The stock dropped 17 percent and is now trading at about half its IPO price.

In itssecond earnings reportas a public company,Snapdisappointed Wall Street with its user growth numbers for the second consecutive time and fell short on earnings.

The stock dropped about 17 percent after hours. It’s now off about 33 percent from its IPO price.

Blue Apron and Snap have a lot in common. They’re consumer focused. They have devoted followers. They’re losing money hand over fist.

And both were targeted directly and aggressively by two of tech’s biggest companies.

Between the time Blue Apron filed for its intial public offering, on June 1, and when it went public, on June 28, Amazon announced that it was buying Whole Foods. The speculation thatAmazonwould use the purchase to improve its home delivery service sent demand for Blue Apron’s IPO down, and the company slashed its IPO range from $15-$17 down to $10-$11.

Then, reports emerged that Amazon had already launched a meal kit, which was on sale in Seattle.

In the case of Snap, it was Facebook. Mark Zuckerberg and company had been fighting to blunt Snap’s growth ever since its co-founder, Evan Spiegel, rejected his buyout offer in 2013. It began to see progress with the launch of Instagram Stories in August 2016, which duplicated Snapchat’s own Stories feature. Over the next year, it gradually copied nearly every major Snapchat feature in its own products.

Less than a year after launch, Instagram Stories has 250 million daily users and is growing at a rate of around 50 million every three months. Snap has 173 million and grew only 7 million during the quarter.

The experiences of these companies are discouraging for start-up investors and founders who dream of someday creating an Amazon or Facebook of their own.

The five big tech companies — Alphabet (Google), Apple, Amazon, Facebook, and Microsoft — have attained unprecedented wealth and power, with trillions of dollars in combined market value and tens of billions of dollars in free cash flow.

They also need to satisfy Wall Street’s appetite for growth, which means they have to get new customers or earn more money from existing customers, quarter after quarter, year after year. One way to do that is to expand into new markets.

They’ll gladly outspend their smaller competitors on product development and hiring while undercutting them on price.

That doesn’t mean curtains for Blue Apron or Snap. Both companies could come up with a leapfrog innovation that catapults them (for a while). Young nimble companies overtake older and slower companies all the time — that’s how the Big Five started. Microsoft disruptedIBM. Google and Apple disrupted Microsoft. And so on.

But companies and tech investors need to be wise about the risks of betting on upstarts that are going up against these giants.

If you hope to make money through online advertising, you’ll be challenging Google and Facebook. If you’re doing anything in e-commerce, logistics or delivery, you’ll run into Amazon. In cloud computing, get ready to see Amazon,Microsoftand Google. If you’re building hardware, Apple likely stands in the way.

It might be better to focus on the niches that the Big Five don’t yet dominate. Their health-care efforts are still in early stages, and none is playing heavily in financial tech, drones or robotics. Microsoft’s power in enterprise software is blunted to some degree by other old giants like IBM,OracleandSAP, plus newer players likeSalesforce.

It’s always been hard to build a successful start-up. With the increasing dominance of the Big Five, it’s harder than ever.

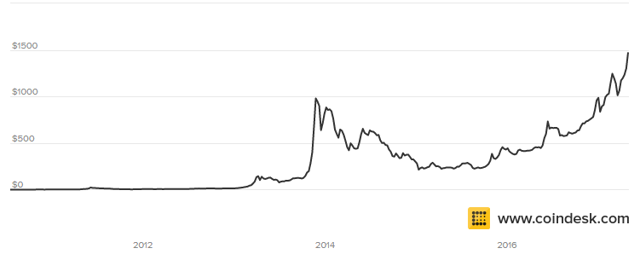

Bitcoin is now up almost 35% since the August 1st fork, and up over 90% from the mid-July fork-fears panic low. Buying was heavy in the overnight Asian session but surged once again this morning, seemingly after US CPI data disappointed, lifting the price to a new record high of $3547.

As we noted earlier,“The real demand for bitcoin will not be known until a global financial crisis guts confidence in central banks and politicized capital controls.”

This is Bitcoin’s best week since pre-Brexit anxiety sent the virtual currency surging in June 2016…

Coinbase CEO Brian Armstrong noted: “Digital currencies are having their ‘Netscape’ moment…The pace of innovation has been accelerating and we are now seeing exciting projects and companies being built on top of digital currencies.”

As CoinTelegraph also notes, recent tension between the US and North Korea has played its part on the global market, rattling some of the major asset classes. However, not being pegged, or controlled by any centralized force, Bitcoin was totally unaffected by the news.

Cryptocurrencies are famous for their volatility, but the non-correlation between the global market slipping and cryptocurrencies mostly staying up shows that these decentralized forms of currency won’t be affected like traditional assets.

Concerns over the future of Social Security play a starring role in American seniors’ overall retirement uncertainty — and that’s before considering how much of the benefit might eventually need to go toward unexpected medical expenses.

After factoring in supplemental insurance premiums and other uninsured health costs, the average retiree only takes home 75% of his or her Social Security benefits, according to a new study from researchers at Tufts University and Boston College.

“A substantial share of other households have even less of their benefits left over,” researchers Melissa McInerney of Tufts and Matthew S. Rutledge and Sara Ellen King of BC wrote.

In fact, for three percent of retirees, out-of-pocket health expenses actually exceed their Social Security Old Age and Survivors Insurance (OASI) benefits, the team concludes.

These findings are part of an overall trend: Despite positive steps such as the introduction of Medicare Part D coverage for prescription drugs in 2006, seniors have increasingly paid more for health expenses directly from their pockets.

“Until a slowdown during this decade, out-of-pocket costs for Medicare beneficiaries rose dramatically — costs increased by 44% between 2000 and 2010 — and they are expected to continue to rise faster than overall inflation,” the researchers wrote.

To perform their study, which was introduced at the annual Joint Meeting of the Retirement Research Consortium in Washington, D.C. last week, the team analyzed individual data points for Social Security recipients aged 65 and older between 2002 and 2014. They found a wide range in medical spending among that cohort: For instance, while the median retiree spent $2,400 in 2014, the total group averaged $3,100 per person, with retirees in the 75th percentile logging $4,400.

The researchers also warn that they only analyzed medical expenses, citing a 2017 paper that concluded that housing costs, taxes, and “non-housing debt” eat up about 30% of a retiree’s income.

“Although out-of-pocket medical spending has declined somewhat since the instruction of Part D … these findings suggest that Social Security beneficiaries’ lifestyles remain vulnerable to a likely revival in medical spending growth,” the team concludes.

Read McInerney, Rutledge, and King’s full findingshere.

Having‘nailed’ the price action recently in Bitcoin(calling the recent pull back, extension beyond $3,000, with a target of $3,915), Goldman notes that it’s getting harder for institutional investors to ignore the rise of cryptocurrencies.

Last month Goldman’s chief technician, Sheba Jafari, issued their forecast of where bitcoin is headed next. Recall, that as wefirst reported three weeks ago,Jafari said that “due to popular demand, it’s worth taking a quick look at Bitcoin here” and warned that “the market has come close (enough?) to reaching its extended (2.618) target for a 3rd of V-waves from the inception low at 3,134.” She concluded that she was “wary of a near-term top ahead of 3,134” and urged clients to “consider re-establishing bullish exposure between 2,330 and no lower than 1,915.”

She was right: on the very day the note came out, both bitcoin and ethereum hit their all time highs and shortly after suffered their biggest drop in over two years.

So what does Jafari thinks will happen next? According to the Goldman technician, Bitcoin is now “in wave IV of a sequence that started at the late-’10/early-’11 lows. Wave III came close enough to reaching its 2.618 extended target at 3,135. Wave IV has already retraced between 23.6% and 38.2% of the move since Jan. ‘15 to 2,330/ 1,915.”

What does this mean for the uninitiated? In short, while bitcoin remains in Wave IV, it could go up… or down. She explains:

It’s worth keeping in mind that fourth waves tend to be messy/complex. This means that it could remain sideways/overlapping for a little while longer. At this point, it’s important to look for either an ABC pattern or a more triangular ABCDE. The former would target somewhere close to 1,856; providing a much cleaner setup from which to consider getting back into the uptrend. The latter would hold within a 2,076/3,000 range for an extended period of time.

However, at that point the next major breakout higher would take place, one which would take bitcoin as high as $3,915.

Either way, eventually expecting one more leg higher; a 5th wave. From current levels, [Bitcoin] has a minimum target that goes out to 3,212 (if equal to the length of wave I). There’s potential to extend as far as 3,915 (if 1.618 times the length of wave I). It just might take time to get there.

Goldman’s analyst concludes with the following summary: “[Bitcoin] could consolidate sideways for a while longer. Shouldn’t go much further than 1,857. Eventually targetingat least 3,212.“

And now, Goldman offers an FAQ for the institutional investor…

The debate has shifted from the legitimacy of the ‘fiat of the internet’ to how fast new entrants are raising funds. The hype cycle is in full effect with Bitcoin, the first, largest and most widely recognized cryptocurrency up almost 200% YTD (v 11% for the S&P 500) and a host of other emerging ‘alt coins’ growing in scope and presence (witness the growth of Ethereum).

Whether or not you believe in the merit of investing in cryptocurrencies (you know who you are) real dollars are at work here and warrant watching especially in light of the growing world of initial coin offerings (ICOs) and fundraising that now exceeds Internet Angel and Seed investing.

