Apparently the biggest banks in the US didn’t learn their lesson the first time around…

Because a few days ago, Wells Fargo, Bank of America, and many of the usual suspects made a stunning announcement that they would start making crappy subprime loans once again!

I’m sure you remember how this all blew up back in 2008.

Banks spent years making the most insane loans imaginable, giving no-money-down mortgages to people with bad credit, and intentionally doing almost zero due diligence on their borrowers.

With the infamous “stated income” loans, a borrower could qualify for a loan by simply writing down his/her income on the loan application, without having to show any proof whatsoever.

Fraud was rampant. If you wanted to qualify for a $500,000 mortgage, all you had to do was tell your banker that you made $1 million per year. Simple. They didn’t ask, and you didn’t have to prove it.

Fast forward eight years and the banks are dusting off the old playbook once again.

Here’s the skinny: through these special new loan programs, borrowers are able to obtain a mortgage with just 3% down.

Now, 3% isn’t as magical as 0% down, but just wait ‘til you hear the rest.

At Wells Fargo, borrowers who have almost no savings for a down payment can actually qualify for a LOWER interest rate as long as you go to some silly government-sponsored personal finance class.

I looked at the interest rates: today, Wells Fargo is offering the exact same interest rate of 3.75% on a 30-year fixed rate, whether you have bad credit and put down 3%, or have great credit and put down 30%.

But if you put down 3% and take the government’s personal finance class, they’ll shave an eighth of a percent off the interest rate.

In other words, if you are a creditworthy borrower with ample savings and a hefty down payment, you will actually end up getting penalized with a HIGHER interest rate.

The banks have also drastically lowered their credit guidelines as well… so if you have bad credit, or difficulty demonstrating any credit at all, they’re now willing to accept documentation from “nontraditional sources”.

In its heroic effort to lead this gaggle of madness, Bank of America’s subprime loan program actually requires you to prove that your income is below-average in order to qualify.

Think about that again: this bank is making home loans with just 3% down (because, of course, housing prices always go up) to borrowers with bad credit who MUST PROVE that their income is below average.

[As an aside, it’s amazing to see banks actively competing for consumers with bad credit and minimal savings… apparently this market of subprime borrowers is extremely large, another depressing sign of how rapidly the American Middle Class is vanishing.]

Now, here’s the craziest part: the US government is in on the scam.

The federal housing agencies, specifically Fannie Mae, are all set up to buy these subprime loans from the banks.

Wells Fargo even puts this on its website: “Wells Fargo will service the loans, but Fannie Mae will buy them.” Hilarious.

They might as well say, “Wells Fargo will make the profit, but the taxpayer will assume the risk.”

Because that’s precisely what happens.

The banks rake in fees when they close the loan, then book another small profit when they flip the loan to the government.

This essentially takes the risk off the shoulders of the banks and puts it right onto the shoulders of where it always ends up: you. The consumer. The depositor. The TAXPAYER.

You would be forgiven for mistaking these loan programs as a sign of dementia… because ALL the parties involved are wading right back into the same gigantic, shark-infested ocean of risk that nearly brought down the financial system in 2008.

Except last time around the US government ‘only’ had a debt level of $9 trillion. Today it’s more than double that amount at $19.2 trillion, well over 100% of GDP.

In 2008 the Federal Reserve actually had the capacity to rapidly expand its balance sheet and slash interest rates.

Today interest rates are barely above zero, and the Fed is technically insolvent.

Back in 2008 they were at least able to -just barely- prevent an all-out collapse.

This time around the government, central bank, and FDIC are all out of ammunition to fight another crisis. The math is pretty simple.

Look, this isn’t any cause for alarm or panic. No one makes good decisions when they’re emotional.

But it is important to look at objective data and recognize that the colossal stupidity in the banking system never ends.

So ask yourself, rationally, is it worth tying up 100% of your savings in a banking system that routinely gambles away your deposits with such wanton irresponsibility…

… especially when they’re only paying you 0.1% interest anyhow. What’s the point?

There are so many other options available to store your wealth. Physical cash. Precious metals. Conservative foreign banks located in solvent jurisdictions with minimal debt.

You can generate safe returns through peer-to-peer arrangements, earning up as much as 12% on secured loans.

(In comparison, your savings account is nothing more than an unsecured loan you make to your banker, for which you are paid 0.1%…)

There are even a number of cryptocurrency options.

Bottom line, it’s 2016. Banks no longer have a monopoly on your savings. You have options. You have the power to fix this.

There was a small ray of hope just after the Lehman collapse that one of the most lamentable characteristics of US society – the relentless urge to build massive McMansions (funding questions aside) – was fading. Alas, as the Census Bureau confirmed this week, that normalization in the innate American desire for bigger, bigger, bigger not only did not go away but is now back with a bang.

According to just released data, both the median and average size of a new single-family home built in 2015 hit new all time highs of 2,467 and 2,687 square feet, respectively.

And while it is known that in absolute number terms the total number of new home sales is still a fraction of what it was before the crisis, the one strata of new home sales which appears to not only not have been impacted but is openly flourishing once more, are the same McMansions which cater to the New Normal uber wealthy (which incidentally are the same as the Old Normal uber wealthy, only wealthier) and which for many symbolize America’s unbridled greed for mega housing no matter the cost.

Not surprisingly, as size has increased so has price: as we reported recently, the median price for sold new single-family homes just hit record a high of $321,100.

The data broken down by region reveals something unexpected: after nearly two decades of supremacy for the Northeast in having the largest new homes, for the past couple of years the region where the largest homes are built is the South.

While historically in the past the need for bigger housing could be explained away with the increase in the size of the US household, this is no longer the case, and as we showed last week, household formation in the US has cratered. In fact, for the first time In 130 years, more young adults live with parents than with partners…

…so the only logical explanation for this latest push to build ever bigger houses is a simple one: size matters.

Furthermore it turns out it is not only size that matters but amenities. As the chart below shows, virtually all newly-built houses have A/Cs, increasingly more have 3 or more car garages, 3 or more bathrooms, and for the first time, there were more 4-bedroom than 3-bedroom new houses built.

In conclusion it is clear that the desire for McMansions has not gone away, at least not among those who can afford them. For everyone else who can’t afford a mega home or any home for that matter: good luck renting Blackstone’s McApartment, whose price incidentally has soared by 8% in the past year.

For those curious for more, here is a snapshot of the typical characteristics of all 2015 new housing courtesy of the Census Bureau:

453,000 were detached homes, 49,000 were attached homes.

327,000 had a 2-car garage and 131,000 had a garage for 3 cars or more.

200,000 had one story, 278,000 had two stories, and 24,000 had three stories or more.

348,000 were paid for using conventional financing and 42,000 were VA-guaranteed.

The median sales price of new single-family homes sold was $296,400 in 2015, compared with the average sales price of $360,600.

The median size of a new single-family home sold was 2,520 square feet.

The type of foundation was a full or partial basement for 80% percent of the new single-family homes sold in the Midwest compared with 8% in the South.

On the heels of the 17-sigma beat in new home sales, pending home sales soared 5.1% MoM in April – 6.5 standard deviations above economist estimates of a 0.7% jump. Pending home sales rose for the third consecutive month in April and reached their highest level in over a decade, according to the National Association of Realtors. All major regions saw gains in contract activity last month (with The West surging 11.5% MoM) except for the Midwest, which saw a meager decline.

Best month since 2010…

Which no one saw coming…. Some context for the “beat”…

Lawrence Yun, NAR chief economist, says vast gains in the South and West propelled pending sales in April to their highest level since February 2006 (117.4).

“The ability to sign a contract on a home is slightly exceeding expectations this spring even with the affordability stresses and inventory squeezes affecting buyers in a number of markets,” he said. “The building momentum from the over 14 million jobs created since 2010 and the prospect of facing higher rents and mortgage rates down the road appear to be bringing more interested buyers into the market.”

