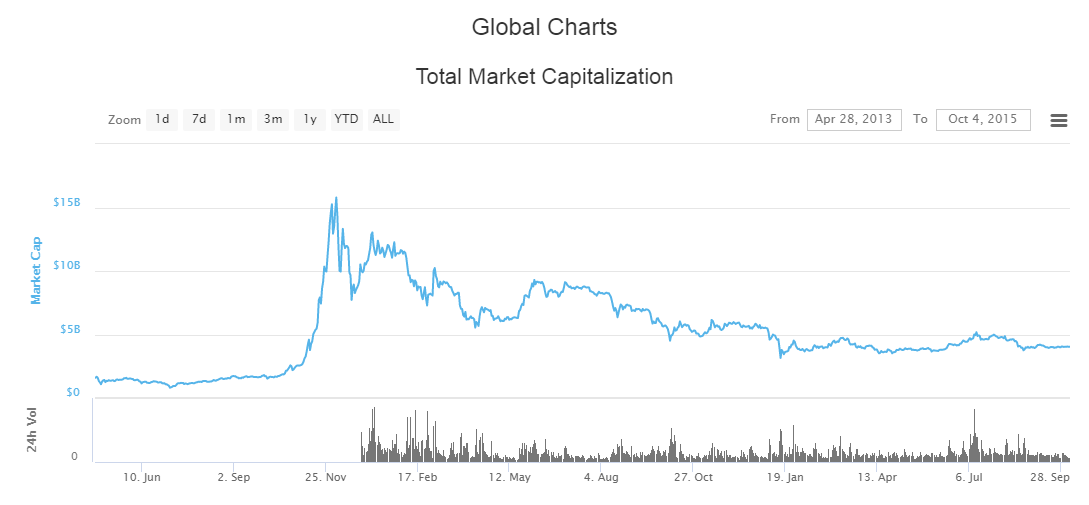

Since bitcoin first seeped into the public consciousness in 2013, the stereotypical image of the cryptocurrency trader is the 25-year-old tech bro who uses phrases like “YOLO” and “FOMO” when describing his trading strategy and general investing philosophy.

In more recent years, the image of the mom-and-pop crypto trader has taken hold,as Mrs. Watanabe– the archetypal Japanese and South Korean house wife once known for trading foreign exchange – has migrated to trading bitcoin and ethereum.

But as theFinancial Timespointed out in a story about financial professionals dabbling in crypto markets, the hoodie-wearing twenty something described above isn’t entirely representative of the crypto community. In fact, many former Wall Street professionals – some with backgrounds working at hedge funds or quantitative trading shops – have embraced cryptocurrency trading.

And while the allure of obscene returns is obviously one reason for the attraction, one venture capitalist interviewed by the FT offered an even more revealing answer:

He embraced crypto after becoming disillusioned with traditional markets, which “no longer make sense” thanks to nearly a decade of central bank intervention.

“I’ve been out of the stock market because it stopped making sense to me,” he says. Central bank support for the markets plus the trend of passive investing have turned it into a game with unclear rules.

“Over the past few years or so, everyone has just been buying indexes and they haven’t been doing price discovery. They’re just investing in a trend of something going up and up and up,” he says.

Until very recently, volatility in global stock markets had fallen to one of the lowest levels in history – making life difficult for quantitative traders who leverage up and play for small moves.

But in the crypto market, circumstances couldn’t be more different. Such high volatility is essentially a quantitative traders’ dream.

“In a days worth of cryptocurrency movement you have a week or a month of equity market movement or a decade of country debt,” he said.

Another apt description came from a hedge fund trader who said financial professionals are drawn to bitcoin for the same reasons they’re drawn to the poker table.

“It’s fun,” one hedge fund trader said, adding that she did not want “fomo,” the acronym for ‘fear of missing out’. One London-based banker was more blunt: it was gambling for people who could afford to lose a bit of money. “That’s it. Nothing else.”

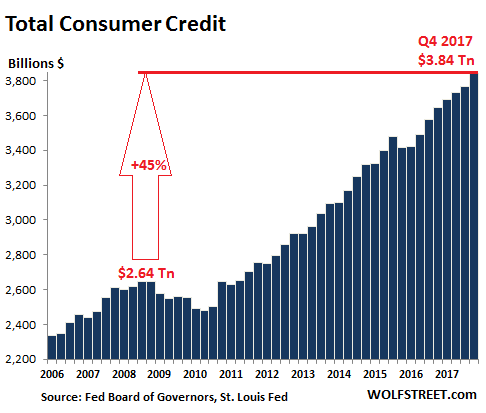

Total consumer credit rose 5.4% in the fourth quarter, year over year, to a record $3.84 trillion not seasonally adjusted, according to theFederal Reserve. This includes credit-card debt, auto loans, and student loans, but not mortgage-related debt. December had been somewhat of a disappointment for those that want consumers to drown in debt, but the prior months, starting in Q4 2016, had seen blistering surges of consumer debt.

Think what you will of the election – consumers celebrated it or bemoaned it the American way: by piling on debt.

The chart below shows the progression of consumer debt since 2006 (not seasonally adjusted). Note the slight dip after the Financial Crisis, as consumers deleveraged – with much of the deleveraging being accomplished by defaulting on those debts. But it didn’t last long. And consumer debt has surged since. It’s now 45% higher than it had been in Q4 2008. Food for thought: Over the period, the consumer price index increased 17.5%:

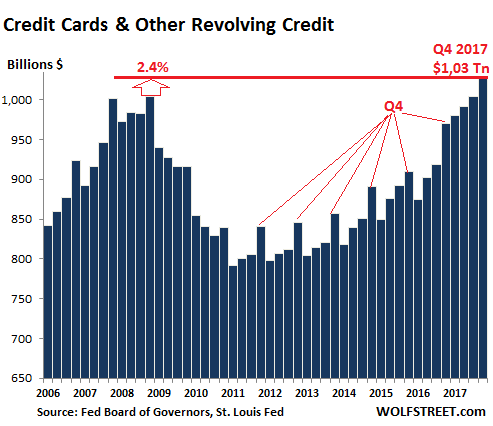

Credit card debt and other revolving credit in Q4 rose 6% year-over-year to $1.027 trillion, a blistering pace, but it was down from the 9.2% surge in Q3, the nearly 10% surge in Q2, and the dizzying 12% surge in Q1. So the growth of credit card debt in Q4 was somewhat of a disappointment for those wanting to see consumers drown in expensive debt.

The chart below shows the leap of the past four quarters over prior years. This pushed credit card debt in Q3 and Q4 finally over the prior record set in Q4 2008 ($1.004 trillion), before it came tumbling down via said “deleveraging.”

These are not seasonally adjusted numbers, and you can see the seasonal surges in credit card debt every Q4 during shopping season (as marked), and the drop afterwards in Q1. But then came 2017. In Q1 2017, credit card debt skyrocketed to an even higher level than Q4, when it should have normally plunged – a phenomenon I have not seen before.

This shows what kind of credit-card party 2017 and Q4 2016 was. Over the four quarter period, Americans added $58 billion to their credit card debt. Over the five-quarter period, they added $109 billion, or 12%! Celebration or retail therapy.

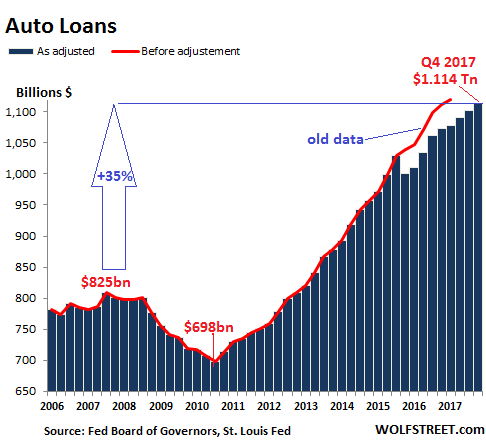

Auto loans rose 3.8% in Q4 year-over-year to $1.114 trillion. It was one of the puniest increases since the auto crisis had ended in 2011. Since then, the year-over-year increases were mostly in the 6% to 9% range. These are loans and leases for new and used vehicles. So the weakness in new-vehicle sales volume in 2017 was covered up by price increases in both new and used vehicles in the second half and strong used-vehicle sales:

The red line in the chart above indicates the old unadjusted data. In September 2017, the Federal Reserve announced a big adjustment of consumer credit data going back through Q4 2015, impacting auto loans, credit card debt, and total consumer credit. This adjustment was based on survey data collected every five years. So routine. But for Q4 2015, the adjustment knocked auto loan balances down by $38 billion.

Hence that misleading dip in auto loans in Q4 2015 in the chart above. This was at the peak of the auto-buying frenzy, and actual auto-loan balances certainly rose.

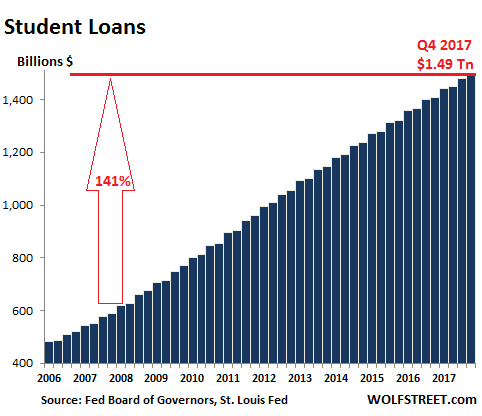

Student loans surged 5.6% in Q4 year-over-year. This seems like a shocking increase, but the year-over-year increases in Q3 and Q4 were the only such increases below 6% in this data series. Between 2007 – as far back as year-over-year comparisons are possible in this data series – and Q3 2012, the year-over-year increases ranged from 11% to 15%:

And there was no dip in student-loan balances during the Financial Crisis; in fact, those were the years with the steepest growth rates. From Q1 2008 to Q4 2017, student loan balances soared 141%, from $619.3 billion to $1.49 trillion, multiplying by 2.4 times over those ten years. More food for thought: Over the same period, the consumer price index rose 17.5%.

The problem with debt is that it doesn’t just go away on its own. If one side cannot pay, the other side takes a loss on their asset. Some auto loans and credit card debts remain on the balance sheet of lenders, while others have been securitized and are spread around among investors. But most student loans are guaranteed by the taxpayer or directly funded by the government.

Over the years, student loans have fattened entire industries: Investors in private colleges, the student housing industry (an asset class within commercial real estate), Apple and other companies supplying students with whatever it takes, the textbook industry…. They’re all feeding at the big trough held up by young people and guaranteed by the taxpayer. Food for thought, so to speak.