FAQs:

1. Two Sides To The Coin: Is Cryptocurrency a “Currency” or “Commodity”?

Answer: It depends who you ask. The complexity exists because coins have attributes of a currency (e.g. presented and trusted by some medium of exchange) and commodity (e.g. limited resource). The classification of cryptocurrencies varies by country, government and even application. In the U.S., the IRS has ruled that virtual currency does not have legal tender status in any jurisdiction. For tax purposes, the IRS treats virtual currency as property.

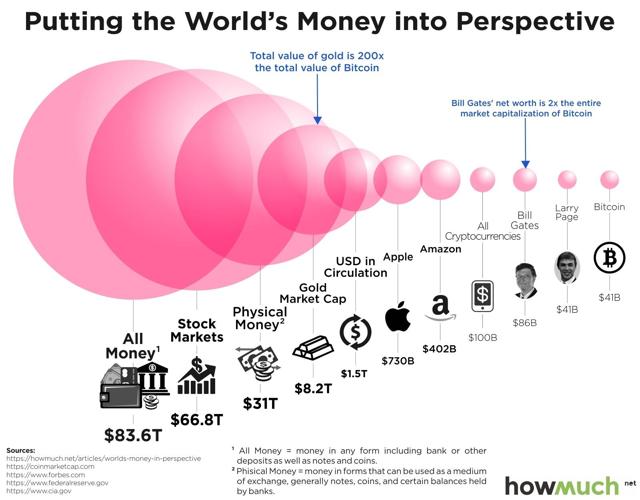

2. How Big Is The Cryptocurrency Market?

Answer: Nearly $120 billion. Bitcoin remains the largest and accounts for nearly 50% of the total market cap (Exhibit 5).

There are currently over 800 cryptocurrencies out there, though just 9 have a market cap in excess of $1 billion.

While its growth has been impressive, the aggregate market cap of cryptocurrencies equates to less than 2% of the value of all the mined gold in the world.

3. What Is Ethereum?

Answer: A Platform 1st, a Cryptocurrency 2nd. Ethereum differs primarily from Bitcoin in the latter is set up to be an alternative to ‘real money’ while the former is more of a platform set up to run any decentralized application and automatically execute “smart contracts” when certain conditions are met. Ethereum offers a digital currency like Bitcoin – called Ether – but this is just one component of its smart contract execution and primarily used to facilitate and reward using the network. However, the rise of Ethereum has not come without setbacks, including the ~$60 million hack of “The DAO”, a venture capital like organization with the mission of “investing” in Ethereum-related start-ups and projects (and is no longer operational today).

4. How Does One Trade Cryptocurrencies in the United States?

Answer: Digital Exchanges, Block Trades and (soon to be) Options. Individual investors can trade virtual coins on various online exchanges. Institutional traders have largely stayed out of the cryptocurrency market due to its relatively small size, structure of mandates and volatility, but block trading exists to facilitate the execution of larger orders. In addition, Bitcoin options exist and are traded on offshore exchanges. Futures and options may also be coming to the US soon. On August 2, 2017, the CBOE entered an agreement with Gemini Trust Co to allow cash-settled Bitcoin futures on CBOE Futures Exchange in 4Q-17 or early 2018.

5. What is an Initial Coin Offering (ICO)?

Answer: Fundraiser through token sales. The amount of money funding ICOs has grown exponentially and the speed at which money is raised via a white paper and internet browser has sounded the alarm bells from parties including the SEC and the People’s Bank of China. According to Coin Schedule, ICOs have raised $1.25 billion this year, outpacing global Angel & Seed stage Internet VC funding in recent months.

The Tezos blockchain raised a record breaking $232 million worth of Bitcoin and Ether through an ICO completed last month. The next closest? Bancor’s ICO which raised $150 million in mid-June. And the speed of ICOs is an added benefit: Gnosis raised more than $12 million in under 15 minutes.

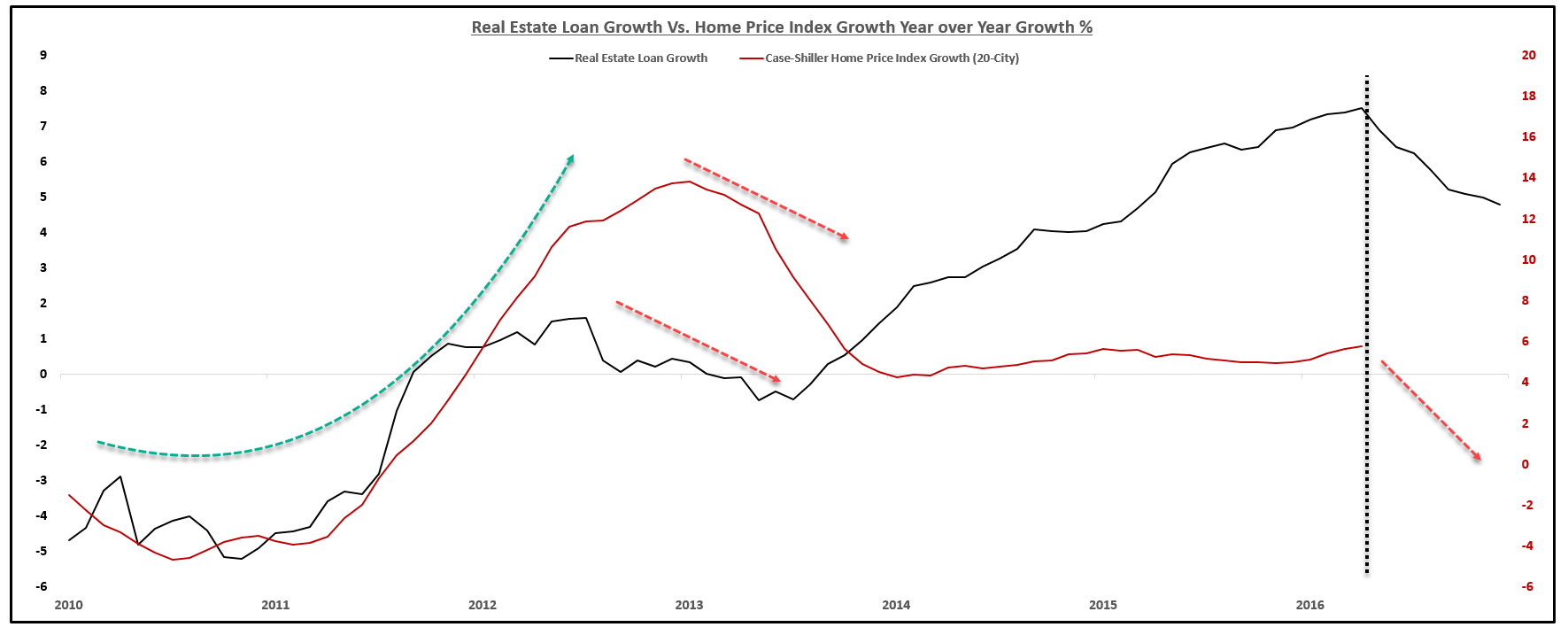

Sin City’s projected 5,000 new apartment units for this year makes no noise nationally in the latest real estate craze. “In 2017, the ongoing apartment building-boom in the US will set a new record: 346,000 new rental apartments in buildings with 50+ units are expected to hit the market,” writes Wolf Richter onWolf Street. That is three times the number of units that came on line in 2011.

Richter continues, “Deliveries in 2017 will be 21% above the prior record set in 2016, based on data going back to 1997, by Yardi Matrix, viaRent Café. And even 2015 had set a record. Between 1997 and 2006, so pre-Financial-Crisis, annual completions averaged 212,740 units; 2017 will be 63% higher!”

