QUESTION: Mr. Armstrong, I think I am starting to see the light you have been shining. Negative interest rates really are “completely insane”. I also now see that months after you wrote about central banks were trapped, others are now just starting to entertain the idea. Is this distinct difference in your views that eventually become adopted with time because you were a hedge fund manager?

ANSWER: I believe the answer is rather simple. How can anyone pretend to be analysts if they have never traded? It would be like a man writing a book explaining how it feels to give birth. You cannot analyze what you have never done. It is just impossible. Those who cannot teach and those who can just do. Negative interest rates are fueling deflation. People have less income to spend so how is this beneficial? The Fed always needed 2% inflation. The father of negative interest rates is Larry Summers. He teaches or has been in government. He is not a trader and is clueless about how markets function. I warned that this idea of negative interest rates was very dangerous.

Yes, I have warned that the central banks are trapped. Their QE policies have totally failed. There were numerous “analysts” without experience calling for hyperinflation, collapse of the dollar, yelling the Fed is increasing the money supply so buy gold. The inflation never appeared and gold declined. Their reasoning was so far off the mark exactly as people like Larry Summers. These people become trapped in their own logic it becomes irrational gibberish. They only see one side of the coin and ignore the rest.

Central banks have lost all ability to manage the economy even in theory thanks to this failed reasoning. They have bought-in the bonds and are unable to ever resell them again. If they reverse their policy of QE and negative interest rates, government debt explodes with insufficient buyers. If the central banks refuse to reverse this crazy policy of QE and negative interest rates they will see a massive capital flight from government to the private sector once the MAJORITY realize the central banks are incapable of any control.

The central banks have played a very dangerous game and lost. It appears we are facing the collapse of Social Security which began August 14th, 1935 (1935.619) because they stuffed with government debt and robbed the money for other things. Anyone else would go to prison for what politicians have done and prosecutors would never defend the people because they want to become famous politicians. We will probably see the end of this Social Security program by 2021.772 (October 9th, 2021), or about 89 weeks into the next business cycle. These people are completely incompetent to manage the economy and we are delusional to think people with no experience as a trader can run things. If you have never traded, you have no busy trying to “manipulate” society with you half-baked theories. So yes. The central banks are trapped. They have lost ALL power. It becomes just a matter of time as the clock ticks and everyone wakes up and say: OMG!

We have government addicted to borrowing and if rates rise, then everything will explode in their face. Western Civilization is finished as we know it just as Communism collapsed because we too subscribe to the theory of Marx that government is capable of managing the economy. Just listen to the candidates running for President. They are all preaching Marx. Vote for me and I will force the economy to do this. IMPOSSIBLE! We have debt which is unsustainable the further you move away from the United States which is the core economy such as emerging markets. Unfunded pensions destroyed the Roman Empire. We are collapsing in the very same manner and for the very same reason. We are finishing a very very very important report on the whole pension crisis issue worldwide.

This predatory exploitation is only possible if the central bank and state have partnered with financial Elites.

After decades of denial, the mainstream has finally conceded that rising income and wealth inequality is a problem–not just economically, but politically, for as we all know wealth buys political influence/favors, and as we’ll see below, the federal government enables and enforces most of the skims and scams that have made the rich richer and everyone else poorer.

Here’s the problem in graphic form: from 1947 to 1979, the family income of the top 1% actually expanded less that the bottom 99%. Since 1980, the income of the 1% rose 224% while the bottom 80% barely gained any income at all.

Globalization, i.e. offshoring of jobs, is often blamed for this disparity, but as I explained in “Free” Trade, Jobs and Income Inequality, the income of the top 10% broke away from the bottom 90% in the early 1980s, long before China’s emergence as an exporting power.

Indeed, by the time China entered the WTO, the top 10% in the U.S. had already left the bottom 90% in the dust.

The only possible explanation of this is the rise of financialization: financiers and financial corporations (broadly speaking, Wall Street, benefited enormously from neoliberal deregulation of the financial industry, and the conquest of once-low-risk sectors of the economy (such as mortgages) by the storm troopers of finance.

Financiers skim the profits and gains in wealth, and Main Street and the middle / working classes stagnate. Gordon Long and I discuss the ways financialization strip-mines the many to benefit the few in our latest conversation (with charts): Our “Lawnmower” Economy.

Many people confuse the wealth earned by people who actually create new products and services with the wealth skimmed by financiers. One is earned by creating new products, services and business models; financialized “lawnmowing” generates no new products/services, no new jobs and no improvements in productivity–the only engine that generates widespread wealth and prosperity.

Consider these favorite financier “lawnmowers”:

1. Buying a company, loading it with debt to cash out the buyers and then selling the divisions off: no new products/services, no new jobs and no improvements in productivity.

2. Borrowing billions of dollars in nearly free money via Federal Reserve easy credit and using the cash to buy back corporate shares, boosting the value of stock owned by insiders and management: no new products/services, no new jobs and no improvements in productivity.

3. Skimming money from the stock market with high-frequency trading (HFT): no new products/services, no new jobs and no improvements in productivity.

4. Borrowing billions for next to nothing and buying high-yielding bonds and investments in other countries (the carry trade): no new products/services, no new jobs and no improvements in productivity.

All of these are “lawnmower” operations, rentier skims enabled by the Federal Reserve, its too big to fail banker cronies, a complicit federal government and a toothless corporate media.

This is not classical capitalism; it is predatory exploitation being passed off as capitalism. This predatory exploitation is only possible if the central bank and state have partnered with financial Elites to strip-mine the many to benefit the few.

This has completely distorted the economy, markets, central bank policies, and the incentives presented to participants.

“A key empirical question in the inequality debate is to what extent rich people derive their wealth from “rents”, which is windfall income they did not produce, as opposed to activities creating true economic benefit.

Political scientists define “rent-seeking” as influencing government to get special privileges, such as subsidies or exclusive production licenses, to capture income and wealth produced by others.

However, Joseph Stiglitz counters that the very existence of extreme wealth is an indicator of rents.

Competition drives profit down, such that it might be impossible to become extremely rich without market failures. Every good business strategy seeks to exploit one market failure or the other in order to generate excess profit.

The bottom-line is that extreme wealth is not broad-based: it is disproportionately generated by a small portion of the economy.”

This small portion of the economy depends on the central bank and state for nearly free money, bail-outs, guarantees that profits are private but losses are shifted to the taxpaying public–all the skims and scams we’ve seen protected for seven long years by Democrats and Republicans alike.

Learn how our “Lawnmower Economy” works (with host Gordon Long; 26:21 minutes)

The S&P 500 closed today exactly where it first crossed in November 2014. In the interim, its been a roller-coaster of rips, dips, spills and thrills.

The thing is, however, this extended period of sideways churning has not materialized under a constant economic backdrop; it does not reflect a mere steady-state of dare-doing at the gaming tables.

Actually, earnings have been falling sharply and macroeconomic headwinds have been intensifying dramatically. So the level of risk in the financial system has been rocketing higher even as the stock averages have labored around the flat-line.

Thus, GAAP earnings of the S&P 500 in November 2014 were $106 per share on an LTM basis compared to $86.44today. So earnings are down by 18.5%, meaning that the broad market PE multiple has escalated from an already sporty 19.3Xback then to an outlandish 23.7Xtoday.

Always and everywhere, such persistent profit collapses have signaled recession just around the corner. And there are plenty of macro-economic data points signaling just that in the remainder of this article (here)

The pessimists are already talking about 3% inflation later this year if energy prices don’t retreat. Most likely, Federal Reserve monetary experimentation will inflict a new great inflation on the U.S., although this is much more likely to occur in the next business cycle rather than the current one. Before that, we’ll get the shock of an economic slowdown — or even recession — which will exert some pause. So many households are right to ask whether their main asset will insulate them from this shock whenever it occurs. The answer from economic science is no.

House prices perform best during the asset-price inflation phase of the monetary cycle. During that period, low or zero rates stimulate investors to search for yield, which many do, shedding their normal skepticism. The growth in irrationality across many marketplaces is why some economists describe set price inflation as a “disease.” Usually, the housing and commercial real estate markets become infected by this disease at some stage.

