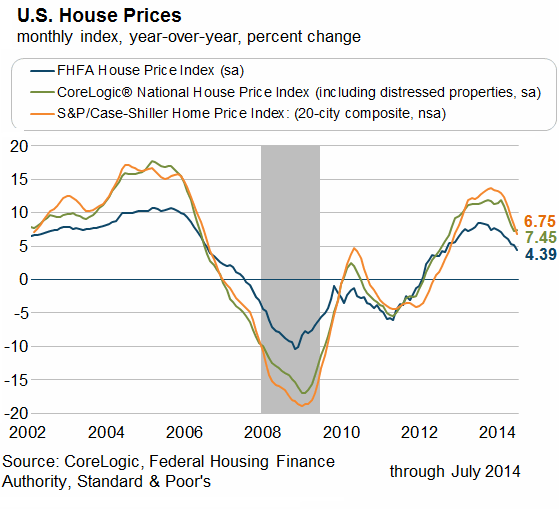

Despite an improving job market and low interest rates, the share of first-time homebuyers fell to its lowest point in nearly three decades and is preventing a healthier housing market from reaching its full potential, according to an annual survey released by the National Association of Realtors (NAR). The survey additionally found that an overwhelming majority of buyers search for homes online and then purchase their home through a real estate agent.

The 2014 NAR Profile of Home Buyers and Sellers continues a long-running series of large national NAR surveys evaluating the demographics, preferences, motivations, plans and experiences of recent home buyers and sellers; the series dates back to 1981. Results are representative of owner-occupants and do not include investors or vacation homes.

The long-term average in this survey, dating back to 1981, shows that four out of 10 purchases are from first-time home buyers. In this year’s survey, the share of first-time home buyers dropped five percentage points from a year ago to 33 percent, representing the lowest share since 1987 (30 percent).

“Rising rents and repaying student loan debt makes saving for a down payment more difficult, especially for young adults who’ve experienced limited job prospects and flat wage growth since entering the workforce,” said Lawrence Yun, NAR chief economist. “Adding more bumps in the road, is that those finally in a position to buy have had to overcome low inventory levels in their price range, competition from investors, tight credit conditions and high mortgage insurance premiums.”

Yun added, “Stronger job growth should eventually support higher wages, but nearly half (47 percent) of first-time buyers in this year’s survey (43 percent in 2013) said the mortgage application and approval process was much more or somewhat more difficult than expected. Less stringent credit standards and mortgage insurance premiums commensurate with current buyer risk profiles are needed to boost first-time buyer participation, especially with interest rates likely rising in upcoming years.”

The household composition of buyers responding to the survey was mostly unchanged from a year ago. Sixty-five percent of buyers were married couples, 16 percent single women, nine percent single men and eight percent unmarried couples.

In 2009, 60 percent of buyers were married, 21 percent were single women, 10 percent single men and 8 percent unmarried couples. Thirteen percent of survey respondents were multi-generational households, including adult children, parents and/or grandparents.

The median age of first-time buyers was 31, unchanged from the last two years, and the median income was $68,300 ($67,400 in 2013). The typical first-time buyer purchased a 1,570 square-foot home costing $169,000, while the typical repeat buyer was 53 years old and earned $95,000. Repeat buyers purchased a median 2,030-square foot home costing $240,000.

When asked about the primary reason for purchasing, 53 percent of first-time buyers cited a desire to own a home of their own. For repeat buyers, 12 percent had a job-related move, 11 percent wanted a home in a better area, and another 10 percent said they wanted a larger home. Responses for other reasons were in the single digits.

According to the survey, 79 percent of recent buyers said their home is a good investment, and 40 percent believe it’s better than stocks.

Financing the purchase Nearly nine out of 10 buyers (88 percent) financed their purchase. Younger buyers were more likely to finance (97 percent) compared to buyers aged 65 years and older (64 percent). The median down payment ranged from six percent for first-time buyers to 13 percent for repeat buyers. Among 23 percent of first-time buyers who said saving for a down payment was difficult, more than half (57 percent) said student loans delayed saving, up from 54 percent a year ago.

In addition to tapping into their own savings (81 percent), first-time homebuyers used a variety of outside resources for their loan downpayment. Twenty-six percent received a gift from a friend or relative—most likely their parents—and six percent received a loan from a relative or friend. Ten percent of buyers sold stocks or bonds and tapped into a 401(k) fund.

Ninety-three percent of entry-level buyers chose a fixed-rate mortgage, with 35 percent financing their purchase with a low-down payment Federal Housing Administration-backed mortgage (39 percent in 2013), and nine percent using the Veterans Affairs loan program with no downpayment requirements.

“FHA premiums are too high in relation to default rates and have likely dissuaded some prospective first-time buyers from entering the market,” said Yun. “To put it in perspective, 56 percent of first-time buyers used a FHA loan in 2010. The current high mortgage insurance added to their monthly payment is likely causing some young adults to forgo taking out a loan.”

Buyers used a wide variety of resources in searching for a home, with the Internet (92 percent) and real estate agents (87 percent) leading the way. Other noteworthy results included mobile or tablet applications (50 percent), mobile or tablet search engines (48 percent), yard signs (48 percent) and open houses (44 percent).

According to NAR President Steve Brown, co-owner of Irongate, Inc., Realtors® in Dayton, Ohio, although more buyers used the Internet as the first step of their search than any other option (43 percent), the Internet hasn’t replaced the real estate agent’s role in a transaction.

“Ninety percent of home buyers who searched for homes online ended up purchasing their home through an agent,” Brown said. “In fact, buyers who used the Internet were more likely to purchase their home through an agent than those who didn’t (67 percent). Realtors are not only the source of online real estate data, they also use their unparalleled local market knowledge and resources to close the deal for buyers and sellers.”

When buyers were asked where they first learned about the home they purchased, 43 percent said the Internet (unchanged from last year, but up from 36 percent in 2009); 33 percent from a real estate agent; 9 percent a yard sign or open house; six percent from a friend, neighbor or relative; five percent from home builders; three percent directly from the seller; and one percent a print or newspaper ad.

Likely highlighting the low inventory levels seen earlier in 2014, buyers visited 10 homes and typically found the one they eventually purchased two weeks quicker than last year (10 weeks compared to 12 in 2013). Overall, 89 percent were satisfied with the buying process.

First-time home buyers plan to stay in their home for 10 years and repeat buyers plan to hold their property for 15 years; sellers in this year’s survey had been in their previous home for a median of 10 years.

The biggest factors influencing neighborhood choice were quality of the neighborhood (69 percent), convenience to jobs (52 percent), overall affordability of homes (47 percent), and convenience to family and friends (43 percent). Other factors with relatively high responses included convenience to shopping (31 percent), quality of the school district (30 percent), neighborhood design (28 percent) and convenience to entertainment or leisure activities (25 percent).

This year’s survey also highlighted the significant role transportation costs and “green” features have in the purchase decision process. Seventy percent of buyers said transportation costs were important, while 86 percent said heating and cooling costs were important. Over two-thirds said energy efficient appliances and lighting were important (68 and 66 percent, respectively).

Seventy-nine percent of respondents purchased a detached single-family home, eight percent a townhouse or row house, 8 percent a condo and six percent some other kind of housing. First-time home buyers were slightly more likely (10 percent) to purchase a townhouse or a condo than repeat buyers (seven percent). The typical home had three bedrooms and two bathrooms.

The majority of buyers surveyed purchased in a suburb or subdivision (50 percent). The remaining bought in a small town (20 percent), urban area (16 percent), rural area (11 percent) or resort/recreation area (three percent). Buyers’ median distance from their previous residence was 12 miles.

Characteristics of sellers The typical seller over the past year was 54 years old (53 in 2013; 46 in 2009), was married (74 percent), had a household income of $96,700, and was in their home for 10 years before selling—a new high for tenure in home. Seventeen percent of sellers wanted to sell earlier but were stalled because their home had been worth less than their mortgage (13 percent in 2013).

“Faster price appreciation this past year finally allowed more previously stuck homeowners with little or no equity the ability to sell after waiting the last few years,” Yun said.

Sellers realized a median equity gain of $30,100 ($25,000 in 2013)—a 17 percent increase (13 percent last year) over the original purchase price. Sellers who owned a home for one year to five years typically reported higher gains than those who owned a home for six to 10 years, underlining the price swings since the recession.

The median time on the market for recently sold homes dropped to four weeks in this year’s report compared to five weeks last year, indicating tight inventory in many local markets. Sellers moved a median distance of 20 miles and approximately 71 percent moved to a larger or comparably sized home.

A combined 60 percent of responding sellers found a real estate agent through a referral by a friend, neighbor or relative, or used their agent from a previous transaction. Eighty-three percent are likely to use the agent again or recommend to others.