Yun expects sales this year to climb above earlier estimates and be around 5.41 million, a 3.0 percent boost from 2015. After accelerating to 6.8 percent a year ago, national median existing-home price growth is forecast to slightly moderate to between 4 and 5 percent.

The usually strong spring housing market could be far stronger this year, if only there were more homes for sale.

The number of listings continues to drop, as demand outstrips supply and potential sellers bow out, fearing they won’t be able to find something else to buy.

The inventory of homes for sale nationally in April was 3.6 percent lower than in April 2015, according to the National Association of Realtors. Redfin, a real estate brokerage, also recently reported a drop in new listings.

The supply numbers are even tighter in certain local markets: Inventory is down 32 percent in Portland, Oregon, from a year ago; down 22 percent in Kansas City; down 21 percent in Dallas and Seattle; down 17 percent in Charlotte, North Carolina; down 12 percent in Atlanta; down nearly 10 percent in Chicago; and down 8 percent in Los Angeles, according to Zillow. Houston and Miami are seeing big gains in supply, due to economic issues specific to those markets.

“The struggle will continue for home shoppers this summer,” said Zillow chief economist Svenja Gudell. “New construction has been sluggish over the past year; we’re building about half as many homes as we should be in a normal market. There still aren’t enough homes on the market to keep up with the high demand from every type of home buyer.”

The short supply is pushing home prices higher than expected this year. Zillow had predicted 2 percent growth in home values from April 2015 to April 2016, but its latest data show values currently soaring more than twice that, at 4.9 percent.

“In many markets, those looking to buy a home in the bottom or middle of the market will need to be prepared for bidding wars and homes selling for over the asking price. This summer’s selling season’s borders will most likely be blurred again, as many buyers are left without homes and will need to keep searching,” added Gudell.

The inventory drops are most severe in the lower-priced tier of the market. Homes in the top tier are seeing gains and therefore show more price cuts. Sixteen percent of top-tier homes had a price cut over the past year, compared with 11 percent of bottom-tier homes and 13 percent of middle-tier, according to Zillow.

Sen. Mike Lee (R-Utah) has an amendment that would actually prohibit this implementation of the Affirmative Furthering Fair Housing (AFFH) regulation, specifically stopping HUD from attaching zoning changes as a condition for receiving funding, and it deserves every senator’s support.

According to the Federal Register, AFFH directs municipalities “to examine relevant factors, such as zoning and other land-use practices that are likely contributors to fair housing concerns, and take appropriate actions in response” as a condition for receipt of the block grants. It’s right there in the regulation.

On the other hand, Sen. Susan Collins (R-Maine) offers an amendment which merely reiterates current law that the federal government cannot compel the local zoning changes, stating no funds can be used “to direct a grantee to undertake specific changes to existing zoning laws.”

As noted by the National Review’s Stanley Kurtz, “Federal law already forbids HUD from mandating the spending priorities of state and local governments or forcing grant recipients to forgo their duly adopted policies or laws, including zoning laws. AFFH gets around this prohibition by setting up a situation in which a locality can’t get any federal grant money unless it ‘voluntarily’ promises to change its zoning laws and change its housing policies in exactly the way HUD wants.”

Kurtz emphasizes the point: “This trick allows HUD to avoid formally ‘directing’ localities to do anything at all in order to get their HUD grants. But HUD gives localities plenty of informal ‘guidance’ that makes it perfectly clear what they actually have to do to get their federal grants.”

Therefore, even with the Collins amendment, AFFH will still require municipalities to “examine relevant factors, such as zoning and other land-use practices that are likely contributors to fair housing concerns, and take appropriate actions in response” as a condition for receipt of the block grants.

This is an attempt by the Senate to pretend to have acted to stop the federalization of local zoning decisions without actually doing so. The Lee amendment will remove the local zoning strings attached to the funding, plain and simple. The Collins amendment will not.

It is telling that President Obama is threatening a veto of an appropriations bill that has “ideological” content, when the President himself is exercising the power of the purse to compel his ideological vision on our nation’s cities, towns and counties through implementation of AFFH.

The Collins amendment, ironically, will enable and advance this ideological agenda — while offering constituents false comfort that it has been abated when it has not. Only the Lee amendment can stop this HUD driven transformation of our neighborhoods.

The House has already passed the Lee language twice with vocal support from across the Conference ranging from Representatives Paul Gosar to Peter King. Americans for Limited Government urges every senator to vote yes on the Lee amendment to the Transportation-HUD appropriations bill — and stop the federalization of local zoning policiesonce and for all.

Unlike recent months when the Census Bureau reported some fireworks in the New Housing Starts and Permits data, the April update was relatively tame, and saw Starts rise from an upward revised 1,099K to 1,172K, beating expectations of a 1,125K print, mostly as a result of a 36K increase in multi-family units which however remain depressed below recent peaks from early 2015, which will likely stoke even higher asking rents, already at record highs across the nation.

But if starts were better than expected, then the future pipeline in the form of Housing Permits disappointed, with 1,116K units permitted for the month of April, below the 1,135K expected, if a rebound from last month’s downward revised 1,077K.

The issue, as with the starts data, is the multi-family, aka rental units, barely rebounded and remained at severely depressed levels last seen in 2013: at 348K rental units permitted in April, this is a far cry from the recent highs of 598K in June.

One wonders if this is intentional, because based on soaring asking rents, as shown in the chart below, with Americans increasingly unable or unwilling to buy single-family units, rental prices have exploded to 8% Y/Y based on Census data.

Should multi-family permits and starts remain as depressed as it has been in recent months, we expect that this chart of soaring median asking rents will only accelerate in the near future, and will require a whole host of seasonal adjustments from making its way into the already bubbly CPI data.

The purpose of the Federal Housing Administration is “to help creditworthy low-income and first-time home buyers“, individuals and families often denied traditional credit, to obtain a mortgage and purchase a home.” This system has been successful, and has aided in promoting home ownership. However, the FHA loan program and its related benefits are under threat as the Department of Justice continues to bring investigations and actions against lenders under the False Claims Act.

Criticism of the DOJ’s approach is that the department is using the threat of treble damages available under the False Claims Act to intimidate lenders into paying outsized settlements and having lenders admit guilt simply to avoid the threat of the enormous liability and the cost of a prolonged defense. If the DOJ wanted to go after bad actors who are truly defrauding the government with dishonest underwriting practices or nonexistent quality control procedures, then that would be acceptable to the industry.

But the DOJ seems to be simply going after deep pockets, where the intentions of the lenders are well-placed and the errors found are legitimate mistakes. Case in point: as of December 2015, Quicken Loans was the largest originator of FHA loans in the country, and they are currently facing the threat of a False Claims Act violation. To date Quicken has vowed to continue to fight, and stated they will expose the truth about the DOJ’s egregious attempts to coerce these unjust “settlements.”

When an originator participates in the FHA program, they are operating under the Housing and Urban Development’s FHA guidelines. As HUD cannot, and does not, check each and every loan guaranteed by FHA to confirm unflawed origination, the agency requires certification that the lender originating the file did so in compliance with the applicable guidelines. If the loan defaults, the lender submits a claim and the FHA will pay out the balance of the loan under the guarantee.

The False Claims Act provides that any person who presents a false claim or makes a false record or statement material to a false claim, “is liable to the United States Government for a civil penalty of not less than $5,500 and not more than $11,000…plus 3 times the amount of damages which the Government sustains because of the act.”

The DOJ argues that when a loan with known origination errors is certified by the lender to the FHA, with a subsequent claim submitted by the lender to the FHA after a default, the lender is in violation of the False Claims Act — because they knew or should have known the loan had defects when they submitted their certification, and yet still allowed the government to sustain a loss when the FHA paid out of the loan balance.

In the mortgage space the potential liability is astronomical because of the aforementioned penalties. The major issues in a False Claims Act violation can be boiled down to two major points: lack of clarity and specificity around what the DOJ considers “errors;” and what constitutes knowing loans were defective under the DOJ’s application of the act.