Real estate markets are certainly not shielded from irrational forces. “Speculative stories” about real estate flourish and quickly gain popularity — whether it’s the ever-growing housing shortage in metropolitan centers; illicit money pouring into the top end from all over the world and high prices rippling down to lower layers of the market; or bricks and mortar (and land), the ultimate safe haven when goods and services inflation ultimately accelerates.

That last story defies much economic experience to the contrary. By the time inflation shock emerges, home prices have already increased so much in real terms under asset-price inflation that they cannot keep up with goods and services inflation, and may even fall in nominal terms. One thinks of the tale of the gold price in the Paris black market during World War II: prices hit their peak just before the Germans entered the city in May 1940 and never returned.

Real estate is only a hedge against high inflation if it is bought early on in the preceding asset-price inflation period. We can generalize this lesson. The arrival of high inflation is an antidote to asset-price inflation. That is, if it has not already reached its late terminal stage when speculative temperatures are falling across an array of markets.

To understand how home prices in real terms behave under inflation shock we must realize how, in real terms, they are driven by expectations of future rents (actual, or as given to homeowners); the cost of capital; and the profit from carry trade. All of these drivers have been operating in the powerful asset-price inflation phase the U.S. and many foreign countries have been experiencing during recent years.

Together they have pushed up the S&P Case Shiller national home price index to almost 20% above its long-run trend (0.6% each year since 1998), having fallen slightly below at its trough in 2011, and having reached a peak 85% above in 2006.

The cost of equity is low, judging by high underlying price earnings ratios in the stock markets. Investors suffering from interest income famine are willing to put a higher price on future earnings, whether in the form of house rents or corporate profits, than they would do under monetary stability.

Leveraged owners of real estate can earn a handsome profit between rental income and interest paid, especially taking account of steady erosion of loan principal by inflation and tax deductions.

The arrival of high inflation would change all these calculations.

Cost of equity would rise as markets feared the denouement of recession, and reckoned with the new burden on economic prosperity. Long-term interest rates would climb starkly in nominal terms. Their equivalent in real terms would be highly volatile and unpredictable, albeit at first low in real terms (inflation-adjusted), meaning that carry trade income for leveraged owners would become elusive.

None of this is to suggest that a high inflation shock is likely in the second quarter. A sustained period of much stronger demand growth across an array of goods, services and labor markets would most likely have to occur first, and could be seen as early as the next cyclical upturn.

An economic miracle could bring a reprieve from inflation. But much more likely, the infernal inflation machine of expanding budget deficits and Fed experimentation will ultimately mow down any resistance in its way.

Several months ago, a chart produced by one of the Big Banks was presented to readers . It was supposed to be innocuous data on global wealth distribution, but instead portrayed a horrifying picture.

The focal point of the aforementioned article was that when it came to “the world’s poorest people,” the Corrupt West has now produced a greater percentage of severe poverty in its own populations than in India, and an equal percentage of such poverty as exists in Africa.

Stacked beside this, we see that when it comes to the richest-of-the-rich, the Corrupt West remains in a league of its own. Supposedly, we are living in “the New Normal,” where life is supposed to get increasingly harder and harder. So why does the New Normal never affect those on top?

Of course all of these extremely poor people being manufactured by our governments (as these regimes give away our jobs, destroy wages, and eviscerate our social programs) have to come from somewhere. Certainly they don’t come from the Wealthy Class.

Indeed, the chart above provides us with a crystal-clear view of where all these poor and very-poor people are coming from: the near-extinct Middle Class. In order to manufacture hundreds of millions of impoverished citizens in our nations, the Old World Order has had to engage in a campaign to end the Middle Class.

We are conditioned to consider economic “classes” within our own societies, but with the chart above, we’re given a global perspective. Where does the Middle Class exist today, globally? At the upper end, it exists in China, and to a lesser extent, in Latin America and other Asian nations. At the lower end of the Middle Class, we see such populations growing in India and even Africa.

Only in the West, and especially North America, is the Middle Class clearly an endangered species. Two incredibly important aspects of this subject are necessary to cover:

1) How and why has the One Bank chosen to perpetrate Middle Class genocide?

2) What are the consequences of the Death of the Middle Class?

Attempting to catalogue the nearly infinite number of ways in which the oligarchs of the One Bank have perpetrated their Middle Class genocide is impractical. Instead, discussion will be limited to the five most important programs responsible for the Death of the Middle Class: three of them relatively new, and two of them old.

a) Globalization

b) Union decimation/wage destruction

c) Small business decimation

d) Money-printing/inflation

e) Income taxation

Globalization was rammed down our throats in the name of “free trade,” the Holy Grail of charlatan economists . But, as previously explained, real free trade is a world of “comparative advantage” where all nations play by a fair-and-equal set of rules. Without those conditions, “free trade” can never exist.

The globalization that has been imposed upon us is, instead, a world of “competitive devaluation,” a corrupt, perpetual, suicidal race to the bottom. The oligarchs understood this, given that they are the perpetrators. The charlatan economists were too blinded by their own dogma to understand this. And, as always, the puppet politicians simply do what they are told.

Next on the list: union decimation and wage destruction are inseparable subjects, virtually the flip side of the same coin. “But wait,” shout the right-wing ideologues, “unions are corrupt, everyone knows that.”

Really? Corrupt compared to whom? Are they “corrupt” standing next to the bankers, who have stolen all our wealth ? Are they “corrupt” standing next to their Masters, the oligarchs who are hoarding all our stolen wealth ? Are they “corrupt” standing next to our politicians, who betrayed their own people to facilitate this economic pillaging? No, compared to any of those groups, unions (back when they still existed) were relative choir-boys.

When it comes to corruption, nobody plays the game as well as those on top. Compared to the Fat Cats, everyone else are rank amateurs. When unions were strong and plentiful, everyone had jobs. Almost everyone earned a livable wage (or better). Gee, weren’t those terrible times! Look how much better off we are now, without all those “corrupt unions.”

The other major new component in the deliberate, systemic slaughter of the Middle Class was and continues to be Small Business decimation. “Small business is the principal job-creator in every economy.” Any politician who ever got elected can tell you that.

If this is so, why do our corrupt governments funnel endless trillions of dollars of Corporate Welfare (our money) into the coffers of Big Business, while complaining there is nothing left to support Small Business? Why do our governments stack the deck in all of our regulations and bureaucracies, greasing the wheels for Big Business and strangling Small Business in their red tape?

Why do our governments refuse to enforce our anti-trust laws? One of the primary reasons for not allowing the corporations of Big Business to grow to an illegal size is because these monopolies and oligopolies make “competition” (meaning Small Business) impossible. One might as well try to start a small business on the Moon.

Then we have the oligarchs’ “old tricks” for stealing from the masses (and fattening themselves): banking and taxation. Of course, to the oligarchs, “banking” means stealing, and you steal by printing money. As many readers are already aware, “inflation” is money-printing – the increase (or inflation) of the supply of money.

“In the absence of the gold standard, there is no way to protect savings [i.e. wealth] from confiscation through inflation”

Remove the Golden Handcuffs , as central banker Paul Volcker bragged of doing in 1971, and then it’s just print-and-steal – until the whole fiat currency Ponzi scheme implodes.

Then of course we have income taxation: 100 years of systemic thievery. No matter what the form or structure, by its very nature every system of income taxation will:

i) Provide a free ride to those at the very, very top

ii) Be revenue-neutral to the remainder of the wealthy

iii) Relentlessly steal out of the pockets of everyone else (via over-taxation)

This is nothing more than a matter of applying simple arithmetic. However, many refuse to educate themselves on how they are being robbed in this manner, year after year, so no more will be said on the subject.

These were the primary prongs of the oligarchs’ campaign to exterminate the Middle Class. As always, skeptical readers will be asking “why?” The answer is most easily summarized via The Bankers’ Manifesto of 1892 . This document was presented to the U.S. Congress in 1907 by Republican congressman, and career prosecutor, Charles Lindbergh Sr.