For the past three years, 88 percent of sellers have sold with the assistance of an agent and only nine percent of sales have been for-sale-by-owner, or FSBO sales.

For-sale-by-owner transactions accounted for 9 percent of sales, unchanged from a year ago and matching the record lows set in 2010 and 2012; the record high was 20 percent in 1987. The share of homes sold without professional representation has trended lower since reaching a cyclical peak of 18 percent in 1997.

Factoring out private sales between parties who knew each other in advance, the actual number of homes sold on the open market without professional assistance was 5 percent. The most difficult tasks reported by FSBOs are getting the right price, selling within the length of time planned, preparing or fixing up the home for sale, and understanding and completing paperwork.

NAR mailed a 127-question survey in July 2014 using a random sample weighted to be representative of sales on a geographic basis. A total of 6,572 responses were received from primary residence buyers. After accounting for undeliverable questionnaires, the survey had an adjusted response rate of 9.4 percent. The recent home buyers had to have purchased a home between July of 2013 and June of 2014. Because of rounding and omissions for space, percentage distributions for some findings may not add up to 100 percent. All information is characteristic of the 12-month period ending in June 2014 with the exception of income data, which are for 2013.

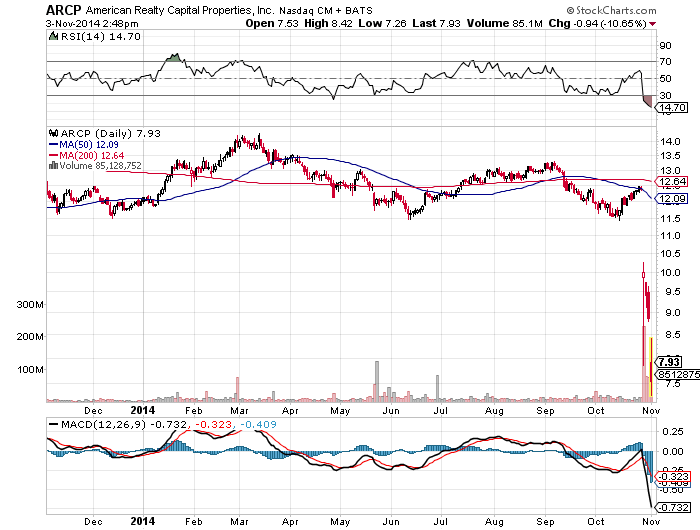

According to a Reuters report, the FBI has opened a criminal probe of American Realty Capital Properties.

This follows the disclosure of accounting errors by the company.

This investigation is in addition to a SEC inquiry.

American Realty Capital Properties (NASDAQ:ARCP) just cannot catch a break. Reuters reported that the Federal Bureau of Investigation has opened a criminal investigation into ARCP, according to their sources. The FBI is conducting the investigation along with prosecutors from U.S. Attorney Preet Bharara’s office in New York, according to the Reuters report.

This news comes just days after the company announced a series of accounting errors which had been intentionally not corrected and thus concealed from the public. The amount of money involved, roughly $9.24 million GAAP and $13.60 million AFFO, was relatively small. However, these accounting errors resulted in the resignation of two senior executives, chief financial officer, Brian Block, and chief accounting officer, Lisa McAlister.

Shares of ARCP were trading for as low as $7.85 each on Wednesday, before recovering to $10 per share after CEO David Kay held fairly well received conference call explaining what happened. In the call, Mr. Kay stressed that ARCP’s key metrics were sound. He reaffirmed that the dividend policy will not change, noting that the operating metrics were not impacted and that the NAV is unchanged at $13.25. Nevertheless, the stock continued to fall, closing the week at below $9 per share. In total, ARCP’s stock has fallen 30% since news of the accounting errors first arose, wiping out $4 billion in market value.

Conclusion:

This is quite the shocking development. Not only is the FBI looking into ARCP, but also the Securities and Exchange Commission, which announced its own investigation of the accounting errors late last week. Furthermore, the company was placed on CreditWatch with negative implications by S&P, which risks putting the credit rating into junk territory.

As I noted in my earlier article, accounting issues equal an automatic sell in my book. I sold most of my ARCP holdings on Wednesday, though I still kept some shares, opting instead to sell calls on the remaining position. I now lament that choice as I fear the stock can fall further. An FBI criminal probe is no small matter and represents a clear material risk. What an absolute disaster.

Update: American Realty Capital Properties: The Turmoil Is Only Getting Worse

ARCP sent shock waves through the analyst community last week after the REIT said its financials should no longer be relied upon and said goodbye to the CFO and CAO.

ARCP is now also attracting heat from the FBI.

In addition, RCS Capital Corporation cancels Cole Capital transaction.

Investors in American Realty Capital Properties (NASDAQ:ARCP) need to demonstrate that they have nerves of steel at the moment. After the company reported that it overstated its AFFO last week, and that its Chief Financial Officer and Chief Accounting Officer departed as a result of the accounting scandal, more bad news are seeing the light of day.

First of all, as various news outlets reported, the Federal Bureau of Investigation is putting up some additional heat on ARCP. As Reuters reported:

(Reuters) – U.S. authorities have opened a criminal probe of American Realty Capital Properties in the wake of the real estate investment trust’s disclosure that it had uncovered accounting errors, two sources familiar with the matter said on Friday.

The Federal Bureau of Investigation is conducting the investigation along with prosecutors from U.S. Attorney Preet Bharara’s office in New York, the sources said. Further details of the probe could not be learned.

The involvement of the New York U.S. Attorney’s office is particularly bad news as Preet Bharara takes a tough stance with companies that break the law or push its limits too far. While the criminal probe certainly is bad news and comes in addition to the involvement of the SEC, something else caused massive irritation among ARCP shareholders today: The Cole Capital deal with RCS Capital Corporation (NYSE: RCAP) is in real danger.

According to ARCP’s latest (and angry) press release:

In the middle of the night, we received a letter from RCS Capital Corporation purporting to terminate the equity purchase agreement, dated September 30, 2014, between RCS and an affiliate of ARCP. As we informed RCS orally and in writing over the weekend, RCS has no right and there is absolutely no basis for RCS to terminate the agreement. Therefore, RCS’s attempt to terminate the agreement constitutes a breach of the agreement. In addition, we believe that RCS’s unilateral public announcement is a violation of its agreement with ARCP. The independent members of the ARCP Board of Directors and ARCP management are evaluating all alternatives under the agreement and with respect to the Cole Capital® business, generally. ARCP management and the independent members of the ARCP Board of Directors are committed to doing what is in the best interests of ARCP stockholders and its business, including Cole Capital.

That’s right. Since the FBI now has its fingers in the pie, and the SEC, management at RCS Capital has informed ARCP that it is terminating the deal. Whatever side you are one, you’ve got to admit: American Realty Capital Properties is just falling apart.

The once mighty real estate investment trust has lost a staggering 36% of its market capitalization since shares closed at $12.38 on October 28, 2014, which is a tough pill to swallow for those investors who pledged allegiance to American Realty Capital Properties, despite the turbulence that erupted a week ago.

Technical picture Shares of American Realty Capital Properties are trading extremely weakly today in light of the new information, and I continue to see further downside potential for this REIT in the near term.

It seems as if all the forces of the universe are conspiring to bring American Realty Capital Properties down to its knees, and an investment in this REIT is not recommendable at the moment.

Source: StockCharts.com

Bottom Line: The American Realty Capital Properties’ story has gotten significantly worse today: In addition to two of the most important executives abruptly leaving the company amid an accounting scandal, the SEC and the FBI are investigating the company, lawyers are very likely going to hit ARCP with litigation, and the latest transaction is in the process of collapsing.

Bulls must either have nerves of steel or clinging to hope. In any case, ARCP’s prospects have gotten much worse today, and I continue to expect further downside potential driven by litigation concerns, potential fines and extremely negative investor sentiment.

American Realty Capital Comes Clean, And I Feel Dirty

American Realty Capital’s restatement has created rampant volatility in a stock already under the gun.

Why I decided to sell half of my position in the company.

Important portfolio takeaways for investors of all kinds.

This is one of the tougher articles I’ve written for Seeking Alpha. Asset allocation and portfolio strategy for income investors has been my focal point of writing over the past three years. I’ve always been of the opinion that talking about how to fish trumps simply giving someone fish to chew on.

Still, I mention equity-income stocks all the time in articles, but it’s rare that I write focus articles. On October third, I wrote, “American Realty Capital Properties: 30% Total Return Next Year“. Less than a month later, I find that post in an inverse position, with American Realty Capital (NASDAQ:ARCP) having dropped around 30% in market value.