To the first point: are the errors of the innocuous, ever-present type found in a large lender’s portfolio, or egregious underwriting errors knowingly committed to increase production while offsetting risk through the FHA program? Obviously, lenders are arguing the former.

Prior to Justice’s aggressive pursuit of these settlements, if the FHA identified an underwriting error the lender would simply indemnify the FHA and not process the claim, effectively making it a lender-owned loan. This was an acceptable risk to lenders, as an error in the origination process could not become such an oversized loss. The liability would be capped to any difference between the borrower’s total debt at the time of foreclosure sale and what the lender could recoup when the property was liquidated. The DOJ’s use of the False Claims Act now triples a lender’s risk when originating FHA loans by threatening damages that are triple the value of the amount paid out by FHA.

In his letter to all JPMorgan Chase & Co. shareholders in April, Chief Executive Officer Jamie Dimon outlined the bank’s reasons for discontinuing its involvement with FHA loans. This perfectly illustrates how the DOJ is basically restoring all the lender risk to FHA-backed originations. Banks originating FHA loans are left with two choices: price in the new risk of underwriting errors into and pass the cost to the end borrower, making the product so costly it becomes pointless to offer; or cease or severely limit FHA offerings. If lenders take either approach, the DOJ will have negated the purpose of the FHA by limiting borrowers’ access to credit.

Walking away from FHA lending is not as simple as it sounds. Most FHA borrowers tend to have lower credit scores and/or require lower down payments. Most FHA loans also tend to be for homes located in low- and moderate-income neighborhoods. Any decline in an institution’s FHA offerings most likely will have a negative impact on an institution’s Community Reinvestment Act ratings. One has to think the DOJ is well aware of this fact and believes it will keep lenders in the FHA business even with the elevated risk, and can simply continue to strong-arm lenders into settlements.

If the Justice Department continues to aggressively utilize the False Claims Act, originators will be forced to evolve and create a product that they can keep as a portfolio loan or sell privately that can reach the same borrowers the FHA-insured products currently do. Again, there is a high likelihood that these products will not have as attractive terms as the FHA loans that borrowers are currently enjoying.

Large lenders will continue to step away from FHA originations, and smaller lenders originating FHA loans should be strongly aware of the risk they are taking on by continuing to originate FHA loans and increasing their portfolios as the larger banks exit the FHA market. Many large lenders have faced or are currently facing these actions, and from the Justice Department’s recent statements it does not appear they will abate anytime soon.

Hillary’s rumored running mate, Housing Secretary Julian Castro, is cooking up a scheme to reallocate funding for Section 8 housing to punish suburbs for being too white and too wealthy.

The scheme involves super-sizing vouchers to help urban poor afford higher rents in pricey areas, such as Westchester County, while assigning them government real estate agents called “mobility counselors” to secure housing in the exurbs.

Castro plans to launch the Section 8 reboot this fall, even though a similar program tested a few years ago in Dallas has been blamed for shifting violent crime to affluent neighborhoods.

It’s all part of a grand scheme to forcibly desegregate inner cities and integrate the outer suburbs.

Anticipating NIMBY resistance, Castro last month threatened to sue suburban landlords for discrimination if they refuse even Section 8 tenants with criminal records. And last year, he implemented a powerful new regulation — “Affirmatively Furthering Fair Housing” — that pressures all suburban counties taking federal grant money to change local zoning laws to build more low-income housing (landlords of such properties are required to accept Section 8 vouchers).

Castro is expected to finalize the new regulation, known as “Small-Area Fair Market Rents” (SAFMR), this October, in the last days of the Obama presidency.

It will set voucher rent limits by ZIP code rather than metro area, the current formula, which makes payments relatively small. For example, the fair market rent for a one-bedroom in New York City is about $1,250, which wouldn’t cover rentals in leafy areas of Westchester County, such as Mamaroneck, where Castro and his social engineers seek to aggressively resettle Section 8 tenants.

In expensive ZIP codes, Castro’s plan — which requires no congressional approval — would more than double the standard subsidy, while also covering utilities. At the same time, he intends to reduce subsidies for those who choose to stay in housing in poor urban areas, such as Brooklyn. So Section 8 tenants won’t just be pulled to the suburbs, they’ll be pushed there.

“We want to use our housing-choice vouchers to ensure that we don’t have a concentration of poverty and the aggregation of racial minorities in one part of town, the poor part of town,” the HUD chief said recently, adding that he’s trying to undo the “result of discriminatory policies and practices in the past, and sometimes even now.”

A draft of the new HUD rule anticipates more than 350,000 Section 8 voucher holders will initially be resettled under the SAFMR program. Under Obama, the total number of voucher households has grown to more than 2.2 million.

The document argues that larger vouchers will allow poor urban families to “move into areas that potentially have better access to jobs, transportation, services and educational opportunities.” In other words, offering them more money to move to more expensive neighborhoods will improve their situation.

But HUD’s own studies show the theory doesn’t match reality.

President Bill Clinton started a similar program in 1994 called “Moving to Opportunity Initiative,” which moved thousands of mostly African-American families from government projects to higher-quality homes in safer and less racially segregated neighborhoods in several counties across the country.

The 15-year experiment bombed.

A 2011 study sponsored by HUD found that adults using more generous Section 8 vouchers did not get better jobs or get off welfare. In fact, more went on food stamps. And their children did not do better in their new schools.

Worse, crime simply followed them to their safer neighborhoods, ruining the quality of life for existing residents.

“Males … were arrested more often than those in the control group, primarily for property crimes,” the study found.

Dubuque, Iowa, for example, received an influx of voucher holders from projects in Chicago — and it’s had a problem with crime ever since. A recent study linked Dubuque’s crime wave directly to Section 8 housing.

Of course, even when reality mugs leftists, they never scrap their social theories. They just double down.

The problem, they rationalized, was that the relocation wasn’t aggressive enough. They concluded they could get the desired results if they placed urban poor in even more affluent areas.

HUD recently tested this new theory in Dallas with disastrous results.

Starting in 2012, the agency sweetened Section 8 voucher payments, and pointed inner-city recipients to the far-flung counties surrounding Dallas. As government-subsidized rentals spread in all areas of the Metroplex (163 ZIP codes vs. 129 ZIP codes), so did crime.

Now Dallas has one of the highest murder rates in the nation, and recently had to call in state troopers to help police control it. For the first time, violent crime has shifted to the tony bedroom communities north of the city. Three suburbs that have seen the most Section 8 transfers — Frisco, Plano and McKinney — have suffered unprecedented spikes in rapes, assaults and break-ins, including home invasions.

Although HUD’s “demonstration project” may have improved the lives of some who moved, it’s ended up harming the lives of many of their new neighbors. And now Castro wants to roll it out nationwide. Soon he will give Section 8 recipients money to afford rent wherever they choose — and if they don’t want to move, he’ll make them an offer they can’t refuse.

Ironically, Hillary’s own hometown of Chappaqua is fighting Section 8 housing because of links to drugs and crime and other problems.

This is a big policy shift that will have broad implications, affecting everything from crime to property values. And it could even impact the presidential election, especially if Castro joins Hillary on the Democratic ticket.

Bay Area residents have had it with high costs and congestion.

According to a 1,000-person poll conducted by the Bay Area Council, a business-sponsored public policy advocacy group, about one-third of people living in the nine counties surrounding the San Francisco Bay are considering moving. According to SF Gate, council president and CEO Jim Wunderman called it the region’s “canary in a coal mine,” forewarning danger if nothing’s done to remedy the issues.

The poll found that 34% of Bay Area residents say that they are either strongly and somewhat likely to move away. While 54% say they have no plans to do so, only 31% feel strongly about staying.

Plans for relocation aside, there has been a considerable drop in optimism in recent years. About 40% of residents think that the area is headed in the right direction, compared to 55% last year and 57% the year before. Meanwhile, another 40% think that the Bay Area is “seriously off the wrong track.” Notably, optimism positively correlates with higher income.