It reads, in part:

The courts must be called to our aid, debts must be collected, bonds and mortgages foreclosed as rapidly as possible.

When through the process of law, the common people have lost their homes they will be more tractable and easily governed through the influence of the strong arm of government applied to a central power of imperial wealth under the control of the leading financiers [the oligarchs]. People without homes won’t quarrel with their leaders.

We have “the strong arm of government.” The oligarchs saw to that by bringing us their “War on Terror.” When it comes to throwing people out of their homes, and creating a population of serfs, that’s a two-part process.

Step 1 is to manufacture artificial housing bubbles across the Western world, and then crash those bubbles. However, this is only partially effective in turning Homeowners into Homeless. To truly succeed at this requires Step 2: exterminating the Middle Class. A Middle Class can survive a collapsing housing bubble, assuming they remained reasonably prudent. The Working Poor cannot.

Finally, after more than a century of scheming, the oligarchs have all of their pieces in place. In the U.S., they’ve even already built many gulags – to warehouse these former Middle Class homeowners – since a large percentage of those people are armed.

This brings us to one, final point: the consequences of the Death of the Middle Class. What happens when you destroy the foundation of a house? Just look.

As readers have been told on many previous occasions, the “velocity of money” is effectively the heartbeat of an economy. It is another way of representing the economics principle known as the Marginal Propensity to Consume, probably the most important principle of economics forgotten by charlatan economists.

The principle is a simple one, since it is half basic arithmetic and half common sense. Unfortunately, these are both skills beyond the grasp of charlatan economists. If you take all of the money out of the pockets of the People, and you stuff it all into the vaults of the wealthy (where it sits in idle hoards), then there is no “capital” for our capitalist economies – and these economiesstarve to death.

What is the response of the oligarchs to the relentless hollowing-out of our economies? They have ordered the puppet politicians to impose Austerity: taking even more money out of the pockets of the people. It is the equivalent to someone with anorexia going to a doctor, and the doctor imposing a severe diet on the patient (i.e. victim). The patient will not survive.

The Middle Class is dying. Unlike the oligarchs’ Big Banks, we are not “too big to fail.”Our jobs are gone. Our unions are gone. Our Middle Class wages are gone. Very soon, our homes will be gone. But don’t worry! It’s just the New Normal.

On the surface, the March jobs reported was better than expected… except for manufacturing workers. As shown in the chart below, in the past month, a disturbing 29,000 manufacturing jobs were lost. This was the single biggest monthly drop in the series going back to December 2009.

But not all is lost: as has been the case for virtually every month during the “recovery”, virtually every laid off manufacturing worker could find a job as a waiter: in March, the workers in the “Food services and drinking places” category, aka waiters, bartenders and minimum wage line cooks, rose again to a new record high of 11,307,000 workers, an increase of 25K in the month, offsetting virtually all lost manufacturing jobs.

This is how the two job series have looked since the start of 2015.

And here is the longer-term, going back to the start of the crisis in December 2007: please do not “peddle fiction” upon seeing this chart.

US Manufacturing Surveys Bounce Despite The Biggest Industry Job Losses In 7 Years

Following China’s miraculous PMI jump back into expansion, Markit reports US Manufacturing also rose to 51.5 in March (despite the biggest drop in manufacturing jobs since 2009). As Markit details, output growth is unchanged from February’s 28-month low, and prices charged decline amid further drop in input costs. ISM Manufacturing also jumpedfrom 49.5 to 51.8 – the first ‘expansion’ in 7 months. Finally, we note that ISM Prices Paid exploded higher (from 38.5 to 51.5) – the biggest jump since Aug 2012.

“V”-shaped recovery in ISM Manufacturing

All of which occurred as the manufacturing sector lost more jobs in March than at any time since 2009…

Every ISM Respondent thinks everything is awesome…

“Unemployment rate is low in our county, making it hard to find workers. We are understaffed and running lots of overtime.” (Plastics & Rubber Products)

“Business in telecom is booming. Fiber plant is at capacity.” (Chemical Products)

“Current trends remain steady. No issues with delivery or costs.” (Computer & Electronic Products) “Capital equipment sales are steady.” (Fabricated Metal Products)

“Requests for proposals for new equipment [are] very strong.” (Machinery)

“Government is spending again. Have received delivery orders.” (Transportation Equipment)

“Things are starting to pick up. Our business is seasonal and it is that time of year.” (Printing & Related Support Activities)

“Business conditions are stable, little change from last month.” (Miscellaneous Manufacturing)

“Incoming sales are improving.” (Furniture & Related Products)

“Our business is still going strong.” (Primary Metals)

But as Markit details, output growth is unchanged from February’s 28-month low, and prices charged decline amid further drop in input costs:

“March’s survey highlights sustained weakness across the US manufacturing sector, meaning that overall growth through the first quarter slowed to its lowest since late-2012. Subdued client spending patterns within the energy sector, ongoing pressure from the strong dollar, and general uncertainty about the business outlook were cited as factors weighing on new order flows in March.

“Meanwhile, price discounting strategies resulted in the first back-to-back drop in factory gate charges for around three-and-a-half years, suggesting another squeeze on margins despite lower materials costs across the manufacturing sector.“

So – to summarize, US manufacturing sector lost more jobs in March than at any time since 2009 BUT the managers that were surveyed by ISM and Markit proclaimed expansion is back and this puts all the pressure back on The Fed once again as more excuses are lost for hiking rates.

Yellen Says Caution in Raising Rates Is ‘Especially Warranted’ … Fed Chair makes case for go-slow changes with rate near zero … Janet Yellen said it is appropriate for U.S. central bankers to “proceed cautiously” in raising interest rates because the global economy presents heightened risks. The speech to the Economic Club of New York made a strong case for running the economy hot to push away from the zero boundary for the Federal Open Market Committee’s target rate. –Bloomberg

Janet Yellen was back at it yesterday, talking down the need for a rate hike.

She is comfortable with the economy running “hot.”

Say what?

After a year or more of explaining why rate hikes were necessary, up to four or more of them in 2016, Ms. Yellen has now begun speechifying about how rate hikes are not a good idea.

It’s enough to give you whiplash.

It sets the stage for increased stagflation in the US and increased price inflation in China. More in a moment.

Here’s the real story. At the last G20 meeting in February, secret agreements were made between the most powerful economies to lift both the US and Chinese economy.

The details of these deals have been leaked on the Internet over the past few weeks and supported by the actions of central bankers involved.

It is what The Daily Reckoning last week called “The most important financial development of 2016, with enormous implications for you and your portfolio.”

The Fed and other members of the G20, which met in February, intend to maintain the current Chinese system.

They want China to stay strong economically.

The antidote to China’s misery, according to the Keynsian-poisoned G20, is more yuan printing. More liquidity that will supposedly boost the Chinese economy.

As a further, formal yuan loosening would yield a negative impact felt round the world, other countries agreed to tighten instead.

This is why Mario Draghi suddenly announced that he was ceasing his much asserted loose-euro program. No one could figure out why but now it’s obvious.

Same thing in Japan, where central bank support for aggressive loosening has suddenly diminished.

The US situation is more complicated. The dollar’s strength is now seen as a negative by central bankers and thus efforts are underway to weaken the currency.

A weaker dollar and a weaker yen supposedly create the best scenario for a renewed economic resurgence worldwide.

The euro and the yen rose recently against the dollar after it became clear that their central banks had disavowed further loosening.

Now Janet Yellen is now coming up with numbers and statistics to justify backing away from further tightening.

None of these machinations are going to work in the long term. And even in the short term, such currency gamesmanship is questionable in the extreme, as the Daily Reckoning and other publications have pointed out when commenting on this latest development.

In China, a weaker yuan will create stronger price inflation. In the US, a weaker dollar will boost stagflation.

We’ve often made a further point: Everything central bankers do is counterproductive on purpose.

The real idea is to make people so miserable that they will accede to further plans for increased centralization of monetary and governmental authority.

Slow growth or no growth in Japan and Europe, supported by monetary tightening, are certainly misery-making.

Stagflation in the US and Canada is similarly misery-provoking, as is price-inflation in China.