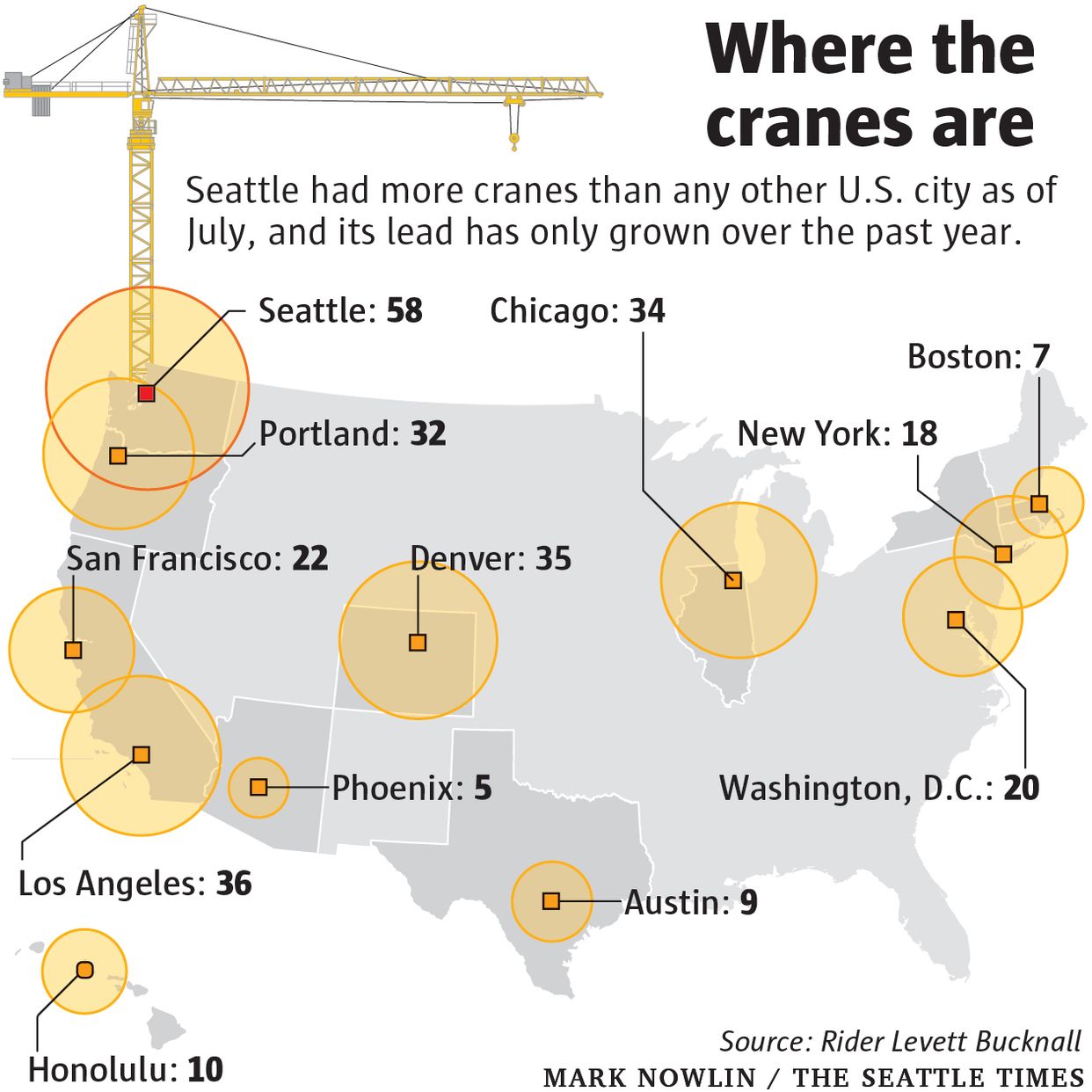

I’ve written before about the high-rise crane craze in Seattle, but that’s nothing compared to New York and Dallas, that are adding 27,000 and 25,000 units, respectively. Chicago is adding 7,800 units despite a shrinking population and rents decreasing 19 percent.

Not surprisingly, Fannie Mae and Freddie Mac are financing this rental housing boom. Iwrote recently, the GSEs made 53% of all apartment loans in 2016, down from their combined 68% market share in 2012. “So, their conservator, The Federal Housing Finance Agency (FHFA), recently eased the GSE’s lending caps so they can crank out even more loans.”

Mary Salmonsen writes formultifamilyexecutive.com, “Currently, Fannie and Freddie are particularly dominant in garden apartments [and] in student housing, with 62% and 61% shares, respectively. The two remain the largest mid-/high-rise lenders but hold only 35% of the market.”

Mr. Richter warns us, “Government Sponsored Enterprises such as Fannie Mae guarantee commercial mortgages on apartment buildings and package them in Commercial Mortgage-Backed Securities. So taxpayers are on the hook. Banks are on the hook too.”

But, for the moment, it’s build them and they will come; first renters, then complex buyers. Wall Street giant “The Blackstone Group acquired three Las Vegas Valley apartment complexes for $170 million, property records show,” writes Eli Segall for theLas Vegas Review Journal. “Overall, it bought 972 units for an average of $174,900 each.”

Sales like this has developers going as fast as they can. I heard an apartment developer say Vegas has at least four more good years left in this cycle and is scrambling for new sites. In the land of Starbucks, Microsoft and Amazon, it’s thought the boom will never end. Richter writes, “the new supply of apartment units hitting the market in 2018 and 2019 will even be larger. In Seattle, for example, there are 67,507 new apartment units in the pipeline.”

However, while no one was paying attention, “the prices of apartment buildings nationally, after seven dizzying boom years, peaked last summer and have declined 3% since,” Richter writes. “Transaction volume of apartment buildings has plunged. And asking rents, the crux because they pay for the whole construct, have now flattened.”

As usual, cheap money entices developers to over do it, and the fall will be just as painful.

It’s been about a decade since the term “mortgage arbitrage” made headlines. It’s back.

In the clearest sign yet of just how late far the investing cycle the developed world finds itself,the FT writes that wealthy British homeowners are again borrowing against their property to invest in bonds, equities, alternative investments or commercial property as the low cost of debt creates opportunities for “mortgage arbitrage”. And while taking out a mortgage to invest in “safer” arbs like corporate bonds, commercial real estate or private equity would be at least understandable, if not excusable, in the current low-yield regime, some more extreme “investment” decisions suggest that the madness and euphoria that marked the peak of the last asset bubble is back: because while growing numbers are prepared to risk using their primary residence as collateral, some are ready to gamble on extremely volatile assets like bitcoin, wine and cars.

One broker said a mortgage-free homeowner with a house valued at £10m had taken out a fixed-rate loan of just under £2m to buy bitcoin, the crypto currency that has seen huge volatility in recent months. Others have invested in classic cars or fine wine. One former banker took out a £500,000 mortgage, not for investment purposes, but to provide a fund for routine spending and other eventualities.

To be sure, while these are extreme – and for now rare – examples of investor euphoria, even the more mundane “mortgage arbitrageurs” are willing to take major gambles: “Interest rates of less than 2 per cent on two- and five-year fixed-rate home loans are tempting high-income, mortgage-free homeowners to raise money against their property in the hope they can profit from higher rates of return elsewhere.”

Simon Gammon, director at mortgage broker Knight Frank Finance, said the arbitrage had emerged as a trend among financially sophisticated clients as mortgage rates fell.

“We’re a specialist lender at the top end but we’re seeing up to a dozen of these deals a month,” he said. “This is something that has come about because of the current environment of low rates.”

How prevalent is this behavior which peaked during the last housing/credit bubble?

Mark Pattanshetti, a mortgage manager at broker Largemortgageloans.com, said the number of borrowers taking out loans to fund investments had risen by about 50% since 2009. “Borrowers have realized the cost of debt is cheap and it isn’t going to get much cheaper,” he said. Unfortunately, what borrowers are forgetting is that home prices can drop as mortgage rates rise, while risk assets – impossible as it may sound – can correct sharply, hitting borrowers with the double whammy of rising LTVs as inbound margin calls force them to liquidate into a sliding market.

Ironically, anecdotal evidence suggests that this troubling behavior has been prompted be declining UK home prices – until recently one of the best performing British assets. This has been the result of Brexit-related concerns, a decline in Chinese and other foreign investors rushing after UK real estate, as well as concerns that the BOE will soon raise rates, resulting in increasingly more “for sale” signs.

As the FT notes, “for debt-free homeowners, remortgaging during the years of booming house prices was often a means of raising cash to carry out home improvements or expand a buy-to-let portfolio. But slowing house price growth and a regulatory and tax crackdown on landlords have made these options less attractive.

Hugh Wade-Jones, group managing director of mortgage broker Enness, said: “It’s accepted that property is no longer going to be the all-conquering investment, doubling every 10 years, so people are looking elsewhere for returns.”

In addition to bitcoin, cars and wines, borrowers with housing equity are putting money into everything from bonds and private equity and commercial property, brokers told the FT. David Adams, managing director of John Taylor, a Mayfair-based estate agent, said investors were borrowing against London residential properties to fund investment in commercial and mixed use developments from Southampton to Birmingham at returns of 6 to 7 per cent.

“Wealthy investors are no longer chasing capital gain. There is a switch to yield,” Adams said.

According to Knight Frank’s Gammon, the practice typically appealed to those with investment experience. “People who have not needed to borrow have looked at the rates available — and we’ve now got five-year fixed rates from 1.65 per cent — and said if I can’t make 1.65 per cent or more from my money, then I don’t know what I’m doing.”

Unfortunately, should home prices in the near future tumble while risk assets slide, crushing the “experienced” investors, that’s exactly what one can conclude.

Making it easier for the “smart investors” to bury themselves with margin calls, there are no regulations prohibiting this kind of behavior:

There is nothing in mortgage regulation to prevent someone raising a loan on a mortgage-free property for personal investments, as long as the lender assesses that the loan is affordable and not being used, for instance, to prop up a business generating income for its repayment.

Lenders, however, may choose to apply criteria that restrict the use of capital raised through a mortgage, although private banks are typically more relaxed about non-property investments than high street banks. For bigger mortgages, lenders will also moderate risk by insisting that the size of the loan does not exceed 60 per cent of the property’s value.

Naturally, it doesn’t take a big drop in the value of the property coupled with a slide in the “alternative investment” to wipe out the LTV buffer, pushing the value of the loan above the underlying collateral. That said, “the Financial Conduct Authority, which regulates mortgage lenders, declined to comment on individuals borrowing against their house for personal investments.”

In a tangent, the FT then focuses on the tax considerations of this risky behavior.

Unlike gains on a principal private residence, any gains on investments would be subject to capital gains tax (CGT). A wealthy homeowner may therefore seek to transfer borrowed funds to a spouse who has not used his or her annual CGT allowance. If the investment is designed to provide a stream of income, there could be a case for a transfer to a spouse who pays the basic rate of income tax, advisers said.

Nimesh Shah, a tax adviser at accountants Blick Rothenberg, said that if a homeowner took out a loan to invest in commercial property — and this was specified as the purpose of the loan — residential mortgage interest could potentially be offset against the commercial rental income.