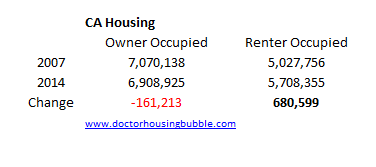

The Census Bureau released its quarterly updateon residential vacancies and home ownership for Q1 which is closely watched for its update of how many Americans own versus rent. It shows that following a modest pickup in the home ownership rate in the prior two quarters, US homeowners once again posted a substantial decline, sliding from 63.8% to 63.5%, and just 0.1% higher than the 50 year low reported in Q2 2015.

And perhaps logically, while home ownership continues to stagnate, the number of renters has continued to soar. In fact, in the first quarter, the number of renter occupied houses rose by precisely double the amount, or 360,000, as the number of owner occupied houses, which was a modest increase of 180,000. This brings the total number of renter houses to 42.85 million while the number of homeowners is virtually unchanged at 74.66 million.

A stark representation of the divergence between renters and owners can be seen in the chart below. It shows that over the past decade, virtually all the housing growth has come thanks to renters while the number of homeowners hasn’t budged even a fraction and has in fact declined in absolute numbers. What is obvious is that around the time the housing bubble burst, many Americans appear to have lost faith in home ownership and decided to become renters instead.

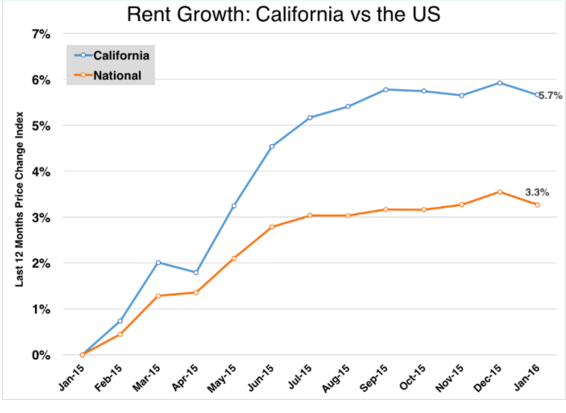

An immediate consequence of the above is that as demand for rental units has soared, so have median asking rents, and sure enough, according to Census, in Q1 the median asking rent at the national level soared to an all time high $870.

Which brings us to the one chart showing where the “missing” runaway inflation in the US is hiding: if one shows the annual increase in asking rents, what one gets is the following stunning chart which shows that while rent inflation had been roughly in the 1-2% corridor for two decades, starting in 2013 something snapped, and rent inflation for some 43 million Americans has exploded and is currently printing at a blended four quarter average rate of just over 8%, the highest on record, and 4 times higher than Yellen’s inflationary target.

So the next time Janet Yellen laments the collapse of inflation, feel free to show her this chart which even she can easily recreate using the government’s own data (the sad reality is that rents are rising even faster than what the government reports) at the following link.

Purchases of new homes unexpectedly declined in March for a third month, reflecting the weakest pace of demand in the West since July 2014.

Total sales decreased 1.5% to a 511,000 annualized pace, a Commerce Department report showed Monday. The median forecast in a Bloomberg survey was for a gain to 520,000. In Western states, demand slumped 23.6%.

Purchases rose in two regions last month, indicating uneven demand at the start of the busiest time of the year for builders and real estate agents. While new construction has been showing limited upside, cheap borrowing costs and solid hiring will help ensure residential real estate continues to expand.

“Housing is certainly not booming,” Jim O’Sullivan, chief U.S. economist at High Frequency Economics Ltd. in Valhalla, N.Y., said before the report. “Some people may be shut out of the market because lending standards are still tight. There may still be some reluctance to buy versus rent.”

Even so, “through the volatility, the trend is still more up than down, and we expect modest growth in sales,” he said.

Economists’ estimates for new-home sales ranged from 488,000 to 540,000. February purchases were revised to 519,000 from 512,000. The monthly data are generally volatile, one reason economists prefer to look at longer term trends.

The report said there was 90% confidence the change in sales last month ranged from a 13.5% drop to a 16.5% increase.

Sales in the West declined to a 107,000 annualized rate in March after surging 21.7% the previous month to 140,000. In the South, purchases climbed 5% to a 314,000 pace in March, the strongest in 13 months. Sales in the Midwest advanced 18.5%, the first gain in three months, and were unchanged in the Northeast.

The median sales price decreased 1.8% from March 2015 to $288,000.

There were 246,000 new houses on the market at the end of March, the most since September 2009. The supply of homes at the current sales rate rose to 5.8 months, the highest since September, from 5.6 months in the prior period.

From a year earlier, purchases increased 5.8% on an unadjusted basis.

New-home sales, which account for less than 10% of the residential market, are tabulated when contracts get signed. They are generally considered a timelier barometer of the residential market than purchases of previously owned dwellings, which are calculated when a contract closes, typically a month or two later.

Borrowing costs are hovering close to a three-year low, helping to bring house purchases within the reach of more Americans. The average rate for a 30-year fixed mortgage was 3.59% last week, down from 3.97% at the start of the year, according to data from Freddie Mac.

The job market is another source of support. Monthly payrolls growth averaged 234,000 in the past year, and the unemployment rate of 5% is near an eight-year low. Still, year-over-year wage gains have been stuck in a 2% to 2.5% range since the economic expansion began in mid-2009.

The market for previously owned homes improved last month, climbing 5.1% to a 5.33 million annualized rate, the National Association of Realtors reported April 20. Prices rose as inventories remained tight.

Even so, the market is getting little boost from first-time buyers, who accounted for 30% of all existing-home purchases, a historically low share, according to the group.

Recent data on home building has been less encouraging, although those figures are volatile month to month. New-home construction slumped in March, reflecting a broad-based retreat, a Commerce Department report showed last week. Home starts fell 8.8% to the weakest annual pace since October. Permits, a proxy for future construction, also unexpectedly dropped.

While the outlook for overall economic growth is darkening, the housing market is expected to keep up its momentum in 2016, according to Freddie Mac’s April 2016 Economic Outlook released on Friday.

Freddie Mac revised downward its forecast for Q1 GDP growth from 1.8 percent down to 1.1 percent. The “advance” estimate for GDP growth in the first quarter will be released by the Bureau of Economic Analysis (BEA) on Thursday, April 28. The GDP grew at an annual rate of just 0.6 percent in the first quarter of 2015 but then shot up to 3.9 percent for Q2; for the third and fourth quarter, the real GDP grew at rates of 2.0 percent and 1.4 percent, respectively.

The first quarter for the last few years has been punctuated by slow economic growth. While some of this can be attributed to seasonality, Ten-X (then Auction.com) Chief Economist Peter Muoio said that last year’s dismal GDP showing in the first quarter could be attributed to the brutal winter which slowed economic activity, labor disagreements at a bunch of the West Coast ports that really slowed the flow of cargo in Q1, and low oil prices (though this was partially offset by lower gas prices which put more money in consumers’ pockets).

“We’ve revised down our forecast for economic growth to reflect the recent data for the first quarter, but our outlook for the balance of the year remains modestly optimistic for the economy,” Freddie Mac Chief Economist Sean Becketti said. “However, we maintain our positive view on housing. In fact, the declines in long-term interest rates that accompanied much of the recent news should increase mortgage market activity, particularly refinance.”

On the positive side, Freddie Mac expects the unemployment rate will fall back below 5 percent for 2016 and 2017 (last month it ticked back up to 5.0 percent after hovering at 4.9 percent for a couple of months). Reduced slack in the labor market will push wage gains above inflation, although the gains are expected to be only modest, according to Freddie Mac.

While the economic forecast for Q1 has grown darker, the forecast looks bright for housing in 2016, however.

“We expect housing to be an engine of growth,” Freddie Mac stated in the report. “Construction activity will pick up as we enter the spring and summer months, and rising home values will bolster consumers and help support renewed confidence in the remaining months of this year.”