First, I will tell readers that I sold a bit more than half of my position as a result of ARCP’s restatement, and still retain shares. However, it is now one of my smallest income portfolio positions and one that I have lost a majority of my conviction in. ARCP, in my mind, has transitioned from being a higher-risk investment into now becoming day-trader fodder, and at least for the near term, highly speculative. I would have been all over this thing during my trading days, but having become more conservative today with less portfolio churn, it has little room in my portfolio.

I considered all options here. I thought about increasing my position, extinguishing it altogether, selling put options at attractive premiums, or potentially doing nothing. Being so supportive of this story over the past year, I was mostly disappointed that I had to put any thought into the matter at all. For a variety of reasons, I came to the conclusion that halving the position — taking a loss, which I needed to do anyway for taxes — was a prudent near-term choice. I will revisit the decision in a month, and could conceivably buy back those shares once wash sale rules have passed.

Though selling during a period of fear and volatility is not typically in my playbook, following this restatement, I have lost confidence in this story. If you follow me, you know that I certainly identified the elevated risk that ARCP brought to real estate investors. Over the past six months, here are some comments that I made in regard to ARCP in several articles:

If you invest in ARCP today, you should expect the unexpected.

Given all the deals and potential for a misstep, there is heightened risk in owning ARCP.

But with the baggage it continues to drag along with it…..it may not necessarily be appropriate for more conservative investors

I do not consider the stock a table pounding buy.

I even compared Nick Schorsch to Monty Hall from “Let’s Make A Deal,” following the Red Lobster purchase and flip-flop on the strip mall IPO-then-sale.

As the year wore on, however, my convictions rose, since the company did not materially change its guidance to investors, despite all the acquisition activity. I figured if there were a stumble, it would have been disclosed earlier this year as the various acquisitions had time to be absorbed into operations.

While there was much criticism over the Cole quasi-divestiture to RCS and lowered guidance, I remained resolute, thinking there wasn’t another buyer, and this at least got Cole out from under the ARCP umbrella.

Of course as we now know, some financial disclosures were not to be relied upon and guidance should have been changed. If there were not so much other controversy with regard to this company, I doubt the stock would have tanked as much as it has. When you have a managerial crisis of confidence already in place and make a restatement announcement, you create panic. If we take this on face value, it does not appear to be a huge restatement, but taken in totality, this is a monumental, perhaps insurmountable, credibility problem. It’s now all aboard for the ambulance-chasing lawyers.

At this point I have decided that it is in my best interest to rip the towel in half and throw it in. I see it as a hedge against further deterioration in this story that I would not necessarily rule out given the loose management style that I and every ARCP investor knew existed.

We’re not talking about some low level accounting bean counter or paper pusher that seems to have perpetrated this; we’re talking about CFO Brian Block, assumedly someone that David Kay and Nick Schorsch had drinks with regularly. So when Kay defended the culture at ARCP on the conference call by uttering, “We don’t have bad people, we had some bad judgment there,” forgive me if I now wonder if he really has a clue how good, sweet, and honest his executives and rank-and-file workers really are. Although the restatements appear isolated to this year’s AFFO, we’ll have to see if anything turns up in 2013. While I’d like to give this company the benefit of the doubt once again, I’m finding myself staring at a slippery slope of hope that another shoe will not drop.

Still, I did not jettison the entire position because these are emotional times, and the glass-is-half-full part of me says the market is overreacting. We are, keep in mind, still talking about a high-quality portfolio of real estate, not a biotech company whose sole drug was deemed inefficacious by the FDA. In the end, however, I had to make a decision for my own portfolio that I deemed appropriate. This was it.

Meanwhile, I would not criticize nor blame someone for selling out here and moving on to more stable pastures. Fellow REIT writer Brad Thomas apparently has. On the flip side, I could see the more adventurous or those with continued conviction buying in now or upping exposure. The “right” thing to do for many investors may be to simply hold through the volatility. As I opined in a past article on ARCP:

But with the considerable sentiment overhang and “show me” attitude of the market, it could take some time and a strong stomach to see it through.

The sentiment “overhang” has basically become something much worse. And at this point I wouldn’t even want to predict how much time it could take for a rebound. Your stomach constitution will need to be stronger than I first suspected.

Portfolio Takeaways

I’ve had more than one reader tell me that the various risks I identified made them conclude that ARCP was not a stock they should own. And given what has happened here, at least for the near-term, that was obviously a prudent decision. We must all come to personal conclusions as to how much risk we are willing to take to attain income and capital growth goals.

For investors of all types, the most important thing to take away from this near-term “disaster” is that diversification and limiting position size is critical. If ARCP amounted to a couple of percent, or less, of a portfolio, the stock’s tank may not be all that impacting. If it was a more concentrated portion of the overall pie, it becomes a more painful near-term event and makes various portfolio maneuver decisions more challenging to come to.

In the end, portfolio management is a personal endeavor that amounts to an inexact science. Whether you think what I’ve done with my ARCP position is right or not is not really all important. The more important thing is whether you are comfortable with the personal portfolio decisions you make or not, why you make them, and whether they are right for your situation.

I’ve used the word “I” more than I normally would in an article. This one was indeed about me and owning up to putting wholesale trust in a management team that apparently I shouldn’t have. And it was a about a decision I really didn’t want to make as a result. Unfortunately, we have to take the bad with the good in the investment world, brush ourselves off, move on, and continue to make personal decisions that are right for our portfolios.

The excesses of 1980s New York investment banking as captured best (and with just a dose of hyperbole) by Bret Easton Ellis’s American Psycho may be long gone in the US, but they certainly are alive and well in other banking meccas, such as the one place where every financier wants to work these days (thanks to the Chinese government making it rain credit): Hong Kong. It is here that yesterday a 29-year-old British banker, Rurik Jutting, a Cambridge University grad and current Bank of America Merrill Lynch, former Barclays employee, was arrested in connection with the grisly murder of two prostitutes. One of the two victims had been hidden in a suitcase on a balcony, while the other, a foreign woman of between 25 and 30, was found lying inside the apartment with wounds to her neck and buttocks, the police said in a statement. | A spokesman for Bank of America Merrill Lynch told Reuters on Sunday that the U.S. bank had, until recently, an employee bearing the same name as a man Hong Kong media have described as the chief suspect in the double murder case. Bank of America Merrill Lynch would not give more details nor clarify when the person had left the bank.

Britain’s Foreign Office in London said on Saturday a British national had been arrested in Hong Kong, without specifying the nature of any suspected crime.

The details of the crime are straight out of American Psycho 2: the Hong Kong Sequel. One of the murdered women was aged between 25 and 30 and had cut wounds to her neck and buttock, according to a police statement. The second woman’s body, also with neck injuries, was discovered in a suitcase on the apartment’s balcony, the police said. A knife was seized at the scene.

According to the WSJ, the arrested suspect, who called police to the apartment in the early hours of Nov. 1, was until recently a Hong Kong-based employee of Bank of America Merrill Lynch.

Filings with Hong Kong’s securities regulator show that the suspect was an employee with the bank as recently as Oct. 31.The man had called police in the early hours of Saturday and asked them to investigate the case, police said.

Hong Kong’s Apple Daily newspaper said the suspect had taken about 2,000 photographs and some video footage of the victims after the killings including close-ups of their wounds. Local media said the two women were prostitutes.

The apartment where the bodies were found is on the 31st floor in a building popular with financial professionals, where average rents are about HK$30,000 (nearly $4,000) a month.

According to the Telegraph the suspect, who had previously worked at Barclays from 2008 until 2010 before moving to BofA, and specifically its Hong Kong office in July last year, had apparently vanished from his workplace a week ago. It has also been reported that he resigned from his post days before news of the murders emerged.

And as usual in situations like these, the UK’s Daily Mail has the granular details. It reports that the British banker arrested on suspicion of a double murder in Hong Kong has been identified as 29-year-old Rurik Jutting.

Mr Jutting, who attended Cambridge University, is being held by police after the bodies of two prostitutes were discovered in his up-market apartment in the early hours of yesterday morning.

Officers found the women, thought to be a 25-year-old from Indonesia and a 30-year-old from the Philippines, after Mr Jutting allegedly called police to the address, which is located near the city’s red light district. The naked body of the Filipina victim, who had suffered a series of knife wounds, was found inside the 31st-floor apartment in J Residence – a development of exclusive properties in the city’s Wan Chai district that are popular with young expatriate executives.

The second woman was reportedly discovered naked and partially decapitated in a suitcase on the balcony of the apartment. She is believed to have been tied up and to have been left there for around a week.

Sex toys and cocaine were also reportedly found, along with a knife which was seized by officers.

Mr Jutting’s phone is today being examined by police in a bid to identify possible further victims, according to the South China Morning Post.

It is understood that photos of the woman who was found in the suitcase, apparently taken after she died, were among roughly 2,000 that officers found on the device.