Of course, the above assumes capital appreciation and therefore, capital gains. For now nobody is worrying on the more unpleasant outcome, one where there are no gains to book taxes again. Then again, in a wholesale wipeout at least the “smart money” will have years and years of NOLs carryforward losses to offset any future income taxes. Just like Donald Trump.

(CNBC) Ride-hailing apps such as Uber and Lyft have been so disruptive to New York City’s taxi industry, they are causing lenders to fail.

Three New York-based credit unions that specialized in loaning money against taxi cab medallions, the hard-to-get licenses that allow the city’s traditional cab fleet to operate, have been placed into conservatorship as the value of those medallions has plummeted.

Just three years ago, cab owners and investors were paying as much as $1.3 million for a medallion. Now they are worth less than half that, and some medallion owners owe more on their loans than the medallions are worth.

“You’ve got borrowers who are under water. This is just like the subprime loan crisis,” said Keith Leggett, a credit union analyst and former senior economist at the American Bankers Association.

LOMTO Federal Credit Union, which was founded by taxi drivers in 1936 for mutual assistance, was placed into conservatorship by the National Credit Union Administration on June 26 “because of unsafe and unsound practices.”

New York City has the nation’s largest taxi industry, with more than 13,000 medallions.

Marcelino Hervias bought his medallion in 1990 for about $120,000 and thought its value would hit $2 million by the time he was ready to retire.

Instead, the 58-year-old said he owes $541,000 and is driving 12 to 16 hours a day to make ends meet.

“I celebrate my kids’ birthdays over the phone. Why?” Hervias said.

While some medallions are held by large owners with fleets, owning a single medallion was long seen as a ticket to the middle class for immigrants like Hervias, who is from Peru.

Many of them now owe more on their medallion loans than they originally paid for the medallions because they used their equity in the medallion for a home, a child’s education or other expenses.

Hervias said he borrowed against his medallion to pay for medical care for his mother, a new car and a visit to his homeland.

“Every time we want to go on vacation or do something, where do we go? To the equity of the medallion,” he said.

Other medallion owners tell similar stories.

Constant Granvil bought his medallion for $102,000 in 1987 and said he now owes more than $300,000 to his lender. He could have sold the medallion for two or three times that a few years ago, “but I said no, I’m not going to sell it,” said Granvil, who is 76. “And then I got caught.”

The value of Granvil’s medallion is hard to pinpoint because 2017 sale prices have varied from the $200,000s to the $500,000s depending on whether lenders are willing to finance the purchase.

Meanwhile, Granvil, who no longer drives because of poor health and uses a broker to hire a driver, said he is facing threats from the lender, Melrose Credit Union, to foreclose on not just his medallion, but also his house.

“How am I going to live?” he said. “And now Melrose wants to take my house?”

The New York State Department of Financial Services took possession of Melrose Credit Union in February and appointed the NCUA as conservator.

Critics say the federal agency is playing hardball with medallion owners like Granvil, who have been making their payments, by demanding that they pay off their loans in full or face foreclosure.

“They’re approaching it with this cookie-cutter idea,” said David Beier, head of the Committee for Taxi Safety, an association of taxi leasing agents. “They want you to mortgage your house to them as collateral. It’s forcing borrowers into bankruptcy.”

John Fairbanks, a spokesman for the NCUA, said that the agency has hired a management team to run Melrose and that it would be inappropriate to comment on the management team’s actions.

Supporters of the yellow cab industry have sued and pushed for city legislation to try to level the playing field between taxis and ride-hailing apps, which they say enjoy advantages like not paying a public transportation improvement surcharge that’s levied on yellow cabs and not having to outfit a percentage of cars with disabled-access features.

City Council member Ydanis Rodriguez, who chairs the council’s transportation committee, called this week for a panel to investigate the fall in medallion values.

According to a Morgan Stanley report, there were 11.1 million yellow cab trips in the city in April 2016, compared with 4.7 million Uber trips and 750,000 Lyft trips. The 11.1 million taxi rides were 9 percent fewer than the April 2015 number.

Some observers believe that the yellow cab’s market share will continue to shrink and that the value of a medallion won’t recover.

“This is a commodity that has been fundamentally disrupted,” said Leggett, who has written about medallion loans in his online newsletter Credit Union Watch. “I don’t see the value of the medallions getting close to what they were.”

Equity bears hunting for excess in the stock market might be better off worrying about bond prices, Alan Greenspan says. That’s where the actual bubble is, and when it pops, it’ll be bad for everyone.

“By any measure, real long-term interest rates are much too low and therefore unsustainable,” the former Federal Reserve chairman said in an interview. “When they move higher they are likely to move reasonably fast. We are experiencing a bubble, not in stock prices but in bond prices. This is not discounted in the marketplace.”

While the consensus of Wall Street forecasters is still for low rates to persist, Greenspan isn’t alone in warning they will break higher quickly as the era of global central-bank monetary accommodation ends. Deutsche Bank AG’s Binky Chadha says real Treasury yields sit far below where actual growth levels suggest they should be. Tom Porcelli, chief U.S. economist at RBC Capital Markets, says it’s only a matter of time before inflationary pressures hit the bond market.

“The real problem is that when the bond-market bubble collapses, long-term interest rates will rise,” Greenspan said. “We are moving into a different phase of the economy — to a stagflation not seen since the 1970s. That is not good for asset prices.”

Stocks, in particular, will suffer with bonds, as surging real interest rates will challenge one of the few remaining valuation cases that looks more gently upon U.S. equity prices, Greenspan argues. While hardly universally accepted,the theory underpinning his view, known as the Fed Model, holds that as long as bonds are rallying faster than stocks, investors are justified in sticking with the less-inflated asset.

Right now, the model shows U.S. stocks at one of the most compelling levels ever relative to bonds. Using Greenspan’s reference of an inflation-adjusted measure of bond yields, the gap between the S&P 500’s earnings yield of 4.7 percent and the 10-year yield of 0.47 percent is 21 percent higher than the 20-year average. That justifies records in major equity benchmarks and P/E ratios near the highest since the financial crisis.

If rates start rising quickly, investors would be advised to abandon stocks apace, Greenspan’s argument holds. Goldman Sachs Group Inc. Chief Economist David Kostin names the threat of rising inflation asone reasonhe isn’t joining Wall Street bulls in uppingyear-end estimatesfor the S&P 500.

While persistently low inflation would imply a fair value of 2,650 on the benchmark gauge, the more likely case is a narrowing of the gap between earnings and bond yields, Kostin says. He is sticking to his estimate that the index will finish the year at 2,400, implying a drop of about 3 percent from current levels.

That’s no slam dunk, as stocks have provenresilient to bond routsso far in the eight-year bull market. While the 10-year Treasury yield has peaked above 3 percent just once in the past six years, sudden spikes in yields in 2013 and after the 2016 election didn’t slow stocks from their grind higher.

Those shocks to the bond market proved short-lived, though, as tepid U.S. growth combined with low inflation to keep real and nominal long-term yields historically low.

That era could end soon, with the Fed widely expected to announce plans for unwinding its $4.5 trillion balance sheet and central banks around the world talking about scaling back stimulus.

“The biggest mispricing in our view across asset classes is government bonds,’’ Deutsche Bank’s Chadha said in an interview. “We should start to see inflation move up in the second half of the year.”

After dropping to an all time low 62.9% in Q2 of 2016, the US home ownership rate rebounded modestly in the subsequent two quarters, then dropped again at the start of the year, before once again rising fractionally to 63.7% in Q2 of 2017 from 63.6% in the previous quarter, just 1% from the all time lows in the series history going back to the mid 1960s.

A breakdown of the data by age group reveals that the primary driver for this decline has been the youngest age cohort. While older Americans, especially those 65 and older, have predictably seen only modest declines in their home ownership in recent decades, it was the youngest age group, those 35 and younger, the Millennials, who over the past decade have seen their home ownership decline steadily from the low 40%’s to the mid-30%, although in Q2 there was a glimmer of good news, as the home ownership rate for Americans 35 and younger posted its first increase in 3 quarters, rising from 34.3% to 35.3%.

As shown in the chart below, the homeownership rate for Millennials has declined from 43.6% in June 2004 to 35.3% in the latest qua rter, and just shy of the lowest rate reported by the Census Bureau going back nearly a quarter century. Of note: while Millennials finally splurged on houses in the latest quarter, the home ownership rates for every other age cohort declined.

But what was most notable in the latest Census data is that for yet another quarter, more Americans opted not to own, but rather rent, and in Q1 the median asking rent jumped by 7.4% Y/Y, from $864 in Q1 to $910.

Broken down by region, the sharpest spike in asking rents was in the Northeast and Western regions, whose median asking rents were nearly identical, at $1,182 and $1,192, an increase of 21% and 16%, respectively.

Finally, what makes the latest spike in rents curious is that while the homeownership vacancy rate declined in the latest quarter, the rental vacancy rate actually increased to 7.3% from 7.0%, the highest since Q1 2016. The rental vacancy has been increasing since Q2 2016 when it troughed at 6.7%, and has since posted four quarters of consecutive growth. It would seem counter intuitive that the vacancy rate is rising even as median asking rents are hitting new all time highs.

While a new record in rents is hardly what Americans want to hear, it will be music to the Fed’s ears as it means that contrary to various other calculations and imputations, inflation in the US is alive and well.

Unofficially, Libor died some time in 2012 when what until then was a giant “conspiracy theory” – namely that the world’s most important reference index, setting the price for $350 trillion in loans, credit and derivative securities had been rigged for years – was confirmed.Officially, Libor died earlier today when the top U.K. regulator, the Financial Conduct Authority which regulates Libor, said the scandal-plagued index would be phased out and that work would begin for a transition to alternate, and still undetermined, benchmarks by the end of 2021.