Low mortgage rates have boosted refinance activity in the housing market during Q1. The 30-year fixed mortgage rate averaged 3.7 percent for the first quarter, which drove an increase for the 1-4 single-family originations estimate for 2016 up by $50 billion up to $1.7 billion. Rates are expected to bump up, however, and average 4 percent over the full year of 2016, according to Freddie Mac. House prices are expected to appreciate by 4.8 percent over 2016 and 3.5 percent for 2017; homeowner equity is expected to rise as a result of the home price appreciation, which could mean more refinance opportunities.

The low mortgage rates combined with solid job growth are expected to make 2016 the strongest year for home sales since the pre-crisis year of 2006 despite the persistently tight inventory of for-sale homes, according to Freddie Mac.

“Sales were slow in the first quarter, but trends in mortgage purchase applications remain robust and we expect home sales to accelerate throughout the second quarter of 2016 as we approach peak home buying season,” Freddie Mac said.

Click here to view the entire Freddie Mac Economic Outlook for April 2016.

It’s 9:30 a.m. on a recent sunny Friday, and 60 people have crammed into an airport hotel conference room in Northern Virginia to hear Kevin Shortle, a veteran real estate professional with a million-watt smile, talk about “architecting a deal.”

Some have worked in real estate before, flipping houses or managing rentals. But the deals Shortle, lead national instructor for a company called Note School, is describing are different: He teaches people how to buy home notes, the building blocks of housing finance.

While titles and deeds establish property ownership, notes — the financial agreements between lenders and home buyers — set the terms by which a borrower will pay for the home. Financial institutions have long passed them back and forth as they re-balance their portfolios.

But the trade in delinquent notes has exploded in the post-financial-crisis world. As government entities like Fannie Mae and Freddie Mac have struggled with the legacies of the housing bust, they’ve sold billions of dollars’ of delinquent notes to big institutional investors, who resell them in turn.

A sign outside a foreclosed home for sale in Princeton, Ill, in January 2014.

And people like the ones in the Sheraton now pay good money to learn how to pursue what Note School calls “rich rewards.” The result: a marketplace where thousands of notes are bought and sold for a fraction of the value of the homes they secure.

A buyer can renegotiate with the homeowner, collecting steady cash. Or she might offer a “cash for keys” payout and seek a tenant or new owner. If all else fails, she can foreclose.

For some housing market observers, the churn in notes is a sign that the financial crisis hasn’t fully healed — and a fresh source of potential abuses. But the people listening to Shortle saw opportunity as he explained how they can “be the bank” for people with mortgage-payment problems.

“You can make a lot of money in the problem-solving business,” Shortle said.

How home notes move through a healing housing market

Since most people buy homes using mortgage financing, notes can be thought of as another name for mortgage agreements. After the home purchase closes, banks and other lenders usually sell them to government entities like Fannie Mae, Freddie Mac, and the Federal Housing Administration.

The housing market has improved since the bust, but hasn’t healed fully. There were 1.4 million foreclosures in 2015, according to real estate data firm RealtyTrac, and more than 17% of all transactions last year were deemed “distressed” — more than double pre-bust levels — in some way.

As the dust has settled, government agencies have begun selling delinquent notes to big institutional investors like Lone Star Funds, Goldman Sachs GS, +2.76% and Fortress Investments FIG, +3.96% as well as some community nonprofits, in bulk. The agencies have sold more than $28 billion in distressed loans since 2012, according to government data.

The big investors then sell some to buyers such as Colonial Capital Management, which is run by the same people who run Note School. Colonial, which buys about 2,000 notes a year, sells most of them one by one to people like the ones who gathered in the Virginia Sheraton.

It’s difficult to know how much this happens and what it has meant for homeowners.

Anyone who buys notes from the government must follow reporting requirements that include information on how the loans perform. Those requirements stay with the notes if they’re resold; they expire four years after the government’s initial sale. But nobody tracks note sales that weren’t made by the government, and even the government’s records don’t link outcomes and note owners.

March data from the Federal Housing Administration only hint at a broad view of how post-sale loans perform. The FHA has sold roughly 89,000 loans since 2012; less than 11% of those homeowners now pay their mortgages on time. Many are simply classified as “unresolved.” More than 34% had been foreclosed upon.

Fannie Mae and Freddie Mac, which began selling notes in 2014, were supposed to report similar data by the end of March. A spokeswoman for the agencies’ regulator said she did not know when that report, still incomplete, would be submitted.

And not all notes are initially sold by the government, making comprehensive oversight of the marketplace even harder. Banks and other lenders often sell notes directly; Colonial doesn’t buy notes from the government, according to Eddie Speed, founder of both Note School and Colonial.

For investors, a cleaner deal than the world of ‘tenants and toilets’

Note buying has attractions for both investors and the communities where the homeowners live.

Delinquent notes can be bought cheaply, often for about a third of a home’s market value. Note buyers get an investment that’s more like a financial asset — and less dirty than the landlord’s world of “tenants and toilets.”

Meanwhile, investors can often afford to cut homeowners a significant break, avoiding foreclosure while still making a profit.

And there’s government money for the taking in the name of helping homeowners. Since the housing crisis, the federal government has allocated nearly $10 billion to states deemed hardest-hit by the bust. Those states funnel the money to borrowers, often to help them reach new agreements with their lenders.

That can help municipalities that lose out on property taxes when homeowners don’t make payments, and which benefit from having more involved owners, Speed says.

Eddie Speed

When Tj Osterman, 38, and Rick Allen, 36, who have worked together as real-estate investors for about 10 years in the Orlando area, first explored note buying, they thought it little different than flipping abandoned houses.

But when they realized homeowners were often still in the picture, they changed their approach to try to work with them. Some of their motivation came from personal experience: Allen went through foreclosure in 2007. “It was a tough time,” he said. “I wish there was someone like me who said, let’s help you keep your house.”

They can buy notes cheaply enough that they can reduce the principal owed by homeowners “as much as 50%, and still turn a nice profit, pay back taxes, [and] get these people feeling good about themselves again,” said Osterman.

They now have a goal of helping save 10,000 homeowners from foreclosure. “I’m so addicted to the socially responsible side of stuff,” Osterman said. “We talk with borrowers like human beings and underwrite to real-world standards.”

‘There’s a system out there that’s broken’

Some housing observers have concerns about drawing nonprofessionals into an often-opaque market. A recent example Shortle used as a case study during the Virginia seminar helps explain why.

A note on an Atlanta-area home was being sold for $24,360; according to estimates from Zillow and local agents, its market value was between $50,000 and $70,000.

Some back taxes were owed, and a payment history showed that while the homeowner was making erratic or partial payments on her $500 monthly mortgage, she hadn’t quit. She had some equity built up in the house, another sign of commitment.

Real-estate investment firm Stonecrest sold her the home in 2012; she had used Stonecrest’s own financing at 9%. Her payment record was spotless until 2014. Stonecrest sold the note to Colonial in 2015 and Colonial offered it for resale in early 2016.

Most notes underpin mortgages. But this one was linked to a land contract, a financial agreement more typical when the seller is offering financing. Land contracts are sometimes criticized for being almost predatory: If a buyer skips a payment, the house and all the money he’s put toward it can be taken away.

And buyers don’t hold the deeds to the home, so the homes can be taken more quickly if they’re delinquent. Note School often steers students to scenarios where government programs like Hardest Hit can be tapped, but those programs don’t apply to land contracts.

Shortle walked his class through different strategies. The new note owner could foreclose; they could also induce the home buyer to walk. “It may be time to give this person a little cash for keys to move on,” he told the class. “They can’t afford it.”

Other data indicated that the house would rent for roughly $750. It might make sense, Shortle suggested, to remove the homeowner, fix up the house, rent it out, then sell the entire arrangement to a cash investor.

If a new note owner took that tack, the note would change hands four times in about as many years—even as the homeowner changed just once. The homeowner might never notice.

Some analysts see evidence of a still-hurting housing market behind all that activity.

