San Diego County’s median home price hit its highest price in history in July, $579,750, while sales hit a four-year low, real estate tracker CoreLogic reported Thursday.

The previous record was$575,000 in May.Home prices have been breaking records on nearly a month-to-month basis all year. As of July, home prices had increased 8 percent in a year — the most of any Southern California county.

Home sales hit its lowest point in years in July with 3,607 sales. The last time sales were that low was July 2014, when the county was still coming out of the housing bust, when there were 3,530 sales.

Affordability constraints for many potential buyers could be the reason why sales are so low despite more homes on the market, said CoreLogic analyst Andrew LePage in the monthly report.

“The overall trend in recent months has been toward more listings,” he wrote, “suggesting that sales also remain weak relative to current housing demand because more and more would-be buyers are unable or unwilling to buy.”

Home inventory has increased slightly in recent months, but it is still below levels reached in years past, said data from the Greater San Diego Association of Realtors. There were 7,613 homes listed for sale in July, up from July 2016 when 5,828 homes were for sale, and 6,571 homes for sale in July 2015.

In 2010, during the Great Recession, there were as many as 13,000 homes on sale in a given month.

In July, resale single-family homes tied the peak median of $630,000 reached in June with 2,314 sales. Resale condos hit their highest ever median of $432,000 with 1,080 sales. The median for newly built homes was $703,750, but was limited to 213 sales.

San Diego County’s 8 percent increase in a year outpaces the rest of the region, but it is still a cheaper option for coastal California.

Orange County home prices were up 6.6 percent in a year with a median of $735,750, Ventura County prices were up 6.3 percent for a median of $595,000 and Los Angeles County increased 5.7 percent for a median of $607,500.

Interior counties’ median home price increases still did not keep up with San Diego. In San Bernardino County, home prices were up 6.6 percent for a median of $325,000 and up 5.8 percent in Riverside County for a median of $386,000.

Dana Kuhn, real estate lecturer at San Diego State University, said affordability constraints and the number of people leaving the region for cheaper areas may slow the price increases. He said declining sales will not be the best indicator that sales are starting to slow down.

“The better indicator of that will be rising inventory of homes for sale and longer market times for those offered,” Kuhn said.

While inventory of homes is increasing, days on market still tends to be very quick. Based on a 12-month rolling average, the average days it took for a San Diego County home to sell in July was 28, down from 31 at the same time last year.

Condos from $250,001 to $500,000 sold the fastest, staying on the market 21 days.

Investors are still finding value in the San Diego market. Absentee buyers, typically investors who don’t intend on living in the home as a primary residence, made up 20.1 percent of sales in July, up from 19.4 percent of sales at the same time last year. In early 2013, more than 30 percent of sales went to absentee buyers.

For areas with at least 10 sales, Solana Beach (92075) had the biggest price increase for single-family resale homes in a year at 41 percent for a median of $1.8 million. It was followed by Coronado (92118) with an increase of 32 percent and a median of $2.4 million and Cardiff (92007) with an increase of 31 percent with a median of $1.1 million.

For resale condos, Oceanside (92054) had the biggest yearly increase at 50 percent with a median of $566,000. It was followed by Clairemont (92117) with a 37 percent increase and a median of $475,000 and Encinitas (92024) with a 32 percent increase and a median of $641,000.

When adjusting for inflation, San Diego County’s home price has still not reached its pre-housing crash price. In November 2005, the median hit $517,500, which would be nearly $660,000 today.

Following the drop in Existing- and New-home sales (as well as another drop in mortgage apps), Pending-home sales missed expectations dramatically, dropping 0.7% MoM in July (+0.3% exp).

This is the seventh straight month of annual declines in pending home sales…

Lawrence Yun, NAR chief economist, says the housing market’s summer slowdown continued in July.

“Contract signings inched backward once again last month, as declines in the South and West weighed down on overall activity,” he said.

“It’s evident in recent months that many of the most overheated real estate markets – especially those out West – are starting to see a slight decline in home sales and slower price growth.”

Yun blames affordability (and supply)…

“The reason sales are falling off last year’s pace is that multiple years of inadequate supply in markets with strong job growth have finally driven up home prices to a point where an increasing number of prospective buyers are unable to afford it.”

The US housing data just keeps getting worse…

Again as we noted previously, none of this should come as a huge surprise since

Sentiment for Home-Buying Conditions are the worst since Lehman…

With The Fed set on its automaton hiking trajectory, we suspect home sales will continue to lag.

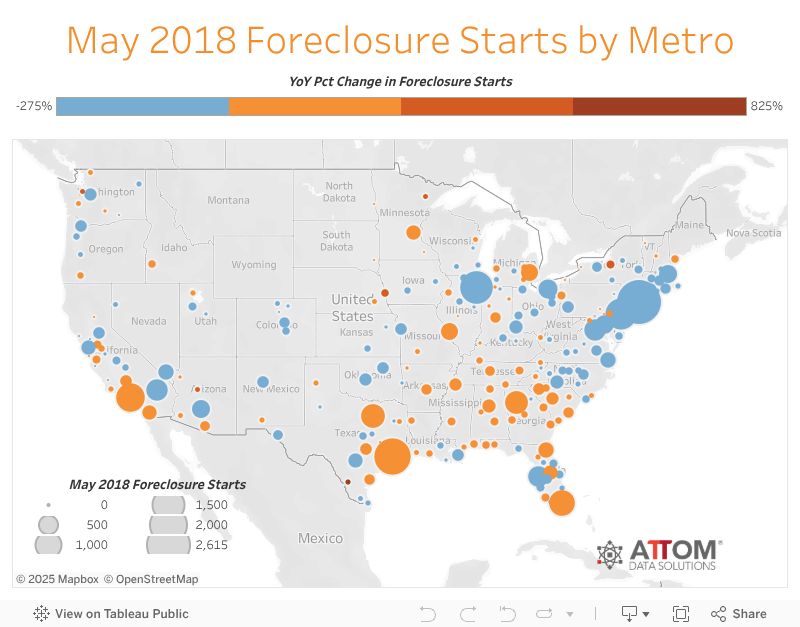

One month ago we discussed why according to the recent data, the “Housing Market Headed For “Broadest Slowdown In Years.” Fast forward to today, when we received the latest confirmation that the US housing market appears to have recently hit a downward inflection point: according to the just released July 2018 U.S. Foreclosure Market Report released byATTOM Data Solutions, foreclosure starts in July increased by 1% from a year ago — the first year-over-year increase following 36 consecutive months of decreases.

Foreclosures rose from a year ago in 96 of the 219 metropolitan statistical areas, or 44% of the markets analyzed in the report; 33 of those areas posted their third straight monthly increase. A total of 30,187 U.S. properties started the foreclosure process for the first time in July, up 1 percent from the previous month and while the increase was less than 1% from a year ago, it marked the first annual increase in exactly 3 years.

21 states posted a year-over-year increase in foreclosure starts in July, including Florida (up 35 percent); California (up 3 percent); Texas (up 7 percent); Illinois (up 7 percent); and Ohio (up 2 percent).

Metro areas posting year-over-year increases in foreclosure starts in July included Los Angeles, California (up 20 percent); Houston, Texas (up 76 percent); Philadelphia, Pennsylvania (up 10 percent); Miami, Florida (up 29 percent); and San Francisco, California (up 10 percent).

“The increase in foreclosure starts is not just a one-month anomaly in many local markets given that July represented the third consecutive month with a year-over-year increase in 33 metro areas, including Los Angeles, Miami, Houston, Detroit, San Diego and Austin,” said Daren Blomquist, senior vice president with ATTOM Data Solutions.

“Gradually loosening lending standards over the past few years have introduced a modicum of risk back into the housing market, and that additional risk is resulting in rising foreclosure starts in a diverse set of markets across the country. Most susceptible to rising foreclosure starts are affordability-challenged markets where home buyers are more financially stretched and markets with some type of trigger event such as a natural disaster or large-scale layoffs.”

The data comes shortly after aseparate reportfound that there has been a plunge of sales in ultra-luxury real estate in New York City, where apartments that cost $5 million or more have seen their sale plunge more than 31% in the first 6 months of the year.

The surprising reversal in the US housing sector comes at a time when the US economy is reportedly firing on all four cylinders, with the stock market at all time highs and not long after the Department of Commerce revised income and spending data to “discover” that US households had actually saved twice as much as previously expected. Which begs the question: is the rise in interest rates a sufficiently adverse development to offset all the other favorable trends in the economy, or is something more sinister – and unknown – taking place in the US economy.

As a reminder it is housing – and not financial markets or stocks – that has traditionally been the most relevant, and aspirational, asset for the US middle class and as such is the best indicator of economic prosperity (or lack thereof) for a majority of the US population. And recent trends are anything but optimistic.

After June’s dismal US housing data, hope was high for a rebound in July but it was crushed as existing home sales tumbled 0.7% MoM (against expectations of a 0.4% jump). This is the longest streak of declines since the taper tantrum in 2013.