As Andrew Bailey,chief executive of the FCA, explainedthe decision to eliminate Libor was made as the amount of interbank lending has hugely diminished and as a result “we do not think markets can rely on Libor continuing to be available indefinitely.”

He is right: whether as a result of central banks effectively subsuming unsecured funding needs, or simply due to trader fears of being caught “red-handed” for simply trading it, the number of transactions directly involving Libor have virtually ground to a halt.According to the WSJ, “in one case banks setting the Libor rate for one version of the benchmark executed just 15 transactions in that currency and duration for the whole of 2016.”

As the WSJ adds, the U.K. regulator has the power to compel banks to submit data to calculate the benchmark. “But we do not think it right to ask, or to require, that panel banks continue to submit expert judgments indefinitely,” he said, adding that many banks felt “discomfort” at the current set up. The FCA recently launched an exercise to gather data from 49 banks to see which institutions are most active in the interbank lending market.

Commeting on the decision, NatWest Markets’ Blake Gwinn told Bloomberg that the decision was largely inevitable: “There had never been an answer as to how you get market participants to adopt a new benchmark. It was clear at some point authorities were going to force them. The FCA can compel people to participate in Libor. What can ICE do if they’ve lost the ability to get banks to submit Libor rates?”

Gwinn then mused that “in the meantime, what’s today’s trade? The U.K. has Sonia, but the U.S. doesn’t have a market. There’s still so much uncertainty at this point” Yesterday, “a Libor swap meant something. Now you can’t rely on swaps for balance-sheet hedging.”

And so the inevitable decision which many had anticipated, was finally made: after 2021 Libor will be no more.

Below is a brief history of what to many was and still remains the most important rate:

1986: First Libor rates published.

2008: WSJ articles show concerns with Libor. Regulators begin probes.

2012: Barclays becomes first bank to settle Libor-rigging allegations. U.K. regulator pledges to reform the benchmark.

2014: Intercontinental Exchange takes control of administering Libor.

2015: Trader Tom Hayes gets 14-year prison sentence after Libor trial.

2017: U.K. regulator plans to phase in Libor alternatives over five years.

Yet while anticipated, the surprising announcement of Libor’s upcoming death has taken many traders by surprise, not least because so many egacy trades still exist. As BLoomberg’s Cameron Crise writes, “There is currently an open interest of 170,000 eurodollar futures contracts expiring in 2022 and beyond – contracts that settle into a benchmark that will no longer exist. What are existing contract holders and market makers supposed to do?“

Then there is the question of succession: with over $300 trillion in derivative trades, and countless billion in floating debt contracts, currently referening Libor, the pressing question is what will replace it, and how will the transition be implemented seamlessly?

The FCA’s CEO didn’t set out exactly what a potential replacement for Libor might look like but a group within the Bank of England is already working on potential replacements. “However, any shift will have to be phased in slowly.”

Bailey said it was up to the IBA and banks to decide how to move Libor-based contracts to new benchmarks. After 2021 IBA could choose to keep Libor running, but the U.K. regulator would no longer compel banks to submit data for the benchmark.

The Fed has already been gearing up for the replacement: last month the Alternative Reference Rates Committee, a group made up of the largest US banks, voted to use a benchmark based on short-term loans known as repurchase agreements or “repo” trades, backed by Treasury securities, to replace U.S. dollar Libor. The new rate is expected to be phased in starting next year,and the group will hold its inaugural meeting in just days, on August 1.

The problem with a repo-based replacement, however, is that it will take the placidity of the existing reference rate, and replace it with a far more volatile equivalent. As Crise points, out, “since 2010 the average daily standard deviation of three month dollar Libor is 0.7 basis points. The equivalent measure for GC repo is 4.25 bps. That’s a completely different kettle of fish.”

So as the countdown to 2021 begins, what replaces Libor is not the only question: a bigger problem, and perhaps the reason why Libor was so irrelevant since the financial crisis, is that short-term funding costs since the financial crisis were virtually non-existent due to ZIRP and NIRP. Now that rates are once again rising, the concern will be that not does a replacement index have to be launched that has all the functionality of Libor (ex rigging of course), but that short-term interest rates linked to the Libor replacement will be inevitably rising. And, for all those who follow funding costs and the upcoming reduction in liquidity in a world of hawkish central banks, this means that volatility is guaranteed. In other words, this forced transition is coming in the worst possible time.

Then again, as many have speculated, with the next recession virtually assured to hit well before 2021, it is much more likely that this particular plan, like so many others, will be indefinitely postponed long before the actual deadline.

Amazon wiped out billions of dollars worth of grocery store market cap last month when they announced plans to purchase Whole Foods. The announcement sent shares of Kroger, Wal-Mart, Sprouts, and Target, among others, plunging… (WMT -4%, TGT -5.5%, SFM -7.6%, KR -12%).

But, as we pointed out back in May, well before Amazon’s decision to buy Whole Foods, Amazon’s success in penetrating the traditional grocery market was always a matter of when, not if. Concept stores, like Amazon Go, already exist that virtually eliminate the need for dozens of in-store employees which will allow them to generate higher returns at lower price points than traditional grocers. And, with grocery margins averaging around 1-2% at best, if Amazon, or anyone for that matter, can truly create smart stores with no check outs and cut employees in half they can effectively destroy the traditional supermarket business model.

And while the demise of the traditional grocery store will undoubtedly take time (recall that people were calling for the demise of Blockbuster for nearly a decade before it finally happened), make no mistake that the retail grocery market 10-15 years from now will not look anything like the stores you visit today.

And while the demise of the traditional grocery store will undoubtedly take time (recall that people were calling for the demise of Blockbuster for nearly a decade before it finally happened), make no mistake that the retail grocery market 10-15 years from now will not look anything like the stores you visit today.

So, grocers have a choice: (i) adapt to the technological revolution that is about to transform their industry or (ii) face the same slow death that ultimately claimed the life of Blockbuster.

As such, as the theSt. Louis Post-Dispatchpoints out today, the relatively small Midwest grocery store chain of Schnucks has decided to roll out the first of what could eventually be a large fleet of grocery stocking robots.

A slender robot named Tally soon will be roaming the aisles at select Schnucks groceries, on the lookout for out-of-stock items and verifying prices.

Maryland Heights-based Schnuck Markets, which operates 100 stores in five states, on Monday will begin testing its first Tally at its store at 6600 Clayton Road in Richmond Heights. The pilot test is expected to last six weeks. A second Tally will appear in coming weeks at Schnucks stores at 1060 Woods Mill Road in Town and Country and at 10233 Manchester Road in Kirkwood.

The robots are the first test of the technology in Missouri and could ultimately be expanded to more Schnucks stores.

Each 30-pound robot is equipped with sensors to help it navigate the store’s layout and avoid bumping into customers’ carts. When it detects product areas that aren’t fully stocked, the data is shared with store management staff so the retailer can make changes, said Dave Steck, Schnuck Markets’ vice president of IT and infrastructure.

Tally, created by a San Francisco-based company named Simbe, is also being tested at other mass merchants and dollar stores all across the country.

Founded in 2014, Simbe has placed Tally robots in mass merchants, dollar stores and groceries across the country, including some Target stores in San Francisco last year.

“The goal of Tally is to create more of a feedback mechanism,” Bogolea said. “Although most retailers have good supply chain intelligence, and point-of-sale data on what they’ve sold, what’s challenging for retailers is understanding the true state of merchandise on shelves. Everyone sees value in higher quality, more frequent information across the entire value chain.”

The robot does take breaks. When Tally senses it’s low on power, it finds its way to a charging dock. And, the robot is designed to stay out of the way of customers. If it detects a congested area, it’ll return to the aisle when it’s less busy. If a shopper approaches the robot, it’s programmed to stop moving.

Meanwhile, with nearly 40,000 grocery stores in the U.S. employing roughly 3.5mm people, most of whom work at or near minimum wage, Bernie’s “Fight for $15” agitators may want to take note of this development.

When you arise in the morning, think of what a precious privilege it is to be alive, to breathe, to think, to enjoy, to love.

–Marcus Aurelius–

Why is it so hard to do the things that are in line with our goals but not with our desires at that moment? How can we harness the power of our minds to create a steady fountain of self-discipline each day?

Dealing with Negative People: Advice from a Roman Emperor

I believe happiness is 10% circumstances and 90% attitude.

How you react to your circumstances makes the biggest impact – and the way you choose to deal with negative people is no exception.

As the ruler of a vast empire, Marcus Aurelius had to deal with negative people on a daily basis. In his writings – the self-addressed Meditations – Aurelius provides us with a quote about dealing with negative people that I find to be an incredibly helpful reminder for setting my attitude.

WASHINGTON, DC – Expectations for 2017 economic growth remain at 2.0 percent amid a projected second half slowdown, according to the Fannie Mae Economic & Strategic Research (ESR) Group’s July 2017 Economic and Housing Outlook. With the expansion having entered its ninth year, incoming data point to a second quarter economic growth rebound to 2.7 percent annualized, up from 1.4 percent in the first quarter. However, the full percentage point rise in the saving rate since December signals increased caution among consumers, despite elevated consumer confidence. Decelerating corporate profit growth, commonly seen in the late stages of an expansion, presents a challenge to business investment that is compounded by tax policy uncertainty. In addition, residential investment will likely contribute less to second half growth due to lackluster homebuilding activity and tight for-sale inventory that is restraining home sales. Consequently, se cond half growth is expected to slow slightly to 1.9 percent. Moderate growth is expected to continue in 2018, with potential changes to fiscal and monetary policy posing both upside and downside risks to the forecast.