Mr Jutting attended Winchester College, an independent boys school in Hampshire, before continuing his studies in history and law at Pembroke College, Cambridge, where he became secretary of the history society.

He appears to have worked at Barclays in London between 2008 and 2010, when he took a job with Bank of America Merrill Lynch. He was moved to the bank’s Hong Kong office in July last year.

A spokesman for Bank of America Merrill Lynch confirmed that it had previously employed a man by the same name but would not give more details nor clarify when the person had left the bank.

CCTV footage from the apartment block, located near Hong Kong’s red light district, showed the banker and the Filipina woman returning to the 31st floor shortly after midnight local time yesterday.

He allegedly called police to his home at 3.42am, shortly after the woman he was seen with is believed to have been killed.

She was found with two wounds to her neck and her throat had been slashed. She was pronounced dead at the scene.

The body on the balcony, wrapped in a carpet and inside a black suitcase, which measured about three feet by 18 inches, was not found by police until eight hours later.

A police source quoted by the South China Morning Post said: ‘She was nearly decapitated and her hands and legs were bound with ropes. ‘She was naked and wrapped in a towel before being stuffed into the suitcase. Her passport was found at the scene.’

Wan Chai, the district where the apartment is located, is known for its bustling nightclub scene of ‘girly bars,’ popular with expatriate men and staffed by sex workers from South East Asia. Police have today been contacting nearby bars in an attempt to find out more about the background of the two murdered women.

One resident in the 40-storey block, where most of the residents are expatriates, said he had noticed an unusual smell in recent days. He told the South China Morning Post that there had been ‘a stink in the building like a dead animal’.

And just like that, the worst excesses of the “peak banking” days from 1980, when sad scenes like these were a frequent occurrence, are back.

Government workers remove the body of a woman who was found dead at a flat in Hong Kong’s Wan chai district in the early hours of this morning. A British man was been arrested in connection with the murders.

A second victim was found stuffed inside a suitcase on the balcony of the residential flat in Hong Kong

The 40-storey J Residence is reportedly a high-end development favored by junior expatriate bankers

Bank Of America Psycho Killer Was Busy Helping Hedge Funds Avoid Taxes During His Business Hours

The most bizarre story of the weekend was that of Bank of America’s 29-year-old banker Rurik Jutting, who shortly after allegedly killing two prostitutes (and stuffing one in a suitcase), called the cops on himself and effectively admitted to the crime having left a quite clear autoreply email message, namely “For urgent inquiries, or indeed any inquiries, please contact someone who is not an insane psychopath. For escalation please contact God, though suspect the devil will have custody. [Last line only really worked if I had followed through..]”

But while his attempt to imitate Patrick Bateman did not go unnoticed, even if it will be promptly forgotten until the next grotesquely insane banker shocks the world for another 15 minutes, the question that has remained unanswered is what did young Master Jutting do when not chopping women up.

The answer, as the WSJ has revealed, is just as unsavory: “he had been part of a Bank of America team that specialized in tax-minimization trades that are under scrutiny from prosecutors, regulators, tax collectors and the bank’s own compliance department, according to people familiar with the matter and documents reviewed by The Wall Street Journal.”

Basically, when not acting as a homicidal psychopath, Jutting was facilitating full-blown tax evasion, just the activity that every developed, and thus broke, government around the globe is desperately cracking down on, and why every single Swiss bank is non-grata in the US and may be arrested immediately upon arrival on US soil.

Mr. Jutting, a U.K. native and a competitive poker player, worked in Bank of America Merrill Lynch’s Structured Equity Finance and Trading group, first in London and then in Hong Kong, according to these people and regulatory filings. Mr. Jutting resigned from the bank sometime before Oct. 27, which police say was the date of the first murder, according to a person familiar with the matter.

The trading group, known as SEFT, employs about three dozen people globally, one of these people said. It helps hedge funds and other clients manage their stock portfolios, often through the use of derivatives, according to the people and internal bank documents.

Mr. Jutting joined Bank of America in 2010 and worked three years in its London office, the bank’s hub for dividend-arbitrage trades, the people familiar with the matter say. He moved to Bank of America’s Hong Kong office in July 2013.

Ironic, because it was just this summer that a Congressional panel headed by Carl Levin was tearing foreign banks Deutsche Bank and Barclays a new one for providing structures such as MAPS and COLT, which did precisely this: give clients a derivative-based means of avoiding taxation (as described in “How Rentec Made More Than 34 Billion In Profits Since 1998 “Fictional Derivatives“).

As it turns out not only did a US-based bank – Bank of America – have an entire group dedicated to precisely the same type of hedge fund, and other Ultra High Net Worth, clients tax evasion advice, but it also housed a homicidal psychopath.

Perhaps if instead Levin had been grandstanding and seeking to punish foreign banks, he had cracked down on everyone who was providing this service, Jutting’s group would have been disbanded long ago, and two innocent lives could have been saved, instead allowing the alleged cocaine-snorting murderer to engage in far more wholesome, banker-approrpriate activities:

During his time in Asia, Mr. Jutting’s pastimes apparently included gambling. In a Sept. 14 Facebook post, he boasted of winning thousands of dollars playing poker at a tournament in the Philippines. He signed off the post: “God I love Manila.” The comment drew eight “likes.”

Alas one will never know “what if.”

But we are certain that with none other than America’s most prominent bank, the one carrying its name, has now been busted for aiding and abetting hedge fund tax evasion around the globe, it will get the same treatment as evil foreign banks Barclays and Deutsche Bank, right Carl Levin?

When it comes to Internet speeds, the U.S. lags behind much of the developed world.

That’s one of the conclusions from a new report by the Open Technology Institute at the New America Foundation, which looked at the cost and speed of Internet access in two dozen cities around the world.

Clocking in at the top of the list was Seoul, South Korea, where Internet users can get ultra-fast connections of roughly 1000 megabits per second for just $30 a month. The same speeds can be found in Hong Kong and Tokyo for $37 and $39 per month, respectively.

For comparison’s sake, the average U.S. connection speed stood at 9.8 megabits per second as of late last year, according to Akamai Technologies.

Residents of New York, Los Angeles and Washington, D.C. can get 500-megabit connections thanks to Verizon, though they come at a cost of $300 a month.

There are a few cities in the U.S. where you can find 1000-megabit connections. Chattanooga, Tenn., and Lafayette, La. have community-owned fiber networks, and Google has deployed a fiber network in Kansas City. High-speed Internet users in Chattanooga and Kansas City pay $70, while in Lafayette, it’s $110.

The problem with fiber networks is that they’re hugely expensive to install and maintain, requiring operators to lay new wiring underground and link it to individual homes. Many smaller countries with higher population density have faster average speeds than the United States.

“Especially in the U.S., many of the improved plans are at the higher speed tiers, which generally are the most expensive plans available,” the report says. “The lower speed packages—which are often more affordable for the average consumer—have not seen as much of an improvement.”

Google is exploring plans to bring high-speed fiber networks to a handful of other cities, and AT&T has also built them out in a few places, but it will be a long time before 1000-megabit speeds are an option for most Americans.

For the second straight month, Midland posted the third lowest unemployment rate in the nation, according to figures released Wednesday by the Bureau of Labor Statistics.

Bismarck, North Dakota, topped the list for the fourth straight month with a jobless rate of 2.1 percent. Fargo, North Dakota, was second at 2.3. Midland and Logan, Utah, tied for third at 2.6.

A total of 10 metropolitan statistical areas around the nation posted unemployment rates of 3.0 percent or lower. Midland was the lone MSA in Texas at or below 3.0.

Midland again ranked near the top of the list of MSAs in the nation when it came to percentage gain in employment. Midland’s 6.4 percent growth ranked second to Muncie, Indiana (8.9 percent). In September, Midland showed a work force 100,100, an increase of nearly 5,000 from September 2013.

The following are the lowest unemployment rates in the nation during the month of September, according to the Bureau of Labor Statistics.

Bismarck, North Dakota 2.1

Fargo, North Dakota 2.3

Midland 2.6

Logan, Utah 2.6

Sioux Falls, South Dakota 2.7

Grand Forks, North Dakota 2.8

Lincoln, Nebraska 2.8

Mankato, Minnesota 2.9

Rapid City, South Dakota 2.9

Billings, Montana 3.0

Lowest rates from August

Bismarck, North Dakota 2.2, Fargo North Dakota 2.4; Midland 2.8. Also: Odessa 3.4

July

Bismarck, North Dakota, 2.4; Sioux Falls, South Dakota, 2.7; Fargo, North Dakota, 2.8; Midland 2.9. Also: Odessa 3.6

June

Bismarck, North Dakota, 2.6, Midland 2.9, Fargo, North Dakota, 3.0. Also: Odessa 3.6

May

Bismarck, North Dakota, 2.2, Fargo, North Dakota, 2.5, Logan, Utah, 2.5, Midland 2.6. Also: Odessa 3.2

If you really would rather own the property than the note, take a few lessons in fraud from Owen Financial Corp. According to allegations from New York’s financial regulator, Benjamin Lawsky, the lender sent “thousands” of foreclosure “warnings” to borrowers months after the window of time had lapsed during which they could have saved their homes[1]. Lawskey alleges that many of the letters were even back-dated to give the impression that they had been sent in a timely fashion. “In many cases, borrowers received a letter denying a mortgage loan modification, and the letter was dated more than 30 days prior to the date that Ocwen mailed the letter.”