Nothing is what it seems in the economic major leagues.

Central banks are actually mandated to act as a secret monopoly, supervised by the Bank for International Settlements and assisted by the International Monetary Fund.

Deceit is mandated. As with law enforcement, central bankers are instructed to lie and dissemble for the “greater good.”

It’s dangerous too.

The Fed along with other central banks have jammed tens of trillions into the global economy over the past seven years. Up to US$100 trillion or more.

They’ve been using Keynesian monetary theories to try to stimulate global growth.

It hasn’t worked of course because money is no substitute for human action. If people don’t want to invest, they won’t.

In the US, the combination of low growth and continual price inflation creates a combination called “stagflation.”

It appeared in its most serious form in the 1970s but it is a problem in the 2000s as well.

According to non-government sources like ShadowStats, Inflation is running between four and eight percent in the US while formal unemployment continues to affect an astonishing 90 million workers.

US consumers on average are said to be living from paycheck to paycheck (if they’ve even got one) with almost no savings.

Some 40 million or more are on foodstamps.

Many workers in the US are probably engaged in some kind of off-the-books work and are concealing revenue from taxation as well.

As US economic dysfunction continues and expands, people grow more alienated and angry. This is one big reason for the current political season with its surprising dislocation of the established political system.

But Yellen has made a deal with the rest of the G20 to goose the US economy, or at least to avoid the further shocks of another 25 basis point rate hike in the near future.

Take their decisions at face value, and these bankers are too smart for their own good.

Expanding US growth via monetary means has created asset bubbles in the US but not much real economic growth.

And piling more yuan on the fire in China is only going to make Chinese problems worse in the long term. More resources misdirected into empty cities and vacant skyscrapers – all to hold off the economic day of reckoning that will arrive nonetheless.

Conclusion: As we have suggested before, the reality for the US going forward is increased and significant stagflation. Low employment, high price inflation. On the bright side, this will push up the prices of precious metals and real estate. Consider appropriate action.

Money is leaving China in myriad ways, chasing after overseas assets in near-panic mode. So Anbang Insurance Group, after having already acquired the Waldorf Astoria in Manhattan a year ago for a record $1.95 billion from Hilton Worldwide Holdings, at the time majority-owned by Blackstone, and after having acquired office buildings in New York and Canada, has struck out again.

It agreed to acquire Strategic Hotels & Resorts from Blackstone for a $6.5 billion. The trick? According to Bloomberg’s “people with knowledge of the matter,” Anbang paid $450 million more than Blackstone had paid for it three months ago!

Other Chinese companies have pursued targets in the US, Canada, Europe, and elsewhere with similar disregard for price, after seven years of central-bank driven asset price inflation [read… Desperate “Dumb Money” from China Arrives in the US].

As exports of money from China is flourishing at a stunning pace, exports of goods are deteriorating at an equally stunning pace. February’s 25% plunge in exports was the 11th month of year-over-year declines in 12 months, as global demand for Chinese goods is waning.

And ocean freight rates – the amount it costs to ship containers from China to ports around the world – have plunged to historic lows.

The China Containerized Freight Index (CCFI), published weekly, tracks contractual and spot-market rates for shipping containers from major ports in China to 14 regions around the world. Unlike most Chinese government data, this index reflects the unvarnished reality of the shipping industry in a languishing global economy. For the latest reporting week, the index dropped 4.1% to 705.6, its lowest level ever.

It has plunged 34.4% from the already low levels in February last year and nearly 30% since its inception in 1998 when it was set at 1,000. This is what the ongoing collapse in shipping rates looks like:

The rates dropped for 12 of the 14 routes in the index. They rose in only one, to the Persian Gulf/Red Sea, perhaps in response to the lifting of the sanctions against Iran, and remained flat to Japan. Rates on all other routes dropped, including to Europe (-7.9%), the US West Coast (-3.5%), the US East Coast (-1.0%), or the worst drop, to the Mediterranean (-13.4%).

The Shanghai Containerized Freight Index (SCFI), which is much more volatile than the CCFI, tracks only spot-market rates (not contractual rates) of shipping containers from Shanghai to 15 destinations around the world. It had surged at the end of last year from record lows, as carriers had hoped that rate increases might stick this time and that the worst was over. But rates plunged again in the weeks since, including 6.8% during the last reporting week to 404.2, a new all-time low. The index is now down 62.3% from a year ago:

Rates were flat for three routes, but dropped for the other 12 routes, including to Europe, where rates plunged nearly 10% to a ludicrously low $211 per TEU (twenty-foot equivalent container unit). Rates to the US West Coast fell 8.4% to $810 per FEU (forty-foot equivalent container unit). Rates to the East Coast fell 5.2% to $1,710 per FEU. Rates to South America plunged 25.4%.

This crash in shipping rates is a result of two by now typical forces: rampant and still growing overcapacity and lackluster demand.

“Typical” because lackluster demand has been the hallmark of the global economy recently, and the problems of overcapacity have also been occurring in other sectors, including oil & gas and the commodities complex. Overcapacity from coal-mining to steel-making, much of it in state-controlled enterprises, has been dogging China for years and will continue to pose mega-problems well into the future. Overcapacity kills prices, then jobs, and then companies.

The ocean freight industry went on a multi-year binge buying the largest container ships the world has ever seen and smaller ones too. It was led by executives who believed in the central-bank dogma that radical monetary policy will actually stimulate the real economy, and they were trying to prepare for it. And it was made possible by central-bank-blinded yield-chasing investors and giddy bankers. As a result, after years of ballooning capacity, carriers added another 8% in 2015, even while demand for transporting containers across the oceans languished near the flat line, the worst performance since 2009.

“The market wants to do it’s sole job which is to establish fair market value. I am talking currencies, housing, crude oil, derivatives and the stock market. This will correct to fair market value. It’s a mathematical certainty, and it’s already begun.”

Financial analyst and trader Gregory Mannarino thinks the coming market crash will be especially bad for people not awake or prepared. Mannarino says, “This is going to get a lot worse. On an individual level, we have to understand what we have to do for ourselves and our families to get through this. No matter what is happening on the political front, there is no stopping what is coming. . . . We’re going back to a two-tier society. We are seeing it happen. The middle class is being systematically destroyed. We are going to have a feudal system of the haves and the have nots. People walking around blindly thinking it’s going to be okay are going to suffer the worst.”

Mannarino’s advice is to “Bet against this debt, and that means hold hard assets; also, become your own central bank. Their system has already failed and it’s coming apart.”

We grow up being taught a very specific set of principles.

One plus one equals two. I before E, except after C.

As we grow older, the principles become more complex.

Take economics for example.

The law of supply states that the quantity of a good supplied rises as the market price rises, and falls as the price falls. Conversely, the law of demand states that the quantity of a good demanded falls as the price rises, and vice versa.

These basic laws of supply and demand are the fundamental building blocks of how we arrive at a given price for a given product.

At least, that’s how it’s supposed to work.

But what if I told you that the principles you grew up learning is wrong?

With today’s “creative” financial instruments, much of what you learned no longer applies in the real world.

Especially when it comes to oil.

The Law of Oil

Long time readers of this Letter will have read many of my blogs regarding commodities manipulation.

With oil, price manipulation couldn’t be more obvious.

“…While agencies have found innovative ways to explain declining oil demand, the world has never consumed more oil.

In 2010, the world consumed a record 87.4 million barrels per day. This year (2014), the world is expected to consume a new record of 92.7 million barrels per day.

Global oil demand is still expected to climb to new highs.

If the price of oil is a true reflection of supply and demand, as the headlines tell us, it should reflect the discrepancy between supply and demand.

Since we know that demand is actually growing, that can’t be the reason for oil’s dramatic drop.

So does that mean it’s a supply issue? Did the world all of a sudden gain 40% more oil? Obviously not.

So no, the reason behind oil’s fall is not the causality of supply and demand.

The reason is manipulation. The question is why.

I go on to talk about the geopolitical reasons of why the price of oil is manipulated.

“On September 11, Saudi Arabia finally inked a deal with the U.S. to drop bombs on Syria.