Yesterday ZeroHedge explainedthat one of the reasons why Deutsche Bank stock had tumbled to the lowest level since 2016, is because its top shareholder, China’s largest and most distressed conglomerate, HNA Group, had reportedly defaulted on a wealth management product sold on Phoenix Finance according to thelocal press reports. While HNA’s critical liquidity troubles havebeen duly noted here and have been widely known, the fact that the company was on the verge (or beyond) of default, and would be forced to liquidate its assets imminently, is what sparked the selling cascade in Deutsche Bank shares, as investors scrambled to frontrun the selling of the German lender which is one of HNA’s biggest investments.

Now, one day later, we find that while Deutsche Bank may be spared for now – if not for long – billions in US real estate will not be, and in a scene right out of the Wall Street movie Margin Call, HNA has decided to be if not smartest, nor cheat, it will be the first, and has begun its firesale of US properties.

According to Bloomberg, HNA is marketing commercial properties in New York, Chicago, San Francisco and Minneapolis valued at a total of $4 billion as the indebted Chinese conglomerate seeks to stave off a liquidity crunch. The marketing document lists six office properties that are 94.1% leased, and one New York hotel, the 165-room Cassa, with a total value of $4 billion.

One of the flagship properties on the block is the landmark office building at 245 Park Ave., according to a marketing document seen by Bloomberg.

245 Park Avenue, New York

HNA bought that skyscraper less than a year ago for $2.21 billion, one of the highest prices ever paid for a New York office building. The company also is looking to sell 850 Third Ave. in Manhattan and 123 Mission St. in San Francisco, according to the document. The properties are being marketed by an affiliate of brokerage HFF.

This is just the beginning as HNA’s massive debt load – which if recent Chinese reports are accurate the company has started defaulting on – is driving the company to sell assets worldwide.

According to Real Capital Analytics estimates, HNA owns more than $14 billion in real estate properties globally. The problem is that the company has a lot more more debt. As of the end of June, HNA had 185.2 billion yuan ($29.3 billion) of short-term debt — more than its cash and earnings can cover. The company’s total debt is nearly 600 billion yuan or just under US$100 billion. Which means that the HNA fire sale is just beginning, and once the company sells the liquid real estate, it will move on to everything else, including its stake in all these companies, whose shares it has already pledged as collateral.

So keep a close eye on Deutsche Bank stock: while HNA may have promised John Cryan it won’t sell any time soon but companies tend to quickly change their mind when bankruptcy court beckons.

Finally, the far bigger question is whether the launch of HNA’s firesale will present a tipping point in the US commercial (or residential) real estate market. After all, when what until recently was one of the biggest marginal buyers becomes a seller, it’s usually time to get out and wait for the bottom.

Growth? Inflation? Be careful what you wish for, as the surge in Treasury yields has sent mortgage interest rates to their highest in four years, flashing a big red warning light for affordability and home sales in 2018…

The U.S. weekly average 30-year fixed mortgage rate rocketed up 10 basis points to 4.32 percent this week. Following a turbulent Monday, financial markets settled down with the 10-year Treasury yield resuming its upward march. Mortgage rates have followed. The 30-year fixed mortgage rate is up 33 basis points since the start of the year.

Will higher rates break housing market momentum?

As the following chart shows, that surge in rates will have a direct impact on home sales (or prices will be forced to adjust lower) as affordability collapses…

The number of US renters is growing much more rapidly than the number of homeowners, so it shouldn’t come as a surprise that rents in the vast majority of American cities climbed again last month – continuing a trend that has largely persisted since the financial crisis, according to data compiled byRentCafe, a website that provides rental listings nationwide. RentCafe occasionally analyzes the reams of data it collects to provide insightful clues about the US housing market. And asmarkets pukedfollowing a robust headline increase in average hourly earnings – one of the first signs that stagnant consumer prices might once again rise – RC’s latest report shows that the national average rent was $1,361, 2.8% higher than this time last year, but flat on a monthly basis.

Nearly 90% of the nation’s biggest cities have seen rents grow in January; in 9% of cities rents remained unchanged, while only 2% experienced price declines…

Contrary to the conventional wisdom, it was actually America’s smaller cities that saw the greatest increases (to be sure, that’s probably because markets like San Francisco are already well past the boundaries of what typical middle-class workers can afford). These markets include Gilbert, AZ rose 8.5%, Roseville, CA (8.5%), and Fort Collins, CO (7.9%) breaking the top 10.

Meanwhile, in a sign that some of the hottest housing markets in the country are starting to buckle under the weight of over development, RC found that the only major market where rents dropped year-over-year was Brooklyn, where rents decreased by 14%.

Read RentCafe’s entire report below:

The price of apartments has gone up in 89% of the nation’s 250 largest cities in January 2018, as demand for rentals remains elevated throughout the country, sustained by an improving economy and low unemployment. Renters continue to embrace apartment life, as rent prices are increasing at a strong and steady annual rate of 2.8%, nationwide, reaching $1,361/month in January 2018.

The price of two-bedroom units is increasing the fastest

One and two-bedroom apartments remain the most in-demand apartment sizes in the U.S. The price of two-bedroom rentals has climbed the most over the year, with a 3.5% increase in rates, exceeding $1,400/month on average, while the price for one-bedroom units has increased by 3.4%, renting for $1,225/month on average in January. The slowest growing apartment type in January were studio apartments, renting for 2.5% more than this time last year.

Rents in 6 cities, including Brooklyn, NY, continue to slide

In only six cities out of the 250 studied are rents cheaper than they were one year ago. With a large new inventory of apartments to fill, the rental market in Lubbock, TX has seen the biggest drop in prices year over year, -6.3%, with an average apartment now renting for less than $900/month. Norman, OK is also seeing a slight decrease in the average rent (-2.3%), as a result of thousands of new apartments hitting the market in just the past few years, with an average rent of $861/month as of January 2018.

Diminished demand for housing has affected prices in McAllen, TX, which have declined by -2.2% year-over-year. Rents in Kansas City, KS and Baton Rouge, LA are also sliding slightly this month, by less than 2%. The only large market to see a decrease in rents is Brooklyn, NY, which had wrapped up last year -1.7% below the previous year’s levels, maintaining the downward direction in January as well, with rents down by -1.1% year over year.

U.S. Cities Where Rents Decreased Y-o-Y in January 2018

Three new cities break the top 10 with greatest rent increases

At the beginning of the year, we have three new cities entering the top 10 for fastest growing rents in the U.S. Fueled by increasing demand, Gilbert, AZ (8.5%), Roseville, CA (8.5%) and Fort Collins, CO (7.9%) saw big rent bumps over the past year. Rental prices in Gilbert, AZ are rising fast, clocking in at $1,156/month in January, as its population has been growing at extremely high rates, demand for housing has skyrocketed,and a big portion of the Gilbert population is renting.

Sacramento Metropolitan Area’s City of Roseville is joining Sacramento — where apartment prices have been on a steep climb for a while now — as one of the top 10 cities in the country with the fastest rising rents. The price ofapartments in Roseville, CAhas jumped by as much as 8.5% year-over-year, with the average rent currently exceeding $1,600/month. Fort Collins, CO has also become one of the country’s fastest growing rental markets, with residents and Colorado State students competing for a limited number of rental apartments. Rates are up almost 8% from the same time last year, a Fort Collins rental apartment costing on average $1,436/month at the moment.

Oil centers Odessa and Midland, TX are still at the top of the list with the highest rent rebounds over the year, 35% and 31.4% respectively. Buffalo, NY (12.1%) and Lancaster, CA (10.2%) also struggling with double-digit price hikes year-over-year.

U.S. Cities with the Fastest Growing Rents in January 2018:

The most expensive California rents push the limits again in January

The priciest cities for renters remain big urban job centers on both coasts, with Manhattan, NY at the top of the list with an average apartment rent of $4,079, unchanged from the previous month and down slightly by -1% over the year.

If renters living in The Golden State where hoping for a respite from high rents in the new year, they’re not getting it yet. Prices went up again in January in all 5 California cities in the top 10 most expensive for renters, with the highest rates in the state being in San Francisco, $3,448/month. Jersey City apartments, the sixth most expensive in the U.S., also saw increased rates this month, reaching $2,855.

Wichita, KS, Tulsa, OK, and Toledo, OH remain the country’s top 3 most affordable cities for renters, alongside 7 other Midwestern and Texan towns where average rents do not exceed $730/month, a fraction of the prices in coastal cities. In fact, things have been quiet in these parts of the country, as rents remained flat or grew slower than the national average in 9 out of 10 cities. Fort Wayne, IN was the only one to see a significant jump in prices for the year, 4.5%

At the start of the new year, rents are expected to continue rising throughout the country slightly above inflation, as demand for apartments remains strong from all generations of renters. Doug Ressler, senior analyst at Yardi Matrix, offered his opinion as to what renters can expect as we begin a new year:

You can find the average rent in your city atRentCafe.

Only one thing matters in bubble markets: sentiment

Yesterday saw Jerome Powell sworn into office as the new Chairman of the Federal Reserve, replacing Janet Yellen. Looking at the sea of red across Monday’s financial markets, Mr. Powell is very likely *not* having the sort of first day on the job he was hoping for…

Jerome H. Powell, new Chairman of the Federal Reserve.

Also having a rough start to the week is anyone with a long stock position or a cryptocurrency portfolio.

The Dow Jones closed down over 1,200 points today, building off of Friday’s plunge of 666 points. The relentless ascension of stock prices has suddenly jolted into reverse, delivering the biggest 2-day drop stocks have seen in years.

But that’s nothing compared to the bloodletting we’re seeing in the cryptocurrency space. The price of Bitcoin just broke below $7,000 moments ago, now nearly two-thirds lower from its $19,500 high reached in mid-December. Other coins, like Ripple, are seeing losses of closer to 80% over the same time period. That’s a tremendous amount of carnage in such a short window of time.

And while stocks and cryptos are very different asset classes, the underlying force driving their price corrections is the same — a change in sentiment.

Both markets had entered bubble territory (stocks much longer ago than the cryptos), and once they did, their continued price action became dependent on sentiment much more so than any underlying fundamentals.

The Anatomy Of A Price Bubble

History is quite clear on how bubble markets behave.

On the way up, a virtuous cycle is created where quick, out sized gains become the rationale that attracts more capital into the market, driving prices up further and even faster. A mania ensues where everyone who missed out on the earlier gains jumps in to buy regardless of the price, desperate not to be left behind (this is called fear of missing out, or “FOMO”).

This mania produces a last, magnificent spike in price — called a “blow-off” top — which is then immediately followed by an equally sharp reversal. The reversal occurs because there are simply no remaining new desperate investors left to sell to. The marginal buyer has suddenly switched from the “greater fool” to the increasingly cautious investor.