Single-family home sales fell 0.2% MoM (-1.2% YoY) to annual rate of 4.75 million

Purchases of condominium and co-op units dropped 4.8% MoM (-3.3% YoY) to a 590,000 pace

As lower-priced home sales collapsed…

This is the weakest SAAR existing home sales (5.34mm) since Feb 2016…

The median sales price increased 4.5% YoY to $269,600, but dipped MoM (seasonal norm)

Lawrence Yun, NAR chief economist, says the continuous solid gains in home prices have now steadily reduced demand.

“Led by a notable decrease in closings in the Northeast, existing home sales trailed off again last month, sliding to their slowest pace since February 2016 at 5.21 million,” he said.

“Too many would-be buyers are either being priced out, or are deciding to postpone their search until more homes in their price range come onto the market.”

“In addition to the steady climb in home prices over the past year, it’s evident that the quick run-up in mortgage rates earlier this spring has had somewhat of a cooling effect on home sales,” said Yun.

“This weakening in affordability has put the most pressure on would-be first-time buyers in recent months, who continue to represent only around a third of sales despite a very healthy economy and labor market.”

Total housing inventory at the end of July decreased 0.5 percent to 1.92 million existing homes available for sale (unchanged from a year ago). Unsold inventory is at a 4.3-month supply at the current sales pace (also unchanged from a year ago).

And finally a glance at the following chart shows that the US housing market is in freefall – not what record high stocks would suggest…

Perhaps this helps explain it – Sentiment for Home-Buying Conditions are the worst since the infamous Lehman Brothers collapse …

After Housing Starts collapsed 12.9% in June, July rebounded just 0.9% (dramatically missing expectations of a 7.4% bounce) as Permits rose 1.5% month over month.

A second month in a row with a massive miss to economists’ expectations…

Single-family starts remain very soft and multi-family starts barely rebound at all from June’s crash…

And housing starts are now down year over year for The 2nd month in a row…

Permits rebounded very modestly in both single- and multi-family units…

Two of four regions posted a gain in starts, with the South increasing 10.4 percent and the Midwest climbing by 11.6 percent; the Northeast declined 4 percent and the West plunged 19.6 percent, the biggest drop since January 2017

Finally we note that US home builder stocks have been tracking fundamentals dramatically lower all years…

Owning a home is generally viewed as a better deal than renting, but in cities with exploding home prices and relatively flat rents, that may not be the case anymore.

According to Trulia, it now makes more financial sense to rent than buy in the nation’s two most expensive markets — San Jose and San Francisco. The balance is also shifting in favor of renting in a few other high-cost cities, such as Honolulu, Seattle and Portland, Oregon, according to a recent study by the San Francisco-based company.

Trulia said the overall U.S. market still solidly provides buyers with a financial benefit. But in the five years since Trulia began estimating the financial advantages of buying versus renting, this is the first time renters have come out ahead in any of the major metros it tracks.

In San Jose and San Francisco, renting was 12 percent and 6 percent cheaper, respectively, for the consumer than buying a home, Trulia said. San Francisco and San Jose are outliers, though. The National Association of Realtors, for example, has estimated that for a person earning $100,000, just 2.5 percent of the June listings in San Jose and 9 percent in San Francisco were affordable. Trulia reported that buyers still have a significant advantage over renters in places like Detroit.

Trulia estimated that on a nationwide basis, buying a home was 26 percent cheaper for a consumer than renting as of last month. This is the narrowest gap in five years, and has come down from 41 percent in 2016, according to Trulia. The key factor in closing the gap is that house prices have increased steeply along with mortgage rates, while rents are remaining relatively stable. In San Jose, for example, home prices have jumped up 29 percent in a year, while rents were unchanged. Home values rose 14 percent in San Francisco, and rents fell by 3 percent.

“There are a lot of factors,” Trulia’s Senior Economist Cheryl Young said during an interview on Thursday. “Obviously, mortgage rates are going up. That is going to tip the scales a little bit toward renting, but also home value appreciation is far outpacing rent growth right now. So, rents are pretty much cooling out. As they cool down and home prices track up, that margin between buying and renting starts closing.”

Young said the balance could tip in favor of renters in other cities as well.

“There are markets that are always close to that margin, and things that could tip it,” she said. “If mortgage rates were to rise and we still see rents flattening and even decreasing as they have been in some places relative to rising home prices, we may see some markets tip.”

Trulia’s calculations include forecasts on future rent and price appreciation, and also estimates on how much a renter can potentially earn by investing in other vehicles. Trulia assumes that the buyer will stay in the home for seven years, put 20 percent down on a 30-year fixed mortgage.

Other housing analysts told Scotsman Guide News that gauging the advantages of buying versus renting can be a tricky exercise.

“The housing market doesn’t necessarily favor either one right now, as the choice of whether to be an owner or the renter is not a purely economic decision, but often includes the lifestyle decisions of an individual,” said Mark Fleming, chief economist for First American Corp.

Fleming also noted that in some of these high-cost cities, renters are in better position now to buy than when home prices were near their low point seven years ago.

“While housing prices are on the rise across the country, by historical standards they are still within reach in many markets,” Fleming said. “In fact, when you account for the historically low interest rate environment and rising incomes, consumer house-buying power is up nearly 24 percent since 2011,” he added.

Len Kiefer, deputy chief economist for Freddie Mac, said that rising home values tend to give the buyer a financial edge over the renter, who is gaining no equity.

“Certainly if we look back historically, homeowners have done pretty well relative to renters,” Kiefer said. “It doesn’t mean that it is going to be true in the future, but if you look at where our forecast is for the overall economy, we are still forecasting home prices to continue to rise at a pretty healthy pace over the next couple of years.”

Kiefer said in a few high-cost cities with high property taxes, homeowners will be hurt by new tax changes that eliminated or reduced homeownership perks in the federal tax code. This may give renters some advantage. He said the tax changes so far don’t seem to have reduced homebuyer demand significantly, though.

“Certainly in the high-cost, high-tax markets, places like parts of California, New Jersey, Illinois, the cost of homeownership is going to be a little bit negative,” Kiefer said. “But if we look at actual data on what has happened in those markets, it is hard to see a discernible impact in terms of slower overall activity that you could attribute to the tax law,” he said. Kiefer said rising prices and higher rates were likely making homebuying less appealing, however.

Renters have been less sold on the financial benefits of owning a home, according to recent Fannie Mae surveys. In January 2010, for example, 76 percent of surveyed renters saw an advantage in buying. That number has fallen to 68 percent as of the end of June.

“Renters’ view of the financial benefit of owning has come down a little bit,” said Mark Palim, deputy chief economist for Fannie Mae. “That probably reflects that home prices are up substantially.”

Palim said that renters are still expressing a strong desire in buying homes for non-financial, quality-of-life factors. He said the improved economy and a surge in household formation has kept the buyer demand up in spite of rising home prices and rates.

“Millennials have really moved into the market in a big way, and they are closing the gap relative to other generations,” Palim said. “People have far more financial means to afford a home and go out and buy a home, and that has translated into pretty brisk demand.”

(Paul Craig Roberts) The housing market is now apparently turning down. Consumer incomes are limited by jobs offshoring and the ability of employers to hold down wages and salaries. The Federal Reserve seems committed to higher interest rates – in my view to protect the exchange value of the US dollar on which Washington’s power is based. The arrogant fools in Washington, with whom I spent a quarter century, have, with their bellicosity and sanctions, encouraged nations with independent foreign and economic policies to drop the use of the dollar. This takes some time to accomplish, but Russia, China, Iran, and India are apparently committed to dropping or reducing the use of the US dollar.

A drop in the world demand for dollars can be destabilizing of the dollar’s value unless the central banks of Japan, UK, and EU continue to support the dollar’s exchange value, either by purchasing dollars with their currencies or by printing offsetting amounts of their currencies to keep the dollar’s value stable. So far they have been willing to do both. However, Trump’s criticisms of Europe has soured Europe against Trump, with a corresponding weakening of the willingness to cover for the US. Japan’s colonial status vis-a-vis the US since the Second World War is being stressed by the hostility that Washington is introducing into Japan’s part of the world. The orchestrated Washington tensions with North Korea and China do not serve Japan, and those Japanese politicians who are not heavily on the US payroll are aware that Japan is being put on the line for American, not Japanese interests.

If all this leads, as is likely, to the rise of more independence among Washington’s vassals, the vassals are likely to protect themselves from the cost of their independence by removing themselves from the dollar and payments mechanisms associated with the dollar as world currency. This means a drop in the value of the dollar that the Federal Reserve would have to prevent by raising interest rates on dollar investments in order to keep the demand for dollars up sufficiently to protect its value.

As every realtor knows, housing prices boom when interest rates are low, because the lower the rate the higher the price of the house that the person with the mortgage can afford. But when interest rates rise, the lower the price of the house that a buyer can afford.