By diffusing distressed loans out into a broader marketplace, lenders avoid the negative publicity that comes with foreclosing on delinquent homeowners. That masks “a layer of distress in the housing market that’s being overlooked,” said Daren Blomquist, vice president at RealtyTrac.

“This has been a way to push aside the crisis and sweep it under the rug,” Blomquist told MarketWatch.

Some analysts see evidence of a still-hurting housing market behind all that activity.

By diffusing distressed loans out into a broader marketplace, lenders avoid the negative publicity that comes with foreclosing on delinquent homeowners. That masks “a layer of distress in the housing market that’s being overlooked,” said Daren Blomquist, vice president at RealtyTrac.

“This has been a way to push aside the crisis and sweep it under the rug,” Blomquist told MarketWatch.

Osterman, left, and Allen

Note investors say they can offer a service others can’t or won’t. “There’s a real issue with how we’re treating hardships,” said Osterman. “There’s a system out there that’s broken and needs to be disrupted in a good way.”

Note School’s founder says the goal is a ‘win-win’

While newer investors like Osterman and Allen have a sense of mission forged during the recent housing crisis, Speed has been in the note business for more than 30 years. He is adamant that it’s in Note School’s best interest to teach students to observe regulation and treat homeowners respectfully. There’s no reason it can’t be a “win-win,” he said.

‘”We’re not teaching people to go and do ‘Wild West investing.’

Colonial Funding doesn’t make buyers of its notes go through Note School, but it does require them to work with licensed mortgage servicers. Note School offers connections to armies of vendors offering services for every step of the process: people who will assess the property’s real market value, “door-knockers” who will hand-deliver letters to homeowners, title research companies, insurers, and more.

“We’ve been in the note buying business for 30 years,” said Speed. “We’re not teaching people to go and do ‘Wild West investing.’”

Speed believes buying distressed notes is a process tailor-made for people with an entrepreneurial approach to doing well by solving problems — and maintains that he is mindful of the postcrisis environment in which they work.

“I’m walking into where the disaster has already happened,” he said. “If I walk into a loan where the customer has vacated, they probably want out. Common sense tells us if the borrower can deed it over to the lender and walk away with dignity, that seems like a good deal for him. We’re trying to do everything we can to reach resolution.”

Parents walk their daughter to class on the first day of kindergarten at the Telesis Academy in West Covina on Aug. 17, 2015. (Los Angeles Times)

Some of America’s most racially integrated neighborhoods and cities are on a path to becoming segregated all over again. In Los Angeles this means neighborhoods where Latinos and Asians now live alongside black or white neighbors may have few to no whites or blacks in 10 to 20 years.

In research I conducted with Siri Warkentien, another sociologist, we used a statistical model and census data to identify the most common changes in racial composition in 10,681 neighborhoods in metropolitan L.A., Houston, Chicago and New York, beginning as far back as 1970 in some areas. That starting point corresponds with the implementation of the 1968 federal Fair Housing Act, which protects buyers and renters from discrimination in choosing where to live.

Covina, 22 miles east of downtown L.A., provides an example of one city at risk of re-segregating. Whites make up about 26% of Covina as of 2014 and Latinos about 57%. Typically we consider neighborhoods with at least 10% of each group to be racially integrated. But the mix is crumbling. Latinos made up 13% of Covina’s residents in 1980, 26% in 1990, 40% in 2000, and 52% in 2010. Four years later, according to the most recent census estimate, the Latino population had grown by five more percentage points. By 2025, Covina is likely to be overwhelmingly Latino.

Something similar happened already in nearby Norwalk. In 1990, just under half its residents were Latino and about a third were white (not unlike Covina now). By 2014, Latinos made up 70% of residents and whites 11%.

The data show that vast portions of south and east Los Angeles are slipping from mixed populations toward single race populations. And the change has not just occurred in formerly white areas. One of the trajectories that we identified followed a similar pattern in neighborhoods that were once black. Compton residents were nearly three-quarters black in 1980; by 1990, the mix was about 52% black and 43% Latino; in 2014, two-thirds Latino. Such slow but steadily increasing Latino growth can be found in 46% of the neighborhoods we studied in the Los Angeles metropolitan region.

What’s causing a shift from mixed to single-race populations?

Immigration is one obvious factor. The Latino population increased in Los Angeles after immigration laws were changed in 1965 to encourage family reunification. That population was bolstered by a steady increase in Mexican immigrants from the mid-1990s until the recession. Newly arrived Latinos, like all immigrant groups, tend to find housing in neighborhoods already pioneered by their countryman who are already here.

Our research found that this process is occurring again in Southern California, but this time among immigrants from Asia, the source of the largest number of U.S. newcomers now. For example, the Asian proportion of the population in Cerritos increased from 44% in 1990 to 58% in 2000 to 62% in 2014. It appears to be following a path toward Asian segregation much like Covina is on the path to Latino segregation.

White preferences are another major factor that helps explain re-segregation.

Our model showed that, broadly speaking, during the 1980s, whites stopped fleeing from neighborhoods that were becoming integrated. But then — more than any other racial group — when whites did move they chose new neighborhoods with same-race neighbors.

In other words, Latinos moving to an area would not cause most whites to move out. But the prospect of having Latino neighbors might be enough to prevent whites from moving into a neighborhood. (Whites are moving to one kind of integrated neighborhoods: those that are gentrifying like downtown Los Angeles. But many fewer neighborhoods are gentrifying than segregating.)

For a time, places like Covina and Norwalk will remain integrated. But as whites in these areas get older and die, the outcome is clear. Consider the age patterns: In Covina, 22% of whites are 65 or older; only 14% are under the age of 18. Among Latinos in Covina, 6% are 65 or older; 32% are younger than 18.

Segregation is not, however, inevitable. Our statistical model found that in 20% of L.A. neighborhoods we examined, whites, blacks, Latinos and Asians have been living together for 10 to 30 years, and no group’s population is changing much faster or slower than any other. In fact, among L.A., Houston, Chicago and New York, Los Angeles had the highest proportion of these “quadrivial” neighborhoods.

There are ways to encourage integration. The Department of Housing and Urban Development has taken a positive step in this direction by requiring all grant recipients to show how they would promote integration, although Congress is threatening to undo this rule. At a local level, investment in neighborhood infrastructure, especially schools, attracts diverse residents and promotes integration. There is also new research that shows whites are choosing same-race neighborhoods not solely because of prejudice or animus, but because they don’t know about more mixed areas. In a separate study of Chicago area residents, for instance, whites were 2 to 6 times less likely than Latinos to even know about majority Latino neighborhoods.

Because so much of the shift in integration is based on whites’ decisions about where they will move next, Los Angeles’ future demographic patterns are in their hands. If whites do their homework, and find out more about neighborhoods that are now unfamiliar to them, they can make L.A. an example to the nation of how to create integration in the 21st century. Otherwise, knowingly or not, they may reproduce the problems of racial segregation for the future.

Chicago area sees greatest population loss of any major U.S. city, region in 2015

Ten years ago, Bonita Hatchett built her dream home in Flossmoor. A lawyer by trade, she moved to the south Chicago suburb to join a diverse community that included black professionals like herself.

But Hatchett is now planning to leave it all behind. The culprit? Property taxes.

“You’re told all your life: Be educated, be successful, work hard and buy a house. But, we’re being abused for doing so,” Hatchett said. “Living in a town like Flossmoor, it’s just not worth it.”

She’s not alone.

Illinoisans pay among the highest property taxes in the nation, according to the nonpartisan Tax Foundation. Some Illinoisans’ property-tax bills are more than their mortgage payments. And the squeeze is getting worse.

Since 1990, the average property-tax bill in Illinois has grown more than three times faster than the state’s median household income, according to Illinois Policy Institute research.

While Hatchett estimates the value of her home has been slashed in half over the past decade, her property tax bill has only gone up. She paid more than $18,000 in property taxes last year — well over 5 percent of what she thinks her house is worth.