Those sitting on early gains and looking to cash out near the top start selling. They don’t mind dropping the price a bit to get out. So the price continues downwards, spooking more and more folks to start selling what they have. Suddenly, the virtuous cycle that drove prices to their zenith has now metastasized into a vicious cycle of selling, driving prices lower and lower as panicking investors give up on their dreams of easy riches and increasingly scramble to limit their mounting losses.

In the end, the market price retraces nearly all of the gains made, leaving a small cadre of now-rich early investors who managed to get out near the top, and a large despondent pool of ‘everyone else’.

We’ve seen this same compressed bell-curve shape in every major asset bubble in financial history:

And we’re seeing it play out in real-time now in both stocks and cryptos.

The Bursting Crypto Bubble

It’s amazing how fast asset price bubbles can pop.

Just a month ago, the Internet was replete with articles proclaiming the new age of cryptocurrencies. Every day, fresh stories were circulated of individuals and companies making overnight fortunes on their crypto bets, shaking their heads at all the rubes who simply “didn’t get” why It’s different this time.

Here at PeakProsperity.com the demand for educational content on cryptocurrencies from our audience rose to a loud crescendo.

We did our best to provide answers as factually as we could through articles and webinars, though we tried very hard not to be seen as encouraging folks to pile in wantonly. A big reason for this is we’re more experienced than most in identifying what asset bubbles look like.

To us, the run-up in the cryptocurrencies seen over 2017 had all the classic hallmarks of an asset price bubble — irrespective of the blockchain’s potential to unlock tremendous long-term economic value. Prices had simply risen way too far way too fast. Which is why we issueda cautionary warningin early December that concluded:

So, if you’ve been feeling like the loser who missed the Bitcoin party bus, you’ve likely done yourself a favor by not buying in over the past few weeks. It is highly, highly likely for the reasons mentioned above that a painful downwards price correction is imminent. One that will end in tears for all the recent FOMO-driven panic buyers.

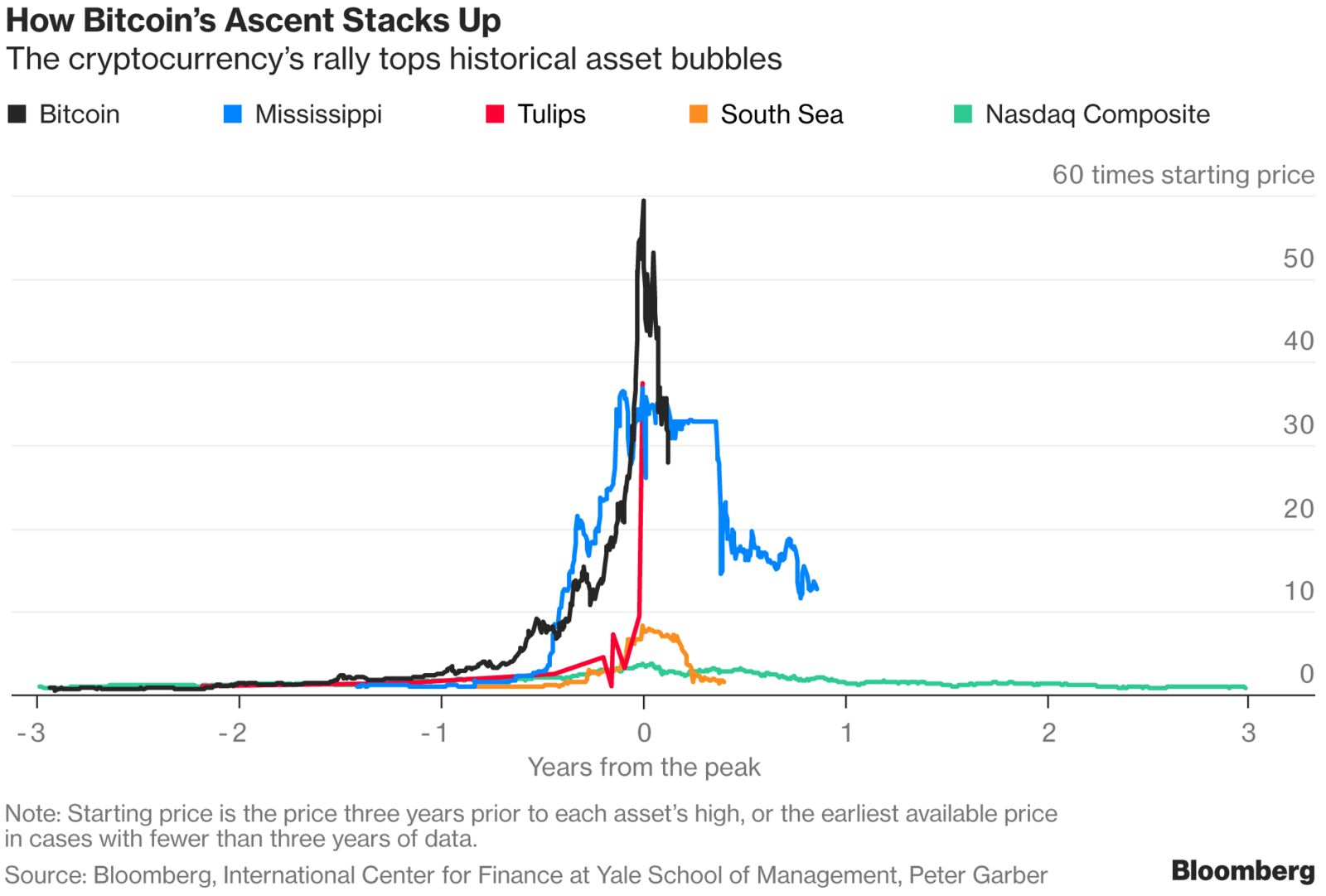

And now that time has shown this warning to have been prescient in both its accuracy and timeliness, we can clearly see that Bitcoin is following the classic price trajectory of the asset price bubble curve. The chart below compares Bitcoin’s current price to that of several of history’s most notorious bubbles:

This chart (which is from Feb 2, so it doesn’t capture Bitcoin’s further decline below $7k) shows that Bitcoin is now about 2/3 of its way through the bubble life-cycle, and about half-way through its fall from its apex.

Projecting from the paths of previous bubbles, we shouldn’t be surprised if Bitcoin’s price ends up somewhere in the vicinity of $2,500-$3,000 by the time the dust settles.

Did The Stock Market Bubble Just “Pop”?

Despite the extreme drop in the stock market over the past two days, any sort of material bubble retracement has yet to begin — which should give you an appreciation of how overstretched its current valuation is.

Look at this chart of the S&P 500 index. Today’s height dwarfs those of the previous two bubbles the index has experienced this century.

The period from 2017 on sure looks like the acceleration seen during a blow-off top. If indeed so, does the 6% drop we’ve just seen over the past two trading days signify the turning point has now arrived?

Crazily, the carnage we’ve seen in the stock market over the past two days is just barely visible in this chart. If indeed the top is in and we begin retracing the classic bubble curve, the absolute value of the losses that will ensue will be gargantuan.

If the S&P only retraces down to the HIGHS of its previous two bubbles (around 1,500), it would need to fall over 43% from where it just closed today. And history suggests a full retracement would put the index closer to 750-1,000 — at least two-thirds lower than its current valuation.

How Spooked Is The Herd?

As a reminder, bubbles are psychological phenomena. They are created when perception clouds judgment to the point where it concludes “Fundamentals don’t matter”.

And they don’t. At least, not while the mania phase is playing out.

But once the last manic buyer (the “greatest” fool) has joined the party, there’s no one left to dupe. And as the meteoric price increase stops and then reverses, the herd becomes increasingly skittish until a full-blown stampede occurs.

We’ve been watching that stampede happen in the crypto space over the past 4 weeks. We may have just seen it start in the stock markets.

How much farther may prices fall from here? And how quickly?

History gives us a good guide for estimating, as we’ve done above. But the actual trajectory will be determined by how spooked the herd is.

For a market that has known no fear for nearly eight years now, a little panic can quickly escalate to an out-of-control selling frenzy.

Want proof? We saw it late today in the complete collapse in XIV, the inverse-VIX (i.e. short volatility) ETN that has been one of Wall Street’s most crowded trades of late. It lost over 90% of its value at the market close:

The repercussions of this are going to send seismic shock waves through the markets as a tsunami of margin calls erupts. A cascading wave of sell-orders that pushes the market further into the red at an accelerating pace from here is a real possibility that can not be dismissed at this point.

Those concerned about what may happen next should read our premium reportIs This It?issued over the past weekend.

In it, we examine the congregating perfect storm of crash triggers — rising interest rates, a fast-weakening dollar, a sudden return of volatility to the markets after a decade of absence, rising oil prices — and calculate whether the S&P’s sudden 6% rout is the start of a 2008-style market melt-down (or worse).

Make no mistake: these are sick, distorted, deformed and liquidity-addicted bubble markets. They’ve gotten entirely too dependent on continued largess from the central banks.

That is now ending.

After so many years of such extreme market manipulation finally gives way, the coming losses will be staggeringly enormous.

The chief concern of any prudent investor right now should be: How do I avoid being collateral damage in the coming reckoning?

A 20-year-old college student from Busan committed suicide this week after losing nearly 200 million won in cryptocurrency.

Korean media reports the student had dropped out of college and was working as a social worker, but he was suffering from depression and insomnia due to the recent drop in cryptocurrency in the country.

He was found lying on his bed Thursday with a plastic compression pack around his head when found by his mother in his apartment. A 13L gas tank of helium was also found in his room according to local media.

In the last major move of Chairwoman Janet Yellen’s reign at the central bank, the Fed said it won’t let Wells FargoWFC, -6.21%add assets beyond the level of the end of 2017 until it improves governance and controls. Wells Fargo ended 2017 with $1.95 trillion in assets.

Wells Fargo will be able to continue current activities including accepting customer deposits or making consumer loans, the Fed said.

“We cannot tolerate pervasive and persistent misconduct at any bank and the consumers harmed by Wells Fargo expect that robust and comprehensive reforms will be put in place to make certain that the abuses do not occur again,” Yellen said in a statement. “The enforcement action we are taking today will ensure that Wells Fargo will not expand until it is able to do so safely and with the protections needed to manage all of its risks and protect its customers.”

The asset cap is unprecedented, according to Federal Reserve officials.

Federal Reserve officials didn’t say it was specifically planned for Yellen’s last day — and they said the bank agreed to the terms on Friday afternoon.

The Fed cited not only the millions of customer accounts Wells Fargo opened without authorization but also more recent revelations that the bank charged hundreds of thousands of borrowers for unneeded guaranteed auto protection or collateral protection insurance for their automobiles.

Wells Fargo will replace three current board members by April and a fourth board member by the end of the year, the Fed said. Sen. Elizabeth Warren, the Massachusetts Democrat, had requested the Fed oust Wells Fargo board members. The Fed didn’t identify which board members will have to leave.