If we are going into an era of higher interest rates, home prices and sales are going to decline.

The “on the other hand” to this analysis is that if the Federal Reserve loses control of the situation and the debts associated with the current value of the US dollar become a problem that can collapse the system, the Federal Reserve is likely to pump out enough new money to preserve the debt by driving interest rates back to zero or negative.

Would this save or revive the housing market?Not if the debt-burdened American people have no substantial increases in their real income. Where are these increases likely to come from? Robotics are about to take away the jobs not already lost to jobs offshoring. Indeed, despite President Trump’s emphasis on “bringing the jobs back,” Ford Motor Corp. has just announced that it is moving the production of the Ford Focus from Michigan to China.

Apparently it never occurs to the executives running America’s off shored corporations that potential customers in America working in part time jobs stocking shelves in Walmart, Home Depot, Lowe’s, etc., will not have enough money to purchase a Ford. Unlike Henry Ford, who had the intelligence to pay workers good wages so they could buy Fords, the executives of American companies today sacrifice their domestic market and the American economy to their short-term “performance bonuses” based on low foreign labor costs.

What is about to happen in America today is that the middle class, or rather those who were part of it as children and expected to join it, are going to be driven into manufactured “double-wide homes” or single trailers. The MacMansions will be cut up into tenements. Even the high-priced rentals along the Florida coast will find a drop in demand as real incomes continue to fall. The $5,000-$20,000 weekly summer rental rate along Florida’s panhandle 30A will not be sustainable. The speculators who are in over their heads in this arena are due for a future shock.

For years I have reported on the monthly payroll jobs statistics. The vast majority of new jobs are in lowly paid nontradable domestic services, such as waitresses and bartenders, retail clerks, and ambulatory health care services. In the payroll jobs report for June, for example, the new jobs, if they actually exist, are concentrated in these sectors: administrative and waste services, health care and social assistance, accommodation and food services, and local government.

High productivity, high value-added manufactured jobs shrink in the US as they are offshored to Asia.High productivity, high value-added professional service jobs, such as research, design, software engineering, accounting, legal research, are being filled by offshoring or by foreigners brought into the US on work visas with the fabricated and false excuse that there are no Americans qualified for the jobs.

America is a country hollowed out by the short-term greed of the ruling class and its shills in the economics profession and in Congress. Capitalism only works for the few. It no longer works for the many.

On national security grounds Trump should respond to Ford’s announcement of offshoring the production of Ford Focus to China by nationalizing Ford. Michigan’s payrolls and tax base will decline and employment in China will rise. We are witnessing a major US corporation enabling China’s rise over the United States. Among the external costs of Ford’s contribution to China’s GDP is Trump’s increased US military budget to counter the rise in China’s power.

Trump should also nationalize Apple, Nike, Levi, and all the rest of the offshored US global corporations who have put the interest of a few people above the interests of the American work force and the US economy. There is no other way to get the jobs back. Of course, if Trump did this, he would be assassinated.

America is ruled by a tiny percentage of people who constitute a treasonous class. These people have the money to purchase the government, the media, and the economics profession that shills for them. This greedy traitorous interest group must be dealt with or the United States of America and the entirety of its peoples are lost.

In her latest blockbuster book, Collusion, Nomi Prinsdocuments how central banks and international monetary institutions have used the 2008 financial crisis to manipulate markets and the fiscal policies of governments to benefit the super-rich.

These manipulations are used to enable the looting of countries such as Greece and Portugal by the large German and Dutch banks and the enrichment via inflated financial asset prices of shareholders at the expense of the general population.

One would think that repeated financial crises would undermine the power of financial interests, but the facts are otherwise. As long ago as November 21, 1933, President Franklin D. Roosevelt wrote to Col. House that “the real truth of the matter is, as you and I know, that a financial element in the larger centers has owned the Government ever since the days of Andrew Jackson.”

Thomas Jefferson said that “banking institutions are more dangerous to our liberties than standing armies” and that “if the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks . . . will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered.”

The shrinkage of the US middle class is evidence that Jefferson’s prediction is coming true.

Tumbling house prices in Sydney and Melbourne are the main drivers behind the first annual drop in national property prices in six years, a new report shows. The national median house price fell 1.0 per cent over the June quarter and year, according to a report by property classifieds group Domain released on Thursday.

It is the first time values have fallen on an annual basis since June 2012.

The negative national growth rate reflects weakening house prices in Sydney and Melbourne, which together represent about two thirds of Australia’s housing market by value.

Sydney house prices fell by 4.5 per cent in the 12 months to the end of June for their largest annual drop since 2008. Sydney units also fell by 3.5 per cent over the same period.

The figures chime with those released this week by property data firm CoreLogic, which said overall Sydney prices fell 5.0 per cent in the 12 months to July 22.

“House and unit prices in Sydney are now back to values seen at the end of 2016,” Domain property analyst Nicola Powell told AAP. Tighter credit availability and a high number of units being built are key factors behind the dive, Dr Powell said.

Australia’s building commencements, fueled by investor apartment construction, look like heading from boom to bust, according to forecaster BIS Oxford Economics.

In a reality check for investors who bought at the top of the apartment boom, BIS is predicting the biggest correction since the global financial crisis hit in 2008, with housing starts set to fall by almost 23 per cent by 2020.

Associate director Adrian Hart told the ABC’s AM program that the slump would be led by high-density dwelling construction, which is set to halve over the next two years

A key factor in the residential slowdown has been tougher regulation by the Australian Prudential Regulation Authority (APRA) to curb investor lending, while the Foreign Investment Review Board (FIRB) and tax office has been clamping down on overseas buyers.

Australian homeowners are trapped in “mortgage prison” because of a rule change. And there is no easy way out.

Changes in bank rules around living expenses calculations have effectively wiped huge amounts off the maximum a bank will allow you to borrow.

Many people are now finding they originally borrowed more than a bank would lend them under current conditions, meaning they haven’t got the option of shopping around to get a better interest rate — no bank will lend them the amount they need.

Precise numbers of Australia’s mortgage prisoners are hard to come by, but Mozo investment and lending expert Steve Jovcevski told news.com.au that he expected most of them are those who have borrowed and bought in the last five years.

Oops!

Jovcevski gave an example in which a couple was able to borrow $800,000 a year ago can now only borrow $680,000 under the same rules.

They are now trapped in a mortgage with no way to refinance and no buyers because of declining prices.

Mortgage Slaves for Life

This is precisely what some us foresaw years ago. It’s finally come home to roost, and at a time China is highly unlikely to bail out these buyers.

Following last month’s disappointing starts/permits data and home sales prints, hope was high for a June rebound but they are gravely disappointed. Existing home sales tumbled 0.6% MoM (vs expectations of a 0.2% rise) and even worse, it’s off a downwardly revised May print of 0.7% MoM, with median home price hitting a record high $276k.

This is the first 3-in-a-row decline for existing home sales since Jan 2014…

Existing Home Sales SAAR is almost at its weakest since Jan 2016…

Lawrence Yun, NAR chief economist, says closings inched backwards in June and fell on an annual basis for the fourth straight month.

“There continues to be a mismatch since the spring between the growing level of homebuyer demand in most of the country in relation to the actual pace of home sales, which are declining,” he said.

“The root cause is without a doubt the severe housing shortage that is not releasing its grip on the nation’s housing market. What is for sale in most areas is going under contract very fast and in many cases, has multiple offers. This dynamic is keeping home price growth elevated, pricing out would-be buyers and ultimately slowing sales.”

The median existing-home price for all housing types in June was $276,900, surpassing last month as the new all-time high and up 5.2% from June 2017 ($263,300). June’s price increase marks the 76th straight month of year-over-year gains.

Homebuilder stocks have generally drifted lower with the dismal data but have yet to take the next leg lower…

Counter to the national trend, several housing markets saw foreclosure starts rise year over year last month, according to a new report from ATTOM Data Solutions, a real estate data firm.

Forty-three percent of local markets saw an annual increase in May in foreclosure starts. Foreclosure starts were most on the rise in Houston, which saw a 153 percent jump from a year ago. Hurricane Harvey struck the Houston metro area in August 2017, tying with Hurricane Katrina as the costliest tropical cyclone on record, and has contributed to many recent foreclosures in the area. Other areas that are seeing foreclosure starts rise: Dallas-Fort Worth (up 46% year over year); Los Angeles (up 14 percent); Atlanta (up 7 percent); and Miami (up 4 percent).

A total of 33,623 U.S. properties started the foreclosure process in May, which is down 6 percent from a year ago. But a number of states—23 states and the District of Columbia—posted a year-over-year increase in foreclosure starts in May.

Overall, the metro areas with the highest foreclosure rates in May were: Flint, Mich.; Atlantic City, N.J.; Trenton, N.J.; Philadelphia; and Columbia, S.C.

View the chart below to see foreclosure starts by metro area.

California’s median home price reached a new high in May at $600,860, surpassing its previous peak of $594,530 11 years ago.