But why?

Saudi Arabia possesses 18 per cent of the world’s proven petroleum reserves and ranks as the largest exporter of petroleum.

Syria is home to a pipeline route that can bring gas from the great Qatar natural gas fields into Europe, making billions of dollars for Saudi Arabia as the gas moves through while removing Russia’s energy stronghold on Europe.

Could the U.S. have persuaded Saudi Arabia, during their September 11 meeting, to lower the price of oil in order to hurt Russia, while stimulating the American economy?

… On October 1, 2014, shortly after the U.S. dropped bombs on Syria on September 26 as part of the September 11 agreement, Saudi Arabia announced it would be slashing prices to Asian nations in order to “compete” for crude market share. It also slashed prices to Europe and the United States.”

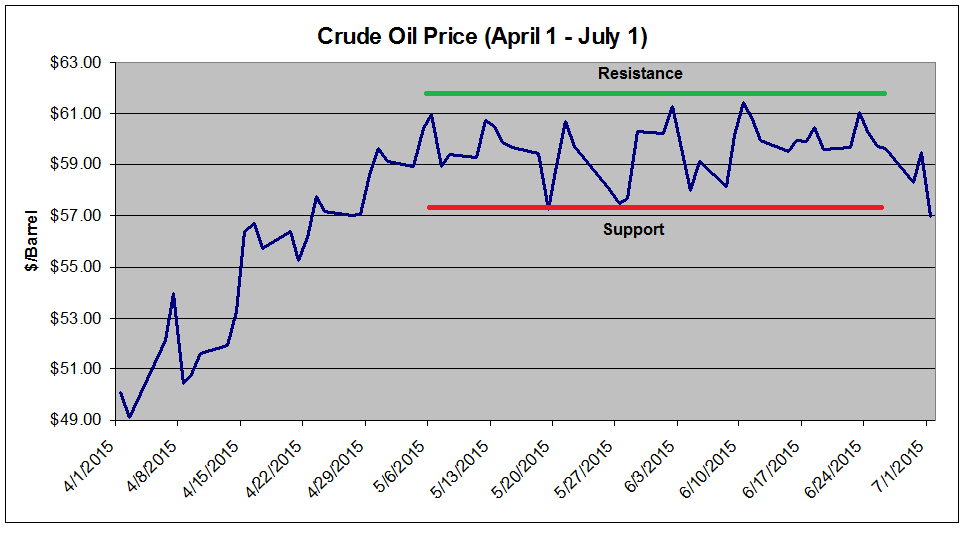

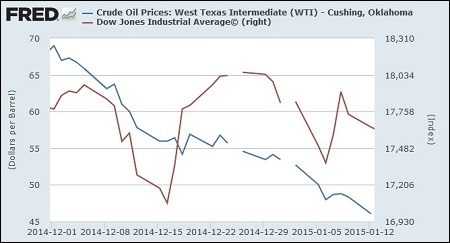

Following Saudi Arabia’s announcement, oil prices have plunged to a level not seen in more than five years.

Is it a “coincidence” that shortly after the Saudi Arabia-U.S. meeting on the coincidental date of 9-11, the two nations inked a deal to drop billions of dollars worth of bombs on Syria? Then just a few days later, Saudi Arabia announces a massive price cut to its oil.

Coincidence?

There are many other factors – and conspiracies – in oil price manipulation, such as geopolitical attacks on Russia and Iran, whose economies rely heavily on oil. Saudi Arabia is also flooding the market with oil – and I would suggest that it’s because they are rushing to trade their oil for weapons to lead an attack or beef up their defense against the next major power in the Middle East, Iran.

However, all of the reasons, strategies or theories of oil price manipulation could only make sense if they were allowed by these two major players: the regulators and the Big Banks.

How Oil is Priced

On any given day, if you were to look at the spot price of oil, you’d likely be looking at a quote from the NYMEX in New York or the ICE Futures in London. Together, these two institutions trade most of the oil that creates the global benchmark for oil prices via oil futures contracts on West Texas Intermediate (WTI) and North Sea Brent (Brent).

What you may not see, however, is who is trading this oil, and how it is being traded.

Up until 2006, the price of oil traded within reason. But all of a sudden, we saw these major price movements. Why?

“Until recently, U.S. energy futures were traded exclusively on regulated exchanges within the United States, like the NYMEX, which are subject to extensive oversight by the CFTC, including ongoing monitoring to detect and prevent price manipulation or fraud.

In recent years, however, there has been a tremendous growth in the trading of contracts that look and are structured just like futures contracts, but which are traded on unregulated OTC electronic markets. Because of their similarity to futures contracts they are often called ”futures look-a likes.”

The only practical difference between futures look-alike contracts and futures contracts is that the look-a likes are traded in unregulated markets whereas futures are traded on regulated exchanges.

The trading of energy commodities by large firms on OTC electronic exchanges was exempted from CFTC oversight by a provision inserted at the behest of Enron and other large energy traders into the Commodity Futures Modernization Act of 2000 in the waning hours of the 106th Congress.

The impact on market oversight has been substantial.

NYMEX traders, for example, are required to keep records of all trades and report large trades to the CFTC. These Large Trader Reports (LTR), together with daily trading data providing price and volume information, are the CFTC’s primary tools to gauge the extent of speculation in the markets and to detect, prevent, and prosecute price manipulation.

…In contrast to trades conducted on the NYMEX, traders on unregulated OTC electronic exchanges are not required to keep records or file Large Trader Reports with the CFTC, and these trades are exempt from routine CFTC oversight.

In contrast to trades conducted on regulated futures exchanges, there is no limit on the number of contracts a speculator may hold on an unregulated OTC electronic exchange, no monitoring of trading by the exchange itself, and no reporting of the amount of outstanding contracts (”open interest”) at the end of each day.

The CFTC’s ability to monitor the U.S. energy commodity markets was further eroded when, in January of this year (2006), the CFTC permitted the Intercontinental Exchange (ICE), the leading operator of electronic energy exchanges, to use its trading terminals in the United States for the trading of U.S. crude oil futures on the ICE futures exchange in London-called ”ICE Futures.”

Previously, the ICE Futures exchange in London had traded only in European energy commodities-Brent crude oil and United Kingdom natural gas. As a United Kingdom futures market, the ICE Futures exchange is regulated solely by the United Kingdom Financial Services rooority. In 1999, the London exchange obtained the CFTC’s permission to install computer terminals in the United States to permit traders here to trade European energy commodities through that exchange.

Then, in January of this year, ICE Futures in London began trading a futures contract for West Texas Intermediate (WTI) crude oil, a type of crude oil that is produced and delivered in the United States. ICE Futures also notified the CFTC that it would be permitting traders in the United States to use ICE terminals in the United States to trade its new WTI contract on the ICE Futures London exchange.

Beginning in April, ICE Futures similarly allowed traders in the United States to trade U.S. gasoline and heating oil futures on the ICE Futures exchange in London. Despite the use by U.S. traders of trading terminals within the United States to trade U.S. oil, gasoline, and heating oil futures contracts, the CFTC has not asserted any jurisdiction over the trading of these contracts.

Persons within the United States seeking to trade key U.S. energy commodities-U.S. crude oil, gasoline, and heating oil futures-now can avoid all U.S. market oversight or reporting requirements by routing their trades through the ICE Futures exchange in London instead of the NYMEX in New York.

As an increasing number of U.S. energy trades occurs on unregulated, OTC electronic exchanges or through foreign exchanges, the CFTC’s large trading reporting system becomes less and less accurate, the trading data becomes less and less useful, and its market oversight program becomes less comprehensive.

The absence of large trader information from the electronic exchanges makes it more difficult for the CFTC to monitor speculative activity and to detect and prevent price manipulation. The absence of this information not only obscures the CFTC’s view of that portion of the energy commodity markets, but it also degrades the quality of information that is reported.

A trader may take a position on an unregulated electronic exchange or on a foreign exchange that is either in addition to or opposite from the positions the trader has taken on the NYMEX, and thereby avoid and distort the large trader reporting system.