The Fed also singled out Stephen Sanger, the former lead independent director, and former CEO John Stumpf with letters excoriating them for the abuses.

The vote for the sanctions was 3-0, with the incoming chairman, Jerome Powell, joining Yellen and Gov. Lael Brainard. The new vice chairman for regulation, Randal Quarles, abstained.

Quarles previously said he would recuse himself from Wells Fargo matters because he and his family previously had a financial interest in the bank.

In after-hours trade late Friday, Wells Fargo shares dropped over 5%.

A historic property in this rustic Italian village could be yours for less than the cost of a coffee — but, of course, there’s a catch

Cagliari, Italy, pictured, is the capital of the island of Sardinia, and lies about 105 kilometers south of Ollolai, where a house can be had for a mere €1.

Ever dreamed of packing up and moving abroad — to, say, a rustic Italian village? Now may be the time to make it happen.

Ollolai, a village on the Mediterranean isle of Sardinia, is,according to CNN, offering up its empty housing stock for the bargain price of just €1, or about $1.25.

The Italian island of Sardinia is highlighted on this European map. It lies just south of the French-controlled island of Corsica.

Of course, there is a catch. Buyers must commit to refurbishing their bargain-basement house within three years, which is likely to carry an estimated additional expense of $25,000 or more.

It’s all part of a plan to bring life back into a town that has watched its population sink from 2,250 to 1,300 over the past half decade, according to CNN. Most of the homes are in poor condition.

“We need to bring our grandmas’ homes back from the grave,” Ollolai Mayor Efisio Arbau reportedly told CNN.

Colorful sunshade umbrellas hang over the street in Pula, Italy, another village on the island of Sardinia, where homes are being sold for just €1.

If the plan works, the town, comprising a virtual maze of alleys and mural-adorned piazzas surrounded by stone dwellings, could turn the city into a stereotypically picturesque Italian village once more. And for homeowners, it could be an opportunity to retire to a more relaxing way of life. The town is known for its locally made premium sheep cheese, Casu Fiore Sardo; handwoven baskets; and traditional celebrations.

But if you think you might want to move to Ollolai, you’ll have to act fast. The €1 pricing is only available through Feb. 7,according to the city’s website.

California is rapidly plunging back into drought, with severe conditions now existing in Santa Barbara, Ventura and Los Angeles counties—home to one-fourth of the state’s population, a national drought monitor said Thursday.

In this Wednesday Jan. 3, 2018 file photo, Grant Davis, director of the Dept. of Water Resources, center, discusses the results of the first snow survey of the season at the nearly snow barren Phillips Station snow course, near Echo Summit, Calif. California’s water managers are carrying out their mid-winter snow pack survey Thursday, Feb. 1, 2018, as the winter’s dry spell persists. (AP Photo/Rich Pedroncelli, File)

The weekly report released by the U.S. Drought Monitor, a project of government agencies and other partners, also shows 44 percent of the state is now considered to be in a moderate drought. It’s a dramatic jump from just last week, when the figure was 13 percent.

“It’s not nearly where we’d like to be,” Frank Gehrke, a state official, acknowledged after separately carrying out manual measurements of winter snowfall in the Sierra Nevada mountains, which supplies water to millions of Californians in a good, wet year.

Overall, the vital snow pack Thursday stood at less than a third of normal for the date.

California lifted a drought state of emergency less than a year ago, ending cutbacks that at the peak of the drought mandated 25 percent conservation by cities and towns, devastated generations of native salmon and other wildlife, made household wells run dry in the state’s middle, and compelled farmers to dig deep, costly wells.

A rainy winter last year in the state’s north finally snapped the worst of that drought.

The new figures from national drought monitors came amid growing concern among state officials about another dry winter. The dry spell is acute in Southern California. Los Angeles and some surrounding areas have received only one significant storm in nearly a year, and it triggered deadly mudslides. The region is now seeing record-setting heat.

The readings detailed Thursday show the drought has worsened to the severe category in 5 percent of the state. The last time even a small part of the state was rated in severe drought was last year.

However, Thursday’s figures were far better than those during the peak of the state’s epic dry spell, when 99.9 percent of California was in some stage of drought, and nearly half in the highest category.

But the drought never really seemed to lift in some Southern California areas, Daniel Swain, a climate scientist at University of California, Los Angeles, noted this week.

In Ventura and Santa Barbara counties, the lack of rain and dry vegetation were perfect fuel for a December wildfire that grew to become the largest recorded in state history. When it finally rained, the scorched earth turned into mudslides that sent earth, water and boulders roaring through neighborhoods.

In California’s Central Valley, the nation’s richest agricultural producer, government officials had to install water systems during and after the five-year drought for small towns such as East Porterville after household wells ran dry.

Even so, deliveries of bottled water continued this week to people outside East Porterville, said resident Elva Beltran, one of many volunteers who helped neighbors without water.

“it never ended,” she said of the drought in her area.

California’s water managers trekked to the mountains on Thursday to check the snow depth—one gauge of the state water supply. Electronic sensors showed statewide snow levels at 27 percent of normal.

A bright spot, said Doug Carlson, spokesman for the state’s Department of Water Resources, which carries out the snowpack surveys, was that reservoirs remain far fuller than usual thanks to last year’s rain in the state’s north.

“As we approach the 8400-8500 level, watch for volume to pick up. One of two things will happen, it will reverse sharply or drive through that level to find another level of value below. If we stall here and a lull in the market occurs, price will consolidate, and then move lower”

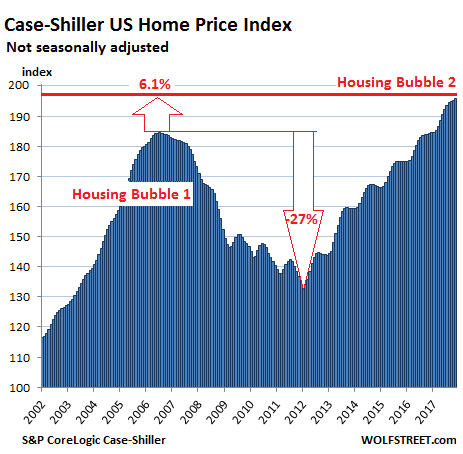

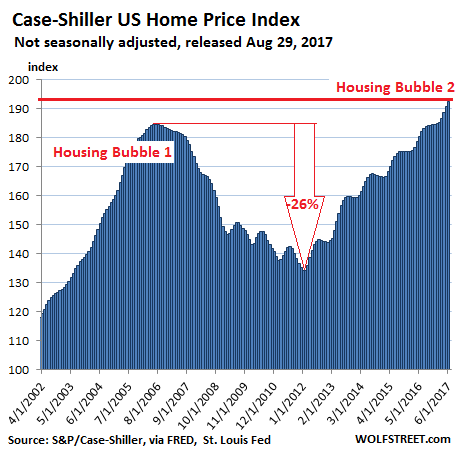

Just after Wolf Richter reported on the minuscule 1.4% year-over-year growth of per-capita “real” disposable income and the lowest saving rate in 12 years —for the lucky ones— there’s another asset-bubble doozie: The S&P CoreLogic Case-Shiller National Home Price Index for November, released this morning, rose 6.2% year-over-year (not-seasonally-adjusted). The index has now surpassed by 6.1% what was afterwards called the crazy peak of Housing Bubble 1 in July 2006 and is up 46% from the bottom of Housing Bust 1:

Real estate prices are a result of local dynamics but are also impacted by national and global factors, including monetary policies and foreign non-resident investors trying to get their money out of harm’s way. This causes local housing bubbles, operating on their own schedules. When enough of them occur simultaneously, it becomes a national housing bubble. See chart above.

The Case-Shiller Index is based on a rolling three-month average; today’s release was for September, October, and November data. Instead of median prices, the index uses “home price sales pairs,” for example for a house that sold in 2010 and then again in 2017. The index provider incorporates other factors and uses algorithms to adjust the price movement into an index data point. The index was set at 100 for January 2000. An index value of 200 means prices as figured by the algorithm have doubled since then.

Here are the most magnificent leaders among the housing bubbles in major metro areas:

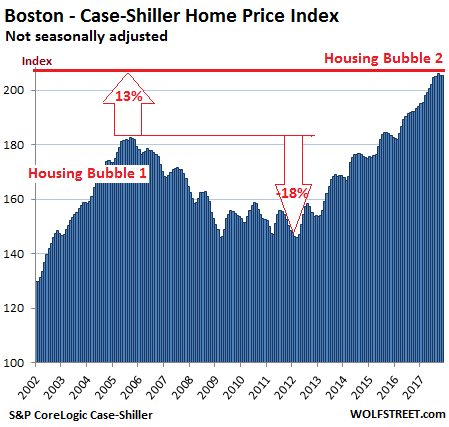

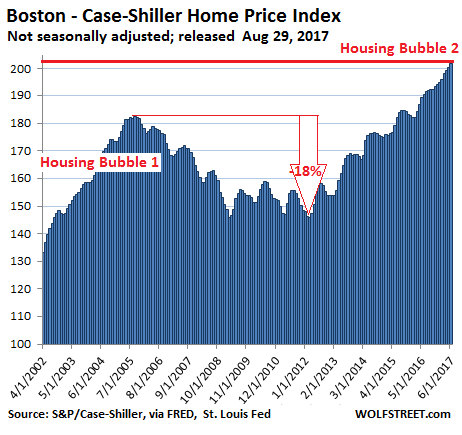

Boston:

The index for the Boston metro area edged down again on a monthly basis, the second decline in a row after 22 months in a row of increases. It has essentially been flat for four months but is still up 6.3% year-over-year. The slight monthly decline could be within the normal seasonal variations but there were no seasonal variations during the relentless surge in 2016 and 2015. During Housing Bubble 1, from January 2000 to October 2005, the index for Boston soared 82% before plunging. The index now exceeds the peak of Housing Bubble 1 by 12.5%:

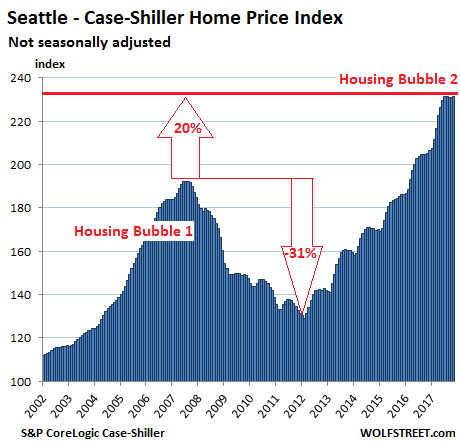

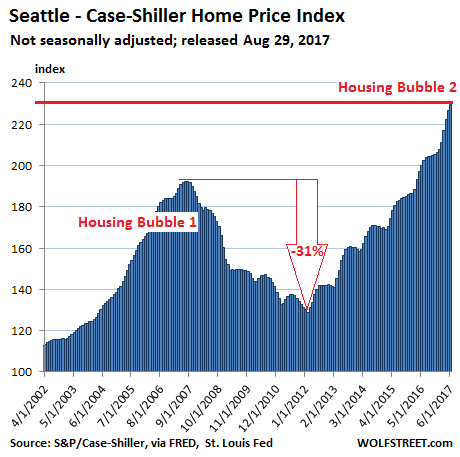

Seattle:

The Case-Shiller home price index for the Seattle metro ticked up a smidgen on a month-to-month basis, after the first two back-to-back declines since the end of 2014! It has now been flat for the past five months. However, flat spots or slight declines in the index this time of the year were not unusual before 2015. The index is up 12.7% year-over-year, 20% from the peak of Housing Bubble 1 (July 2007), and 79% from the bottom of Housing Bust 1 in February 2011:

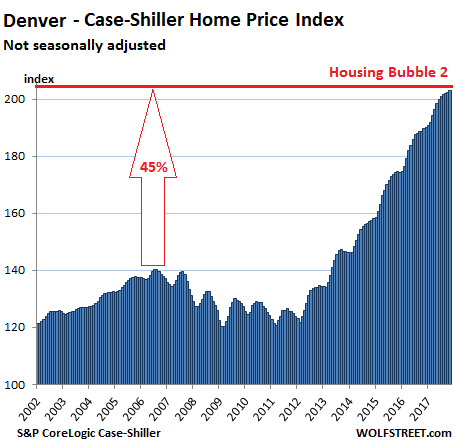

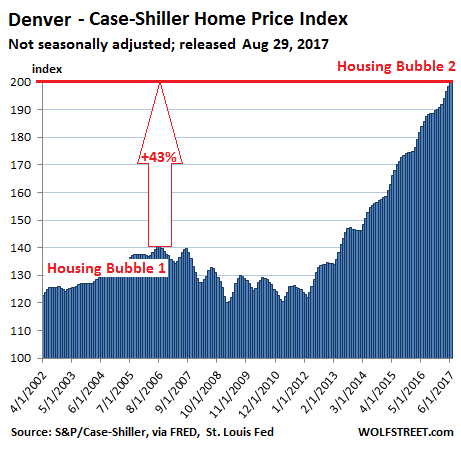

Denver:

The index for the Denver metro ticked up again on a monthly basis, the 25th increase in a row. It is up 7.0% year-over-year and has surged 45% above the prior peak in July 2006. Instead of the craziness of Housing Bubble 1, Denver experienced more “normal” home-price increases, and was therefore also spared the ravages of Housing Bust 1. But in 2012, Housing Bubble 2 erupted in full force:

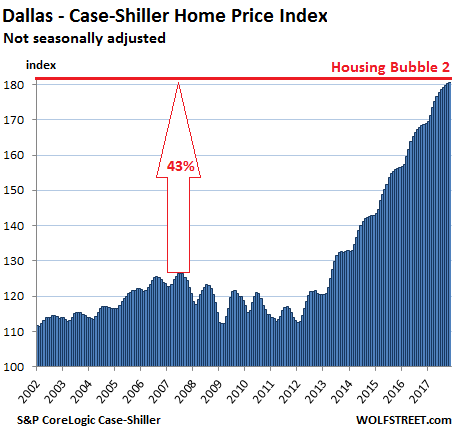

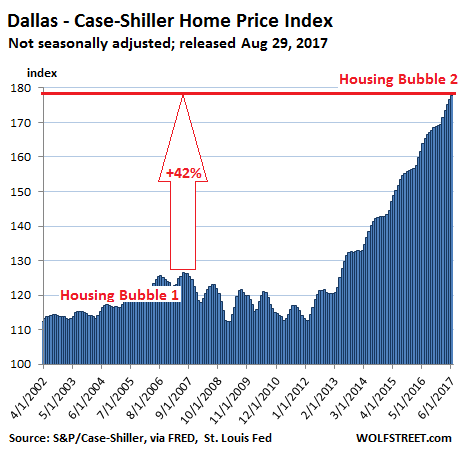

Dallas-Fort Worth:

The index for the Dallas-Fort Worth metro ticked up again on a monthly basis — the 46th month in a row of increases. It is up 7.0% year-over-year and 43% from the prior peak in June 2007. Like Denver, Dallas experienced saner times during Housing Bubble 1. But prices began to surge relentlessly in 2012:

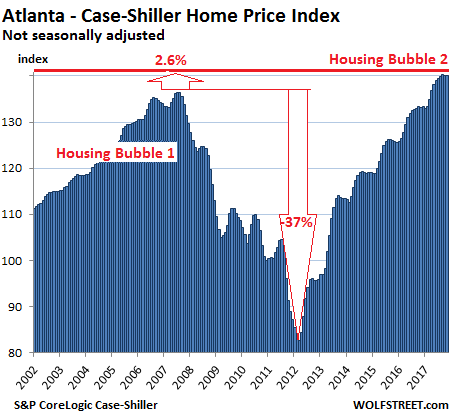

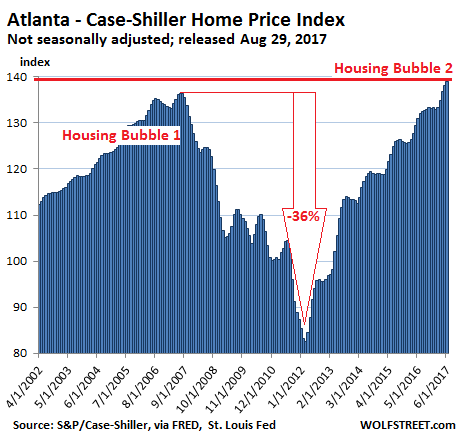

Atlanta:

The home price index for the Atlanta metro has now been flat (actually down a tiny bit) for three months in a row, in line with prior seasonal declines, but is still up 5.2% year-over-year and 2.6% above the peak of Housing Bubble 1 in July 2007. From that peak, the index plunged 37%. It’s now up 70% since February 2012:

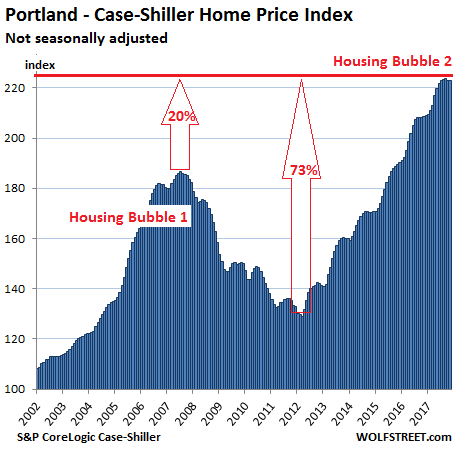

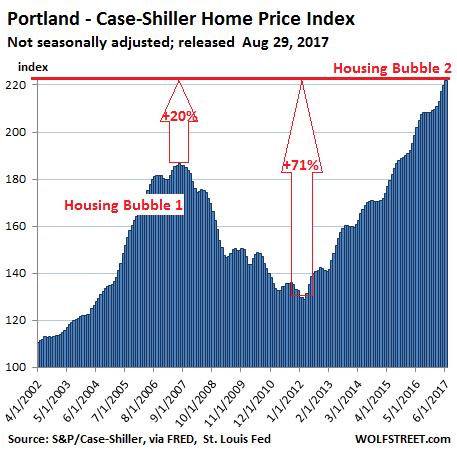

Portland:

The Case-Shiller index for Portland was flat in November, and has now been flat or slightly down for five months in a row, and for now still in the range of normal seasonal patterns. The index is up 6.9% year-over-year and has skyrocketed 73% in five years. It’s 20% above the crazy peak of Housing Bubble 1 and has ballooned 123% since 2000:

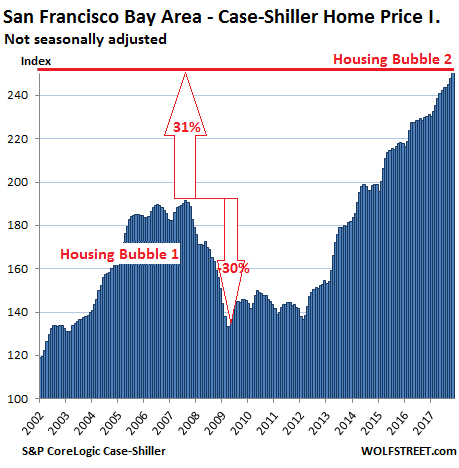

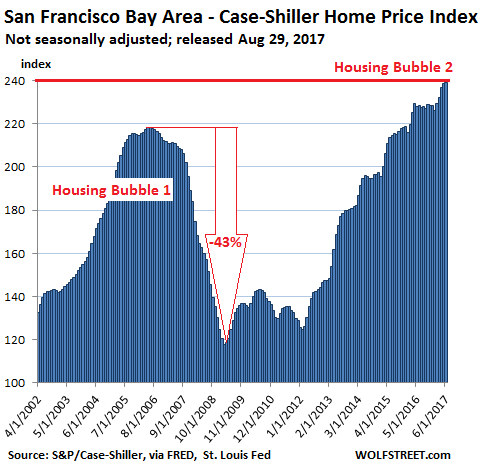

San Francisco Bay Area:

The index for “San Francisco” covers the county of San Francisco plus four other Bay Area counties — Alameda, Contra Costa, Marin, and San Mateo (the northern part of Silicon Valley). It jumped 1.4% for the month, after jumping 1.2% in the prior month. It’s up 9.1% year-over-year, up 31.3% from the insane peak of Housing Bubble 1, and up 85% from the end of Housing Bust 1. The index has surged 151% since 2000:

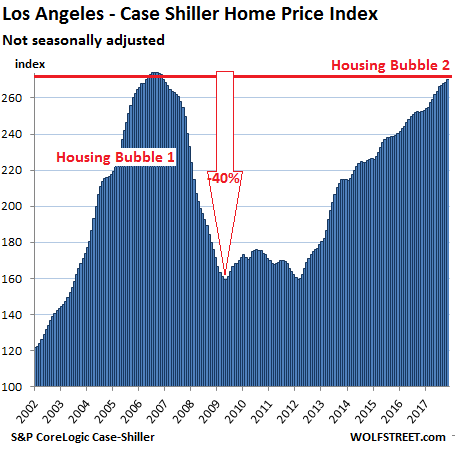

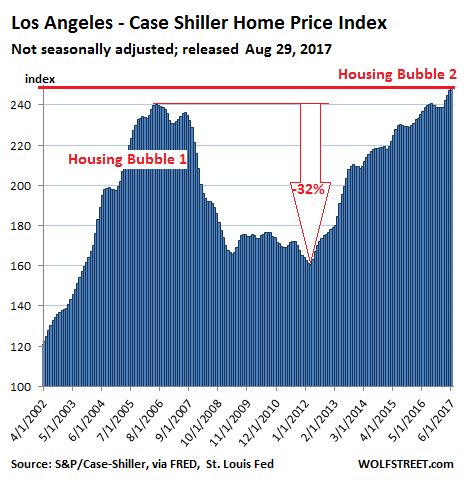

Los Angeles:

Home prices in the Los Angeles metro, as tracked by the index, rose 0.7% for the month, and 7.0% year-over-year. LA’s Housing Bubble 1 was in a category of its own in its steepness on both sides, with home prices skyrocketing 174% from January 2000 to July 2006, before collapsing and surrendering much of the gains. The index has skyrocketed since Housing Bust 1 and is now within a smidgen of the prior insane peak:

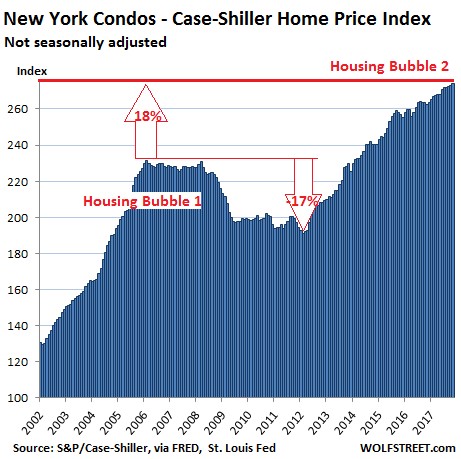

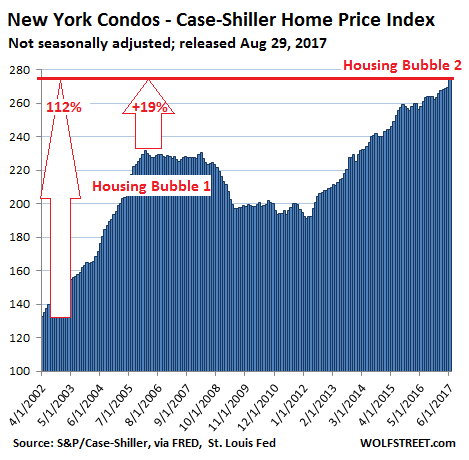

New York City Condos:

Case-Shiller has a special index for New York City’s condo because this is such a vast market. And this index rose another notch in November and is up 4.4% year-over-year. The index soared 131% from 2000 to February 2006 during Housing Bubble 1, barely deflated during the bust before QE unleashed money from around the world which then re-floated Wall Street more than anything else. The index is 18% above the peak of Condo Bubble 1 and has nearly tripled over the past 17 years:

This is asset-price inflation at work — now that “homes” have become a global asset class. These homes didn’t get 50% bigger or 50% nicer over the past few years. Instead the purchasing power of the dollar with regards to these assets has been purposefully demolished by the Fed’s monetary policies that resulted in practically no wage inflation, moderate consumer price inflation, but massive asset-price inflation. Asset-price inflation without corresponding wage inflation means that the value of labor (wages earned) with regards to homes and other assets has been crushed — a phenomenon now hypocritically called the “affordability crisis” in many big urban areas in the US.

The housing market continues to operate in a very lean environment. Home builders are building but are focusing their efforts on multi-family units to cater to agrowing renting population. Builders are also shy about placing big bets given the recent memory of the previous housing bubble. Places where they can build freely like Arizona, Nevada, and Florida are known to pop as quickly as they go up in value. And in areas like California, where NIMBYism rules the day, people are now convinced that prices will never go down so the ratio of bulls to bears is extremely high. The sentiment seems to be that there could be no wrong in purchasing real estate even if it means leveraging up into acrap shack. Yet what is very telling is that inventory is still very low after many years.

Bouncing at the bottom

Inventory has been bouncing near the lows for almost six years now:

Nationwide inventory is down 10 percent year-over-year from an already low year.

In Los Angeles, inventory is down 22 percent year-over-year from an already low year.

What this means for house buyers is that you are going to encounter slim pickings, house lusting shoppers, and a market sentiment favoring sellers. If you are buying, you are not in the driver’s seat. If you are selling, you can command top dollar even for a shantycrap shack.

One thing that has changed since the late 1990s is that we now seem to live in a perpetual boom and bust cycle. Housing being a safe investment that tracks inflation is no longer the case. Real estate is now like a hot stock with big leverage behind it. When things are good, it can be very good. When things go bad, they can turn quickly. And for most people, the challenge in the last housing bust was simply making the mortgage payment. Recessions tend to expose those who are over leveraged in debt.

People seem to think this hot market is because of the current administration which is hard to believe. Timothy Geithner set the markets on fire in 2009 with QE:

Quantitative Easing essentially reversed the market and we have yet to look back since 2009. But this happened nearly a decade ago which is hard to believe. Yet to think all of this euphoria is happening because of current policy is incorrect. And clearly anyone in power is going to leverage positive factors to their side, regardless of party affiliation. But one things is clear and that is things are looking frothy across multiple asset classes.

The housing market is deep into a FOMO stage. There is a deep seated fear now that people will miss out: That$700,000 crap shack will be $1 million. Bitcoin will be $30,000. The Dow will hit 30,000. Everything seems to be going up yet the homeownership rate is stagnant and housing inventory is in the dumps.

The continued drought in inventory means that people will be bidding up crap shacks. The typical home in the US costs $206,000. The typical L.A. home is $632,000. It’ll be interesting to see how much more this market can sustain because the bull fever is definitely out:

The VIX Index shows near record low volatility meaning people expect the party to go on forever. The index nearly looks as low as housing inventory.

The chart does not quite show what MND headline says but the difference is a just a few basis points. I suspect rates inched lower just after the article came out.

For the past few weeks, rates made several successive runs up to the highest levels in more than 9 months. It was really only the spring of 2017 that stood in the way of rates being the highest since early 2014. After Friday marked another “highest in 9 months” day, it would only have taken a moderate movement to break into the “3+ year” territory. The move ended up being even bigger.

From a week and a half ago, most borrowers are now looking at another eighth of a percentage point higher in rate. In total, rates are up the better part of half a point since December 15th. This marks the only time rates have risen this much without having been at long term lows in the past year. For example, late 2010, mid-2013, mid-2015, and late 2016 all saw sharper increases in rates overall, but each of those moves happened only 1-3 months after a long term rate low.

Not a Drill

So far this month, MBS have stunningly dropped over 200 bps, which easily translates into a .5% or more increase in rates. I’ve been shouting “lock early” for quite a while, and this is precisely why, This isn’t a drill, or a momentary rate upturn. It’s likely the end of a decade+ long bull bond market. LOCK EARLY. -Ted Rood, Senior Originator

Housing Bust Coming

Drill or not, if rising rates stick, they are bound to have a negative impact on home buying.

In the short term, however, rate increases may fuel the opposite reaction people expect.

Why?

Those on the fence may decide it’s now or never and rush out to purchase something, anything. If that mentality sets in, there could be one final homebuilding push before the dam breaks. That’s not my call. Rather, that could easily be the outcome.

Completed Homes for Sale

Speculation by home builders sitting on finished homes in 2007 is quite amazing.

What about now?

Supply of Homes in Months at Current Sales Rate

Note that spikes in home inventory coincide with recessions.

A 5.9 month supply of homes did not seem to be a problem in March of 2006. In retrospect, it was the start of an enormous problem.

In absolute terms, builders are nowhere close to the problem situation of 2007. Indeed, it appears that builders learned a lesson.

Nonetheless, pain is on the horizon if rates keep rising.

Price Cutting Coming Up?

If builders cut prices to get rid of inventory, everyone who bought in the past few years is likely to quickly go underwater.

For the 29th month in a row, US home prices rose at a faster pace than incomes with November prices rising a better than expected 6.41% – the highest since July 2014.

The 20-City Composite rose 6.41% YoY in November (above the 6.30% expectations)

The 20-City Composite price index is within 1% of its record highs from 2006…

It is safe to say that one of the most popular, and important, charts of 2017, was the one showing the ongoing and projected decline across central bank assets, which from a record expansion of over $2 trillion in early 2017 is expected to turn negative by mid 2019. This is shown on both a 3- and 12-month rolling basis courtesy of these recent charts from Citi.

The reason the above charts are key, is because as Citi’s Matt King, DB’s Jim Reid, BofA’s Barnaby Martin and countless other Wall Street commentators have pointed out, historically asset performance has correlated strongly with the change in central bank balance sheets, especially on the way up.

As a result, the big question in 2017 (and 2018) is whether risk assets would exhibit the same correlation on the way down as well, i.e. drop.

We can now say that for credit the answer appears to be yes, because as the following chart shows, the ongoing decline in CB assets is starting to have an adverse impact on investment grade spreads which have been pushing wider in recent days, in large part due to the sharp moves in government bonds underline the credit spread.

And, what is more important, is that investors appear to have noticed the repricing across credit. This is visible in two places: on one hand while inflows into broader credit have remained generally strong, there has been a surprisingly sharp and persistent outflow from US high yield funds in recent weeks. These outflows from junk bond funds have occurred against a backdrop of rising UST yields, which recently hit 2.67%, the highest since 2014, another key risk factor to credit investors.

But while similar acute outflows have yet to be observed across the rest of the credit space, and especially among investment grade bonds, JPM points out that the continued outflows from HY and some early signs of waning interest in HG bonds in the ETF space in the US has also been accompanied by sharp increases in short interest ratios in LQD (Figure 13), the largest US investment grade bond ETF…

… as well as HYG, the largest US high yield ETF by total assets,

This, together with the chart showing the correlation of spreads to CB assets, suggests that positioning among institutional investors has turned markedly more bearish recently.

Putting the above together, it is becoming increasingly apparent that a big credit-quake is imminent, and Wall Street is already positioning to take advantage of it when it hits.

So what about stocks?

Well, as Citi noted two weeks ago, one of the reasons why there has been a dramatic surge in stocks in the new years is that while the impulse – i.e., rate of change – of central bank assets has been sharply declining on its way to going negative in ~18 months, the recent boost of purchases from EM FX reserve managers, i.e. mostly China, has been ahuge tailwind to stocks.

This “intervention”, as well as the recent retail capitulation which has seen retail investors unleashed across stock markets, buying at a pace not seen since just before both the 1987 and 2008 crash, helps explain why stocks have – for now – de-correlated from central bank balance sheets. This is shown in the final chart below, also from Citi.

And while the blue line and the black line above have decoupled, it is only a matter of time before stocks notice the same things that are spooking bonds, and credit in general, and get reacquainted with gravity.