“While second quarter growth is poised to rebound, we expect growth to moderate through the remainder of 2017. Consumer spending, traditionally the largest contributor to economic growth, is sluggish and is lagging positive consumer sentiment and solid hiring,” said Fannie Mae Chief Economist Doug Duncan. “While labor market slack continues to diminish, wage growth is not accelerating and inflation has moved further below the Fed’s target. These conditions support our call that the Fed will continue gradual monetary policy normalization, announce its balance sheet tapering policy in September, and wait until December for additional data, especially on inflation, before raising the fed funds rate for the third time this year.”

“Construction activity has lost some steam following the first quarter’s weather-driven boost,” Duncan continued. “Meanwhile, very lean inventory continues to act as a boon for home prices and a bane for affordability, particularly among potential first-time homeowners. According to our second quarterMortgage Lender Sentiment Survey, lenders expect to ease credit standards further. However, we continue to project that the pace of growth in total home sales will slow to 3.3 percent this year, as we believe rapid home price gains amid scarce supply will remain a hurdle for potential homebuyers despite improvements in credit access.”

Visit theEconomic & Strategic Researchsite atwww.fanniemae.comto read the full July 2017 Economic Outlook, including the Economic Developments Commentary, Economic Forecast, Housing Forecast, and Multifamily Market Commentary. To receive e-mail updates with other housing market research from Fannie Mae’s Economic & Strategic Research Group, pleaseclick here.

Existing Home Sales in June Dive 1.8 Percent: Same Old Problem? Second and Third Quarter Impact?

The wind down to the end of the second quarter is not going very well. Existing home sales in June fell 1.8% to a seasonally adjusted annualized rate of 5.52 million. The Econoday consensus estimate was 5.58 million.

The slip in pending home sales was no false signal as existing home sales fell 1.8 percent in June to a lower-than-expected annualized rate of 5.520 million. Year-on-year, sales are still in the plus column but not by much, at 0.7 percent which is the lowest reading since February.

Compared to sales, prices are rich with the median of $263,800 up 6.5 percent from a year ago. Another negative for sales is supply which fell 0.5 percent in the month to 1.96 million for an on-year decline of 7.1 percent. Relative to sales, supply is at 4.3 months vs 4.2 months in May.

High prices appear to be keeping first-time buyers out of the market with the group representing 32 percent of sales vs 33 percent in May and 35 percent for all of last year.

Rising prices and thin supply, not to mention low wages, are offsetting favorable mortgage rates and holding down sales. Housing data have been up and down and unable to find convincing traction so far this year. Watch for new home sales on Wednesday where general strength is the expectation.

Existing Homes Sales Month-Over-Month and Year-Over-Year

Existing home sales slipped in June, with the blame again placed on low levels of inventory. The decline in sales, announced on Monday by the National Association of Realtors® (NAR), was anticipated, as pending home sales have decreased in each of the previous three months, ticking down 0.8 percent in May.

NAR said sales of existing single-family houses, townhouses, condos and cooperative apartments were down 1.8 percent in June, to a seasonally adjusted annual rate of 5.52 million units, the second slowest performance of the year.

Lawrence Yun, NAR chief economist, says the pullback in existing home sales in June reflected the lull in contract activity in March, April, and May. “Closings were down in most of the country last month because interested buyers are being tripped up by supply that remains stuck at a meager level and price growth that’s straining their budget,” he said. “The demand for buying a home is as strong as it has been since before the Great Recession. Listings in the affordable price range continue to be scooped up rapidly, but the severe housing shortages inflicting many markets are keeping a large segment of would-be buyers on the sidelines.”

The median existing-home price for all housing types in June was $263,800, up 6.5 percent from June 2016 ($247,600). This is a new peak price, surpassing the record set in May. June marked the 64th straight month of year-over-year gains.

The median existing single-family home price was $266,200 in June and the median existing condo price was $245,900. Those prices reflected annual increases of 6.6 percent and 6.5 percent respectively.

The tight supply of homes continues to be reflected in short marketing period. Properties typically stayed on the market for 28 days in June, one day more than in May, but six days fewer than in June 2016. Short sales were on the market the longest at a median of 102 days in June, while foreclosures sold in 57 days and non-distressed homes took 27 days. Fifty-four percent of homes sold in June were on the market for less than a month.

“Prospective buyers who postponed their home search this spring because of limited inventory may have better luck as the summer winds down,” said NAR President William E. Brown. “The pool of buyers this time of year typically begins to shrink as households with children have likely closed on a home before school starts. Inventory remains extremely tight, but patience may pay off in coming months for those looking to buy.”

First-time buyers accounted for 32 percent of existing home sales in June, down from 33 percent the previous month and a year earlier, while individual investors purchased 13 percent, unchanged from a year ago.

Convoluted Logic

Supposedly buyers may have better luck because the pool of buyers is shrinking as summer winds down. Really? By that logic, if there was only one person looking there would be a 100% success rate.

Yun says “The demand for buying a home is as strong as it has been since before the Great Recession.”

Really? By what measure?

Attitudes and Price

This is not a case of inventory or strong unmet demand. Here are the real factors.

The Fed re-blew the housing bubble and wages did not keep up. People cannot afford the going prices. Thus, the number of first-time buyers keeps shrinking.

Millenials do not have the same attitudes towards debt, housing, and family formations as their parents.

Millenials are unwilling to spend money they do not have, for a place that will keep them tied down. They would rather be mobile.

Second and Third Quarter Impact

The decline in existing home purchases portends weakness in consumer spending.

There will be fewer people painting, buying furniture, updating appliances, remodeling kitchens, adding landscaping etc. The pass through effect will be greatest in the third quarter unless there is a rebound.

College graduates and other young Americans are increasingly clustering in urban centers like New York City, Chicago and Boston. And now, American companies are starting to follow them. Companies looking to appeal to, and be near, young professionals versed in the world of e-commerce, software analytics, digital engineering, marketing and finance are flocking to cities. But in many cases, they’re leaving their former suburban homes to face significant financial difficulties, according tothe Washington Post.

Earlier this summer, health-insurer Aetna said it would move its executives, plus most of technology-focused employees to New York City from Hartford, Conn., the city where the company was founded, and where it prospered for more than 150 years.GE said last year it would leave its Fairfield, Conn., campus for a new global headquarters in Boston. Marriott International is moving from an emptying Maryland office park into the center of Bethesda.

Meanwhile, Caterpillar is moving many of its executives and non-manufacturing employees to Deerfield, Ill. from Peoria, Ill., the manufacturing hub that CAT has long called home. And McDonald’s is leaving its longtime home in Oak Brook, Ill. for a new corporate campus in Chicago.

“Visitors to the McDonald’s wooded corporate campus enter on a driveway named for the late chief executive Ray Kroc, then turn onto Ronald Lane before reaching Hamburger University, where more than 80,000 people have been trained as fast-food managers.

Surrounded by quiet neighborhoods and easy highway connections, this 86-acre suburban compound adorned with walking paths and duck ponds was for four decades considered the ideal place to attract top executives as the company rose to global dominance.

Now its leafy environs are considered a liability. Locked in a battle with companies of all stripes to woo top tech workers and young professionals, McDonald’s executives announced last year that they were putting the property up for sale and moving to the West Loop of Chicago where “L” trains arrive every few minutes and construction cranes dot the skyline.”

The migration to urban centers, according toWaPo,threatens the prosperity outlying suburbs have long enjoyed, bringing a dose of pain felt by rural communities and exacerbating stark gaps in earnings and wealth that Donald Trump capitalized on in winning the presidency.

Many of these itinerant companies aren’t really moving – or at least not entirely. Some, like Caterpillar, are only moving executives, along with workers involved in technology and marketing work, while other employees remain behind.

“Machinery giant Caterpillar said this year that it was moving its headquarters from Peoria to Deerfield, which is closer to Chicago. It said it would keep about 12,000 manufacturing, engineering and research jobs in its original home town. But top-paying office jobs — the type that Caterpillar’s higher-ups enjoy — are being lost, and the company is canceling plans for a 3,200-person headquarters aimed at revitalizing Peoria’s downtown.”

Big corporate moves can be seriously disruptive for a cohort of smaller enterprises that feed on their proximity to big companies, from restaurants and janitorial operations to other subcontractors who located nearby. Plus, the cancellation of the new headquarters was a serious blow. Not to mention the rollback in public investment.

“It was really hard. I mean, you know that $800 million headquarters translated into hundreds and hundreds of good construction jobs over a number of years,” Peoria Mayor Jim Ardis (R) said.

For the village of Oak Brook, being the home of McDonald’s has always been a point of pride. Over the year’s the town’s brand has become closely intertwined with the company’s. But as McDonald’s came under pressure to update its offerings for the Internet age, it opened an office in San Francisco and a year later moved additional digital operations to downtown Chicago, strategically near tech incubators as well as digital outposts of companies that included Yelp and eBay. That precipitated the much larger move it is now planning to make.

“The village of Oak Brook and McDonald’s sort of grew up together. So, when the news came, it was a jolt from the blue — we were really not expecting it,” said Gopal G. Lalmalani, a cardiologist who also serves as the village president.