The correspondence gave borrowers 30 days from the date of the denial letter to appeal, but the borrowers received the letters after more than 30 days had passed. The issue is not a small one, either. Lawskey says that a mortgage servicing review at Ocwen revealed “more than 7,000” back-dated letters.”

In addition to the letters, Ocwen only sent correspondence concerning default cures after the cure date for delinquent borrowers had passed and ignored employee concerns that “letter-dating processes were inaccurate and misrepresented the severity of the problem.” While Lawskey accused Ocwen of cultivating a “culture that disregards the needs of struggling borrowers,” Ocwen itself blamed “software errors” for the improperly-dated letters[2]. This is just the latest in a series of troubles for the Atlanta-based mortgage servicer; The company was also part the foreclosure fraud settlement with 49 of 50 state attorneys general and recently agreed to reduce many borrowers’ loan balances by $2 billion total.

Most people do not realize that Ocwen, although the fourth-largest mortgage servicer in the country, is not actually a bank. The company specializes specifically in servicing high-risk mortgages, such as subprime mortgages. At the start of 2014, it managed $106 billion in subprime loans. Ocwen has only acknowledged that 283 New York borrowers actually received improperly dated letters, but did announce publicly in response to Lawskey’s letter that it is “investigating two other cases” and cooperating with the New York financial regulator.

WHAT WE THINK: While it’s tempting to think that this is part of an overarching conspiracy to steal homes in a state (and, when possible, a certain enormous city) where real estate is scarce, in reality the truth of the matter could be even more disturbing: Ocwen and its employees just plain didn’t care. There was a huge, problematic error that could have prevented homeowners from keeping their homes, but the loan servicer had already written off the homeowners as losers in the mortgage game. A company that services high-risk loans likely has a jaded view of borrowers, but that does not mean that the entire culture of the company should be based on ignoring borrowers’ rights and the vast majority of borrowers who want to keep their homes and pay their loans. Sure, if you took out a mortgage then you have the obligation to pay even if you don’t like the terms anymore. On the other side of the coin, however, your mortgage servicer has the obligation to treat you like someone who will fulfill their obligations rather than rigging the process so that you are doomed to fail.

Do you think Lawskey is right about Ocwen’s “culture?” What should be done to remedy this situation so that note investors and homeowners come out of it okay?

Thank you for reading the Bryan Ellis Investing Letter!

— Ocwen posts open letter and apology to borrowers Pledges independent investigation and rectification October 27, 2014 10:37AM

Ocwen Financial (OCN) has taken a beating after the New York Department of Financial Services sent a letter to the company on Oct. 21 alleging that the company had been backdating letters to borrowers, and now Ocwen is posting an open letter to homeowners.

Ocwen CEO Ron Faris writes to its clients explaining what happened and what steps the company is taking to investigate the issue, identify any problems, and rectify the situation.

Click here to read the full text of the letter.

“At Ocwen, we take our mission of helping struggling borrowers very seriously, and if you received one of these incorrectly-dated letters, we apologize. I am writing to clarify what happened, to explain the actions we have taken to address it, and to commit to ensuring that no borrower suffers as a result of our mistakes,” he writes.

“Historically letters were dated when the decision was made to create the letter versus when the letter was actually created. In most instances, the gap between these dates was three days or less,” Faris writes. “In certain instances, however, there was a significant gap between the date on the face of the letter and the date it was actually generated.”

Faris says that Ocwen is investigating all correspondence to determine whether any of it has been inadvertently misdated; how this happened in the first place; and why it took so long to fix it. He notes that Ocwen is hiring an independent firm to conduct the investigation, and that it will use its advisory council comprised of 15 nationally recognized community advocates and housing counselors.

“We apologize to all borrowers who received misdated letters. We believe that our backup checks and controls have prevented any borrowers from experiencing a foreclosure as a result of letter-dating errors. We will confirm this with rigorous testing and the verification of the independent firm,” Faris writes. “It is worth noting that under our current process, no borrower goes through a foreclosure without a thorough review of his or her loan file by a second set of eyes. We accept appeals for modification denials whenever we receive them and will not begin foreclosure proceedings or complete a foreclosure that is underway without first addressing the appeal.”

Faris ends by saying that Ocwen is committed to keeping borrowers in their homes.

“Having potentially caused inadvertent harm to struggling borrowers is particularly painful to us because we work so hard to help them keep their homes and improve their financial situations. We recognize our mistake. We are doing everything in our power to make things right for any borrowers who were harmed as a result of misdated letters and to ensure that this does not happen again,” he writes.

Last week the fallout from the “Lawsky event” – so called because of NYDFS Superintendent Benjamin Lawsky – came hard and fast.

Compass Point downgraded Ocwen affiliate Home Loan Servicing Solutions (HLSS) from Buy to Neutral with a price target of $18.

Meanwhile, Moody’s Investors Service downgraded Ocwen Loan Servicing LLC’s servicer quality assessments as a primary servicer of subprime residential mortgage loans to SQ3 from SQ3+ and as a special servicer of residential mortgage loans to SQ3 from SQ3+.

Standard & Poor’s Ratings Services lowered its long-term issuer credit rating to ‘B’ from ‘B+’ on Ocwen on Wednesday and the outlook is negative.

—- Ocwen Writes Open Letter to Homeowners Concerning Letter Dating Issues October 24, 2014

Dear Homeowners,

In recent days you may have heard about an investigation by the New York Department of Financial Services’ (DFS) into letters Ocwen sent to borrowers which were inadvertently misdated. At Ocwen, we take our mission of helping struggling borrowers very seriously, and if you received one of these incorrectly-dated letters, we apologize. I am writing to clarify what happened, to explain the actions we have taken to address it, and to commit to ensuring that no borrower suffers as a result of our mistakes.

What Happened Historically letters were dated when the decision was made to create the letter versus when the letter was actually created. In most instances, the gap between these dates was three days or less. In certain instances, however, there was a significant gap between the date on the face of the letter and the date it was actually generated.

What We Are Doing We are continuing to investigate all correspondence to determine whether any of it has been inadvertently misdated; how this happened in the first place; and why it took us so long to fix it. At the end of this exhaustive investigation, we want to be absolutely certain that we have fixed every problem with our letters. We are hiring an independent firm to investigate and to help us ensure that all necessary fixes have been made.

Ocwen has an advisory council made up of fifteen nationally recognized community advocates and housing counsellors. The council was created to improve our borrower outreach to keep more people in their homes. We will engage with council members to get additional guidance on making things right for any borrowers who may have been affected in any way by this error.

We apologize to all borrowers who received misdated letters. We believe that our backup checks and controls have prevented any borrowers from experiencing a foreclosure as a result of letter-dating errors. We will confirm this with rigorous testing and the verification of the independent firm. It is worth noting that under our current process, no borrower goes through a foreclosure without a thorough review of his or her loan file by a second set of eyes. We accept appeals for modification denials whenever we receive them and will not begin foreclosure proceedings or complete a foreclosure that is underway without first addressing the appeal.

In addition to these efforts we are committed to cooperating with DFS and all regulatory agencies.

We Are Committed to Keeping Borrowers in Their Homes Having potentially caused inadvertent harm to struggling borrowers is particularly painful to us because we work so hard to help them keep their homes and improve their financial situations. We recognize our mistake. We are doing everything in our power to make things right for any borrowers who were harmed as a result of misdated letters and to ensure that this does not happen again. We remain deeply committed to keeping borrowers in their homes because we believe it is the right thing to do and a win/win for all of our stakeholders.

We will be in further communication with you on this matter.

Sincerely, Ron Faris CEO

YOU DECIDE — Ocwen Downgrade Puts RMBS at Risk

Moody’s and S&P downgraded Ocwen’s servicer quality rating last week after the New York Department of Financial Services made “backdating” allegations. Barclays says the downgrades could put some RMBS at risk of a servicer-driven default.