What happens next? Well, if the Citi correlation extrapolation is accurate, and historically it has been, it would imply that by mid-2019, equities are facing a nearly 50% drop to keep up with central bank asset shrinkage. Which is why it is safe to say that this is one time when the bulls will be praying that correlation is as far from causation as statistically possible.

Hackers able to make ATMs spit cash like winning slot machines are now operating inside the United States, marking the arrival of “jackpotting” attacks after widespread heists in Europe and Asia, according to the world’s largest ATM makers and security news website, Krebs on Security.

Thieves have usedskimming deviceson ATM machines to steal debit card information, but “jackpotting” augurs more sophisticated technological challenges that American financial firms will face in coming years.

“This is the first instance of jackpotting in the United States,” said digital security reporter Brian Krebs, a former Washington Post reporter. “It’s safe to assume that these are here to stay at this point.”

On his website, KrebsreportedSaturday that the Secret Service has warned financial institutions about “jackpotting” attacks in the past few days, though specifics have not been revealed.

He cites an alert sent by ATM maker NCR Corp. to its customers:

“This represents the first confirmed cases of losses due to logical attacks in the U.S.,” the alert read. “This should be treated as a call to action to take appropriate steps to protect their ATMs against these forms of attack and mitigate any consequences.”

Krebsreportedthat criminal gangs are targeting Diebold Nixdorf ATM machines — the stand-alone kind you might see in a drive-through or pharmacy. He shared the ATM giant’ssecurity notice. It described similar attacks in Mexico, in which criminals used a modified medical endoscope to access a port inside the machines and install malware. Diebold is also one of the largest manufactures of eVoting machines, based upon the same software as their casino slot machines and ATM’s used throughout the Americas and Western Europe.

Both ATM makers confirmed toReutersthat they sent out alerts.

Diebold Nixdorf spokesman Mike Jacobsen declined to provide the number of banks targeted in Mexico and the United States or comment on losses, according toReuters.

Hackers have also been reported to remotely infect ATMs or completely swap out their hard drives. The Secret Service could not be immediately reached for comment about the nature of the reported U.S. attacks.

Whichever method is used, the results are about the same. At a hacker conference in 2010,Wired reported, a researcher brought two infected ATMs to the stage and gave a demonstration.

Over the span of 2000-2016, the amount of money spent on food by the average American household increased from $5,158 to $7,203, which is a 39.6% increase in spending.

Despite this,as Visual Capitalist’s Jeff Desjardins notes, for most of the U.S. population, food actually makes up a decreasing portion of their household spending mix because of rising incomes over time. Just 13.1% of income was spent on food by the average household in 2016, making it a less important cost than both housing and transportation.

That said, fluctuations in food prices can still make a major impact on the population. For lower income households, food makes up a much higher percentage of incomes at 32.6% – and how individual foods change in price can make a big difference at the dinner table.

FLUCTUATING GROCERY PRICES

Today’s infographic comes from TitleMax, and it uses data from the Bureau of Labor Statistics to show the prices for 30 common grocery staples over the last decade.

‘No one can predict the future, but everyone can predict the futures’

The CME (NASDAQ:CME) and Cboe/CFE (NASDAQ:CBOE), two large, well respected, USA regulated futures exchanges, recently started trading Bitcoin futures. These venues make it possible to trade on Bitcoin’s value without being exposed to the uncertainties of the mostly unregulated Bitcoin exchanges.

To understand Bitcoin futures you need to recognize, among some other things, that these futures are not in the business of predicting Bitcoin’s price.

Bitcoin Futures are Not Trying to Predict the Future!

It’s reasonable to assume that a product named a future is attempting to predict the future. For Bitcoin futures, this is definitely not what they deliver. The core utility of the futures markets is not predicting the future prices of their product but rather the secure delivery of a product at a known price, quality, and date. If there’s product seasonality (e.g., specific harvest times) or foreseeable shortages/abundances then future’s prices may reflect that but neither of these factors applies to Bitcoin.

I’m not saying that Bitcoin futures won’t be used by speculators making bets on Bitcoin-they certainly will be- but when you see Bitcoin futures trading higher or lower than the current Bitcoin exchange values (spot value) it’s not a prediction-it’s a reflection of the inner workings of the futures market.

How Are Bitcoin futures prices established?

If you look at the quotes for Bitcoin futures you’ll see at least three things, the expiration code (shorthand for a specific expiration date ) the bid (buy price) and the ask (sell price). If you’re ever confused as to which one to use in your situation it’s easy to sort out-start with the price that’s worse for you.

Important agents interacting with those prices are operating in one of three roles: individual speculator, market maker, or arbitrageur. A key role is market maker-a firm that has agreed to simultaneously act as both a buyer and seller for a specific security. When companies sign up for this role they agree to keep the bid/ask prices relatively close to each other-for example even if they aren’t keen on selling Bitcoins at the moment they can’t just set the ask price to an outrageous level. The agreed-upon maximum bid/ask ranges might be tied to market conditions (e.g., wider when deemed a “fast market”) and might allow time-outs but in general, the market maker agrees to act as a buffer between supply and demand.

The Market Makers:

The existence of market makers (e.g.,Virtu Financial) refutes a common assertion about futures-that there’s always a loser for every winner, that it’s a zero-sum game. It’s true that derivatives like stock options and futures are created in matched pairs-a long and a short contract. If two speculators own those two contracts the profits on one side are offset by losses on the other but market makers are not speculators. In general, they’re not betting on the direction of the market. They act as intermediaries, selling to buyers at the higher ask price and buying from sellers at the lower bid price- collecting the difference.

Market makers are challenged in fast markets-when either buyers or sellers are dominating and prices are moving rapidly. When this happens market makers are obligated to continue quoting bid and ask prices that maintain some semblance of an orderly market. If they start accumulating uncomfortably large net long or short inventories they may start hedging their positions to protect themselves. For example, if they are short Bitcoin futures they can buy Bitcoin futures with different expirations or directly buy Bitcoins to hedge their positions. The hedged portion of the market maker’s portfolio is not sensitive to Bitcoin price movements-their profit/losses on the short side are offset by their long positions.

The market maker’s ability to hedge out their exposure demonstrates that futures aren’t inherently a zero sum gain. They can accommodate the market and still be profitable-regardless of the market’s direction.

The Arbitrageur:

The arbitrageur is hyper-focused on the price difference between the Bitcoin future and the exchange price. If those prices differ enough they can lock in risk-free profits. You can imagine how much capital is available if risk-free profits are in the offing…

The arbitrageur very carefully calculates the costs of buying or shorting Bitcoin futures while selling short or buying actual Bitcoins.

These calculations include

Time value of money required for margin deposits

Fees

Transaction costs (bid/ask spread)

Contract expiration settlement price risk (Bitcoin futures are cash settled)

Borrow costs for shorting Bitcoin if going short

The amount of profit that their bosses expect from them.

Normally commodity futures arbitrageurs have to account for things like storage costs (e.g. warehouses, silos), insurance (in-case the storage facility is robbed or burns down), and seasonal price variations but none of these apply to Bitcoin, so somewhat ironically the crazy Bitcoin market is simpler for them.

Knowing their estimated costs and profit requirements the arbitrageur determines a minimum difference they need between the futures’ prices and the spot price before they will enter the market. They then monitor the price difference between Bitcoin futures and the Bitcoin exchanges and if large enough they act to profit on that gap. For example, if a specific Bitcoin future (e.g., February contract) is trading sufficiently higher than the current Bitcoin exchange price they will short that Bitcoin future and hedge their position by buying Bitcoins on the exchange. At that point, if they have achieved trade prices within their targets, they have locked in a guaranteed profit. They will hold those positions until contract expiration (or until they can cover their short futures and sell Bitcoins at a profit).

They’ll do the complementary transaction if the price of a specific future is enough lower than spot price. They’ll buy futures and short Bitcoins to lock in profits in that case.

Arbitrageurs provide a critical role in futures markets because they’re the adults in the room that keep futures prices attuned to Bitcoin exchange prices. If there are multiple futures providers (Cboe and CME in this case) they’ll also act to keep the futures from the various exchanges aligned with each other.

If Bitcoin futures prices get too high relative to spot arbitragers are natural sellers and if the futures prices get too low they are natural buyers. Their buying and selling actions naturally counteract price distortions between markets. If they’re somehow prevented from acting (e.g., if shorting Bitcoin was forbidden) then the futures market would likely become decoupled from the underlying spot price-not a good thing.

The Term Structure:

A key attribute of a futures market is how its contract’s prices vary by expiration date. The succession of futures prices over time is called the “term structure”. If supply is stable (no seasonality or shortages) then typically futures prices will increase with expirations further in the future. This term structure configuration is called “contango” and it accounts for the fact that carry costs (e.g., time value of money) and profit expectations increase with time. Unless there are big changes in interest rates or the way that Bitcoin exchanges work I expect the level of contango in the Bitcoin futures term structure to be small. Bitcoins don’t cost much to hodl (once you have your hardware wallet) and there’s no apparent seasonality. The chart below from VIX Central shows a typical Bitcoin term structure (click on chart to get current data):

Click chart for interactive version.

Cboe vs CME: Sizes & Settlement:

There are two USA regulated Bitcoin futures exchanges in operation. TheCME’s contractunit is five Bitcoins whereas theCboe’s contractunit is one-that’s the biggest difference between these futures. The upfront money to buy or sell short a CME contract will be about five times higher than the Cboe contract. Larger investors won’t care but this will be an issue for smaller investors. Another difference is the spot/settlement process that the exchanges use. In the case of Cboe futures, the contracts will be settled to a 4 pm ETGemini exchange auction priceon the day of expiration, for the CME futures the settlement price is acomplex calculationusing an hour of volume weighted data from multiple exchanges (currently Bitstamp, itBit, Kraken, and GDAX). With the CME’s approach, it will be harder to manipulate the settlement price but it doesn’t give arbitrageurs a physical mechanism to trade their positions-possibly an issue.

There’s nothing to prevent people from closing out their contracts before final settlement but typically there is some premium remaining until the very end.

Unlike many commodity futures, Bitcoin futures are cash settled rather than physically settled. Cash settlement is a relatively new development in futures trading,first introduced in 1981for Eurodollar futures, that addresses the problem of how to settle futures contracts on things that are difficult/impossible to deliver physicially-things like interest rates, large stock indexes (e.g., S&P 500), and volatility indexes (Cboe’s VIX). Futures physical settlement involves actual shipment/change of ownership of the underlying product to the contract holder but in practice, it’s rarely used (~2% of the time). Instead, most organizations that are using futures to hedge prices of future production/usage will make separate arrangements with suppliers/customers for physical delivery and just use the futures to protect against contrary price changes. In practice, the final settlement price of the contract can be used to provide the desired price protection regardless of whether the futures contract specifies physically delivery or cash-settlement.