Home sales declined by 1.8 percent from April and down 4.6 percent compared to May 2017 levels.

May marked the first year-over-year sales decline in four months and the lowest sales level in more than a year.

In Santa Barbara, median home price reached a new historic high in May at $1.2 million, while inventory continues to remain low.

“The softening in May home sales was due in part to the spike in interest rates in mid-April, when the 30-year fixed mortgage rate jumped 20 basis points in just one week to reach the highest level since 2014,” said Steve White, California Association of Realtors president.

“Homebuyers may have postponed escrow closings to wait out the effects of the rate surge,” White said.

“Additionally, the specter of rate increases earlier in the year may have pulled sales forward into the first quarter, which resulted in the subpar performance in the last couple of months,” he said.

“Looking ahead, higher mortgage rates and elevated home prices will heighten affordability constraints that will likely temper the housing market in the coming months,” he said.

While America, and more recently Canada, have both had their ups and downs with housing bubbles, nothing in the world compares to what is going on in Hong Kong, that mecca of overpriced real estate: overnight the Rating and Valuation Department announced that Hong Kong’s private home prices rose 1.7% in May, 15% higher from a year ago. This was the 19th consecutive record price, and a non-stop advance since April 2016.

“Hong Kong’s home prices have smashed records every month this year and we do not see the increase ending any time soon,” said Derek Chan, head of research at Ricacorp Properties. “One record high after another is making people panic.”

The unprecedented surge in prices, means that Hong Kong has persistently been among thecities identified by UBSas being in a real estate bubble.

It is also the world’s most unaffordable city: the same UBS report found that a skilled service worker would need to work 20 years to buy a 650-square-foot (60 square meter) apartment near the city center.

This is because real incomes have virtually stagnated in Hong Kong for many years, with UBS noting that “housing is less affordable here than in any other city we considered, and the average living space per person amounts to only 14m2 (150 sqft).”

So if it is not rising median wealth, what is behind this torrid demand for HK real estate? According to UBS “the latest boom stemmed from strong investor demand, general positive sentiment and the “fear of missing out” on capital gains. This is reflected as well in a frozen secondary market in which people hold on to their properties, expecting prices to rise further.”

In its latest attempt to moderate the housing bubble, on Thursday Hong Kong’s Executive Council approved several proposals, one of which includes introducing a vacancy tax on newly built flats that remain unsold, to cool down the overheating property market. Additionally, it is expected that Hong Kong’s flat-hoarding developers will face an annual vacancy tax amounting to double a property’s annual rental income.

However, according to analysts and agents the policy is not a long-term fix to the city’s housing crisis and urged the government to boost land supply.

“The extra supply of 9,000 [vacant] flats is even less than one third of the annual housing supply expected to offer by developers,” said Vincent Cheung, deputy managing director for Asia valuation and advisory services at Colliers International. “It would only work together with other mid- to long-term policies, such as reducing land premium and increasing the ratio of public land supply to private land supply.”

Until a solution is found, amid this “frozen” bubble of a housing market where normal buyers and Chinese oligarch sellers can rarely if ever that scenes such as the following are a common occurrence: watch as Hong Kong real estate agents literally throw punches, kick each other to the ground and otherwise pull their best kung fu moves as they brawl with one another to get a client’s business.

Chinese capital controls and a slump in foreign buyers? Check.

Trade war with the US? Check.

Things are not looking good for Canada’s national housing market, which as VCG reports, continued its sluggish performance in the month of May. Despite the warmer weather and usually busy spring selling season, buying activity has been awfully quiet. New mortgage regulations which are now in full swing have stymied fringe buyers, particularly millennials. According tonew data from credit bureau TransUnion, new mortgage originations among millennials in Canada fell by 19.5% between the last quarter of 2017 and the first three months of 2018.

That has also been showing up sales data.

As shown in the chart below, national home sales in Canada plunged by 16% Y/Y for the month of May. This was the worst decline since the great financial crisis in 2008 when home sales dipped 17% that May. Furthermore, total home sales of 50,604 marked the lowest total since May 2011.

Seasonally adjusted home sales edged 0.1% lower on a month over month basis, and 15% on a year over year basis. Or, as Steve Saretsky put it, “either way you slice it not a great month for one of the worlds most resilient housing markets.”

And as sales continue to slide inventory is beginning to build. For sale inventory crept up by 4% year over year, increasing for the first time in three years, and the highest May increase since 2010.

In light of the above, it is not surprising that the average sales price dipped 6% year over year in May, which however was not nearly as bad as April when year over year declines registered a head turning 11% decline.

But more troubling is that when looking at the smoothed out index of the MLS HPI prices showed the smallest possible increase of just 1% year over year in May, the lowest since September 2009. Not only did this mark the 13th consecutive month of decelerating year over year gains per theCanadian Real Estate Association, but at the current rate of slowdown, next month Canada will record the first annual drop in home prices since the global financial crisis.

The silver lining: condos continue to hold up well as buyers tumble down the housing ladder; here prices posted a 13% increase from May 2017.

CREA’s chief economist Gregory Klump shouldered much of the blame on tighter borrowing conditions, “This year’s new stress-test became even more restrictive in May, since the interest rate used to qualify mortgage applications rose early in the month. Movements in the stress test interest rate are beyond the control of policy makers. Further increases in the rate could weigh on home sales activity at a time when Canadian economic growth is facing headwinds from U.S. trade policy frictions.”

Klump’s theory stacks up well with recent data which suggests fringe borrowers are being pushed towards the private lending space, particularly in Ontario. Mortgage originations at private lenders in the Q1 2018rose to $2.09 billion in Ontario, a 2.95% increase from last year. The market share of private lending went from 5.71% of originations in Q1 2017, to 7.87% in Q1 2018, despite originations at other channels dropping.

In other words, there is a surge in unregulated, non-bank lending, just as the housing bubble pops, precisely what happened the last time there was a full-blown financial crisis.

Several Silicon Valley employees, including a software engineer for Twitter who made a $160,000 salary,were mocked online after complaining about their living standards inan articlefor The Guardian.

In the article, entitled “Scraping by on six figures? Tech workers feel poor in Silicon Valley’s wealth bubble,” the employee complained that his six-figure salary was “pretty bad” for the area.

“I didn’t become a software engineer just to make ends meet,”proclaimed the employee. “Families are priced out of the market.”

“The biggest cost is his $3,000 rent – which he said is ‘ultra cheap’ for the area – for a two-bedroom house in San Francisco, where he lives with his wife and two children,”reported The Guardiansympathetically. “He’d like a slightly bigger place, but finds himself competing with groups of twenty somethings happy to share accommodation while paying up to $2,000 for a single room.”

“Prohibitive costs have displaced teachers, city workers, firefighters and other members of the middle class, not to mention low-income residents,” they continued. “Now techies, many of whom are among the highest 1% of earners, are complaining they, too, are being priced out.”

The Guardian also covered other Silicon Valley employees in the piece who were earning “between $100,000 and $700,000 a year” but still allegedly had trouble “making ends meet.”

“One Apple employee was recently living in a Santa Cruz garage, using a compost bucket as a toilet. Another tech worker, enrolled in a coding boot camp, described how he lived with 12 other engineers in a two-bedroom apartment rented via Airbnb,” The Guardian reported.

“It was $1,100 for a fucking bunk bed and five people in the same room. One guy was living in a closet, paying $1,400 for a ‘private room,’” one man complained, while a female employee added, “We make over $1m between us, but we can’t afford a house… This is part of where the American dream is not working out here.”

Other established San Francisco residents mocked tech employees for their complaints.

House flipping activitysurged to an 11-year highthis year, with more than 207,000 homes flipped, according to ATTOM Data Solutions, a real estate data firm. But the key is knowing where to be and when. “The sweet spot for successful home flipping is finding the neighborhoods just emerging as the next hot neighborhoods in a city,” says Daren Blomquist, a senior vice president at ATTOM Data Solutions. The firm says the average profit for a housing flip in 2017 was $68,100.

Realtor.com® ranked the 200 largest metros according to the share of all home sales categorized as a flip (defined as any type of home that is bought and resold within a three- to 12-month period). Researchers limited their rankings to two metros per state for geographic diversity and only included markets where the average profit was at least $30,000.

The following are the best housing markets for home flippers, according to realtor.com®:

The early stages of a housing cycle are fun for pretty much everyone. Homeowners see their equity start to rise and feel smart for having bought, home seekers have to pay up, but not too much, and fully expect their new home to keep appreciating. People with modest incomes feel a bit of pinch but can still afford to stick around.

But later on the bad starts to outweigh the good. Existing homeowners still enjoy the ride but would-be buyers find themselves priced out of their top-choice neighborhoods. And residents who aren’t tech millionaires find that they can no longer afford to live where they work. Consider the plight of a teacher or cop pretty much anywhere in California these days:

Drew Barclay has a master’s degree in education and three years of experience as an English teacher, but, like most new teachers in Davis, he can’t afford to live there.