Not only can the CFTC be misled by these trading practices, but these trading practices could render the CFTC weekly publication of energy market trading data, intended to be used by the public, as incomplete and misleading.”

Simply put, any one can now speculate and avoid being tagged with illegal price. The more speculative trading that occurs, the less “real” price discovery via true supply and demand become.

With that in mind, you can now see how the big banks have gained control and cornered the oil market.

Continued from the Report:

“…Over the past few years, large financial institutions, hedge funds, pension funds, and other investment funds have been pouring billions of dollars into the energy commodities markets…to try to take advantage of price changes or to hedge against them.

Because much of this additional investment has come from financial institutions and investment funds that do not use the commodity as part of their business, it is defined as ”speculation” by the Commodity Futures Trading Commission (CFTC).

…Reports indicate that, in the past couple of years, some speculators have made tens and perhaps hundreds of millions of dollars in profits trading in energy commodities.

This speculative trading has occurred both on the regulated New York Mercantile Exchange (NYMEX) and on the over-the-counter (OTC) markets.

The large purchases of crude oil futures contracts by speculators have, in effect, created an additional demand for oil, driving up the price of oil to be delivered in the future in the same manner that additional demand for the immediate delivery of a physical barrel of oil drives up the price on the spot market.

As far as the market is concerned, the demand for a barrel of oil that results from the purchase of a futures contract by a speculator is just as real as the demand for a barrel that results from the purchase of a futures contract by a refiner or other user of petroleum.

Although it is difficult to quantify the effect of speculation on prices, there is substantial evidence that the large amount of speculation in the current market has significantly increased prices.

Several analysts have estimated that speculative purchases of oil futures have added as much as $20-$25 per barrel to the current price of crude oil, thereby pushing up the price of oil from $50 to approximately $70 per barrel.”

The biggest banks in the world, such as Goldman Sachs, Morgan Stanley, Citigroup, JP Morgan, are now also the biggest energy traders; together, they not only participate in oil trades, but also fund numerous hedge funds that trade in oil.

Knowing how easy it is to force the price of oil upwards, the same strategies can be done in reverse to force the price of oil down.

All it takes is for some media-conjured “report” to tell us that Saudi Arabia is flooding the market with oil, OPEC is lowering prices, or that China is slowing, for oil to collapse.

Traders would then go short oil, kicking algo-traders into high gear, and immediately sending oil down further. The fact that oil consumption is actually growing really doesn’t matter anymore.

In reality, oil price isn’t dictated by supply and demand – or OPEC, or Russia, or China – it is dictated by the Western financial institutions that trade it.

“For years, I have been talking about how the banks have taken control of our civilization.

…With oil prices are falling, economies around the world are beginning to feel the pain causing a huge wave of panic throughout the financial industry. That’s because the last time oil dropped like this – more than US$40 in less than six months – was during the financial crisis of 2008.

…Let’s look at the energy market to gain a better perspective.

The energy sector represents around 17-18 percent of the high-yield bond market valued at around $2 trillion.

Over the last few years, energy producers have raised more than a whopping half a trillion dollars in new bonds and loans with next to zero borrowing costs – courtesy of the Fed.

This low-borrowing cost environment, along with deregulation, has been the goose that laid the golden egg for every single energy producer. Because of this easy money, however, energy producers have become more leveraged than ever; leveraging themselves at much higher oil prices.

But with oil suddenly dropping so sharply, many of these energy producers are now at serious risk of going under.

In a recent report by Goldman Sachs, nearly $1 trillion of investments in future oil projects are at risk.

…It’s no wonder the costs of borrowing for energy producers have skyrocketed over the last six months.

…many of the companies are already on the brink of default, and unable to make even the interest payments on their loans.

…If oil continues in this low price environment, many producers will have a hard time meeting their debt obligations – meaning many of them could default on their loans. This alone will cause a wave of financial and corporate destruction. Not to mention the loss of hundreds of thousands of jobs across North America.”

You may be thinking, “if oil’s fall is causing a wave of financial disaster, why would the banks push the price of oil down? Wouldn’t they also suffer from the loss?”

Great question. But the banks never lose. Continued from my letter:

“If you control the world’s reserve currency, but slowly losing that status as a result of devaluation and competition from other nations (see When Nations Unite Against the West: The BRICS Development Bank), what would you do to protect yourself?

You buy assets. Because real hard assets protect you from monetary inflation.

With the banks now holding record amounts of highly leveraged paper from the Fed, why would they not use that paper to buy hard assets?

Bankers may be greedy, but they’re not stupid.

The price of hard physical assets is the true representation of inflation.

Therefore, if you control these hard assets in large quantities, you could also control their price.

This, in turn, means you can maintain control of your currency against monetary inflation.

And that is exactly what the banks have done.

The True World Power

Last month, the U.S. Senate’s Permanent Subcommittee on Investigations published a 403-page report on how Wall Street’s biggest banks, such as Goldman Sachs, Morgan Stanley, and JP Morgan, have gained ownership of a massive amount of commodities, food, and energy resources.

The report stated that “the current level of bank involvement with critical raw materials, power generation, and the food supply appears to be unprecedented in U.S. history.”

For example:

“…Until recently, Morgan Stanley controlled over 55 million barrels of oil storage capacity, 100 oil tankers, and 6,000 miles of pipeline. JPMorgan built a copper inventory that peaked at $2.7 billion, and, at one point, included at least 213,000 metric tons of copper, comprising nearly 60% of the available physical copper on the world’s premier copper trading exchange, the LME.

In 2012, Goldman owned 1.5 million metric tons of aluminum worth $3 billion, about 25% of the entire U.S. annual consumption. Goldman also owned warehouses which, in 2014, controlled 85% of the LME aluminum storage business in the United States.” – Wall Street Bank Involvement with Physical Commodities, United States Senate Permanent Subcommittee on Investigations

From pipelines to power plants, from agriculture to jet fuel, these too-big-to-fail banks have amassed – and may have manipulated the prices – of some of the world’s most important resources.

The above examples clearly show just how much influence the Big Banks have over our commodities through a “wide range of risky physical commodity activities which included, at times, producing, transporting, storing, processing, supplying, or trading energy, industrial metals, or agricultural commodities.”

With practically an unlimited supply of cheap capital from the Federal Reserve, the Big Banks have turned into much more than lenders and facilitators. They have become direct commerce competitors with an unfair monetary advantage: free money from the Fed.

Of course, that’s not their only advantage.

According to the report, the Big Banks are engaging in risky activities (such as ownership in power plants and coal mining), mixing banking and commerce, affecting prices, and gaining significant trading advantages.

Just think about how easily it would be for JP Morgan to manipulate the price of copper when they – at one point – controlled 60% of the available physical copper on the world’s premier copper trading exchange, the LME.

How easy would it be for Goldman to control the price of aluminum when they owned warehouses – at one point – that controlled 85% of the LME aluminum storage business in the United States?

And if they could so easily control such vast quantities of hard assets, how easy would it be for them to profit from going either short or long on these commodities?

Always a Winner

But if, for some reason, the bankers’ bets didn’t work out, they still wouldn’t lose.

That’s because these banks are holders of trillions of dollars in FDIC insured deposits.

In other words, if any of the banks’ pipelines rupture, power plants explode, oil tankers spill, or coal mines collapse, taxpayers may once again be on the hook for yet another too-big-to-fail bailout.

If you think that there’s no way that the government or the Fed would allow this to happen again after 2008, think again.

Via the Guardian:

“In a small provision in the budget bill, Congress agreed to allow banks to house their trading of swaps and derivatives alongside customer deposits, which are insured by the federal government against losses.

The budget move repeals a portion of the Dodd-Frank financial reform act and, some say, lays the groundwork for future bailouts of banks who make irresponsibly risky trades.”

Recall from my past letters where I said that the Fed wants to engulf you in their dollars. If yet another bailout is required, then the Fed would once again be the lender of last resort, and Americans will pile on the debt it owes to the Fed.