While “physical” delivery of Bitcoins as part of a futures contract would certainly be possible it raises regulatory and security issues in today’s environment where the cybercurrency exchanges are mostly unregulated, somewhat unreliable, and theft due to security hacks is distressingly common. By selecting cash settlement the CME and Cboe completely avoid the transfer of custody issues and shift those problems to somebody else-namely the market makers and arbitrageur.

Leverage:

One traditional attraction of trading futures is the ability to use relatively small amounts of money to potentially achieve outsized returns. In many futures markets the margin, the amount of money that your broker requires up-front before executing the trade can be quite small compared to the ultimate value of the contract. For example, as of 22-Dec-2017, each E-mini S&P 500 contract was worth $134K ($50*S&P 500 index value)-this “list price” of the contract is called its notional value. The CME only requires you to maintain a minimum margin of $4.5K (3.4% of notional) to control this contract (brokers often require additional margin). Margin requirements this low are only possible because the volatility of the S&P 500 is well understood and your margin account balance is adjusted at the end of every trading day to account for the winnings or losses of the day. If your account balance falls below the margin minimum of $4.5K you’ll need to quickly add money to your account or your position will be summarily closed out by your broker. On the plus side, if you’ve predicted the S&P’s direction correctly your profits will be that same as if you completely owned the underlying stocks in the index. A +1% daily move in the S&P500 would yield $1340 in profit even though you only have $4500 invested- a 29% return-this multiplier effect is called leverage.

Currently, Bitcoin futures have very high margin requirements. The Cboe requires 40% of the notional amount formaintenance margin, the CME requires 43%. Your broker will likely require more than that. The culprit behind these high requirements is Bitcoin’s high volatility-until that calms down the exchanges will protect themselves by requiring a bunch of up-front money. If you don’t come up with the money for a margin call they want to close out your position without leaving a negative balance.

Because of the high margin requirements, Bitcoin futures don’t offer much leverage compared to just buying Bitcoins outright. However, Bitcoin futures do offer the trader time-tested exchanges that are not nearly as susceptible to hacks, thefts, and unscheduled downtime.

Conclusion:

In the movie “Trading Places,” there’s awild scenewhere fortunes are made and lost in the orange juice future pit ina matter of minutes. This scene epitomizes what most of us envision futures trading to look like. The movie depicts a situation where the supply of oranges from the next harvest is unknown-and that is the source of the craziness.

Bitcoins don’t have seasonal variabilities-supply as it’s quantity is always known. This supply stability makes Bitcoin futures a lot less dramatic but in the case of Bitcoins this is a real plus-there’s already plenty of drama in the exchanges-the futures market will be the safe and quiet space. A different sort of trading places with guys like this …

Following yesterday’sdisastrous drop in existing home sales(due to record low supply), new home sales plunged 9.3% MoM after November saw its biggest surge since Jan 1992, revised dramatically lower.

The November 17.5% spike was revised dramatically down to 15.0% spike – the highest since 1993 but December’s 9.3% plunge was already worse than the expected 7.9% giveback…

Biggest MoM drop since Aug 2016.

In fact the downward revisions are huge… October from 624K to 599K; November from 733K to 689K

As good as it gets?

While the blame is immediately laid on weather, the regional drops show that is simply not correct:

Purchases fell in all four U.S. regions, led by a 10 percent drop in the Midwest and a 9.8 percent slide in the South.

Median Home Prices reached a new record high…at $335,400

As Bloomberg notes, new-home sales, tabulated when contracts get signed, account for about 10 percent of the market. They’re considered a timelier barometer than purchases of previously owned homes, which are calculated when contracts close and are reported by the National Association of Realtors.

But the ongoing lack of supply remains the most notable aspect in the US housing ‘recovery’.

Alhambra’s Jeffrey Snider notescritically that it’s what’s going on underneath the headline that really matters (as always). The reluctance of Americans to sell their houses has become such a contradiction to the attempt to paint the housing market, and therefore the overall economic condition, as healthy, even robust. Prices are rising, in some places quickly. Yet, inventory of available-for-sale homes continues to decline, sharply once again in December.

It’s a glaring dichotomy that ever the NAR’s Chief Economist, Larry Yun, has been forcedto grudgingly address.

Existing sales concluded the year on a softer note, but they were guided higher these last 12 months by a multi-year streak of exceptional job growth, which ignited buyer demand. At the same time, market conditions were far from perfect. New listings struggled to keep up with what was sold very quickly, and buying became less affordable in a large swath of the country. These two factors ultimately muted what should have been a stronger sales pace.

It’s the “exceptional job growth” premise that leads toward only confusion. It’s one of those terms, like “globally synchronized growth” or “economic boom”, that refers quite differently to only the mainstream depiction of the economy, the one that has been consistently overoptimistic about things for a decade. The actual data suggests an entirely separate set of circumstances, which is where all this misunderstanding comes in.

In truth, falling inventory is quite easily explained, and in a way that is perfectly consistent with labor market and national (labor) income statistics as they are. The BLS outside of the unemployment rate, which, for the nth time doesn’t include Americans who would work if there was work, actually has been describing a consistently and persistently slowing labor market. The timing of where that started matches with where resale inventory began to contract.

There is actually a big difference between an average payroll gain of 150k and 250k; the latter is barely minimal, while the former is what panicked the Fed into launching QE3 in 2012. Last year was by every reasonable measure not even close to a good one for American workers.

The primary effect of sluggish, constrained payroll expansion, along with parallel effects in other labor factors, is weakened aggregate income. Even people who are working start to become uncertain or even fearful when the jobs market as a whole slows down – and not just slows, but continues to decelerate year after year (after year). This trend will be starting its fourth year. At that length, workers and prospective workers become quite certain about their general uncertainty.

If your ground-level view of the jobs environment and therefore economy is far more unsteady and dour than exceptional, you are not going to be as sure about selling your existing home to move up, taking on a larger monthly payment in the process. The more people like you who pass on the opportunity to cash in on higher prices, the more that says this is a widespread view quite different from the narrative established in consumer sentiment surveys and what news outlets write about in their headlines.

The economy is what actually happens, not what people think other people think Economists say is happening. Talk isn’t cheap, it’s wayovervalued.

A little over a year ago, home prices finally surpassed their prior all-time highs, reached during the heyday of the housing bubble back in 2006.

But with home prices in 80% of US cities are growing twice as fast as wages, working-class families across the US are finding it increasingly difficult to support their families – let alone afford a home. But fortunately, this hasn’t been a problem for institutional investors like Blackstone, which are presently enjoying the luxury of a controversial valuation assessment known as a Broker Price Opinion – or BPO.

As the Wall Street Journalexplains, Congress prohibited the use of BPOs to underpin traditional mortgages as part of Dodd-Frank. But, fortunately for private-equity firms and their limited partners, that prohibition doesn’t apply to investors buying tens of thousands of homes.

Blackstone and its lender, Deutsche Bank AG, settled on a sort of drive-by valuation done by real-estate agents that are more cursory and cost far less than traditional appraisals.

Congress outlawed the use of such assessments, called broker price opinions, or BPOs, to value properties for traditional mortgages. But the prohibition, enacted as part of postcrash financial regulation, doesn’t apply to investors buying tens of thousands of houses.

Now these perfunctory valuations abound, underpinning tens of billions of dollars of home deals. Sometimes the process is outsourced to India, where companies charge real-estate agents a few dollars to come up with U.S. home values by consulting Google Earth and real-estate websites.

That’s right: Shoddy satellite photos and workers at call centers in India – thousands of miles away from the homes they’re evaluating – are making up prices for homes that are then used to value collateral used in bond offerings. In fact, BPOs have been used to value collateral in the more than $20 billion of bonds sold by institutional landlord. They’re also thefast-growing business of lending to individual house flippers. Banks request them when considering whether to foreclose or negotiate repayment plans with delinquent homeowners.

Their popularity shows how Wall Street is finding ways to adapt to government efforts to crack down on some of the excesses that contributed to the housing crisis. Whileauthorities in Canada and Australiahave passed laws to curb speculation in their respective housing markets, US regulators have been unwilling to challenge BPOs – though the SEC is investigating whether certain rental-home companies used these shoddy valuations to distort the value of bonds tied to the deal. Critics say BPOs are ill-suited to gauge home values and could leave debt holders with less collateral than they thought.

So what are the risks, exactly? Well, inaccurate pricing information could result in abrupt and unexpected losses for investors when a more thorough appraisal is sought.

“BPOs are a creature of financial institutions that want deals to close fast, and so they don’t have to use an appraiser,” said Donald Epley, a retired University of South Alabama professor who helped write national appraisal standards after the 1980s savings-and-loan collapse. “You’re just dumbing down the standards to make the loan.”

Some credit rating firms have realized that these valuations aren’t reliable, and have stopped accepting them, or sought a second opinion.

When Fannie Mae last year guaranteed about $1 billion of Invitation Homes debt, it accepted BPOs for the 7,204 houses serving as collateral. Assuming a typical appraisal price of $450 and the $95 that Invitation Homes pays per BPO, the company saved about $2.6 million.

Credit-rating firms usually discount BPO values when grading rent-backed bonds. Kroll Bond Rating Agency has trimmed them by about 10% and uses the lower of the reduced BPOs and the amounts spent buying and renovating the homes.

“We’re never taking BPOs at face value,” said Kroll’s Daniel Tegen.

With many institutional investors expect, as Goldman Sachs put it, “a strong and synchronous global expansion” during the coming year, housing bears are difficult to come by. But Bloomberg managed to find one: James Stack, an investor who manages $1.3 billion for high net worth individuals, says that his “Housing Bubble Bellwether Barometer” is flashing red again. Stack predicted the housing crash back in 2005, just as home prices were reaching their peak.

His assessment of the market should send a chill down the spine of foreign investors who have poured money into New York City, San Francisco and other hot urban housing markets that have led the recovery in home valuations.

“It is 2005 all over again in terms of the valuation extreme, the psychological excess and the denial,” said Stack, whose fireproof files of newspaper articles on bear markets date back to 1929. “People don’t believe housing is in a bubble and don’t want to hear talk about prices being a little bit bubblish.”

Despite the torrid rally in home prices, Stack is one of the few real-estate market observers who foresee a sizable correction in prices. Indeed, as the vital spring selling season approaches, there are plenty of reasons for buyers to be optimistic – not the least of which is the “wealth effect” stemming from gains in equity prices. A backup in home building following the recession has left a paucity of inventory just as the housing needs of two generations – millennials who are buying their first homes and Baby Boomers who are downsizing in retirement – are shifting.

But there’s a structural mismatch between different tiers of the housing market that are poised to create problems for home builders.