Lalmalani is no stranger to the desire of young professionals to live in cities: His adult daughters, a lawyer and an actress, live in Chicago. When McDonald’s arrived in Oak Brook, in 1971, many Americans were migrating in the opposite direction, away from the city. In the years since, the tiny village’s identity became closely linked with the fast-food chain as McDonald’s forged a brand that spread across postwar suburbia one Happy Meal at a time.

“It was fun to be traveling and tell someone you’re from Oak Brook and have them say, ‘Well, I never heard of that,’ and then tell them, ‘Yes, you have. Look at the back of the ketchup package from McDonald’s,’ ” said former village president Karen Bushy. Her son held his wedding reception at the hotel on campus, sometimes called McLodge.

The village showed its gratitude — there is no property tax — and McDonald’s reciprocated with donations such as $100,000 annually for the Fourth of July fireworks display and with an outsize status for a town of fewer than 8,000 people.”

Robert Gibbs, the former White House press secretary who is now a McDonald’s executive vice president, said the company had decided that it needed to be closer not just to workers who build e-commerce tools but also to the customers who use them.

“The decision is really grounded in getting closer to our customers,” Gibbs said.

Some in Oak Brook have begun to invent conspiracy theories about why McDonald’s is moving, including one theory that the company is trying to shake off its lifetime employees in Oak Brook in favor of hiring cheaper and younger urban workers.

“The site of the new headquarters, being built in place of the studio where Oprah Winfrey’s show was filmed, is in Fulton Market, a bustling neighborhood filled with new apartments and some of the city’s most highly rated new restaurants.

Bushy and others in Oak Brook wondered aloud if part of the reasoning for the relocation was to effectively get rid of the employees who have built lives around commuting to Oak Brook and may not follow the company downtown. Gibbs said that was not the intention.

‘Our assumption is not that some amount [of our staff] will not come. Some may not. In some ways that’s probably some personal decision. I think we’ve got a workforce that’s actually quite excited with the move,’ he said.”

Despite Chicago’s rapidly rising murder rate and one would think its reputation as an indebted, crime-ridden metropolis would repel companies looking for a new location for their headquarters. But crime and violence rarely penetrate Chicago’s tony neighborhoods like the Loop, where most corporate office space is located.

“Chicago’s arrival as a magnet for corporations belies statistics that would normally give corporate movers pause. High homicide rates and concerns about the police department have eroded Emanuel’s popularity locally, but those issues seem confined to other parts of the city as young professionals crowd into the Loop, Chicago’s lively central business district.

Chicago has been ranked the No. 1 city in the United States for corporate investment for the past four years by Site Selection Magazine, a real estate trade publication.

Emanuel said crime is not something executives scouting new offices routinely express concerns about. Rather, he touts data points such as 140,000 — the number of new graduates local colleges produce every year.

“Corporations tell me the number one concern that t: Zerohey have — workforce,” he said.”

Chicago Mayor Rahm Emanuel said the old model, where executives chose locations near where they wanted to live has been upturned by the growing influence of technology in nearly every industry. Years ago, IT operations were an afterthought. Now, people with such expertise are driving top-level corporate decisions, and many of them prefer to live in cities.

“It used to be the IT division was in a back office somewhere,” Emanuel said. “The IT division and software, computer and data mining, et cetera, is now next to the CEO. Otherwise, that company is gone.”

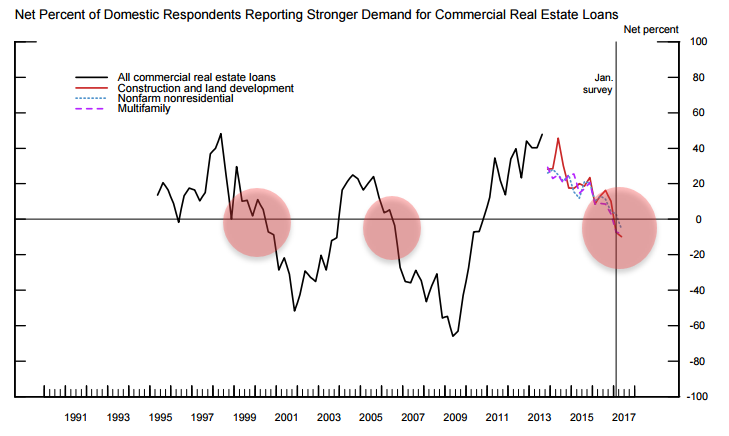

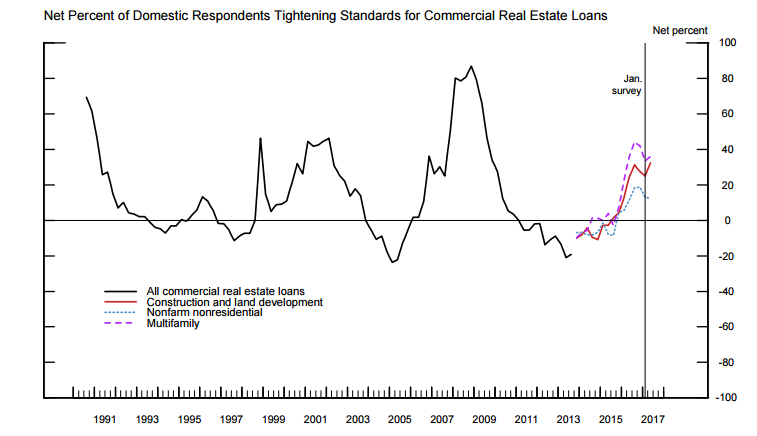

Even the Fed put commercial real estate on its financial-stability worry list.

No, the crane counters were not wrong. In 2017, the ongoing apartment building-boom in the US will set a new record: 346,000 new rental apartments in buildings with 50+ units are expected to hit the market.

How superlative is this? Deliveries in 2017 will be 21% above the prior record set in 2016, based on data going back to 1997, by Yardi Matrix,via Rent Café. And even 2015 had set a record. Between 1997 and 2006, so pre-Financial-Crisis, annual completions averaged 212,740 units; 2017 will be 63% higher!

These numbers do not include condos, though many condos are purchased by investors and show up on the rental market. And they do not include apartments in buildings with fewer than 50 units. This chart shows just how phenomenal the building boom of large apartment developments has been over the past few years:

The largest metros are experiencing the largest additions to the rental stock. The chart below shows the number of rental apartments to be delivered in those metros in 2017. But caution in over-interpreting the chart – the population sizes of the metros differ enormously.

The New York City metro includes Northern New Jersey, Central New Jersey, and White Plains and is by far the largest metro in the US. So the nearly 27,000 apartments it is adding this year cannot be compared to the 5,400 apartments for San Francisco (near the bottom of the list). The city of San Francisco is small (about 1/10th the size of New York City itself), and is relatively small even when part of the Bay Area is included.

Other metros on this list are vast, such as the Dallas-Fort Worth metro which includes the surrounding cities such as Plano. Driving through the area on I-35 East gives you a feel for just how vast the metro is. However, I walk across San Francisco in less than two hours:

Special note: Chicago is adding 7,800 apartments even though the population has begun to shrink. So this isn’t necessarily going to work out.

This building boom of large apartment buildings is starting to have an impact on rents. In nearly all of the 12 most expensive rental markets, median asking rents have fallen from their peaks, and in several markets by the double digits,including Chicago (-19%!), Honolulu, San Francisco, and New York City.

And it has an impact on the prices of these buildings. Apartments are a big part of commercial real estate. They’re highly leveraged. Government Sponsored Enterprises such as Fanny Mae guarantee commercial mortgages on apartment buildings and package them in Commercial Mortgage-Backed Securities. So taxpayers are on the hook. Banks are on the hook too.

This is big business. And it is now doing something it hasn’t done since the Great Recession. The Commercial Property Price Index (CPPI) byGreen Street, which tracks the “prices at which commercial real estate transactions are currently being negotiated and contracted,” plateaued briefly in December through February and then started to decline. By June, it was below where it had been in June 2016 – the first year-over-year decline since the Great Recession:

Some segments in the CPPI were up, notably industrial, which rose 9% year over year, benefiting from the shift to ecommerce, which entails a massive need for warehouses by Amazon [Is Amazon Eating UPS’s Lunch?] and other companies delivering goods to consumers.

But prices of mall properties fell 5%, prices of strip retail fell 4%, and prices of apartment buildings fell 3% year-over-year.

So for renters, there is some relief on the horizon, or already at hand – depending on the market. There’s nothing like an apartment glut to bring down rents. See what the oil glut in the US has done to the price of oil.

Investors in apartment buildings, lenders, and taxpayers (via Fannie Mae et al. that guarantee commercial mortgage-backed securities), however, face a treacherous road. Commercial real estate goes in cycles as the above chart shows. Those cycles are not benign. Plateaus don’t last long. And declines can be just as sharp, or sharper, than the surges, and the surges were breath-taking.

Even the Fed has put commercial real estate on its financial-stability worry list and has been tightening monetary policy in part to tamp down on the multi-year price surge. The Fed is worried about the banks, particularly the smaller banks that are heavily exposed to CRE loans and dropping collateral values.

But the new supply of apartment units hitting the market in 2018 and 2019 will even be larger. In Seattle, for example, there are 67,507 new apartment units in the pipeline.