It’s no wonder that in the report, it actually notes that the Fed was the facilitator of this sprawl by the banks:

“Without the complementary orders and letters issued by the Federal Reserve, many of those physical commodity activities would not otherwise have been permissible ‘financial’ activities under federal banking law. By issuing those complementary orders, the Federal Reserve directly facilitated the expansion of financial holding companies into new physical commodity activities.”

The Big Banks have risked tons of cash lending and facilitating in oil business. But in reality they haven’t risked anything. They get free money from the Fed, and since they aren’t supposed to be directly involved in natural resources, they obtain control in other ways.

Remember, the big banks – and ultimately the Fed who controls them – are the ones who truly control the world. Their monetary actions are the cause of many of the world’s issues and have been used for many years to maintain control of other nations and the world’s resources.

But they can’t simply go into a country, put troops on the ground and take over. No, that would be inhumane.

“Currency manipulation allows developed countries to print and lend to other developing countries at will.

A rich nation might go into a developing nation and lend them millions of dollars to build bridges, schools, housing, and expand their military efforts. The rich nation convinces the developing nation that by borrowing money, their nation will grow and prosper.

However, these deals are often negotiated at a very specific and hefty cost; the lending nation might demand resources or military and political access. Of course, developing nations often take the loans, but never really have the chance to pay it back.

When the developing nations realize they can’t pay back the loans, they’re at the mercy of the lending nations.

The trick here is that the lending nations can print as much money as they want, and in turn, control the resources of developing nations. In other words, the loans come at a hefty cost to the borrower, but at no cost to the lender.”

This brings us back to oil.

We know that oil’s crash has put a heavy burden on many debt facilities that are associated with oil. We also know that the big banks are all heavily leveraged within the sector.

If that is the case, why are the big banks so calm?

The answer is simple.

Asset-Backed Lending

Most of the loans associated with oil are done through asset-backed loans, or reserve-based financing.

It means that the loans are backed by the underlying asset itself: the oil reserves.

So if the loans go south, guess who ends up with the oil?

According to Reuters, JP Morgan is the number one U.S. bank by assets. And despite its energy exposure assumed at only 1.6 percent of total loans, the bank could own reserves of up to $750 million!

“If oil reaches $30 a barrel – and here we are – and stayed there for, call it, 18 months, you could expect to see (JPMorgan’s) reserve builds of up to $750 million.”

No wonder the banks aren’t worried about a oil financial contagion – especially not Jamie Dimon, JP Morgan’s Chairman, CEO and President:

“…Remember, these are asset-backed loans, so a bankruptcy doesn’t necessarily mean your loan is bad.” – Jamie Dimon

As oil collapses and defaults arise, the banks have not only traded dollars for assets on the cheap, but gained massive oil reserves for pennies on the dollar to back the underlying contracts of the oil that they so heavily trade.

The argument to this would be that many emerging markets have laws in place that prevent their national resources from being turned over to foreign entities in the case of corporate defaults.

Which, of course, the U.S. and its banks have already prepared for.

“…If the Fed raises interest rates, many emerging market economies will suffer the consequence of debt defaults. Which, historically means that asset fire sales – often commodity-based assets such as oil and gas – are next.

Historically, if you wanted to seize the assets of another country, you would have to go to war and fight for territory. But today, there are other less bloody ways to do that.

Take, for example, Petrobras – a semi-public Brazilian multinational energy corporation.

…Brazil is in one of the worst debt positions in the world with much of its debt denominated in US dollars.

Earlier this year (2015), Petrobras announced that it is attempting to sell $58 billion of assets – an unprecedented number in the oil industry.

Guess who will likely be leading the sale of Petrobras assets? Yup, American banks.

“…JPMorgan would be tasked with wooing the largest number of bidders possible for the assets and then structure the sales.”

As history has shown, emerging market fire sales due to debt defaults are often won by the US or its allies. Thus far, it appears the Petrobras fire sale may be headed that way.

‘Brazilian state-run oil company Petróleo Brasileiro SA said Tuesday (September 22, 2015) it is closing a deal to sell natural-gas distribution assets to a local subsidiary of Japan’s Mitsui & Co.’

The combination of monetary policy and commodities manipulation allows Western banks and allies to accumulate hard assets at the expense of emerging markets. And this has been exactly the plan since day one.

As the Fed hints of raising rates, financial risks among emerging markets will continue to build. This will trigger a reappraisal of sovereign and corporate risks leading to big swings in capital flows.”

Not only are many of the big banks’ practices protected by government and Fed policies, but they’re also protected by the underlying asset itself. If things go south, the bank could end up owning a lot of oil reserves.

No wonder they’re not worried.

And since the banks ultimately control the price of oil anyway, it could easily bring the price back up when they’re ready.

Controlling the price of oil gives U.S. and its banks many advantages.

For example, the U.S. could tell the Iranians, the Saudis, or other OPEC nations, whose economies heavily rely on oil, “Hey, if you want higher oil prices, we can make that happen. But first, you have to do this…”

You see how much control the U.S., and its big banks, actually have?

At least, for now anyway.

Don’t think for one second that nations around the world don’t understand this.

Just ask Venezuela, and many of the other countries that have succumbed to the power of the U.S. Many of these countries are now turning to China because they feel they have been screwed.

The World Shift

The diversification away from the U.S. dollar is the first step in the uprising against the U.S. by other nations.

As the power of the U.S. dollar diminishes, through international currency swaps and loans, other trading platforms that control the price of commodities (such as the new Shanghai Oil Exchange) will become more prominent in global trade; thus, bringing some price equilibrium back to the market.

And this is happening much faster than you expect.

Chinese President Xi Jinping returned home Sunday after wrapping up a historic trip to Saudi Arabia, Egypt, and Iran with a broad consensus and 52 cooperation agreements set to deepen Beijing’s constructive engagement with the struggling yet promising region.

During Xi’s trip, China upgraded its relationship with both Saudi Arabia and Iran to a comprehensive strategic partnership and vowed to work together with Egypt to add more values to their comprehensive strategic partnership.

Regional organizations, including the Organization of Islamic Cooperation (OIC), the Cooperation Council for the Arab States of the Gulf (GCC) and the Arab League (AL), also applauded Xi’s visit and voiced their readiness to cement mutual trust and broaden win-win cooperation with China.

AL Secretary General Nabil al-Arabi said China has always stood with the developing world, adding that the Arab world is willing to work closely with China in political, economic as well as other sectors for mutual benefit.

The Belt and Road Initiative, an ambitious vision Xi put forward in 2013 to boost inter-connectivity and common development along the ancient land and maritime Silk Roads, has gained more support and popularity during Xi’s trip.

…Xi and leaders of the three nations agreed to align their countries’ development blueprints and pursue mutually beneficial cooperation under the framework of the Belt and Road Initiative, which comprises the Silk Road Economic Belt and the 21st Century Maritime Silk Road.

The initiative, reiterated the Chinese president, is by no means China’s solo, but a symphony of all countries along the routes, including half of the OIC members.

During Xi’s stay in Saudi Arabia, China, and the GCC resumed their free trade talks and “substantively concluded in principle the negotiations on trade in goods.” A comprehensive deal will be made within this year.”

In other words, the big power players in the Middle East – who produce the majority of the world’s oil – are now moving closer to cooperation with China, and away from the U.S.

As this progresses, it means the role of the U.S. dollar, and its value in world trade, will diminish.

And the big banks, which hold trillions of dollars in U.S. assets, aren’t concerned.

China’s slowdown, cash-strapped emerging markets, the negative interest rate contagion – news from the world economy has been almost uniformly negative for much of the past twelve months. The bright spot amid the gloom has been the relatively upbeat US economy, the strength of which finally convinced the Fed to nudge up interest rates last December. At that time, based on the available data, we concurred that a slow liftoff was the right course of action. But a growing number of macroeconomic reports issued since call that decision into question. From productivity to durable goods orders to real GDP growth, indications are that the pace of recovery is waning. Not enough to raise fears of an imminent recession, but enough to stoke the flames of negative sentiment currently afflicting risk asset markets around the world.

Mary Mary Quite Contrary, How Does Your Economy Grow?