Hatchett plans to move to Indiana, where taxes on residential property are capped at 1 percent of the value.

Seventy miles from Hatchett’s home, in the northwest Chicago suburb of Crystal Lake, Cassandra Bajak thinks this coming Christmas will be her two children’s last in their home. Since she and her husband, an Army veteran, built the house in 2002, their property-tax bills have doubled — eclipsing their mortgage payments.

Her family now is choosing between a move to a southern state or downsizing in their community.

“We’re being taxed out of our home,” Mrs. Bajak said. “The only reason we would ever leave our home or this state is property taxes, and that’s what’s going to happen.”

In McHenry County, where the Bajaks reside, property taxes eat up nearly 8 percent of the median household income. What’s worse, Illinoisans aren’t getting much bang for their tax bucks.

Property taxes at the municipal level have not been going to fund spotless roads or other public works. Instead, they’re mostly funding out-of-control pension costs.

Just take a look at Springfield, where 98 percent of the city’s 2014 property tax levy went to pensions. And where, from 2000 to 2014, members of the typical household have seen their property-tax bill grow more than twice as fast as their income.

Despite that, city-worker retirements are still in jeopardy.

While taxpayers have more than doubled their contributions to the local police and firefighter pension systems over the past decade, Springfield’s police pension fund has a mere 53 cents in the bank for every dollar it needs to pay out future benefits; for firefighter pensions, only 45 cents.

Forcing homeowners to keep shoveling more property tax dollars into broken pension systems has become a morally bankrupt solution to the problem.

In Springfield, for example, residents already contribute four times more money into police, fire and municipal employee pensions than do the employees.

The problem is that, in Illinois, state politicians mandate pension benefits for local government workers, with little regard to fairness for local taxpayers.

Many communities would prefer not to pay the high cost of workers enjoying early retirement ages, health insurance benefits normal residents could never afford, and annual 3 percent cost-of-living adjustments that private-sector workers could only dream of.

So how can the state protect homeowners?

Forcing local governments to begin to live within their means through a property-tax freeze, as has been proposed by Gov. Bruce Rauner, is necessary. But solving the root cause of the property-tax problem will require further reform, such as moving all new government workers from defined-benefit to self-managed retirement plans, transferring the power to negotiate pension benefits down to local leaders, and encouraging aggressive consolidation and resource-sharing across units of local government. For some communities, the only option to undo decades of mismanagement will be bankruptcy.

Until sincere efforts are made at reform, Illinoisans will continue to live in fear: taxpayers of being squeezed out of their homes, and government workers of pension payments that may never come.

Chicago area sees greatest population loss of any major U.S. city, region in 2015

After years of financial woes, Lindsey Yates and her husband had to at last address the nagging question: Should they stay or should they go?

The young couple’s continued residency in Chicago was threatened by new obstacles every few months. First came the rising property taxes, then the stress of finding a decent school for their 2-year-old son in a neighborhood they could afford.

Three weeks ago, Yates and her family hit the road, leaving the South Loop and successful careers in the rearview mirror as they headed toward their new house in a Denver suburb.

“The thing that boggles my mind: How is it that a dentist and a business professional and their one young son” can’t make it work financially? Yates asked from the road, at a pit stop in Nebraska, where her in-laws are living. “If we can’t make it work, who can?” she asked.

By almost every metric, Illinois’ population is sharply declining, largely because residents are fleeing the state. The Tribune surveyed dozens of former residents who’ve left within the last five years, and each offered their own list of reasons for doing so. Common reasons include high taxes, the state budget stalemate, crime, the unemployment rate and the weather. Census data released Thursday suggest the root of the problem is in the Chicago metropolitan area, which in 2015 saw its first population decline since at least 1990.

Chicago’s metropolitan statistical area, defined by the U.S. Census Bureau, includes the city and suburbs and extends into Wisconsin and Indiana.

The Chicago area lost an estimated 6,263 residents in 2015 — the greatest loss of any metropolitan area in the country. That puts the region’s population at 9.5 million.

While the numbers fell overall, there were some bright spots in the Chicago area: Will, Kane, McHenry and Kendall counties saw growth spurts, according to census data.

A crumbling, dangerous South Side creates exodus of black Chicagoans

The Chicago region’s decline extended to the state. In fact, Illinois was one of just seven states to see a population dip in 2015, and had the second-greatest decline rate last year after West Virginia, census data show. While the state’s population dropped by 7,391 people in 2014, the number more than tripled in 2015, to 22,194.

The plunge is mainly a result of the large number of residents leaving the state last year — about 105,200 in all — which couldn’t be offset by new residents and births, according to census data. The last year Illinois saw its population plunge was 1988.

The potential fallout is both political and financial. Federal and state government dollars are often distributed to local government agencies based on population; so the population loss creates long-term budget concerns. Communities pouring millions into new roads and schools, for example, based on rosy projections of future growth are left with fewer taxpayers to cover the cost.

Sights set on sun

Illinois has a long-standing pattern of losing residents to other states, but the loss has generally been offset by births and migration from other countries. Residents are mostly flocking to Sun Belt states — those with the country’s warmest climates, such as Nevada, Arizona and Florida.

During the years after the economic recession of the mid-2000s, migration to those states slowed, but it’s heated up again as states in the South and West have sunnier job opportunities and affordable housing.

“The old Snow Belt-to-Sun Belt movement is picking back up again, and movement south and west is fueling up,” said William Frey, a demographer with the Brookings Institution who analyzes census data.

Richard Morton, an Illinois resident of 62 years, is building a house in Panama City Beach, Fla., and plans to move into it in March 2017.

“We’ll say ‘hasta la vista, Illinois.’ I say that rather humorously, but I’m really rather sad about it,” he said. “My mother was born in Illinois. My grandparents lived their entire lives in Downers Grove.”

The clear draw for Morton is Florida’s weather but also what he calls an “attractive economy.”

“I used to enjoy Illinois and the area,” he said. “But everyday there’s a reason to not want to stay here. Between (Gov. Bruce) Rauner and (House Speaker Michael) Madigan, how will the state ever fix its pension problem? To me it seems unfixable, and I don’t want to have to pay for it.”

Texas attracts the greatest number of Illinois residents, followed by Florida, Indiana, California and Arizona, according to 2013 IRS migration data. Weather isn’t the only reason people are leaving the state.

More Illinois residents move to other Midwestern states than the number of Midwesterners moving to Illinois, said Michael Lucci, vice president of policy at the right-leaning Illinois Policy Institute. Job and business creation are simply stronger in neighboring states, he said.

“We talk opportunity all the time. If you’re moving to California, you might be a tech worker, or you might be someone who likes sunshine,” he said. “But when you see Illinois losing people to every Midwestern state, you know it’s not weather. People are moving for economic reasons.”

Through the 1990s and 2000s, Illinois saw what demographers consider normal rates of exodus for the state, about 50,000 to 70,000 more residents moving away from the state than moving in. But in 2015, the number spiked to about 95,000, and in 2015 it reached more than 100,000 people, according to census data.

Several moving companies that examine industry trends found high numbers of Illinoisans moving out of state. Allied Van Lines this year ranked Illinois No. 2 on its list of states with greatest outbound moves with 1,240, said spokeswoman Violette Sieczka. The numbers are limited to the movement of entire households.

The loss of residents over the last 20 years translates to about $50 billion in lost taxable income, and about $8 billion each year in lost state and local tax revenues, Lucci said.

“Frankly, we have this state budget problem, and it would be a lot less of a problem if we had all these people,” he said. “Growth makes problems better, out-migration makes problems worse.”

Losing faith in city

The main factors in Chicago’s population dip are diminished immigration, the aging of the Mexican immigrant population that bolstered the city throughout the 1990s as well as an exodus of African-Americans, experts say.

More than any other city, Chicago has depended on Mexican immigrants to balance the sluggish growth of its native-born population, said Rob Paral, a Chicago-based demographer who advises nonprofits and community groups. During the 1990s, immigration accounted for most of Chicago’s population growth. The number of Mexican immigrants rose by 117,000 in Chicago that decade, according to data gathered by Paral’s firm, Rob Paral and Associates.