Instead, Barclay, 31, shares a rental in Sacramento that costs him $950 a month — about 40 percent of the $2,550 he brings home each month after taxes.

He is so certain that he won’t be able to qualify for a loan for a home in Davis on his $47,000 annual salary that he hasn’t bothered to house hunt. The median price for a house in the city in March was $682,500, according to tracking firm CoreLogic. Renting also is prohibitive, with the average rent in Davis about $2,500 a month, according to Zillow, a real estate website.

Davis Joint Unified officials hope to get a little help from state legislators. Last week, the state Senate voted 24-8 to waive the annual school district parcel tax of $620 for teachers and other employees of the Yolo County school district.

Davis school board member Alan Fernandes said that about two-thirds of the district’s teachers live outside Davis where housing is less expensive. He said the bill would encourage more of the district’s teachers to live in the community they serve.

Davis Joint Unified regularly passes parcel taxes to keep class sizes down and to support classroom programs. In 2016, 71 percent of Davis voters approved Measure H, a yearly tax of $620 on each parcel of taxable real property in the district for eight years. The measure raises $9.5 million a year to support math, reading and science programs and reduced class sizes for elementary grades.

But the roughly $50 a month exemption isn’t likely to help Davis Joint Unified teachers enough to make buying a house affordable. The teachers are some of the lowest-paid educators in the region, with some of the highest health care costs.

Barclay said he knows teachers 10 or 15 years older than he is who are renting rooms in other educators’ homes to get by. He said some teachers have weekend jobs to make enough money to pay their bills.

“Because I’m fairly certain I can’t put down permanent roots here, I don’t see this position as a permanent one,” Barclay said of his job as an English teacher at Davis Senior High School.

California school districts have responded by offering signing bonuses, housing stipends, computers and free tuition to educators who sign up with their districts.

When housing costs reach this point there’s no real fix. Raise taxes to increase teacher pay and there’s political trouble. Cut back on other services and the quality of life declines. “Streamline” the schools and educational outcomes and teacher morale plummet.

There’s a limit, in other words, to the ascent of home prices beyond which the system starts to break down. And when the people who make a town run smoothly – teachers, firefighters, cops, sanitation workers – can no longer afford to live there, that town has clearly crossed the line.

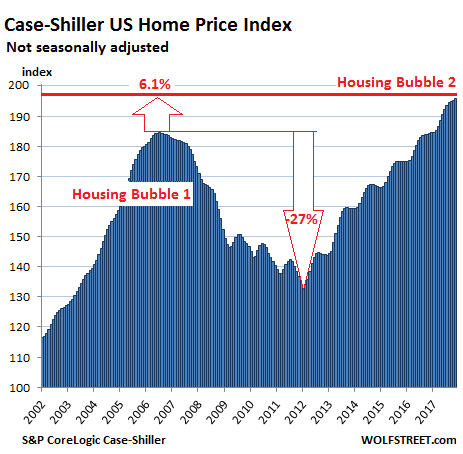

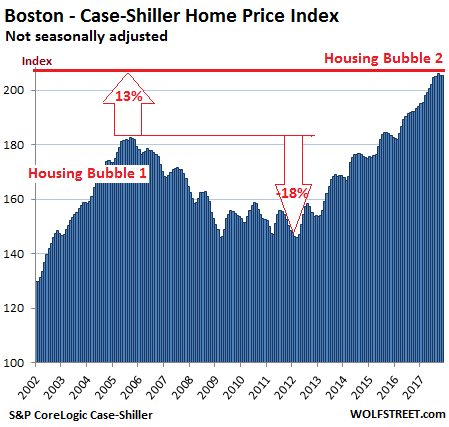

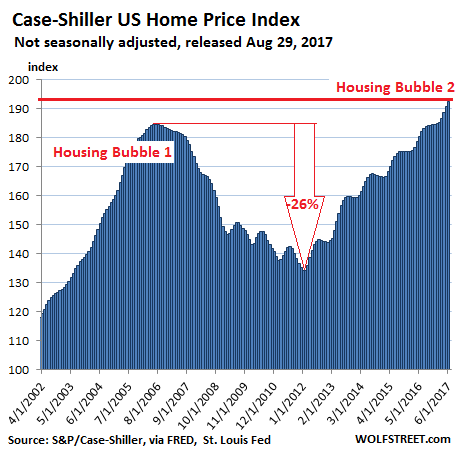

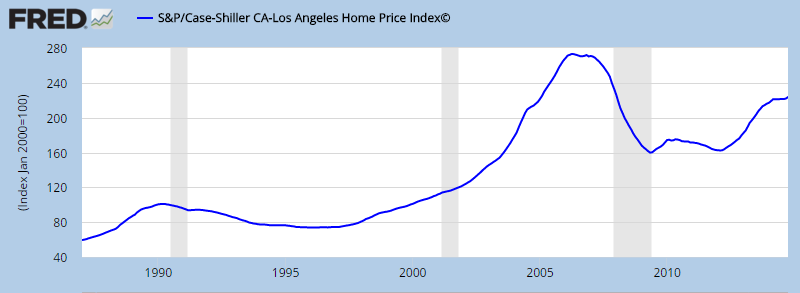

Based on the Case-Shiller home price index, which is now back to its 2007 housing bubble peak, there are a lot more Davis, CAs out there, with all the pathologies that that implies.

A housing bubble, of course, is just a symptom of a bigger problem. Easy money distorts the workings of a market economy by causing the prices of many assets to soar beyond all reason, enriching the owners and impoverishing the users. Typically, when housing reaches this point so have stocks and other financial assets,CEO salaries, corporate concentration, political corruption and a long list of other evils that feed on low interest rates and lax lending standards. The confluence of resulting problems then brings the cycle to a noisy end.

There are a large number of public and private services that measure the change in home prices. The algorithms behind these services, while complex, are primarily based on recent sale prices for comparative homes and adjusted for factors like location, property characteristics and the particulars of the house. While these pricing services are considered to be well represented measures of house prices, there is another important factor that is frequently overlooked despite the large role in plays in house prices.

In August 2016, the 30-year fixed mortgage rate as reported by the Federal Reserve hit an all-time low of 3.44%. Since then it has risen to its current level of 4.50%. While a 1% increase may appear small, especially at this low level of rates, the rise has begun to adversely affect housing and mortgage activity. After rising 33% and 22% in 2015 and 2016 respectively, total mortgage originations were down -16% in 2017. Further increases in rates will likely begin to weigh on house prices and the broader economy. This article will help quantify the benefit that lower rates played in making houses more affordable over the past few decades. By doing this, we can appreciate how further increases in mortgage rates might adversely affect house prices.

Lower Rates

In 1981 mortgage rates peaked at 18.50%. Since that time they have declined steadily and now stands at a relatively paltry 4.50%. Over this 37-year period, individuals’ payments on mortgage loans also declined allowing buyers to get more for their money. Continually declining rates also allowed them to further reduce their payments through refinancing. Consider that in 1990 a $500,000 house, bought with a 10%, 30-year fixed rate mortgage, which was the going rate, would have required a monthly principal and interest payment of $4,388. Today a loan for the same amount at the 4.50% current rate is almost half the payment at $2,533.

The sensitivity of mortgage payments to changes in mortgage rates is about 9%, meaning that each 1% increase or decrease in the mortgage rate results in a payment increase or decrease of 9%. From a home buyer’s perspective, this means that each 1% change in rates makes the house more or less affordable by about 9%.

Given this understanding of the math and the prior history of rate declines, we can calculate how lower rates helped make housing more affordable. To do this, we start in the year 1990 with a $500,000 home price and adjust it annually based on changes in the popular Case-Shiller House Price Index. This calculation approximates the 28-year price appreciation of the house. Second, we further adjust it to the change in interest rates. To accomplish this, we calculated how much more or less home one could buy based on the change in interest rates. The difference between the two, as shown below, provides a value on how much lower interest rates benefited home buyers and sellers.

Data Courtesy: S&P Core Logic Case-Shiller House Price Index

The graph shows that lower payments resulting from the decline in mortgage rates benefited buyers by approximately $325,000. Said differently, a homeowner can afford $325,000 more than would have otherwise been possible due to declining rates.

The Effect of Rising Rates

As stated, mortgage rates have been steadily declining for the past 37 years. There are some interest rate forecasters that believe the recent uptick in rates may be the first wave of a longer-term change in trend. If this is, in fact, the case, quantifying how higher mortgage rates affect payments, supply, demand, and therefore the prices of houses is an important consideration for the direction of the broad economy.

The graph below shows the mortgage payment required for a $500,000 house based on a range of mortgage rates. The background shows the decline in mortgage rates (10.00% to 4.50%) from 1990 to today.

To put this into a different perspective, the following graph shows how much a buyer can afford to pay for a house assuming a fixed payment ($2,333) and varying mortgage rates. The payment is based on the current mortgage rate.