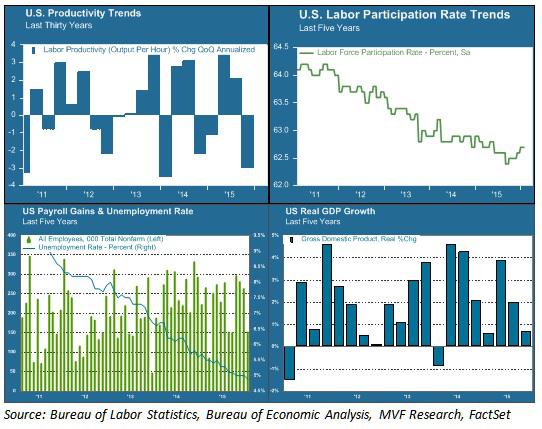

Jobs Friday may be the headline event for macro data nerds, but in our opinion, Productivity Wednesday was the more significant event of the week. The Bureau of Labor Statistics release this past midweek showed that fourth quarter 2015 productivity declined by three percent (annualized) from the previous quarter. Now, productivity can be sporadic from quarter to quarter, but this week’s release is part of a larger trend of lackluster efficiency gains.

As measured by real GDP, an economy can only grow in three ways: population growth, increased labor force participation, or increased output per hour of labor – i.e. productivity. Unfortunately, none of these are trending positive. The chart below offers a snapshot of current labor, productivity and growth trends.

Labor force participation (upper right area of chart) has been in steep decline for the past five years – an outcome of both the jobs lost from the 2007-09 recession and the retirement of baby boomers from the workplace. This decline has helped keep the headline unemployment rate low (blue line in the bottom left chart) and also explains in part the anemic growth in hourly wages over this period. This trend is unlikely to reverse any time soon. If real GDP growth (bottom right chart) is to return to its pre-recession normal trend line, it will have to come from productivity gains. That is why the current trend in productivity (upper left chart) is of such concern.

Of Smartphones and Sewage

The last sustained productivity surge we experienced was in the late 1990s. It is attributed largely to the fruits of the Information Age – the period when the innovations in computing and automation of the previous decades translated into increased efficiencies in the workplace. From 1995 to 2000, quarterly productivity gains averaged 2.6 percent on an annual basis. The pace slackened in the first decade of the current century. In the first five years of this decade – from 2010 to the present – average quarterly productivity growth amounted to just 0.6 percent – more than three times slower than the gains of the late 1990s.

Is that all we can expect from the Smartphone Age? Or are we simply in the middle of an innovation gap – a period in between technological breakthroughs and the translation of those breakthroughs to actual results? It is possible that a new growth age is just around the corner, powered by artificial intelligence, virtual reality and the Internet of Things, among other inventions. It is also possible that the innovations of our day simply don’t pack the same punch as those of other ages. Economist Robert Gordon makes a version of this argument in his recent book, The Rise and Fall of American Growth. Gordon points to the extraordinary period of growth our country experienced from 1870 to 1970 – growth delivered largely thanks to the inventions of electricity and the internal combustion engine – and argues that this was a one-off anomaly that we should not expect to continue indefinitely. What would you rather live without – your Twitter feed and Uber app, or indoor plumbing?

We don’t necessarily agree with Gordon’s conclusion that nothing will ever again rival electricity and motorized transport as an economic growth driver. But we do believe that the growth equation is currently stuck, and the headline data we have seen so far this year do nothing to indicate its becoming unstuck. Long-term growth is not something that drives day-to-day fluctuations in asset prices. But its absence is a problem that is increasingly part of the conversation about where markets go from here. Stay tuned for more Productivity Wednesdays.

No one has called long-duration treasury yields better than Lacy Hunt at Hoisington Management. He says they are going lower. If the US is in or headed for recession then I believe he is correct.

“Debt only works if it generates an income to repay principle and interest.”

Research indicates that when public and private debt rises above 250% of GDP it has very serious effects on economic growth. There is no bit of evidence that indicates an indebtedness problem can be solved by taking on further debt.

One of the objectives of QE was to boost the stock market, on theory that an improved stock market will increase wealth and ultimately consumer spending. The other mechanism was that somehow by buying Government securities the Fed was in a position to cause the stock market to rise. But when the Fed buys government securities the process ends there. They can buy government securities and cause the banks to surrender one type of government asset for another government asset. There was no mechanism to explain why QE should boost the stock market, yet we saw that it did. The Fed gave a signal to decision makers that they were going to protect financial assets, in other words they incentivized decision makers to view financial assets as more valuable than real assets. So effectively these decision makers transferred funds that would have gone into the real economy into the financial economy, as a result the rate of growth was considerably smaller than expected.

“In essence the way in which it worked was by signaling that real assets were inferior to financial assets. The Fed, by going into an untested program of QE effectively ended up making things worse off.”

Flattening of the Yield Curve

“Monetary policies currently are asymmetric. If the Fed tried to do another round of QE and/or negative interest rates, the evidence is overwhelming that will not make things better. However if the Fed wishes to constrain economic activity, to tighten monetary conditions as they did in December; those mechanisms are still in place.”

They are more effective because the domestic and global economy is more heavily indebted than normal. The fact we are carrying abnormally high debt levels is the reason why small increases in interest rate channels through the economy more quickly.

If the Fed wishes to tighten which they did in December then sticking to the old traditional and tested methods is best. They contracted the monetary base which ultimately puts downward pressure on money and credit growth. As the Fed was telegraphing that they were going to raise the federal funds rate it had the effect of raising the intermediate yield but not the long term yields which caused the yield curve to flatten. It is a signal from the market place that the market believes the outlook is lower growth and lower inflation. When the Fed tightens it has a quick impact and when the Fed eases it has a negative impact.

The critical factor for the long bond is the inflationary environment. Last year was a disappointing year for the economy, moreover the economy ended on a very low note. There are outward manifestations of the weakening in economy activity. One impartial measure is what happened to commodity prices, which are of course influenced by supply and demand factors. But when there are broad declines in all the major indices it is an indication of a lack of demand. The Fed tightened monetary conditions into a weakening domestic global economy, in other words they hit it when it was already receding, which tends to further weaken the almost non-existent inflationary forces and for an investor increases the value.

Failure of Quantitative Easing

“If you do not have pricing power, it is an indication of rough times which is exactly what we have.”

The fact that the Fed made an ill-conceived move in December should not be surprising to economists. A detailed study was done of the Fed’s 4 yearly forecasts which they have been making since 2007. They have missed every single year.

That was another in a series of excellent interviews by Gordon Long. There’s much more in the interview. Give it a play.

Finally, lest anyone scream to high heavens, Lacy is obviously referring to price inflation, not monetary inflation which has been rampent.

From my standpoint, consumer price deflation may be again at hand. Asset deflation in equities, and junk bonds is a near given.

The Fed did not save the world as Ben Bernanke proclaimed. Instead, the Fed fostered a series of asset bubble boom-bust cycles with increasing amplitude over time.

The bottom is a long, long ways down in terms of time, or price, or both.

Earlier this week, before first JPM and then Wells Fargo revealed that not all is well when it comes to bank energy loan exposure, a small Tulsa-based lender, BOK Financial, said that its fourth-quarter earnings would miss analysts’ expectationsbecause its loan-loss provisions would be higher than expected as a result of a single unidentified energy-industry borrower. This is what the bank said:

“A single borrower reported steeper than expected production declines and higher lease operating expenses, leading to an impairment on the loan. In addition, as we noted at the start of the commodities downturn in late 2014, we expected credit migration in the energy portfolio throughout the cycle and an increased risk of loss if commodity prices did not recover to a normalized level within one year. As we are now into the second year of the downturn, during the fourth quarter we continued to see credit grade migration and increased impairment in our energy portfolio. The combination of factors necessitated a higher level of provision expense.”

Another bank, this time the far larger Regions Financial, said its fourth-quarter charge-offs jumped $18 million from the prior quarter to $78 million, largely because of problems with a single unspecified energy borrower. More than one-quarter of Regions’ energy loans were classified as “criticized” at the end of the fourth quarter.