After 2007, falling Mexican-born populations became a trend across the country’s major metropolitan areas. But most of those cities were able to make up for the loss with the growth of their native populations, Paral said. Chicago couldn’t.

Some experts also attribute the decline to the city’s African-American population, in part because of historically black communities hit hard by the foreclosure crisis, making houses cheap and easy to buy for Hispanics and whites who were willing to move for a bargain.

The 2010 census reported a 17 percent drop in the city’s black population over the previous decade. That number declined another an additional 4 percent through 2014, to 852,756.

“White people have left the state for years,” Paral said. “But African-Americans? That’s the one-two punch.”

Chicago residents leaving the state have cited the Chicago Public Schools’ financial crisis and the city’s red light camera controversy as motivating factors. The greatest concern, however, seems to be safety. Despite being the nation’s third most populous city, Chicago outpaces New York City and Los Angeles in the number of homicides and shootings, though it fares better than some smaller cities on a per capita comparison.

Melissa Koski, who moved to Arizona in 2008, said she left after being the victim of two crimes. One involved a break-in at her University Village neighborhood apartment while she slept, and the second involved being robbed at gunpoint near Grand and Milwaukee avenues with her mother.

“He got a whopping $40, but I still remember his smell and can feel his sweaty body wrapped around mine, with what felt like a gun pressed to my back,” she said.

Pat and Anna van Slee, longtime residents of the Uptown neighborhood, spent Thursday morning packing their house, preparing for their move to Thousand Oaks, Calif.

Their last apartment was in a six-flat that saw a series of crimes in and around the building in recent years. In one instance, a neighbor was mugged outside the complex; in another, a homeless man seeking shelter in the complex’s basement crawled through the window of the van Slees’ downstairs neighbor, Anna van Slee said.

“We’ve always lived in developing neighborhoods, but when you have a baby it makes you look at things differently,” Anna van Slee said, referring to her son, 4-month-old Orion. While the couple is moving primarily because of job opportunities, they’re glad to not have to enroll Orion in a CPS school, either, they said.

“Oddly, this was a safer neighborhood when it was rougher. It didn’t have some of the tension there is now, when million-dollar condos are going up next to subsidized housing,” she said.

Stemming the tide

There are things that can be done in coming years to mitigate the further exodus of residents from the state, said Lucci, of the Illinois Policy Institute. He recommends refocusing on manufacturing jobs in the state and curbing property taxes.

“We’re never gonna have Colorado’s mountains or California’s beaches,” he said. “But we have historically had an attractive business and job market. The problem is that we don’t have that anymore.”

Indeed, the employment rate is an issue: Illinois this year is tied with West Virginia for the 46th worst employment rate of all states, at 6.3 percent, according to Bureau of Labor Statistics.

“People are leaving Illinois because we rank near the bottom in job growth in the Midwest and have among the highest property taxes in America,” Catherine Kelly, a spokeswoman for Rauner, wrote in an emailed statement. “We have to make structural changes in Illinois to ensure talented people — many of whom run businesses — stay in Illinois to help grow the economy and improve our state’s future.”

In response to the decline in the region’s census numbers, Mayor Rahm Emanuel’s office issued a statement, saying the mayor was “working hard to build the Chicago economy of tomorrow by investing in a diverse economy and highly educated workforce that will continue to bring jobs and people to Chicago.”

It’s important that communities engage in careful discussion about cutbacks, and begin planning for smaller populations and smaller economic growth, said Eric Zeemering, a professor at Northern Illinois University’s School of Public and Global Affairs. But those discussions tend to be difficult and unpopular, he said.

“When politicians are focused on their next elections, it’s hard to have conversations about cutbacks and the realistic budgetary future,” Zeemering said.

In the meantime, he expects local leaders will make efforts to promote and advertise their towns as great places to live. The goal is that these communities will keep their residents despite the state’s problems.

“At the end of the day, some people are happy to live in snowy weather,” Zeemering said. “We don’t want to be a state people view in a negative light.”

The pessimists are already talking about 3% inflation later this year if energy prices don’t retreat. Most likely, Federal Reserve monetary experimentation will inflict a new great inflation on the U.S., although this is much more likely to occur in the next business cycle rather than the current one. Before that, we’ll get the shock of an economic slowdown — or even recession — which will exert some pause. So many households are right to ask whether their main asset will insulate them from this shock whenever it occurs. The answer from economic science is no.

House prices perform best during the asset-price inflation phase of the monetary cycle. During that period, low or zero rates stimulate investors to search for yield, which many do, shedding their normal skepticism. The growth in irrationality across many marketplaces is why some economists describe set price inflation as a “disease.” Usually, the housing and commercial real estate markets become infected by this disease at some stage.

Real estate markets are certainly not shielded from irrational forces. “Speculative stories” about real estate flourish and quickly gain popularity — whether it’s the ever-growing housing shortage in metropolitan centers; illicit money pouring into the top end from all over the world and high prices rippling down to lower layers of the market; or bricks and mortar (and land), the ultimate safe haven when goods and services inflation ultimately accelerates.

That last story defies much economic experience to the contrary. By the time inflation shock emerges, home prices have already increased so much in real terms under asset-price inflation that they cannot keep up with goods and services inflation, and may even fall in nominal terms. One thinks of the tale of the gold price in the Paris black market during World War II: prices hit their peak just before the Germans entered the city in May 1940 and never returned.

Real estate is only a hedge against high inflation if it is bought early on in the preceding asset-price inflation period. We can generalize this lesson. The arrival of high inflation is an antidote to asset-price inflation. That is, if it has not already reached its late terminal stage when speculative temperatures are falling across an array of markets.

To understand how home prices in real terms behave under inflation shock we must realize how, in real terms, they are driven by expectations of future rents (actual, or as given to homeowners); the cost of capital; and the profit from carry trade. All of these drivers have been operating in the powerful asset-price inflation phase the U.S. and many foreign countries have been experiencing during recent years.

Together they have pushed up the S&P Case Shiller national home price index to almost 20% above its long-run trend (0.6% each year since 1998), having fallen slightly below at its trough in 2011, and having reached a peak 85% above in 2006.

The cost of equity is low, judging by high underlying price earnings ratios in the stock markets. Investors suffering from interest income famine are willing to put a higher price on future earnings, whether in the form of house rents or corporate profits, than they would do under monetary stability.

Leveraged owners of real estate can earn a handsome profit between rental income and interest paid, especially taking account of steady erosion of loan principal by inflation and tax deductions.

The arrival of high inflation would change all these calculations.

Cost of equity would rise as markets feared the denouement of recession, and reckoned with the new burden on economic prosperity. Long-term interest rates would climb starkly in nominal terms. Their equivalent in real terms would be highly volatile and unpredictable, albeit at first low in real terms (inflation-adjusted), meaning that carry trade income for leveraged owners would become elusive.

None of this is to suggest that a high inflation shock is likely in the second quarter. A sustained period of much stronger demand growth across an array of goods, services and labor markets would most likely have to occur first, and could be seen as early as the next cyclical upturn.

An economic miracle could bring a reprieve from inflation. But much more likely, the infernal inflation machine of expanding budget deficits and Fed experimentation will ultimately mow down any resistance in its way.

The next housing crisis is here and this time it is all about one thing: supply.

Following the mid-aughts housing bubble that saw homeowners across the country get themselves upside down in homes and mortgages they couldn’t ever afford to repay — a crisis that was as much about too much supply as it was about too much bad financing — the market has gone the complete other direction.

First-time home buyers are crowded out, with Trulia’s chief economist Ralph McLaughlin writing Monday that the number of starter homes on the market has declined 43.6% in the last four years.

Homeowners that want to move from a starter home to something better can’t afford the next step. McLaughlin notes that the number of “trade-up” homes on the market is also down about 40% over the same period.