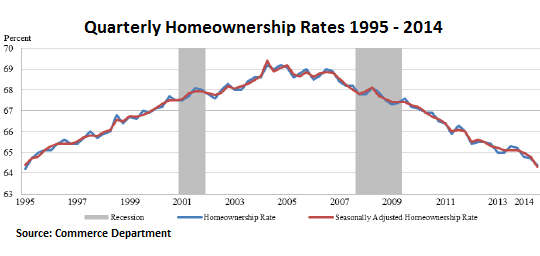

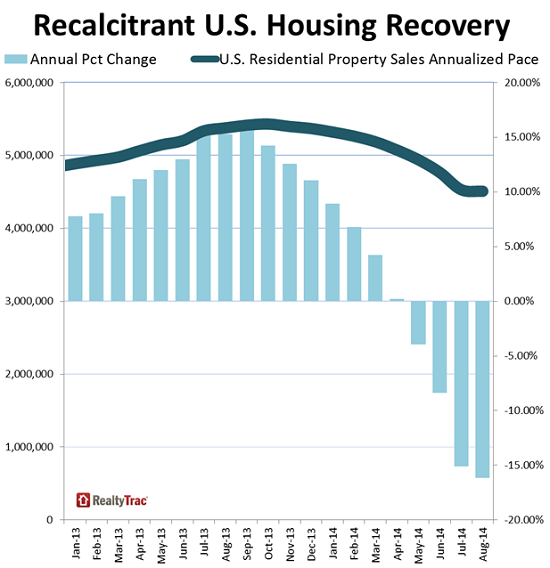

The quintessential ingredient in the stew that makes up a thriving housing market has been evaporating in America. And a recent phenomenon has taken over: private equity firms, REITs, and other Wall-Street funded institutional investors have plowed the nearly free money the Fed has graciously made available to them since 2008 into tens of thousands of vacant single-family homes to rent them out. And an apartment building boom has offered alternatives too.

Since the Fed has done its handiwork, institutional investors have driven up home prices and pushed them out of reach for many first-time buyers, and these potential first-time buyers are now renting homes from investors instead. Given the high home prices, in many cases it may be a better deal. And apartments are often centrally located, rather than in some distant suburb, cutting transportation time and expenses, and allowing people to live where the urban excitement is. Millennials have figured it out too, as America is gradually converting to a country of renters.

So in its inexorable manner, home ownership has continued to slide in the third quarter, according to the Commerce Department. Seasonally adjusted, the rate dropped to 64.3% from 64.7 in the prior quarter. It was the lowest rate since Q4 1994 (not seasonally adjusted, the rate dropped to 64.4%, the lowest since Q1 1995).

This is what that relentless slide looks like:

Home ownership since 2008 dropped across all age groups. But the largest drops occurred in the youngest age groups. In the under-35 age group, where first-time buyers are typically concentrated, home ownership has plunged from 41.3% in 2008 to 36.0%; and in the 35-44 age group, from 66.7% to 59.1%, with a drop of over a full percentage point just in the last quarter – by far the steepest.

Home ownership, however, didn’t peak at the end of the last housing bubble just before the financial crisis, but in 2004 when it reached 69.2%. Already during the housing bubble, speculative buying drove prices beyond the reach of many potential buyers who were still clinging by their fingernails to the status of the American middle class … unless lenders pushed them into liar loans, a convenient solution many lenders perfected to an art.

It was during these early stages of the housing bubble that the concept of “home” transitioned from a place where people lived and thrived or fought with each other and dealt with onerous expenses and responsibilities to a highly leveraged asset for speculators inebriated with optimism, an asset to be flipped willy-nilly and laddered ad infinitum with endless amounts of cheaply borrowed money. And for some, including the Fed it seems, that has become the next American dream.

Despite low and skidding home ownership rates, home prices have been skyrocketing in recent years, and new home prices have reached ever more unaffordable all-time highs.

One of the most surprising developments in the aftermath of the housing crisis is the sharp rise in apartment building construction. Evidently post-recession Americans would rather rent apartments than buy new houses.

When I noticed this trend, I wanted to see what was behind the numbers.

Is it possible Americans are giving up on the idea of home ownership, the very staple of the American dream? Now that would be a good story.

What I found was less extreme but still interesting: The American dream appears merely to be on hold.

Economists told me that many potential home buyers can’t get a down payment together because the recession forced them to chip away at their savings. Others have credit stains from foreclosures that will keep them out of the mortgage market for several years.

More surprisingly, it turns out that the millennial generation is a driving force behind the rental boom. Young adults who would have been prime candidates for first-time home ownership are busy delaying everything that has to do with becoming a grown-up. Many even still live at home, but some data shows they are slowly beginning to branch out and find their own lodgings — in rental apartments.

A quick Internet search for new apartment complexes suggests that developers across the country are seizing on this trend and doing all they can to appeal to millennials. To get a better idea of what was happening, I arranged a tour of a new apartment complex in suburban Washington that is meant to cater to the generation.

What I found made me wish I was 25 again. Scented lobbies crammed with funky antiques that led to roof decks with outdoor theaters and fire pits. The complex I visited offered Zumba classes, wine tastings, virtual golf and celebrity chefs who stop by to offer cooking lessons.

“It’s like an assisted-living facility for young people,” the photographer accompanying me said.

Economists believe that the young people currently filling up high-amenity rental apartments will eventually buy homes, and every young person I spoke with confirmed that this, in fact, was the plan. So what happens to the modern complexes when the 20-somethings start to buy homes? It’s tempting to envision ghost towns of metal and pipe wood structures with tumbleweeds blowing through the lobbies. But I’m sure developers will rehabilitate them for a new demographic looking for a renter’s lifestyle.

We have a very serious problem with Hillary. I was asked years ago to review Hillary’sCommodity Tradingto explain what went on. Effectively, they did trades and simply put winners in her account and the losers in her lawyer’s. This way she gets money that is laundered through the markets – something that would get her 25 years today.People forget, but Hillary was really President – not Bill. Just 4 days after taking office, Hillary was given the authority to start a task force for healthcare reform. The problem was, her vision was unbelievable. The costs upon business were oppressive so much so that not even the Democrats could support her. When asked how was a small business mom and pop going to pay for healthcare she said “if they could not afford it they should not be in business.” From that moment on, my respect for her collapsed. She revealed herself as a real Marxist.Now, that she can taste the power of Washington, and I dare say she will not be a yes person as Obama and Bush seem to be, therein lies the real danger. Giving her the power of dictator, which is the power of executive orders, I think I have to leave the USA just to be safe.Hillaryhas stated when she ran the White Housebefore regarding her idea of healthcare, “We can’t afford to have that money go to the private sector. The money has to go to the federal government because the federal government will spend that money better than the private sector will spend it.” When has that ever happened?

Hillary believes in government at the expense of the people. I do not say this lightly, because here she goes again. She just appeared at aBoston rallyfor Democrat gubernatorial candidate Martha Coakley on Friday. She was off the hook and amazingly told the crowd gathered at the Park Plaza Hotel not to listen to anybody who says that “businesses create jobs.”“Don’t let anybody tell you it’s corporations and businesses that create jobs,” Clinton said.“You know that old theory, ‘trickle-down economics,’” she continued. “That has been tried, that has failed. It has failed rather spectacularly.”“You know, one of the things my husband says when people say ‘Well, what did you bring to Washington,’ he said, ‘Well, I brought arithmetic,” Hillary said.

I wrote anOp-Ed for the Wall Street Journalon Clinton’s Balanced Budget. It was smoke and mirrors. Long-term interest rates were sharply higher than short-term. Clinton shifted the national debt to save interest expenditures. He also inherited a up-cycle in the economy that always produces more taxes.Yet she sees no problem with the math of perpetually borrowing. Perhaps she would get to the point of being unable to sell debt and just confiscate all wealth since government knows better.

Here’s a shocker or is it? Take the quiz and then check your answers at the bottom. Then take action!!!

And, no, the answers to these questions aren’t all “Barack Obama”!

1) “We’re going to take things away from you on behalf of the common good.” A. Karl Marx

B. Adolph Hitler

C. Joseph Stalin D. Barack Obama

E. None of the above

2) “It’s time for a new beginning, for an end to government of the few, by the few, and for the few…… And to replace it with shared responsibility, for shared prosperity.” A. Lenin

B. Mussolini

C. Idi Amin

D. Barack Obama E. None of the above

3) “(We)…..can’t just let business as usual go on, and that means something has to be taken away from some people.” A. Nikita Khrushchev

B. Joseph Goebbels

C. Boris Yeltsin D. Barack Obama

E. None of the above

4) “We have to build a political consensus and that requires people to give up a little bit of their own … in order to create this common ground.” A. Mao Tse Tung

B. Hugo Chavez

C. Kim Jong II D. Barack Obama

E. None of the above

5) “I certainly think the free-market has failed.” A. Karl Marx

B. Lenin

C. Molotov

D. Barack Obama E. None of the above

6) “I think it’s time to send a clear message to what has become the most profitable sector in (the) entire economy that they are being watched.” A. Pinochet

B. Milosevic

C. Saddam Hussein D. Barack Obama

E. None of the above

and the answers are ~~~~~~~~~~~~~

(1) E. None of the above. Statement was made by Hillary Clinton 6/29/2004 (2) E. None of the above. Statement was made by Hillary Clinton 5/29/2007 (3) E. None of the above. Statement was made by Hillary Clinton 6/4/2007 (4) E. None of the above. Statement was made by Hillary Clinton 6/4/2007 (5) E. None of the above. Statement was made by Hillary Clinton 6/4/2007 (6) E. None of the above. Statement was made by Hillary Clinton 9/2/2005

Want to know something scary? She may be the next POTUS.

