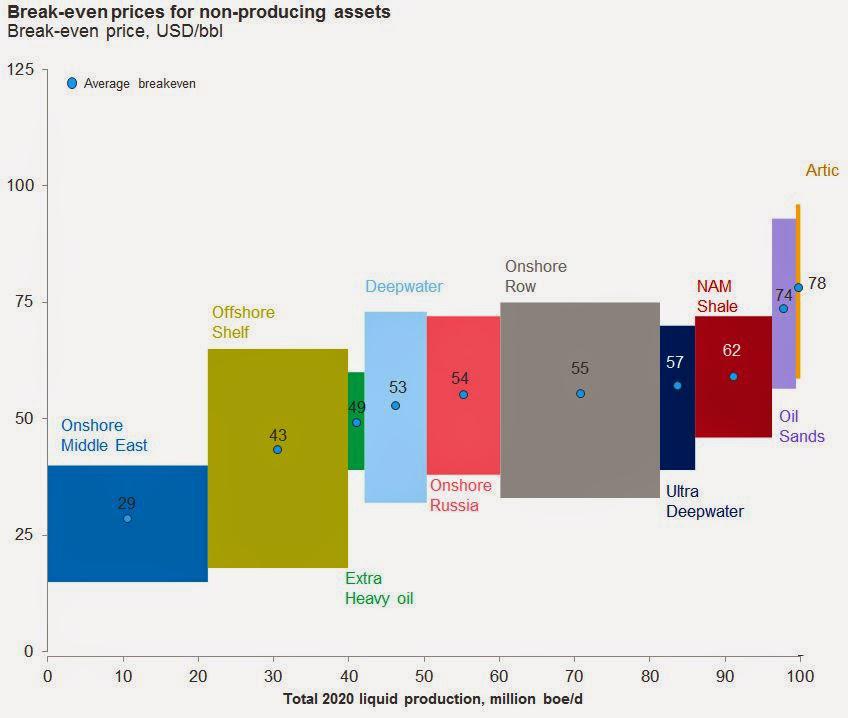

Breakeven price

At first, one is inclined to say yes, for the simple reason that Saudi (and most OPEC) oil is significantly cheaper to get out of the ground.

(click to enlarge)

This suggests that all OPEC has to do is to keep output high and sooner or later the oversupply will work itself off the market, and expensive oil is more likely to see cutbacks than cheaper oil, although this critically depends on incentives facing individual producers.

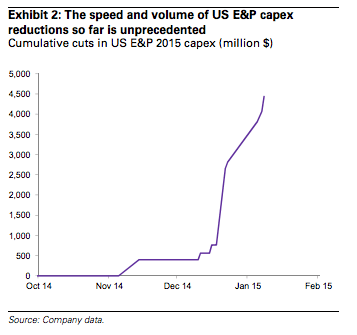

Capex decline

It is therefore no wonder that we’ve seen significant declines in rig counts and numerous companies have announced considerable capex declines. While this needs time to work out into supply cutbacks, these will eventually come.

For instance BP (NYSE:BP) cutting capex from $22.9B in 2014 to $20B in 2015, or Conoco (NYSE:COP) reducing expenditures by more than 30% to $11.5B this year on drilling projects from Colorado to Indonesia. There are even companies, like SandRidge (NYSE:SD), that are shutting 75% of their rigs.

Leverage

It is often argued that the significant leverage of many American shale companies could accelerate the decline, although it doesn’t necessarily have to be like that.

While many leveraged companies will make sharp cutbacks in spending, which has a relatively rapid effect on production (see below), others have strong incentives to generate as much income as possible, so they might keep producing.

Even the companies that go belly up under a weight of leverage will be forced to relinquish their licenses or sell them off at pennies to the dollar, significantly lowering the fixed cost for new producers to take their place.

Hedging

Many shale companies have actually hedged much of their production, so they are shielded from much of the downside (at a cost) at least for some time. And they keep doing this:

Rather than wait for their price insurance to run out, many companies are racing to revamp their policies, cashing in well-placed hedges to increase the number of future barrels hedged, according to industry consultants, bankers and analysts familiar with the deals. [Reuters]

Economics

Being expensive is not necessarily a sufficient reason for being first in line for production cuts. For instance, we know that oil from the Canadian tar sands is at the high end of cost, but simple economics can explain why production cuts are unlikely for quite some time to come.