As the graphs portray, home buyers will be forced to make higher mortgage payments or seek lower-priced houses if rates keep rising.

Summary

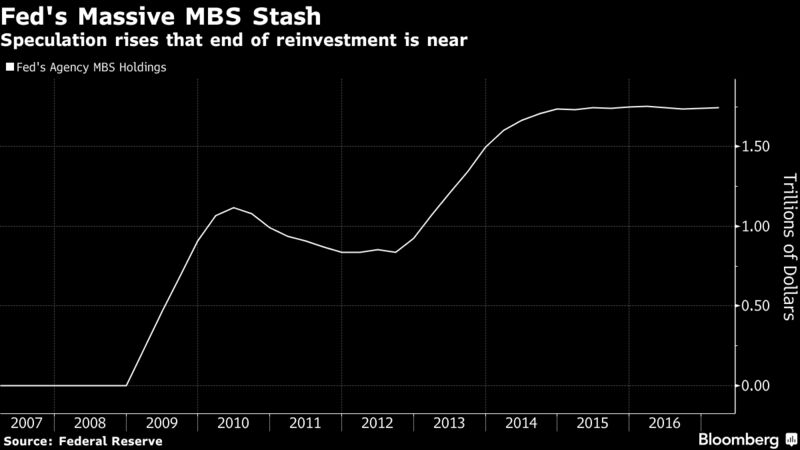

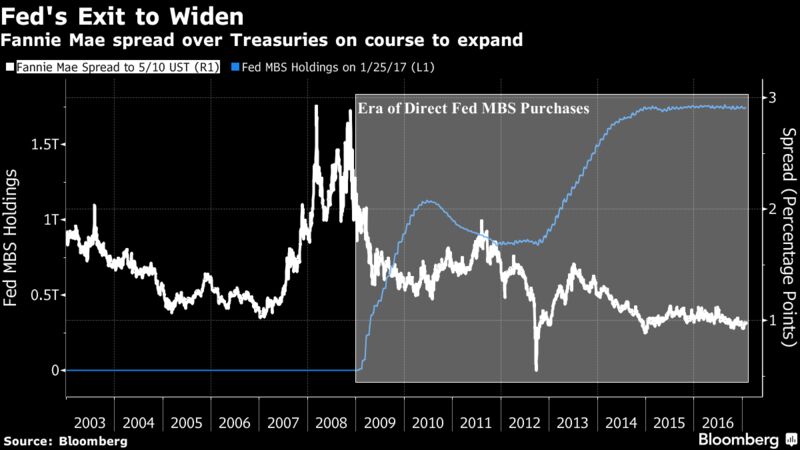

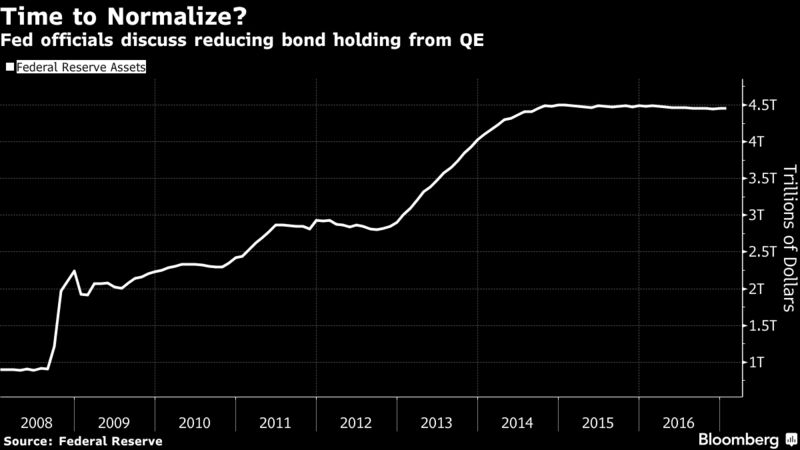

The Fed has raised interest rates six times since the end of 2015. Their forward guidance from recent Federal Open Market Committee (FOMC) meeting statements and minutes tells of their plans on continuing to do so throughout this year and next. Additionally, the Fed owns over one-quarter of all residential mortgage-backed securities (MBS) through QE purchases. Their stated plan is to reduce their ownership of those securities over the next several quarters. If the Fed continues on their expected path with regard to rates and balance sheet, it creates a significant market adjustment in terms of supply and demand dynamics and further implies that mortgage rates should rise.

The consequences of higher mortgage rates will not only affect buyers and sellers of housing but also make borrowing on the equity in homes more expensive. From a macro perspective, consider that housing contributes 15-18% to GDP, according to the National Association of Home Builders (NAHB). While we do not expect higher rates to devastate the housing market, we do think a period of price declines and economic weakness could accompany higher rates.

This analysis is clinical using simple math to illustrate the relationship, cause, and effects, between changes in interest rates and home prices. However, the housing market is anything but a simple asset class. It is among the most complex of systems within the broad economy. Rising rates not only impact affordability but also the general level of activity which feeds back into the economy. In addition to the effect that rates may have, also consider that the demographics for housing are challenged as retiring, empty-nest baby boomers seek to downsize. To whom will they sell and at what price?

If interest rates do indeed continue to rise, there is a lot more risk embedded in the housing market than currently seems apparent as these and other dynamics converge. The services providing pricing insight into the value of the housing market may do a fine job of assessing current value, but they lack the sophistication required to see around the next economic corner.

Home values have been rising for six straight years, and the gains have been accelerating for the past two years.

The average rate on the 30-year fixed mortgage is nearly a full percentage point higher today than it was in September 2017, its latest low.

Homebuyer demand may be weakening. A monthly survey from Redfin found fewer potential buyers requesting home tours or making offers.

Home values have been rising for six straight years, and the gains have been accelerating for the past two years. Unlike the last housing boom, the gains are not driven by fast and easy mortgage money, but instead by solid buyer demand and very low supply. Still, like the last housing boom, some are starting to warn these price gains cannot continue.

“The continuing run-up in home prices above the pace of income growth is simply not sustainable,” wrote Lawrence Yun, chief economist for the National Association of Realtors, in response to the latest price reading from the much-watched S&P CoreLogic Case Shiller Home Price Indices. “From the cyclical low point in home prices six years ago, a typical home price has increased by 48 percent while the average wage rate has grown by only 14 percent.”

Yun also pointed to rising mortgage interest rates as a factor that would weaken affordability. The average rate on the 30-year fixed mortgage is nearly a full percentage point higher today than it was at its most recent low in September 2017.

Some argue that despite weakened affordability, demand is just so strong that it can support higher home prices. Improving economic factors are seeing to that.

“A generally strong economy and favorable demographic tailwinds driven by the huge millennial generation aging into their home buying prime will help ensure that demand stays high, even as prices rise,” wrote Aaron Terrazas, senior economist at Zillow. “Getting a mortgage remains incredibly affordable compared to paying rent each month.”

But he admits that the “advantage is starting to erode, as mortgage interest rates rise alongside prices and income growth lags behind.”

Weakening Demand

And demand may in fact be weakening. A monthly survey from Redfin found fewer potential buyers requesting home tours or making offers.

“April was the first time in 27 months that we saw a year-over-year decline in the number of customers touring homes,” said Redfin’s chief economist, Nela Richardson. “We believe this was driven by the low levels of new listings in March.”

Richardson points to an increase in new listings in April is a positive turn for home buyers, which could bode well for futures sales. Prices, however, still stand in the way, and the increased inventory was more pronounced in higher-priced tiers.

Meanwhile the home price gains are widest on the low end of the market, where supply is leanest. That is why home sales have been dropping most on the low end. Evidence is now mounting that a growing number of first-time buyers are giving up and dropping out of the market altogether. Sales to first-time buyers dropped 2 percent in the first quarter of this year compared with the first quarter of 2017, according to Genworth Mortgage Insurance.

“This quarter’s decline in first-time home buyer sales reflects a slowdown in cyclical momentum as the first-time home buyer market approached its historical norms. It also reflects a shortage of available homes priced at or below the median first-time home buyer market price of $250,000,” wrote Tian Liu, Genworth’s chief economist. “Supply pressures will continue to drive price appreciation and freeze out a large percentage of the 2.7 million first-time home buyers who are still missing from the market.”

Competition from all-cash investors continues to thwart first-time buyers, most of whom are reliant on mortgage financing. With so little supply available, bidding wars are the rule, rather than the exception.

“When you’re competing against 10 other offers, you have to stand out, so sometimes a letter to the sellers can pull on the emotional heartstrings, but really it’s all about the dollars,” said Karen Kelly, a real estate agent with Compass in the Washington, D.C., area.

Measuring Affordability

Half of the homes on the market in D.C. in April sold in eight days or less, according to the Greater Capital Area Association of Realtors. Home prices in D.C. were over 13 percent higher in April of this year compared with a year ago. The number of listings was down more than 3 percent.