House flippers buy run-down properties, fix them up and resell them quickly at a higher price. Above, a home under renovation in Amsterdam, N.Y. (Mike Groll / Associated Press)

Can you still do a short-term house flip using federally insured, low-down payment mortgage money? That’s an important question for buyers, sellers, investors and realty agents who’ve taken part in a nationwide wave of renovations and quick resales using Federal Housing Administration-backed loans during the last four years.

The answer is yes: You can still flip and finance short term. But get your rehabs done soon. The federal agency whose policy change in 2010 made tens of thousands of quick flips possible — and helped large numbers of first-time and minority buyers with moderate incomes acquire a home — is about to shut down the program, FHA officials confirmed to me.

In an effort to stimulate repairs and sales in neighborhoods hard hit by the mortgage crisis and recession, the FHA waived its standard prohibition against financing short-term house flips. Before the policy change, if you were an investor or property rehab specialist, you had to own a house for at least 90 days before reselling — flipping it — to a new buyer at a higher price using FHA financing. Under the waiver of the rule, you could buy a house, fix it up and resell it as quickly as possible to a buyer using an FHA mortgage — provided that you followed guidelines designed to protect consumers from being ripped off with hyper-inflated prices and shoddy construction.

Since then, according to FHA estimates, about 102,000 homes have been renovated and resold using the waiver. The reason for the upcoming termination: The program has done its job, stimulated billions of dollars of investments, stabilized prices and provided homes for families who were often newcomers to ownership.

However, even though the waiver program has functioned well, officials say, inherent dangers exist when there are no minimum ownership periods for flippers. In the 1990s, the FHA witnessed this firsthand when teams of con artists began buying run-down houses, slapped a little paint on the exterior and resold them within days — using fraudulent appraisals — for hyper-inflated prices and profits. Their buyers, who obtained FHA-backed mortgages, often couldn’t afford the payments and defaulted. Sometimes the buyers were themselves part of the scam and never made any payments on their loans — leaving the FHA, a government-owned insurer, with steep losses.

For these reasons, officials say, it’s time to revert to the more restrictive anti-quick-flip rules that prevailed before the waiver: The 90-day standard will come back into effect after Dec. 31.

But not everybody thinks that’s a great idea. Clem Ziroli Jr., president of First Mortgage Corp., an FHA lender in Ontario, says reversion to the 90-day rule will hurt moderate-income buyers who found the program helpful in opening the door to home ownership.

“The sad part,” Ziroli said in an email, “is the majority of these properties were improved and [located] in underserved areas. Having a rehabilitated house available to these borrowers” helped them acquire houses that had been in poor physical shape but now were repaired, inspected and safe to occupy.

Paul Skeens, president of Colonial Mortgage in Waldorf, Md., and an active rehab investor in the suburbs outside Washington, D.C., said the upcoming policy change will cost him money and inevitably raise the prices of the homes he sells after completing repairs and improvements. Efficient renovators, Skeens told me in an interview, can substantially improve a house within 45 days, at which point the property is ready to list and resell. By extending the mandatory ownership period to 90 days, the FHA will increase Skeens’ holding costs — financing expenses, taxes, maintenance and utilities — all of which will need to be added onto the price to a new buyer.

Paul Wylie, a member of an investor group in the Los Angeles area, says he sees “more harm than good by not extending the waiver. There are protections built into the program that have served [the FHA] well,” he said in an email. If the government reimposes the 90-day requirement, “it will harm those [buyers] that FHA intends to help” with its 3.5% minimum-down-payment loans. “Investors will adapt and sell to non-FHA-financed buyers. Entry-level consumers will be harmed unnecessarily.”

Bottom line: Whether fix-up investors like it or not, the FHA seems dead set on reverting to its pre-bust flipping restrictions. Financing will still be available, but selling prices of the end product — rehabbed houses for moderate-income buyers — are almost certain to be more expensive.

The slump in the oil price is primarily a result of extreme short positioning, a headline-driven anxiety and overblown fears about the global economy.

This is a temporary dip and the oil markets will recover significantly by H1 2015.

Now is the time to pick the gold nuggets out of the ashes and wait to see them shine again.

Nevertheless, the sky is not blue for several energy companies and the drop of the oil price will spell serious trouble for the heavily indebted oil producers.

Introduction:

It has been a very tough market out there over the last weeks. And the energy stocks have been hit the hardest over the last five months, given that most of them have returned back to their H2 2013 levels while many have dropped even lower down to their H1 2013 levels.

But one of my favorite quotes is Napoleon’s definition of a military genius: “The man who can do the average thing when all those around him are going crazy.” To me, you don’t have to be a genius to do well in investing. You just have to not go crazy when everyone else is.

In my view, this slump of the energy stocks is a deja-vu situation, that reminded me of the natural gas frenzy back in early 2014, when some fellow newsletter editors and opinion makers with appearances on the media (i.e. CNBC, Bloomberg) were calling for $8 and $10 per MMbtu, trapping many investors on the wrong side of the trade. In contrast, I wrote a heavily bearish article on natural gas in February 2014, when it was at $6.2/MMbtu, presenting twelve reasons why that sky high price was a temporary anomaly and would plunge very soon. I also put my money where my mouth was and bought both bearish ETFs (NYSEARCA:DGAZ) and (NYSEARCA:KOLD), as shown in the disclosure of that bearish article. Thanks to these ETFs, my profits from shorting the natural gas were quick and significant.

This slump of the energy stocks also reminded me of those analysts and investors who were calling for $120/bbl and $150/bbl in H1 2014. Even T. Boone Pickens, founder of BP Capital Management, told CNBC in June 2014 that if Iraq’s oil supply goes offline, crude prices could hit $150-$200 a barrel.

But people often go to the extremes because this is the human nature. But shrewd investors must exploit this inherent weakness of human nature to make easy money, because factory work has never been easy.

Let The Charts And The Facts Speak For Themselves

The chart for the bullish ETF (NYSEARCA:BNO) that tracks Brent is illustrated below:

And the charts for the bullish ETFs (NYSEARCA:USO), (NYSEARCA:DBO) and (NYSEARCA:OIL) that track WTI are below:

and below:

and below:

For the risky investors, there is the leveraged bullish ETF (NYSEARCA:UCO), as illustrated below:

It is clear that these ETFs have returned back to their early 2011 levels amid fears for oversupply and global economy worries. Nevertheless, the recent growth data from the major global economies do not look bad at all.

In China, things look really good. The Chinese economy grew 7.3% in Q3 2014, which is way far from a hard-landing scenario that some analysts had predicted, and more importantly the Chinese authorities seem to be ready to step in with major stimulus measures such as interest rate cuts, if needed. Let’s see some more details about the Chinese economy:

1) Exports rose 15.3% in September from a year earlier, beating a median forecast in a Reuters poll for a rise of 11.8% and quickening from August’s 9.4% rise.

2) Imports rose 7% in terms of value, compared with a Reuters estimate for a 2.7% fall.

3) Iron ore imports rebounded to the second highest this year and monthly crude oil imports rose to the second highest on record.

4) China posted a trade surplus of $31.0 billion in September, down from $49.8 billion in August.

Beyond the encouraging growth data coming from China (the second largest oil consumer worldwide), the US economy grew at a surprising 4.6% rate in Q2 2014, which is the fastest pace in more than two years.

Meanwhile, the Indian economy picked up steam and rebounded to a 5.7% rate in Q2 2014 from 4.6% in Q1, led by a sharp recovery in industrial growth and gradual improvement in services. And after overtaking Japan as the world’s third-biggest crude oil importer in 2013, India will also become the world’s largest oil importer by 2020, according to the US Energy Information Administration (EIA).

The weakness in Europe remains, but this is nothing new over the last years. And there is a good chance Europe will announce new economic policies to boost the economy over the next months. For instance and based on the latest news, the European Central Bank is considering buying corporate bonds, which is seen as helping banks free up more of their balance sheets for lending.