The tar sands involve a much higher fraction as fixed cost:

Oil-sands projects are multibillion-dollar investments made upfront to allow many years of output, unlike competing U.S. shale wells that require constant injections of capital. It’s future expansion that’s at risk. “Once you start a project it’s like a freight train: you can’t stop it,” said Laura Lau, a Toronto-based portfolio manager at Brompton Funds. Current oil prices will have producers considering “whether they want to sanction a new one.” [Worldoil]

So, once these up-front costs are made, these are basically sunk, and production will only decline if price falls below marginal cost. As long as the oil price stays above that, companies can still recoup part of their fixed (sunk) cost and they have no incentive to cut back production.

But, of course, you have tar sand companies that have not yet invested all required up-front capital and new capex expenditures will be discouraged with low oil prices. So, there is still the usual economic upward sloping supply curve operative here.

Swing producer

The funny thing is American shale oil is at the opposite end of this fixed (and sunk) cost universe, apart from acquiring the licenses. As wells have steep decline curves, production needs constant injection of capital for developing new wells.

Production can therefore be wound down pretty quickly should the economics require, and it can also be wound back up relatively quickly, which we think is enough reason why American shale is becoming the new (passive) swing producer. This has very important implications:

- The relevant oil price to look at isn’t necessarily the spot price, but the 12-24 months future price, the time frame between capex and production.

- OPEC will not only need to produce a low oil price today, that price needs to be low for a prolonged period of time in order to see cutbacks in production of American shale oil. Basically, OPEC needs the present oil price to continue indefinitely, as soon as it allows the price to rise again, shale oil capex will rebound and production will increase fairly soon afterwards.

So basically, shale is the proverbial toy duck which OPEC needs to submerge in the bathtub, but as soon as it releases the pressure, the duck will emerge again.

Declining cost curves

The shale revolution caught many by surprise, especially the speed of the increase in production. While technology and learning curves are still improving, witness how production cost curves have been pushed out in the last years:

There is little reason this advancement will come to a sudden halt, even if capex is winding down. In fact, some observers are arguing that producers shift production from marginal fields to fields with better production economics, and the relatively steep production decline curves allow them to make this shift pretty rapidly.

Others point out that even the rapid decline in rig count will not have an immediate impact on production, as the proportion of horizontal wells and platforms where multiple wells are drilled from the same location are increasing, all of which is increasing output per rig.

Another shift that is going on is to re-frack existing wells, instead of new wells. The first is significantly cheaper:

Beset by falling prices, the oil industry is looking at about 50,000 existing wells in the U.S. that may be candidates for a second wave of fracking, using techniques that didn’t exist when they were first drilled. New wells can cost as much as $8 million, while re-fracking costs about $2 million, significant savings when the price of crude is hovering close to $50 a barrel, according to Halliburton Co., the world’s biggest provider of hydraulic fracturing services. [Bloomberg]

Production cuts will take time

The hedging and shift to fields with better economics is only a few of the reasons why so far there has been little in the way of actual production cuts in American shale production, the overall oil market still remains close to record oversupply. The International Energy Agency (IEA) argues:

It is not unusual in a market correction for such a gap to emerge between market expectations and current trends. Such is the cyclical nature of the oil market that the full physical impact of demand and supply responses can take months, if not years, to be felt [CNBC].

In fact, the IEA also has explicit expectations for American shale oil itself:

The United States will remain the world’s top source of oil supply growth up to 2020, even after the recent collapse in prices, the International Energy Agency said, defying expectations of a more dramatic slowdown in shale growth [Yahoo].

OPEC vulnerable itself

Basically, the picture we’re painting above is that American shale will be remarkably resilient. Yes, individual companies will struggle, sharp cutbacks in capex are already underway, and some companies will go under, but the basic fact is that as quick as capex and production can fall, they can rise as quickly again when the oil price recovers.

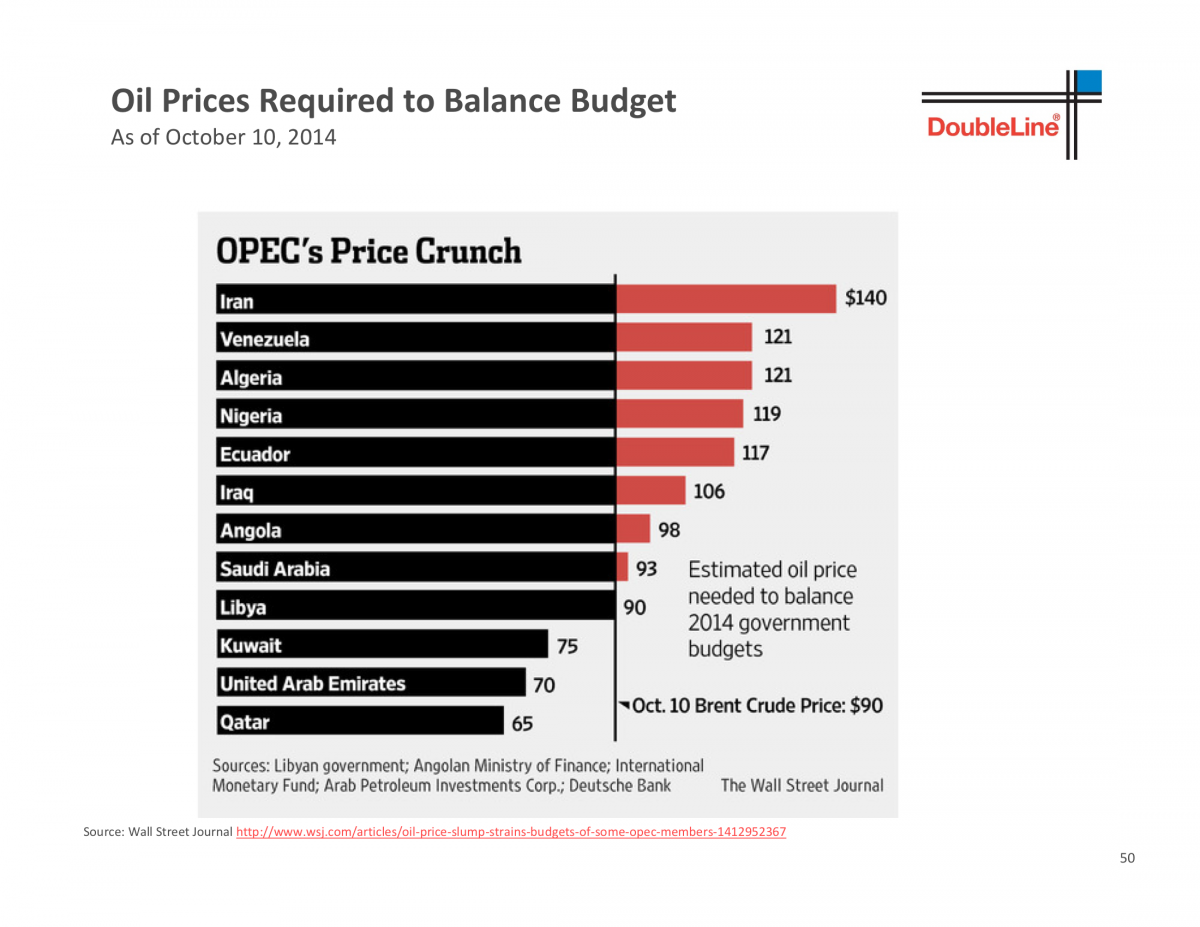

How much of OPEC can the storm of the oil price crash, very much remains to be seen. There is pain all around, which isn’t surprising as one considers that most OPEC countries have budgeted for much higher oil prices for their public finances.

(click to enlarge)

You’ll notice that these prices are all significantly, sometimes dramatically, higher than what’s needed to balance their budgets. Now, many of these countries also have very generous energy subsidies on domestic oil use, supposedly to share the benefits of their resource wealth (and/or provide industry with a cost advantage).

So, there is a buffer as these subsidies can be wound down relatively painless. Some of these countries also have other buffers, like sovereign wealth funds or foreign currency reserves. And there is often no immediate reason for public budgets to be balanced.

But to suggest, as this article is doing, that OPEC is winning the war is short-sighted.

Conclusion

While doing damage to individual American shale oil producers and limiting its expansion, the simple reality is that for a host of reasons discussed above, OPEC can’t beat American shale oil production unless it is willing to accept $40 oil indefinitely. While some OPEC countries might still produce profitably at these levels, the damage to all OPEC economies will be immense, so, we can’t really see this as a realistic scenario in any way.