Affordability continues to be a tricky metric to monitor. Some economists argue that housing is no less affordable than it was in the early part of this century, when adjusting for inflation. No question, though, even if home prices are still lower than they were during the last housing boom, adjusting for inflation, the mortgage market today is nothing like it was then.

In fact, affordability was largely meaningless back then, since buyers could put no money down for a home and pay incredibly low monthly payments, using mortgage products that adjusted higher over time and tacked huge costs onto later payments. Those so-called negative amortization loans caused the housing crash and are not offered today.

Thanks to a modest downward revision in February’s print, March’s Case-Shiller 20-City Composite Home Price Index rose at 6.79% YoY – the fastest price appreciation since June 2014.

Surpassing July 2006’s record high…

Broadening out from the 20-City composite, the national home-price gauge climbed 6.5% YoY, matching February’s YoY advance that was the biggest since May 2014.

Of course, since March, interest rates have spiked and along with them mortgage rates, plunging mortgage apps, and as property-price appreciation continues to outpace worker pay (by 3.8 times!), it is proving a disadvantage for younger or first-time buyers even as it means rising homeowner equity for others.

“Months-supply, which combines inventory levels and sales, is currently at 3.8 months, lower than the levels of the 1990s, before the housing boom and bust,” – David Blitzer, chairman of the S&P index committee, said in a statement –

“Until inventories increase faster than sales, or the economy slows significantly, home prices are likely to continue rising.”

All 20 cities in the index showed year-over-year gains, led by a 13 percent increase in Seattle, a 12.4 percent advance in Las Vegas and 11.3 percent pickup in San Francisco.

Purchases fell in three of four regions, including a 2.9 percent decline in the South and a 3.3 percent drop in the West

Notably, while single-family home sales decreased 3 percent last month to an annual rate of 4.84 million, purchases of condominium and co-op units rose 1.6 percent to a 620,000 pace.

On a YoY basis, it looks like we have hit peak housing…

“Since NAR began tracking this data in May 2011, the median days a listing was on the market was at an all-time low in April, and the share of homes sold in less than a month was at an all-time high.”

The median existing-home price for all housing types in April was $257,900, up 5.3 percent from April 2017 ($245,000). March’s price increase marks the 74th straight month of year-over-year gains, but price growth is slowing…

And just like new home sales, all the positives are at the higher-end…

“We are seeing no breakout in home sales,” Lawrence Yun, NAR’s chief economist, said at a press briefing accompanying the report. “We are stuck in this narrow range at a time when the economy is doing well.”

“However, inventory shortages are even worse than in recent years, and home prices keep climbing above what many home shoppers can afford,” Yun said in a statement.

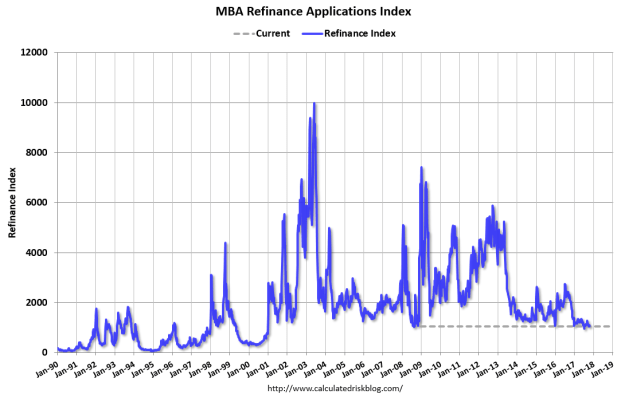

Yesterday when looking at the latest MBA Mortgage Application data, we found that, as mortgage rates jumped to the highest level since 2011, mortgage refi applications, not unexpectedly tumbled to the lowest level since the financial crisis, choking off a key revenue item for banks, and resulting ineven more painfor the likes of Wells Fargo.

Today, according to the latest Freddie Mac mortgage rates report, after plateauing in recent weeks, mortgage rates reversed course and reached a new high last seen eight years ago as the 30-year fixed mortgage rate edged up to 4.61% matching the highest level since May 19, 2011.

But while the highest mortgage rates in 8 years are predictably crushing mortgage refinance activity, they appears to be having the opposite effect on home purchases, where there is a sheer scramble to buy, and sell, houses. AsBloomberg notes, citing brokerage Redfin, the average home across the US that sold last month went into contract after a median of 36 only days on the market – a record speed in data going back to 2010.

To Sam Khater, chief economist of Freddie Mac, this was a sign of an economy firing on all cylinders: “This is what happens when the economy is strong,” Khater told Bloomberg in a phone interview. “All the higher-rate environment does is it either causes them to try and rush or look at different properties that are more affordable.”

Of course, one can simply counter that what rising rates rally do is make housing – for those who need a mortgage – increasingly more unaffordable, as a result of the higher monthly mortgage payments. Case in point: with this week’s jump, the monthly payment on a $300,000, 30-year loan has climbed to $1,540, up over $100 from $1,424 in the beginning of the year, when the average rate was 3.95%.

As such, surging rates merely pulls home demand from the future, as potential home buyers hope to lock in “lower” rates today instead of risking tomorrow’s rates. It also means that after today’s surge in activity, a vacuum in transactions will follow, especially if rates stabilize or happen to drop. Think “cash for clunkers”, only in this case it’s houses.

Meanwhile, the short supply of home listings for sale and increased competition is only making their purchases harder to afford: according to Redfin, this spike in demand and subdued supply means that home prices soared 7.6% in April from a year earlier to a median of $302,200, and sellers got a record 98.8% of what they asked on average.

Call it the sellers market.

Furthermore, bidding wars are increasingly breaking out: Minneapolis realtor Mary Sommerfeld said a family she works with offered $33,000 more than the $430,000 list price for a home in St. Paul. The listing agent gave her the bad news: There were nine offers and the family’s was second from the bottom.

For Sommerfeld’s clients, the lack of inventory is a bigger problem than rising mortgage rates. If anything, they want to close quickly before they get priced out of the market — and have to pay more interest.

“I don’t think it’s hurting the buyer demand at all,” she said. “My buyers say they better get busy and buy before the interest rates go up any further.”

Then again, in the grand scheme of things, 4.61% is still low. Kristin Wilson, a loan officer with Envoy Mortgage in Edina, Minnesota, tells customers to keep things in perspective. When she bought a house in the early 1980s, the interest on her adjustable-rate mortgage was 12 percent, she said.

“One woman actually used the phrase: ‘Rates shot up,’” Wilson said. “We’ve been spoiled after a number of years with rates hovering around 4 percent or lower.”

Of course, if the average mortgage rate in the America is ever 12% again, look for a real life recreation of Mad Max the movie in a neighborhood near you…

Today in “free-market capitalism actually benefits consumers” news, rents are being slashed across the board in Queens as landlords make concessions to deal with a supply glut and keep tenants renting. This lowering of rents taking place in Queens – to the tune of 12% YOY –was reported on by Bloombergon Thursday morning:

For New York City apartment hunters, April was another good month to find a deal on rents. But no one fared better than those in northwest Queens.

Rents there dropped 12 percent from a year earlier, to a median of $2,646 a month after landlord giveaways were subtracted, according to a report Thursday by appraiserMiller Samuel Inc.and brokerageDouglas Elliman Real Estate. Those giveaways were offered on 65 percent of all new leases signed in the area, excluding renewals, a record share in data going back to the beginning of 2016.

The result from the price deflation that our Fed pins as the devil incarnate? More renters, more business and higher quality tenants:

The enticements brought in more renters. New leases in northwest Queens — Long Island City, Astoria, Sunnyside and Woodside — jumped 11 percent to 272, the firms said.

“More customers who were originally looking in Manhattan and Brooklyn are considering Queens,” said Hal Gavzie, Douglas Elliman’s executive manager of leasing. “It used to be just 100 percent a different consumer.”

New York City tenants are crossing borders to compare deals in a market groaning under the weight of new supply. Landlords, who’ve accepted they need to compete to keep their units filled, are working to attract new tenants and offering sweeter renewal terms to keep the ones they have, Gavzie said.

Who knew this could happen to industries and sectors where the government is not subsidizing or interfering with the pricing – and where free market capitalism is actually, in some facet, allowed to run its course?

The consumer now has the control because the concessions landlords are making are benefiting the them. Bloomberg continued:

In Manhattan, 44 percent of all new leases came with a landlord concession, such as a free month of rent or payment of broker fees. In Brooklyn, the share was 51 percent, a record for the borough.

Still, the number of new leases in Manhattan and Brooklyn fell 3.5 percent and 1.6 percent, respectively, a sign that renters there found good reason to stay in their current apartments, Gavzie said.

“Tenants negotiating a renewal, they’ve looked around to see what deals they can get,” he said. “So their landlord gives them a sweet offer to stay.”

Manhattan rents in April, after subtracting concessions, fell 2.2 percent, to a median of $3,236, the fifth consecutive month of year-over-year declines. In Brooklyn, where rents have also fallen for five months, the decline was 2.9 percent, to a median of $2,686.

This comes just about one month after we reported about downtown Manhattan basically turning into a ghost towndue to just the opposite – prices rising and government overreach. Pricing out of tenants in some main downtown areas and shopping districts have caused vacancies in areas that have been occupied for decades.

The Fed loves to repeat how necessary and vital inflation is for economic prosperity, but in the case of midtown Manhattan’s “prime” retail real estate, it is doing nothing but helping cause once extremely prominent shopping areas become the very same “ghost towns” they turned into during the 2008 housing crisis.

Mayor DeBlasio’s asinine solution to this issue created in part by faulty government policy: more government and more regulation.

So much for the recovery.

As if brick and mortar retail didn’t have enough problems to deal with being methodically decimated by the ever growing behemoth that is Amazon, store owners are now facing rent that is simply so high it makes it impossible for most to open retail stores and do business in once prominent areas of downtown Manhattan.

If you want to see the future of storefront retailing, walk nine blocks along Broadway from 57th to 48th Street and count the stores.

The total number comes to precisely one — a tiny shop to buy drones.

That’s right: On a nine-block stretch of what’s arguably the world’s most famous avenue, steps south of the bustling Time Warner Center and the planned new Nordstrom department store, lies a shopping wasteland.

To be sure, none of this comes as a surprise to us – or our regular readers – because inlate March we recalled our own 2009 tour of Madison Avenueto discover that it also had turned into a ghost town. Just a week ago we told our readers that the ghost town that was New York’s “Golden Mile” was not surprising: after all the US economy had just been hit with the worst recession since the Great Depression, and only an emergency liquidity injection of trillions of dollars prevented a global financial collapse.

What is more surprising is why nearly 9 years later, at a time of what is supposed to be a coordinated global recovery, a walk along Madison Avenue reveals the exact same picture.

We would love for these two sets of facts to bludgeon the government and regulators over the head and make them realize that inflation isn’t the solution. Rather, they should realize from this that deflation can actually be a reward for capitalism, causing prices to fall, increased competition between sellers, and benefits for buyers.

Last month, a Wall Street Journal op-ed posited that the new tax bill could create a mass exodus of roughly800,000 residentsfrom the state of California who will flee the state for low-tax red states.

“In the years to come, millions of people, thousands of businesses, and tens of billions of dollars of net income will flee high-tax blue states for low-tax red states. This migration has been happening for years. But the Trump tax bill’s cap on the deduction for state and local taxes, or SALT, will accelerate the pace. The losers will be most of the Northeast, along with California. The winners are likely to be states like Arizona, Nevada, Tennessee, Texas and Utah.” –WSJ

Taxes aside, anew report by Next 10 and Beacon Economics suggests the California exodus may get a lot worse, as new housing construction since the Great Recession has been tepid at best, and as a result, California faces a housing backlog of 3.4 million unitsby 2025 if the trend continues – and 2.8 million units at the current rate of construction.

From 2007 to 2017, only 24.7 housing permits were filed for every 100 new residents in California – much lower than the U.S. average of 43.1 permits.

By 2025, California would have a housing backlog of 3.4 million units if the trend continues. At the current pace of construction, California would add just a minimal amount of new housing – about 600,000 new housing units (net of housing unit losses due to demolition and other causes) – leaving the state with a housing gap of 2.8 million units by 2025. –Next10

“California’s current housing supply is not able to support its growing population,” the report concludes, and as such “the low levels of construction will likely result in further increases in home prices, such that fewer and fewer California residents will be able to afford homes.“

According to the report, California lost over a million residents in the decade between 2006 and 2016, due primarily to the high cost of housing disproportionately hurting lower income households. Over 20% of those who moved over that decade did so in 2006 – at the height of the housing bubble.

And since American consumers are genetically predisposed to never learning from their mistakes, median home prices in California are once again gapping well above the national average in a very similar pattern, making housing once again prohibitively expensive:

Meanwhile, migration out of California is mostly tied to income, as most of those leaving the state earn less than $30,000 per year.

Those migration patterns are shaped by socioeconomics. Most people leaving the state earn less than $30,000 per year, even as those who can afford higher housing costs are still arriving. As the report noted, California was also a net importer of highly skilled professionals from the information, professional and technical services, and arts and entertainment industries. On the other hand, California saw the largest exodus of workers in accommodation, construction, manufacturing and retail trade industries. –MarketWatch

Crunched California homeowners spent an average of 21.9% of their income on housing expenses in 2016, while home ownership rates are terrible at just 53.6% of homes owner-occupied; the 49th worst in the nation on both counts. California renters meanwhile come in 48th in the nation when it comes to percentage of income spent on housing at 32.8%.

And how are Californians coping with the skyrocketing costs of housing? One strategy is doubling up – as nearly 14% of renters have more than one person per bedroom, making it the state with the highest percentage of overcroweded renter households.

Another solution?

Leaving.

In a separate analysis noted byMarketWatch‘s Andrea Riquier, “Realtor.com found that the number of people searching real estate listings in the 16 top California markets compared to people living there and searching elsewhere was more than double that of other areas — and growing.”

Searches for homes in pricey California towns – primarily Santa Clara, San Mateo and Los Angeles – experienced virtually no increase over the past year, while views of listings in other parts of the country were up 15%.

So where do most broke Californians move? Texas, Arizona, Nevada, Oregon and Washington .

It is official. Consumers in Colorado appear to be tapped out.

This comes at a time when the recovery is now tied for the second-longest economic expansion in American history. The stock market is near an all-time high, unemployment is the lowest in two decades, consumer confidence is beyond euphoric, and Trump tax cuts are stoking the best earnings quarter since 2011 — unleashing a record amount of corporate stock buybacks.

While a real economic recovery could be plausible this late in the business cycle, the unevenness of the recovery has left many residents in Colorado without a paddle. Accelerating real estate and rent prices across Colorado are squeezing residents out of their homes at an alarming pace.

According toABC Denver 7, Denver metro area’s skyrocketing cost of living, stagnate wage growth, and lack of affordable real estate has fueled an enormous housing crisis — overwhelming the state’s eviction courts.

Colorado Center on Law and Policy (CCLP), which has spent decades advocating for tenant rights, warns that an eviction crisis is underway in the Denver region.

ABC Denver 7 said, “27 percent of all civil cases filed in Colorado in 2017 were evictions, which represents 45,000 cases.” In Denver alone, eviction cases accounted for nearly 18 percent (8,000 eviction cases) of all evictions across the state. Arapahoe County, the third-most populated county outside of Denver, experienced the most significant number of eviction cases at nearly 22 percent (10,000 eviction cases) in 2017.

Jack Regenbogen, attorney and policy advocate for the Colorado center on Law and Policy, told ABC Denver 7 that most tenants are underrepresented in eviction court cases. In return, this has led to more evictions forcing tenants out onto the streets. He says about 90 percent of landlords are represented by legal counsel during an eviction process, but less than one percent of tenants have legal assistance.

“Traditionally, Colorado has been a very friendly state towards landlords. We really need our policymakers to begin investing meaningful resources to address this issue,” said adds.

ABC Denver 7 indicates that more than 50 percent of Coloradans are renting, and as court dockets continue to expand with evictions in 2018, the crisis is far from over.

According to the Denver Metro Association of Realtors (DMAR) May housing trends report, the average cost of a single-family home in the Denver metro area edged up, as it hit $543,059 in April. More and more homes are listing in the range between $500,000 to $750,000 than all of the price ranges below $500,000 combined. A spokesman from DMAR said homes priced between $500,000 and $749,000, is now considered the “new norm.”

“This demonstrates home buyer demand remains robust,” said Steve Danyliw, Chairman of the DMAR Market Trends Committee. “As new listings poured into the market, buyers that were waiting for them quickly gobbled them up, driving the average days on market down to 20 days.”

Danyliw, further said housing activity remains stable, but increasing interest rates could have an eventual impact on the real estate market.

Evidence continues to build that housing affordability is getting worse, particularly for everyday Americans. Colorado is the latest example of consumers physically tapping out, as they can no longer afford soaring real estate/rent prices – which is now overwhelming state courts in Denver.

Rents in all unit sizes picked up steam in April. Among the largest cities, Las Vegas, Denver, and Detroit led the pack.

The Rent Cafe’sMonthly Rent Reportfor the 250 largest US cities shows a 3.2% Y-o-Y surge.

The national average rent in April clocked in at $1,377. This marks the highest annual growth rate since the end of 2016.

By Size

Large cities: Las Vegas sees the fastest increasing rents Y-o-Y (6.0%), followed by Denver (5.8%) and Detroit (5.4%). Apartment prices in Brooklyn and Manhattan continue to slide, while rents in Washington,D.C., Portland, and Austin have been steady, growing by less than 1.5%.

Mid-size cities: Rents in Sacramento cooled down to 6%, but still lead. At the other end of the spectrum are New Orleans (-2.2%), Tulsa (0.5%), and Wichita (1.0%), where rents are growing the slowest.