All in all, and considering the recent growth data from the three biggest oil consumers worldwide, I get the impression that the global economy is in a better shape than it was in early 2011. On top of that, EIA forecasts that WTI and Brent will average $94.58 and $101.67 respectively in 2015, and obviously I do not have any substantial reasons to disagree with this estimate.

The Reasons To Be Bullish On Oil Now

When it comes to investing, timing matters. In other words, a lucrative investment results from a great entry price. And based on the current price, I am bullish on oil for the following reasons:

1) Expiration of the oil contracts: They expired last Thursday and the shorts closed their bearish positions and locked their profits.

2) Restrictions on US oil exports: Over the past three years, the average price of WTI oil has been $13 per barrel cheaper than the international benchmark, Brent crude. That gives large consumers of oil such as refiners and chemical companies a big cost advantage over foreign rivals and has helped the U.S. become the world’s top exporter of refined oil products.

Given that the restrictions on US oil exports do not seem to be lifted anytime soon, the shale oil produced in the US will not be exported to impact the international supply/demand and lower Brent price in the short-to-medium term.

3)The weakening of the U.S. dollar: The U.S. dollar rose significantly against the Euro over the last months because of a potential interest rate hike.

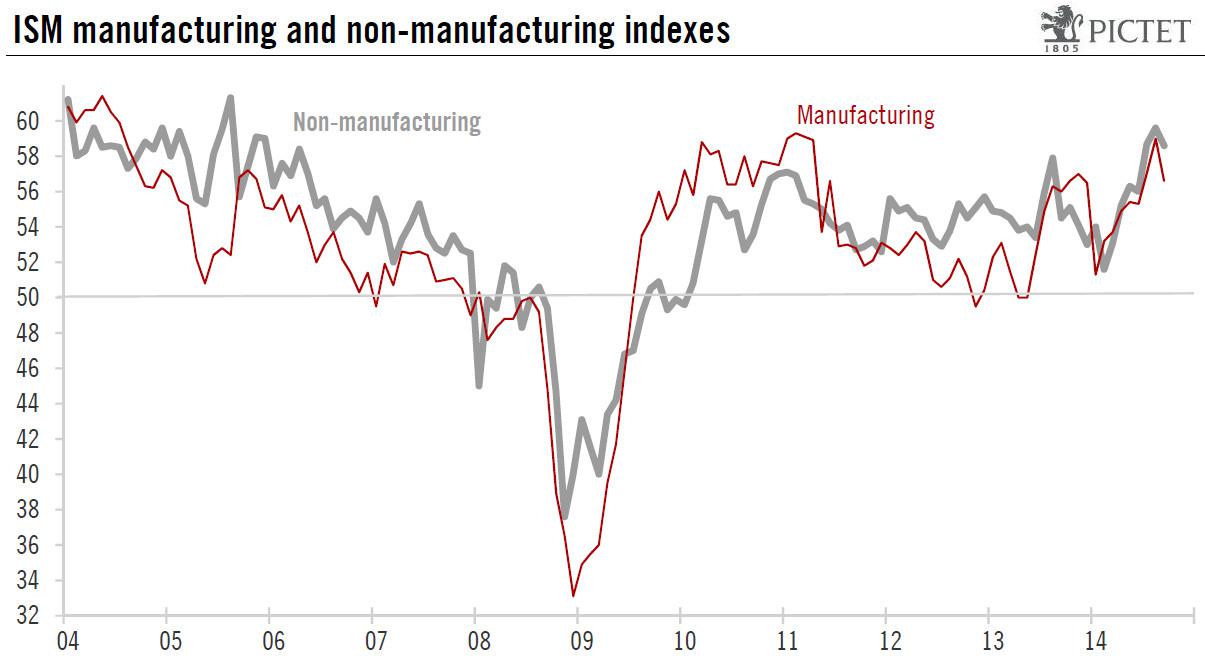

However, U.S. retail sales declined in September 2014 and prices paid by businesses also fell. Another report showed that both ISM indices weakened in September 2014, although the overall economic growth remained very strong in Q3 2014.

The ISM manufacturing survey showed that the reading fell back from 59.0 in August 2014 to 56.6 in September 2014. The composite non-manufacturing index dropped back as well, moving down from 59.6 in August 2014 to 58.6 in September 2014.

(click to enlarge)

Source: Pictet Bank website

These reports coupled with a weak growth in Europe and a potential slowdown in China could hurt U.S. exports, which could in turn put some pressure on the U.S. economy.

These are reasons for caution and will most likely deepen concerns at the U.S. Federal Reserve. A rate hike too soon could cause problems to the fragile U.S. economy which is gradually recovering. “If foreign growth is weaker than anticipated, the consequences for the U.S. economy could lead the Fed to remove accommodation more slowly than otherwise,” the U.S. central bank’s vice chairman, Stanley Fischer, said.

That being said, the US Federal Reserve will most likely defer to hike the interest rate planned to begin in H1 2015. A delay in expected interest rate hikes will soften the dollar over the next months, which will lift pressure off the oil price and will push Brent higher.

4)OPEC’s decision to cut supply in November 2014: Many OPEC members need the price of oil to rise significantly from the current levels to keep their house in fiscal order. If Brent remains at $85-$90, these countries will either be forced to borrow more to cover the shortfall in oil tax revenues or cut their promises to their citizens. However, tapping bond markets for financing is very expensive for the vast majority of the OPEC members, given their high geopolitical risk. As such, a cut on promises and social welfare programs is not out of the question, which will likely result in protests, social unrest and a new “Arab Spring-like” revolution in some of these countries.

This is why both Iran and Venezuela are calling for an urgent OPEC meeting, given that Venezuela needs a price of $121/bbl, according to Deutsche Bank, making it one of the highest break-even prices in OPEC. Venezuela is suffering rampant inflation which is currently around 50%, and the government currency controls have created a booming black currency market, leading to severe shortages in the shops.

Bahrain, Oman and Nigeria have not called for an urgent OPEC meeting yet, although they need between $100/bbl and $136/bbl to meet their budgeted levels. Qatar and UAE also belong to this group, although hydrocarbon revenues in Qatar and UAE account for close to 60% of the total revenues of the countries, while in Kuwait, the figure is close to 93%.

The Gulf producers such as the UAE, Qatar and Kuwait are more resilient than Venezuela or Iran to the drop of the oil price because they have amassed considerable foreign currency reserves, which means that they could run deficits for a few years, if necessary. However, other OPEC members such as Iran, Iraq and Nigeria, with greater domestic budgetary demands because of their large population sizes in relation to their oil revenues, have less room to maneuver to fund their budgets.

And now let’s see what is going on with Saudi Arabia. Saudi Arabia is too reliant on oil, with oil accounting for 80% of export revenue and 90% of the country’s budget revenue. Obviously, Saudi Arabia is not a well-diversified economy to withstand low Brent prices for many months, although the country’s existing sovereign wealth fund, SAMA Foreign Holdings, run by the country’s central bank, consisting mainly of oil surpluses, is the world’s third-largest, with assets totaling 737.6 billion US dollars.

This is why Prince Alwaleed bin Talal, billionaire investor and chairman of Kingdom Holding, said back in 2013: “It’s dangerous that our income is 92% dependent on oil revenue alone. If the price of oil decline was to decline to $78 a barrel there will be a gap in our budget and we will either have to borrow or tap our reserves. Saudi Arabia has SAR2.5 trillion in external reserves and unfortunately the return on this is 1 to 1.5%. We are still a nation that depends on the oil and this is wrong and dangerous. Saudi Arabia’s economic dependence on oil and lack of a diverse revenue stream makes the country vulnerable to oil shocks.”

And here are some additional key factors that the oil investors need to know about Saudi Arabia to place their bets accordingly:

a) Saudi Arabia’s most high-profile billionaire and foreign investor, Prince Alwaleed bin Talal, has launched an extraordinary attack on the country’s oil minister for allowing prices to fall. In a recent letter in Arabic addressed to ministers and posted on his website, Prince Alwaleed described the idea of the kingdom tolerating lower prices below $100 per barrel as potentially “catastrophic” for the economy of the desert kingdom. The letter is a significant attack on Saudi’s highly respected 79-year-old oil minister Ali bin Ibrahim Al-Naimi who has the most powerful voice within the OPEC.

b) Back in June 2014, Saudi Arabia was preparing to launch its first sovereign wealth fund to manage budget surpluses from a rise in crude prices estimated at hundreds of billions of dollars. The fund would be tasked with investing state reserves to “assure the kingdom’s financial stability,” Shura Council financial affairs committee Saad Mareq told Saudi daily Asharq Al-Awsat back then. The newspaper said the fund would start with capital representing 30% of budgetary surpluses accumulated over the years in the kingdom. The thing is that Saudi Arabia is not going to have any surpluses if Brent remains below $90/bbl for months.