Therental apocalypsecontinues in Los Angeles. It is interesting to see how far some house humpers will go trying to justify prices. Some are arguing future weed sales are going to create another boom which is somewhat ironic since the benefits are actually to mellow you out, not turn you into a Taco Tuesday baby boomer that becomes a cubicle stressed slave just to purchase a home. And many times people plan on having a family shortly after which means higher childcare costs which they tend to forget. However, Los Angeles once again continues to be theworst place to rent in terms of affordability(and own for that matter). Zillow put out some interesting research and of course as you would expect, those spending nearly half of their income on rent are simply not saving for retirement.

L.A. is the Whole Foods of rental markets

I liken the L.A. housing market to Whole Foods. Great and healthy items that usually break the bank. L.A. has a large number of young and healthy hipsters and Millennials but most can’t buy a home. Heck, most Uber and Lyft drivers have nicer cars than most of us. So we live in this market where the perception is that everyone is well off and healthy when in reality many homeowners are stuck in a ridiculous commute for acrap shack and that is bad for your health.

Of course this isn’t some made up figure. Just take a look at how much income is dumped on rent in various markets:

Los Angeles by far is the worst market for renters surpassing even New York and San Francisco. I’ve made this argument multiple times and that has to do with incomes being far lower in this area compared toSan Franciscoand New York. Of course to house humpers they only see coastal Santa Monica and somehow use this as the reference for every other hood in the area where most of the plebs live. They forget that L.A. County has 10,000,000 people with most not living on the coast.

So it is also telling that L.A. is largely a renting household dominated county. You havemillions of Millennialsacross the state living at home with their parents because rents are too expensive. There is also this romantic idea that many people are stashing millions of dollars away by doing this but the stats show a different story. Some are, but most are not.

What you have is Taco Tuesday baby boomers now stuck in granite countertop HGTV upgraded sarcophagi that they can’t leave for a variety of reasons including locked in Prop 13 tax assessments and adult children back in their nursery rooms. You also have the issue of low inventory that is plaguing the country:

The low inventory dilemma is not only a SoCal phenomenon but has also impacted most urban metro markets. This is why housing as an entire asset class has soared with the stock market since 2009. Unlike the stock market however, scarcity has been a large factor driving prices up in real estate.

The issue of rents is problematic however. As the percentage of households that rent grows, you are going to get those in the middle being squeezed. What do renter households care if taxes get increased on property if they don’t own? Back in 1978 when Prop 13 passed you had a much larger percentage of California homeowners. Today that is clearly not the case. “Well we’ll just increase the rent and pass it on!” Do you think people think like this? Of course not! Just take a look at New York City where only 31 percent of households own. And look at how they tax people there. That is the future. Where only the uber elite will be comfortable in their homes. Grandfathered in Taco Tuesday baby boomer homeowners will live in million dollarcrap shacksand shop at the 99 Cents Store.

The idea that broke Millennials were going to buy in mass in Los Angeles never made sense. Many would rather eat out, work out, and live a more Spartan life (many by necessity). Ironically more are healthier than those pot belly cubicle dwellers that are stuck in obscene traffic everyday having to make that massive 30-year mortgage commitment. But hey, we do live in the Whole Foods of housing markets.

The housing market is suffering from a supply shortage, not a demand dilemma. As Millennial first-time homebuyer demand continues to increase, the inventory of homes for sale tightens. At the same time, prices are increasing, so why aren’t there more homeowners selling their homes?

In most markets, the seller, or supplier, makes their decision about adding supply to the market independent of the buyer, or source of demand, and their decision to buy. In the housing market, the seller and the buyer are, in many cases, actually the same economic actor. In order to buy a new home, you have to sell the home you already own.

So, in a market with rising prices and strong demand, what’s preventing existing homeowners from putting their homes on the market?

“Existing homeowners are increasingly financially imprisoned in their own home by their historically low mortgage rate. It makes choosing a kitchen renovation seem more appealing than moving.”

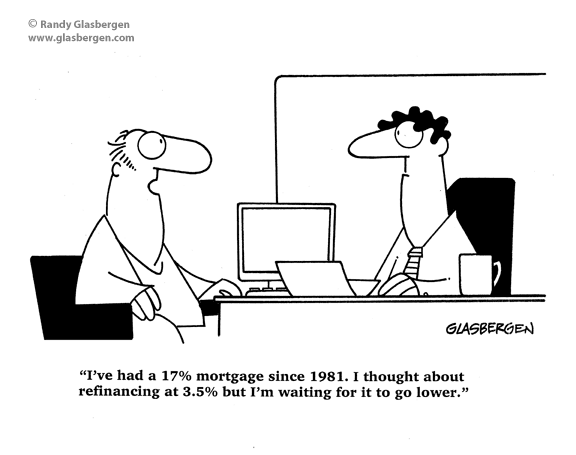

The housing market has experienced a long-run decline in mortgage rates from a high of 18 percent for the 30-year, fixed-rate mortgage in 1981 to a low of almost 3 percent in 2012. Today, five years later, mortgage rates remain just a stone’s throw away from that historic low point. This long-run decline in rates encouraged existing homeowners to both move more often and to refinance more often, in many cases refinancing multiple times between each move.

It’s widely expected that mortgage rates will rise further. This is more important than we may even realize because the housing market has not experienced a rising rate environment in almost three decades! No longer is there a financial incentive to refinance for most homeowners, and there’s more to consider when moving. Why move when it will cost more each month to borrow the same amount from the bank? A homeowner can re-extend the mortgage term another 30 years to increase the amount one can borrow at the higher rate, but the mortgage has to be paid off at some point. Hopefully before or soon after retirement. Existing homeowners are increasingly financially imprisoned in their own home by their historically low mortgage rate. It makes choosing a kitchen renovation seem more appealing than moving.”

There is one more possibility caused by the fact that the existing-home owner is both seller and buyer. In today’s market, sellers face a prisoner’s dilemma, a situation in which individuals don’t cooperate with each other, even though it is seemingly in their best interest to do so.

Consider two existing homeowners. They both want to buy a new house and move, but are unable to communicate with each other. If they both choose to sell, they both benefit because they increase the inventory of homes available, and collectively alleviate the supply shortage. However, if one chooses to sell and the other doesn’t, the seller must buy a new home in a market with a shortage of supply, bidding wars and escalating prices. Because of this risk, neither homeowner sells (non-cooperation) and neither get what they wanted in the first place – a move to a new, more desirable home. Imagine this scenario playing out across an entire market. If everyone sells there will be plenty of supply. But, the risk of selling when others don’t convinces everyone not to sell and produces the non-cooperative outcome.

Possible Outcomes

Owner moves, but pays a price escalated by supply shortages for a more desirable home

Owner stays in current house and does not get a more desirable home

Owner moves, finding a more desirable home without paying a price escalated by supply shortages

Rising mortgage rates and the fear of not being able to find something affordable to buy is imprisoning homeowners and causing the inventory shortages that are seen in practically every market across the country. So, what gives in a market short of supply relative to demand? Prices.According to the First American Real House Price Index, the fast pace of house price growth, combined with rising rates, has had a material impact on affordability. In our most recent analysis in April, affordability was down 11 percent compared to a year ago. It was once said that a man’s home is his castle. In today’s market, a man’s home may be his prison, but he is getting wealthier for it.

The formation of a BRICS gold marketplace, which could bypass the U.S. Petrodollar in bilateral trade, continues to take shape as Russia’s largest bank, state-owned Sberbank, announced this week that its Swiss subsidiary had begun trading in gold on the Shanghai Gold Exchange.

Russian officials have repeatedly signaled that they plan to conduct transactions with China using gold as a means of marginalizing the power of the US dollar in bilateral trade between the geopolitically powerful nations. This latest movement is quite simply the manifestation of a larger geopolitical game afoot between great powers.

Sberbank was granted international membership of the Shanghai exchange in September last year and in July completed a pilot transaction with 200 kg of gold kilobars sold to local financial institutions, the bank said.

Sberbank plans to expand its presence on the Chinese precious metals market and anticipates total delivery of 5-6 tonnes of gold to China in the remaining months of 2017.

Gold bars will be delivered directly to the official importers in China as well as through the exchange, Sberbank said.

Russia’s second-largest bank VTB is also a member of the Shanghai Gold Exchange.

To be clear, there is a revolutionary transformation of the entire global monetary system currently underway, being driven by an almost perfect storm. The implications of this transformation are extremely profound for U.S. policy in the Middle East, which for nearly the past half century has been underpinned by its strategic relationship with Saudi Arabia.

THE RISE & FALL OF THE PETRODOLLAR

The dollar was established as the global reserve currency in 1944 with the Bretton Woods agreement, commonly referred to as the gold standard. The U.S. leveraged itself into this power position by holding the largest reserve of gold in the world. The dollar was pegged at $35 an ounce — and freely exchangeable into gold.

By the 1960s, a surplus of U.S. dollars caused by foreign aid, military spending, and foreign investment threatened this system, as the U.S. did not have enough gold to cover the volume of dollars in worldwide circulation at the rate of $35 per ounce; as a result, the dollar was overvalued.

America temporarily embraced a new paradigm in 1971, as the dollar became a pure fiat currency (decoupled from any physical store of value), until the petrodollar agreement was concluded by President Nixon in 1973.

The quid pro quo was that Saudi Arabia would denominate all oil trades in U.S. dollars, and in return, the U.S. would agree to sell Saudi Arabia military hardware and guarantee the defense of the Kingdom.

Areport by the Centre for Research on Globalizationclarifies the implications of these most recent moves by the Russians and the Chinese in an ongoing drive to replace the US petrodollar as the global reserve currency: