For those looking for key market inflection points, BMO’s Brad Wishak highlights a divergence that was a key tell for recent market action, and may portend even more pain in the coming weeks.

According to Wishak, one place that telegraphed the recent market turmoil was the venerable New York Stock Exchange: the NYSE is the worlds largest stock exchange by market cap (21 trillion) yet “seems to get very little main stream attention for reasons I’ll never understand.”

And, Wishak adds, “when the largest stock exchange in the world throws up a few negative divergences, I want to listen” for the following three reasons:

While the other major indices are hugging their 200 dma, the NYSE is firmly through it

Additionally, the 2018 Channel trend line support broken

But the biggest tell for me took place in September….while all the other majors were marking fresh all time highs, the largest exchange in the world wasn’t even close to confirming ….this doesn’t happen often………another one for the radar

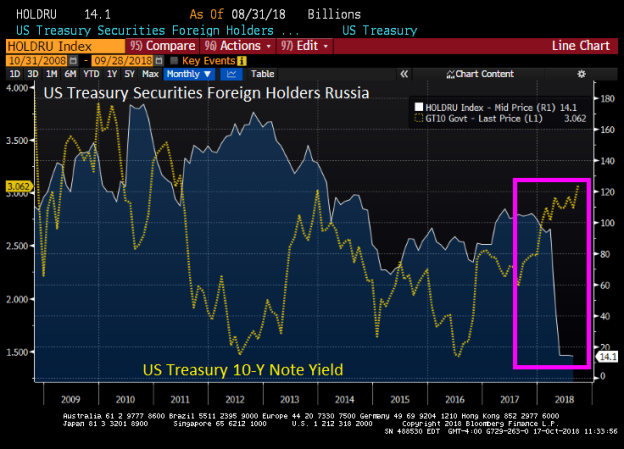

As predicted, Russia has reduced its holdings of US Treasuries as US rates continue to rise.

But Russia is a relatively small player in the US Treasury market (unless they are using proxies like postage-stamp sized Luxembourg, Ireland or the Cayman Islands).

As The Federal Reserve SLOWLY unwinds its balance sheet, the Confounded Interest blog is surprised that Japan and China have not unloaded MORE of their Treasury holdings.

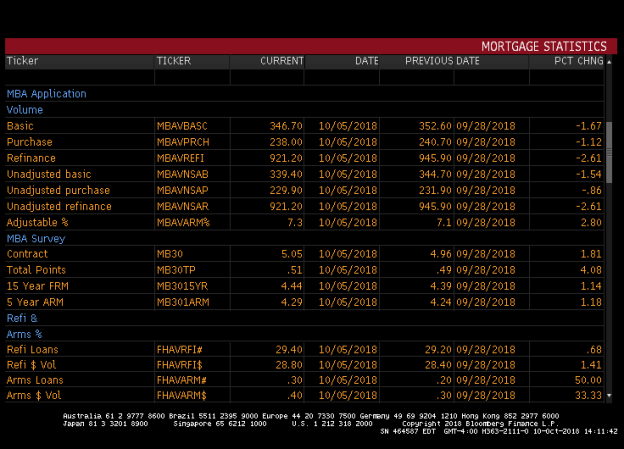

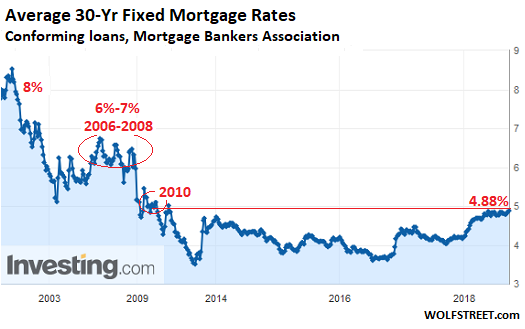

After sliding 2.1% the prior week, mortgage applications collapsed 7.1% last week as mortgage rates topped 5.00%…

Ignoring the collapses during the Xmas week of 12/29/00 and 12/26/14, this is the lowest level of mortgage applications since September 2000…

The Refinance Index decreased 9 percent from the previous week.

The seasonally adjusted Purchase Index decreased 6 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was 2 percent higher than the same week one year ago.

Perhaps this is why…

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) increased to its highest level since February 2011, 5.10 percent, from 5.05 percent, with points increasing to 0.55 from 0.51 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

Still, The Fed should keep on hiking, right? Because – “greatest economy ever..” and so on…

As we noted previously,the refinance boom that rescued so many in the post-2008 ‘recovery’ is now over. If rates hit 5%, the pool of homeowners who would qualify for and benefit from a refinance will shrink to 1.55 million, according to mortgage-data and technology firm Black Knight Inc. That would be down about 64% since the start of the year, and the smallest pool since 2008.

Naturally, hardest hit by the rising rates will be young and first-time buyers who tend to make smaller down payments than older buyers who have built up equity in their previous homes, and middle-income buyers, who can least afford the extra cost. Khater said that about 45% of the loans that Freddie Mac is backing are to first-time buyers, up from about 30% normally, which also means that rising rates could have an even bigger impact on the market than usual.

Younger buyers are also more likely to be shocked by higher rates because they don’t remember when rates were more than 18% in the early 1980s, or more recently, the first decade of the 2000s, when rates hovered around 5% to 7%.

“There’s almost a generation that has been used to seeing 3% or 4% rates that’s now seeing 5% rates,” said Vishal Garg, founder and chief executive of Better Mortgage.

Between Hurricanes Michael and Hurricane Jerome (Powell), mortgage refinancing applcations are taking a big hit.

The Mortgage Bankers Association (MBA) refinancing applications index fell 9% from the previous week as 30-year mortgage rate continued to rise.

Mortgage purchase applications fell 5.52% WoW, but it is in the “mean season” for mortgage purchase applications and there was a hurricane (Michael). And then you have hurricane Jerome (Powell) battering the mortgage markets.

In addition to Hurricane (weather and Federal government), there is also the decline in Adjustable Rate Mortgages (ARMs) since the financial crisis.

(Blinders Off Research) We have been testing the upper limits of used vehicle pricing (and new) all year. I think we have finally reached a point where the consumer has started rejecting higher prices (used vehicles for now). There were a couple of events last month that raised concern ahead of the most recent used car and truck CPI report:

2. There was a significant drop in used vehicle values during the last week of September.

The sudden increase in used vehicle inventory is a strong signal that the rate of sale has slowed due to price increases that consumers are not willing to absorb. Most retail dealers have a rigid 60-day cut off for used vehicle inventory. As a vehicle nears the 60-day mark, the dealer is forced to heavily discount that vehicle or face an even greater loss by disposing of it through wholesale auction (60 days of depreciation, reconditioning expense, transportation and auction fees). This is also likely related to the sharp drop in used vehicle values during week 4 of September as retail dealers returned to auction and adjusted their bids after realizing the vehicles they previously purchased did not sell at the prices they anticipated.

New and used inventory levels are still showing a draw YTD, but the rate of change is concerning. I am completely convinced that the strength we’ve seen in both new vehicle volume and pricing this year is due in large part to the incredibly strong performance in used vehicle values. If the recent trend in used vehicle values changes, things could get ugly and FAST!

Additionally, take note of the dip in time to equity from 2006-2007 and how similar it is to the dip in 2018. It took this year’s used vehicle appreciation in order to offset the consistent increase in loan terms since 2009. If used vehicle values roll over, we have the same exact setup that led to the spike in time to equity from 2007-2008.

I would take the drop in used car and truck CPI as a serious warning with larger implications to come. I am still confident in Q3 earnings for manufacturers, retail dealers and rental car companies but would proceed with caution going forward.

(ZeroHedge) Last March, wediscussedwhy few things are as important for China’s wealth effect and economy, as its housing bubble market. Specifically, as Deutsche Bank calculated at the time, “in 2016 the rise of property prices boosted household wealth in 37 tier 1 and tier 2 cities by RMB24 trillion, almost twice their total disposable income of RMB12.9 trillion.” The German lender added that this (rather fleeting) wealth effect “may be helping to sustain consumption in China despite slowing income growth” warning that “a decline of property price would obviously have a large negative impact.”

Naturally, as long as the housing bubble keeps inflating and prices keep rising, there is nothing to worry about as the population will keep spending money buoyed by illusory wealth appreciation. It is when housing starts to drop that Beijing begins to panic.

Fast forward to today, when Beijing may be starting to sweat because whereas Chinese property developers usually count on September and October to be their “gold and silver” months for sales, this year has turned out to be different. As the SCMP reports, not only were sales figures grim for September, but the seven-day national holiday last week also brought at least two “fangnao” incidents – when angry, and often violent, homeowners protest against price cuts offered by developers to new buyers.

These protests are often directed at sales offices, with varying levels of intensity – from throwing rocks to holding banners and putting up funeral wreaths. The risk, of course, is that as what has gone up (wealth effect) will come down, and as home ownership has remained the most important channel of investment for urban households in China in the past decade, price cuts have become increasingly unacceptable and a cause for social unrest.

Just last week, angry homeowners who paid full price for units at the Xinzhou Mansion residential project in Shangrao attacked the Country Garden sales office in eastern Jiangxi province last week, after finding out it had offered discounts to new buyers of up to 30%.

Country Garden cut the selling price at one of its residential developments by 1/3. Those who paid full price smashed the sales office. Similar incidents had happened before, and will again. It’s impossible to remove “the guarantee of principal”(刚性兑付)in China. pic.twitter.com/UxHFODYxmc

A similar incident took place in suburban Shanghai, where the same developer slashed prices at another project called One Mansion by a quarter.

While the protests have been isolated so far, the risk is that the greater the slide in property prices, the more widespread popular anger will become:

“Property accounts for roughly 70 per cent of urban Chinese families’ total assets – a home is both wealth and status. People don’t want prices to increase too fast, but they don’t want them to fall too quickly either,” said Shao Yu, chief economist at Oriental Securities.

Or fall at all, for that matter.

While China’s stock market has had its ups and down, along the way accompanied by various “rolling” bubbles affecting assored Chinese assets, China’s property market has soared since the 2000s making home ownership the quickest way to gain wealth. In Beijing, homes that went for an average of around 4,000 yuan (US$580) per square metre in 2003 are now above 60,000 yuan (US$8,600) a square metre, according to property price data provider creprice.cn.

And, in a page right out of Ben Bernanke’s playbook, who in 2005 claimed that “we’ve never had a decline in housing prices on a nationwide basis” and as a result never would, what is now taking place in China is nothing short of a shock to the general population: “People are so used to rising prices that it never occurred to them that they can fall too. We shouldn’t add to this illusion,” Shao said.

Meanwhile, dreading that this moment would eventually come, the government has been working on measures to cool property prices for years, calling residential real estate not only an economic issue but also “an important issue for people’s livelihoods that influences social stability”, in a directive back in 2010.

And while the industry remained strong in the first eight months of the year it started slowing last month, according to data provider China Real Estate Information Corp. Official statistics showed that in Shangrao, where the violent protest occurred, transactions of homes last month fell by 22% from August and 18% from the same month last year. In Shanghai, sales in the past five weeks have risen slightly from the same period last year, but average prices dropped in September by over 3% from August and 1.4% from the same period last year.

Quoted by SCMP, Zhang Dawei, chief analyst at Centaline Property, warned that not only were the overall sales dropping, but poor construction quality could also be a cause for more violence. “Try not to buy homes built in 2018, because while the developers were short of money, the same is the case with contractors,” he said, and had an even more ominous warning about what’s coming: “The fourth quarter would be a peak time for residential project completion. Issues which used to be papered over by rising prices could erupt in this period… so we should look out for a sudden surge [public violence] in the coming months.”

Ultimately, it’s all a question of public expectations: expectations that have been number following years of government bailouts and bubble reflating, making sure that every single drop in housing was promptly offset. Hu Xingdou, a Beijing-based economist, said despite China’s market-oriented reforms 40 years ago, investors still lacked respect for market and social rules.

“They don’t have the spirit of contract, and they always think they can fight against the rules,” he said. “As a commodity, the value of homes can both rise and fall. Investors should obey this fundamental rule.”

But why should they if until recently, policymakers did everything in their power to avoid them this simplest of lessons.

To be sure, public anger at falling prices is hardly new. Rampaging against price cuts was first seen in 2011, when homebuyers of a residential project named Oriental Rose in Beijing’s Tongzhou district mobbed a Huaye sales office after the firm cut prices by a tenth.

Similar incidents have erupted whenever investors have found their property value depreciating. And, in a country where there are relatively fewer investment channels and an unpredictable stock market, such protests are always couched as a struggle to protect individual rights. In many such cases, protesters demand compensation or cancellation of their purchase, and in order to prevent further social disorder, developers often accept their demands.

In other words, moral hazard in China is so pervasive, it threatens the very fabric of society.

Wang Cailiang, director of the Beijing Cailiang Law Firm, said although fangnao was against the law, the government had tolerated such protests because it was ultimately responsible for the surging prices; and it is better to punt to the real estate company than being forced to directly bailout consumers.

“It was the government that pushed up the prices by profiting from selling land to developers in the past two decades,” he said. “Now public anger over home prices has become a major social issue.”

At a meeting of the Communist Party’s Politburo in late July, top officials reiterated that “containing home price gains” would be a priority in the second half of the year. Of course, if home price losses accelerate to the downside, Beijing will have no choice but to scramble and reflate another bubble, even as the Trump administration scrutinizes every monetary and fiscal decision by Beijing with a fine toothed comb.

Meanwhile, anger is only set to grow, the only question is whether it will be a slow boil or a violent eruption. Economist Shao expected average home prices to drop slightly in the coming months as the government continued efforts to control them. In the first two weeks of September, growth was close to stagnating in 40 major cities across the mainland with the total number of new home sales up by just 1% from the previous month, according to China Real Estate Information Corp data.

Should this slowdown accelerate significantly to the downside, then the “working class insurrection” that China has been preparing for since 2014…

… will finally materialize with dire consequences for the entire world.

A real estate brokerage near San Francisco is capitalizing on the mass exodus out of the Bay Area.

According to anApril reportby a Bay Area advocacy group, 46% of locals say they want to move out of the area within the next few years, citing the high cost of living and skyrocketing housing prices as main reasons for wanting out. In February,CBS San Franciscoreported that the number of people packing up and leaving the Bay Area has reached its highest level in more than a decade. And fo the first time in ages, the number of people leaving are outnumbering the people coming in.

Meanwhile, a statewide poll conducted by UC Berkeley last year revealed that56 percent of voters have considered moving due to the housing crisis– and 1 in 4 of those residents said they’d leave the state.

To serve the real estate needs of soon-to-be former Bay Area residents, East-Bay broker Scott Fuller – a real estate broker of 18 years, launchedLeavingTheBayArea.com, which helps clients design a relocation strategy. After helping clients sell their home “within a timeframe that works for you,” Fuller will “partner you up with a real estate specialist” in the desired destination city in order to perform an “in-depth needs analysis” in order to coordinate the move.

Fuller says that the majority of his clientele are retirees looking to cash out and move to cheaper pastures in areas such as Portland, Las Vegas, Reno, Dallas, Austin and cities in Arizona. Those looking to remain in California have been moving to Folsom and El Dorado Hills.

The concept of strategic relocation is not new, but it’s recently become more popular, as more and more liberty-loving folks get tired of being crammed into crowded public transportation or spending hours on the road in the daily snail-pace commute. For many, the thought of leaving everything can be a bit terrifying, and if you have a family who doesn’t want to leave, you might be thinking that your Big Move is more of a pipe dream than a real possibility, even though you see the death grip on your everyday freedoms tightening by the day. Here’s the truth: it can be done. And yes, you can be amazingly happy in a new location that is more conducive to the type of life you want to live.

Just like changing your physical condition requires time, discipline, and effort, so does changing your permanent residence. Add to that a lot of planning, and you’ll see yet another reason why a lot of people don’t do it. Before we get into how to effectively and efficiently plan such a move, however, let’s look at why you might choose that path — or at least, why you’re probably interested in the idea. Over the next few days we’ll go through the process of aligning your thought process, getting down to brass tacks, and even what you should be doing when you get to your new location.

Why Move?

Maybe you live in a high-crime neighborhood. Contrary to what society will tell you these days, moving because you don’t want to deal with crime, homeless camps, drug addicts, or other social problems and vices does not make you a racist. If you want a safer environment for your family, then moving might be your best bet. When I first purchased my home in a quiet lake community north of Seattle, it was a great environment for my kid to grow up, with lots of opportunities. A few short years later, within a five block radius, there was a convicted rapist, a chop shop, a meth house, two shootings, and a hotbed of criminal activity on the next corner. That’s not counting the commute, which more than doubled in time due to exploding population. It was time to go, and I don’t regret making that move one bit. It was hard — and it continues to be. For us, it’s worth it, and we would never even consider leaving our little farm.

There is a long list of reasons why moving out of the city is an excellent choice; if you’re already considering it, then you’ve probably already thought of at least some of these:

Crowds

Crime

Traffic/Long commutes

Nosy neighbors

Inability to become truly sustainable

Lack of room for storing preps or other necessities

Higher prices and cost of living

Draconian HOAs and suburban “beautification” organizations

Gun laws

Overregulation, ordinances, taxes, levies, and all the related idiocy

Wanting to get your kids out of public schools

Lack of like-minded attitudes or political/religious ideals

Another thing you might be dealing with in your area is the locale’s natural disaster type. Everything is a trade, and while preparing for natural disaster is somewhat the same regardless of where you live, each area has its own specific challenges that you might not be okay with.

If you live in an urban or even suburban area, you might also find that you’re having a hard time finding people who believe as you do, whether that be your worldview, politics, or religious belief. Like it or not, harassment is a very real thing—and not in the ways the media would have you believe. Being liberty-minded, religious, or even just the wrong color in certain areas can get you in big trouble—and that goes for anyone. Regardless of what race you are, there are places you aren’t welcome.

The reasons to move are many, and the bottom line is that you don’t need to justify those reasons to anyone. What matters is what’s best for you and your family, and if that means pulling stakes, then so be it. If you’re set on moving, let’s talk about how to make it happen.

Choosing a Location

Once you’ve outlined your reasons for moving (thereby outlining what you’d need in a new location), you’ll need to figure out where to go. Do you just move to a different neighborhood? Out of the city into a nearby suburb? Do you stay in the same state but move to a rural locale? Or do you go all out and move to a different part of the country?

A lot of this will depend on what your reasons for moving are. If state gun laws are an issue for you, for instance, then you’ll probably need to move out of state. If you just want to be able to see your kids go to a less violent or better school, you may be able to get away with just moving to a different neighborhood. If you’ve ever wanted to try your hand at homesteading, you’ll be looking at states where that’s being done successfully.

If you use social media, you can look at groups that are local to the area you’re interested in moving to, to get a feel for the culture. Read their local paper, maybe even pull up the radio frequencies for their local police and fire and listen to the type of calls they’re dealing with on a daily basis. Are they getting a lot of overdoses? Shootings? What area of the town or county are the calls coming from? Are they places you can avoid? Is the crime location-based (such as a specific block or business) or is it widespread all over the county? If you notice over the course of a few weeks of paying attention that a specific street gets a lot of calls, or maybe the cops get called to a certain bar for fights, you can avoid that problem by simply not going to that location.

Look up the laws in your proposed new locale and see what’s considered legal and what’s not. You may very well choose to ignore certain laws in your quest for more freedom, but you should at least be able to make an informed decision about what you’re choosing, and what the potential consequences are so you can mitigate any potential fallout.

Check the county zoning laws and building permit requirements, too. One person I know found the perfect off-grid home—only to find that it was sitting just on the wrong side of the county line, in a location where the county wanted permits for everything and lots of taxes and fees. They chose to pass on that house and went to a county where there are no building permits, and no one cares what they do on their land.

Before choosing a location, you can also pull up all manner of data on everything from average income and education level to demographics, home prices, economic growth, and anything else you’d like to know. It all depends on what kinds of information you seek, and whether you’re willing to do the research. You’re never going to find the perfect place; you can, however, find something that fits the non-negotiables. Check out the local weather too, and keep in mind what will be expected in that area. Are you choosing a place with hard winters? Super-hot summers? Higher altitude? Before you throw out the idea of living in a place with rough winter, for instance, keep in mind that there are positives to everything. Snow runoff, for instance, can help you water your garden months later during a drought if you’ve thought ahead in terms of collection. And after the busyness of spring and summer, you’ll look forward to winter, when you have a freezer full of meat, shelves and root cellar packed with food, enough firewood to keep the house warm, and lots of time to work on indoor projects or study new skills in preparation for spring thaw.

One more thing—be aware of any tourist attractions, natural wonders, or other curiosities in your area. They draw crowds and everything that goes with them. You might have your heart set on living in the mountains of Wyoming—only to later realize that you moved too close to Yellowstone National Park and now have tens of thousands of people clogging your local area for half the year.

Taking the Next Step

Once you’ve decided on a location (or at least narrowed it down to 2), it’s time to talk funding. Look at average rents/mortgage payment amounts. You may need to rent a smaller place until you can buy. You may want a bit of land to raise animals. You may choose to live remotely or in a small town near a larger area. If your ultimate goal is to get as off-grid as possible, understand that you’re not going to want to go directly from an urban or suburban environment directly to a place where you have no electricity and have to haul water. You and your family will get frustrated very fast, and you’ll be tempted to move back. Start small; rent a place with a well and power.

Above all, be realistic about how it’ll be. The first year is really, really hard. The second year is a bit easier but it’s still difficult. Don’t be tempted to show up and assume you’ll be able to be fully sustainable within a year. You’ll learn some hard lessons; those lessons, however, will not only make you stronger, but you’ll find that you’re able to adapt better for the next situation. You’ll learn to use what you have instead of running to the store for everything. Depending on where you end up, you may find that certain times of the year require you to prepare, or forego certain activities in favor of making your life easier later. You’ll learn that at least part of each season is spent preparing for the next one, or getting done various tasks that need doing. There’s a routine to it, however, and over time you’ll also find that you are emotionally attached and invested in your homestead. It’s something you’ve worked on and sweated over, and it helps you survive. If you can find your spot in a state or area that is also more liberty-minded than where you are, you’re doubly blessed.

If you’ve read this far and aren’t interested in taking the leap of faith, that’s fine too — there are those who believe that freedom can be found anywhere. Ultimately, it’s your choice, and you don’t have to defend that to anyone either. For those who can smell the fresh air and imagine a different life for yourself and your family, however, stay tuned. Tomorrow we’ll talk about where you’ll find the money to make it happen.

(ZeroHedge) When we reported Wells Fargo’s Q1 earningsback in April, we drew readers’ attention to one specific line of business, the one we dubbed the bank’s “bread and butter“, namely mortgage lending, and which as we then reported was “the biggest alarm” because “as a result of rising rates, Wells’ residential mortgage applications and pipelines both tumbled, sliding just shy of the post-crisis lows recorded in late 2013.”

Then, a quarter ago a glimmer of hope emerged for the America’s largest traditional mortgage lender (which has since lost the top spot to alternative mortgage originators), as both mortgage applications and the pipeline posted a surprising, if modest, rebound.

However, it was not meant to last, because buried deep in its presentation accompanyingotherwise unremarkable Q3 results(modest EPS miss; revenues in line), Wells just reported that its ‘bread and butter’ is once again missing, and in Q3 2018 the amount in the all-important Wells Fargo Mortgage Application pipeline shrank again, dropping to $22 billion, the lowest level since the financial crisis.

Yet while the mortgage pipeline has not been worse in a decade despite the so-called recovery, at least it has bottomed. What was more troubling is that it was Wells’ actual mortgage applications, a forward-looking indicator on the state of the broader housing market and how it is impacted by rising rates, that was even more dire, slumping from $67BN in Q2 to $57BN in Q3, down 22% Y/Y and the the lowest since the financial crisis (incidentally, a topic we covered recently in “Mortgage Refis Tumble To Lowest Since The Financial Crisis, Leaving Banks Scrambling“).

Meanwhile, Wells’ mortgage originations number, which usually trails the pipeline by 3-4 quarters, was nearly as bad, dropping $4BN sequentially from $50 billion to just $46 billion. And since this number lags the mortgage applications, we expect it to continue posting fresh post-crisis lows in the coming quarter especially if rates continue to rise.

That said, it wasn’t all bad news for Wells, whose Net Interest Margin managed to post a modest increase for the second consecutive quarter, rising to $12.572 billion. This is what Wells said: “NIM of 2.94% was up 1 bp LQ driven by a reduction in the proportion of lower yielding assets, and a modest benefit from hedge ineffectiveness accounting.” On the other hand, if one reads the fine print, one finds that the number was higher by $80 million thanks to “one additional day in the quarter” (and $54 million from hedge ineffectiveness accounting), in other words, Wells’ NIM posted another decline in the quarter.

There was another problem facing Buffett’s favorite bank: while true NIM failed to increase, deposits costs are rising fast, and in Q3, the bank was charged an average deposit cost of 0.47% on $907MM in interest-bearing deposits, nearly double what its deposit costs were a year ago.

Just as concerning was the ongoing slide in the scandal-plagued bank’s deposits, which declined 3% or $40.1BN in Q3 Y/Y (down $2.3BN Q/Q) to $1.27 trillion. This was driven by consumer and small business banking deposits of $740.6 billion, down $13.7 billion, or 2%.

But even more concerning was the ongoing shrinkage in the company’s balance sheet, as average loans declined from $944.3BN to $939.5BN, the lowest in years, and down $12.8 billion YoY driven by “driven by lower commercial real estate loans reflecting continued credit discipline” while period-end loans slipped by $9.6BN to $942.3BN, as a result of “declines in auto loans, legacy consumer real estate portfolios including Pick-a-Pay and junior lien mortgages, as well as lower commercial real estate loans.” This is a problem as most other banks are growing their loan book, Wells Fargo’s keeps on shrinking.

And finally, there was the chart showing the bank’s overall consumer loan trends: these reveal that the troubling broad decline in credit demand continues, as consumer loans were down a total of $11.3BN Y/Y across most product groups.

What these numbers reveal, is that the average US consumer can barely afford to take out a new mortgage at a time when rates continued to rise – if not that much higher from recent all time lows. It also means that if the Fed is truly intent in engineering a parallel shift in the curve of 2-3%, the US can kiss its domestic housing market goodbye.

With US consumers suddenly dreading to see the bottom line on their next 401(k) statement, they now have the housing market to worry about.

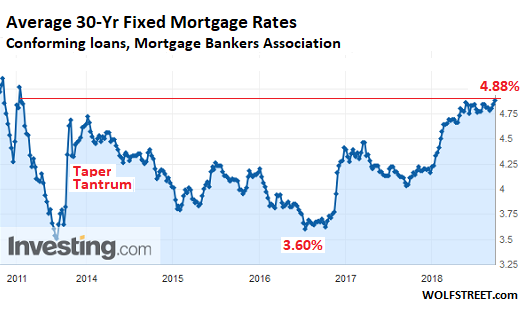

As interest rates spiked in the past month, one direct consequence is that U.S. mortgage rates, already at a seven-year high, surged by the most since the Trump elections.

According to the latest weeklyFreddie Mac statement, the average rate for a 30-year fixed mortgage jumped to 4.9%, up from 4.71% last week and the highest since mid-April 2011. It was the biggest weekly increase since Nov. 17, 2016, when the 30-year average surged 37 basis points.

With this week’s jump, the monthly payment on a $300,000, 30-year loan has climbed to $1,592, up from $1,424 in the beginning of the year, when the average rate was 3.95%.

Even before this week’s spike, the rise in mortgage rates had cut into affordability for buyers, especially in markets where home prices have been climbing faster than incomes,which as we discussed earlier this week, is virtually all. That’s led to a sharp slowdown in sales of both new and existing homes: last month the NAR reported that contracts to buy previously owned properties declined in August by the most in seven months, as purchasing a new home becomes increasingly unaffordable.

“With the escalation of prices, it could be that borrowers are running out of breath,” said Sam Khater, chief economist at Freddie Mac.

“Rising rates paired with high and escalating home prices is putting downward pressure on purchase demand,” Khater told Bloomberg, adding that while rates are still historically low, “the primary hurdle for many borrowers today is the down payment, and that is the reason home sales have decreased in many high-priced markets.”

Meanwhile, lenders and real-estate agents say that, even now, all but the most qualified buyers making large down payments face borrowing rates of 5%. And while rates have been edging higher in recent months, “the last week we’ve seen an explosion higher in mortgage rates,” said Rodney Anderson, a mortgage lender in the Dallas area quoted by the WSJ.

Meanwhile, theWSJ reportsthat once-hot markets are showing signs of cooling down. Bill Nelson, president of Your Home Free, a Dallas-based real-estate brokerage, said that in the neighborhoods where he works, the number of homes experiencing price cuts is more than double the number that are going into contract.

The rise in rates could have far-reaching effects for the mortgage industry. Some lenders—particularly non-banks that don’t have other lines of business —could take on riskier customers to keep up their level of loan volume, or be forced to sell themselves. Many U.S. mortgage lenders, including some of the biggest players, didn’t exist a decade ago and only know a low-rate environment, and many younger buyers can’t remember a time when rates were higher.

Meanwhile, in more bad news for the banks, higher rates will kill off any lingering possibility of a refinancing boom, which bailed out the mortgage industry in the years right after the 2008 financial crisis. If rates hit 5%, the pool of homeowners who would qualify for and benefit from a refinance will shrink to 1.55 million, according to mortgage-data and technology firm Black Knight Inc. That would be down about 64% since the start of the year, and the smallest pool since 2008.

Naturally, hardest hit by the rising rates will be young and first-time buyers who tend to make smaller down payments than older buyers who have built up equity in their previous homes, and middle-income buyers, who can least afford the extra cost. Khater said that about 45% of the loans that Freddie Mac is backing are to first-time buyers, up from about 30% normally, which also means that rising rates could have an even bigger impact on the market than usual.

Younger buyers are also more likely to be shocked by higher rates because they don’t remember when rates were more than 18% in the early 1980s, or more recently, the first decade of the 2000s, when rates hovered around 5% to 7%.

“There’s almost a generation that has been used to seeing 3% or 4% rates that’s now seeing 5% rates,” said Vishal Garg, founder and chief executive of Better Mortgage.

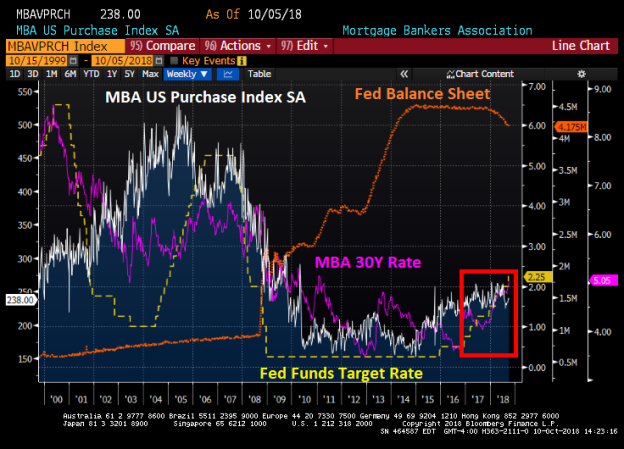

It was inevitable. Federal Reserve rate hikes and balance sheet shrinkage is having the predictive effect: killing mortgage refinancing applications.

And, mortgage purchases applications SA have stalled in terms of growth with Fed rate hikes and balance sheet shrinkage.

WASHINGTON, D.C. (October 10, 2018) – Mortgage applications decreased 1.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 5, 2018.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.7 percent on a seasonally adjusted basis from one week earlier. On an un-adjusted basis, the Index decreased 2 percent compared with the previous week. The Refinance Index decreased 3 percent from the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The un-adjusted Purchase Index decreased 1 percent compared with the previous week and was 2 percent higher than the same week one year ago.

The refinance share of mortgage activity decreased to 39.0 percent of total applications from 39.4 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 7.3 percent of total applications.

The FHA share of total applications increased to 10.5 percent from 10.2 percent the week prior. The VA share of total applications remained unchanged at 10.0 percent from the week prior. The USDA share of total applications increased to 0.8 percent from 0.7 percent the week prior.

With unaffordability reaching levels not seen in decades across some of the most expensive urban markets in the US, a housing-market rout that began in the high-end of marketslike New York Cityand San Francisco is beginning to spread. And as home sales continued to struggle in August, a phenomenon that realtorshave blamed on a dearth of properties for sale,those who are choosing to sell might soon see a chasm open up between bids and asks – that is, if they haven’t already.

While home unaffordabilityis most egregious in urban markets,cities don’t have a monopoly on unaffordability. According to a report byATTOM, which keeps the most comprehensive database of home prices in the US, of the 440 US counties analyzed in the report, roughly 80% of them had an unaffordability index below 100, the highest rate in ten years. Any reading below 100 is considered unaffordable, by ATTOM’s standards. Based on their analysis, one-third of Americans (roughly 220 million people) now live in counties where buying a median-priced home is considered unaffordable. And in 69 US counties, qualifying for a mortgage would require at least $100,000 in annual income (Assuming a 3% down payment and a maximum front-end debt-to-income ratio of 28%). As one might expect, prohibitively high home prices are inspiring some Americans to relocate to areas where the cost of living is lower. US Census data revealed that two-thirds of those highest-priced markets experienced negative net migration, while more than three-quarters of markets where people earning less than $100,000 a year can qualify for a mortgage experienced net positive migration.

Rising home prices have played a big part in driving home unaffordability, but they’re not the whole story. Stagnant wages are also an important factor. The median nationwide home price of $250,000 in Q3 2018 climbed 6% from a year earlier, which is nearly twice the 3% growth in wages during that time. Looking back over a longer period, median home prices have increased 76% since bottoming out in Q1 2012, while average weekly wages have increased 17% over the same period.

Instead of fighting to overpay for existing inventory, one study showed that, for now at least, most Americans would be better off renting than buying a residential property. According to the latest national index produced byFlorida Atlantic University and Florida International Universityfaculty, renting and reinvesting will “outperform owning and building equity in terms of wealth creation.”

However, withthe average national rent at an all-time high,American consumers are increasingly finding that there are no good options in the modern housing market. Which could be one reason why millennials, despite having more college degrees than any preceding generation,are increasingly choosing to rentinstead of buying, even after they get married and start a family.

Chase, one of the biggest home lenders, announces cutting employees in Florida, Ohio, Arizona.

J.P. Morgan Chase CEO Jamie Dimon, Getty Images

JPMorgan Chase & Co. is laying off about 400 employees in its consumer mortgage banking division as parts of the market slow down, people familiar with the matter said.

The bankJPM, -0.56%one of the largest mortgage lenders with about 34,000 mortgage-banking employees, is in the midst of laying off employees in cities including Jacksonville, Fla.; Columbus, Ohio; Phoenix and Cleveland particularly as mortgage servicing has fallen, the people said.

Home sales have slowed as the rise in mortgage rates has been compounded by a lack of homes for sale, increasing prices and a tax bill that reduced some incentives for home ownership. Rising interest rates have also discouraged homeowners from either refinancing their current mortgage or moving and having to get a new mortgage.

JPMorgan isn’t the only bank to lay off mortgage employees. Wells Fargo & Co.WFC, -0.60%the largest U.S. mortgage lender, said in August it is laying off about 650 mortgage employees who mainly work in retail fulfillment and mortgage servicing “to better align with current volumes.”

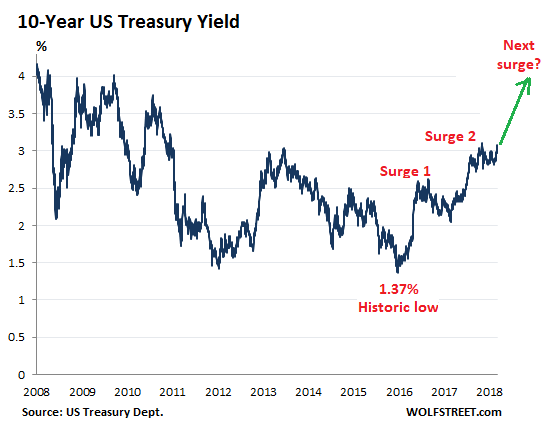

(Nedbank) The first half of 2018 was dominated by tighter global financial conditions amid the contraction in Global $-Liquidity, which resulted in the stronger US dollar weighing heavily on the performance of risks assets, particularly EM assets.

GLOBAL BOND YIELDS ON THE MOVE AMID TIGHTER GLOBAL FINANCIAL CONDITIONS

Global bond yields are on the rise again, led by the US Treasury yields, which as we have highlighted in numerous reports, is the world’s risk-free rate.

The JPM Global Bond yield, after being in a tight channel, has now begun to accelerate higher. There is scope for the JPM Global Bond yield to rise another 20-30bps, close to 2.70%, which is the ‘Rubicon level’ for global financial markets, in our view.

If the JPM Global Bond yield rises above 2.70%, the cost of global capital would rise further, unleashing another risk-off phase. Our view is that 2.70% will hold, for the time being.

We believe the global bond yield will eventually break above 2.70%, amid the contraction in Global $-Liquidity.

GLOBAL LIQUIDITY CRUNCH NEARING AS GLOBAL YIELD CURVE FLATTENS/INVERTS

A stronger US dollar and the global cost of capital rising is the perfect cocktail, in our opinion, for a liquidity crunch.

Major liquidity crunches often occur when yield curves around the world flatten or invert. Currently, the global yield curve is inverted; this is an ominous sign for the global economy and financial markets, especially overvalued stocks markets like the US.

The US economy remains robust, but we believe a global liquidity crunch will weigh on the economy. Hence, we believe a US downturn is closer than most market participants are predicting.

GLOBAL VELOCITY OF MONEY WOULD LOSE MOMENTUM

The traditional velocity of money indicator can be calculated only on a quarterly basis (lagged). Hence, we have developed our own velocity of money indicator that can be calculated on a monthly basis.

Our Velocity of Money Indicator (VoM)is a proprietary indicator that we monitor closely. It is a modernized version of Irving Fisher’s work on the Quantity Theory of Money, MV=PQ.

We believe it is a useful indicator to understand the ‘animal spirits’ of the global economy and a leading indicator when compared to PMIs, stock prices and business cycle indicators, at times.

The cost of capital and Global $-Liquidity tend to lead the credit cycle (cobweb theory), which in turn filters through to prospects for the real economy.

Prospects for global growth and risk assets are likely to be dented over the next 6-12 months, as the rising cost of capital globally will likely weigh on the global economy’s ability to generate liquidity – this is already being indicated by our Global VoM indicator.

(ZeroHedge) The epidemic of falling rents at shopping malls across the United States has been well duly documented here over the past year. In June, wewroteabout an abandoned Macy’s that had been turned into a homeless shelter. Just days agowe followed upon the trend of malls falling victim to the “Amazon effect” in areas like Detroit. Today, we note the latest confirmation that the trend of dying malls across the entire U.S. isn’t stopping anytime soon.

According to a WSJreport, the average rent for malls in the third-quarter fell 0.3% to $43.25 a square foot. This is down from $43.36 in the second quarter and is the first time this number has fallen sequentially since 2011, according to research firm Reis, Inc.

At the same time, vacancy rates are on the ascent, rising to 9.1% in the third quarter from 8.6% in the second quarter. This is the highest they’ve been since the third quarter of 2011, when these rates hit 9.4%. Barbara Denham, senior economist with Reis, told the Journal: “The retail sector is still correcting”. It sure is, Barb.

For instance, here are some photos we included in arecent articleabout one of the hardest hit areas, Detroit:

The depleted food court at Laurel Park Place on Sept. 25, 2018 (Source/ Detroit Free Press)

There are numerous vacant storefronts inside Eastland Center mall in Harper Woods on Sept. 21, 2018 (Source/ Detroit Free Press)

A vacant storefront in Lakeside Mall in Sterling Heights on Sept. 23, 2018 (Source/ Detroit Free Press)

Shopping mall data stands in stark contrast to the rest of the US economy which, as one look at Trump’s twitter account, is widely heralded as “outperforming” (amazing what $1.5 trillion in fiscal stimulus 9 years into an expansion will do). Solid job growth numbers and a good economic outlook have ensured that the Fed’s ultimate goal of people spending money that they don’t have continues; the only difference is that that fascinating creature known as the US consumer simply isn’t racking up this debt at shopping malls anymore, and is opting for online spending like Amazon instead.

At the same time, consumer confidence was at an 18 year high last month and the stock market is also at all-time highs.

Many retail brands are also benefiting from the booming economy and continue to buy back their own stock using debt post “strong” earnings numbers.

The rise in vacancy rates was attributed mostly to closings by Bon-Ton Stores – whichfiledfor Chapter 11 earlier this year – and zombie retailer Sears, which somehow has continued to dodge bankruptcy but is closing stores at an accelerated rate. To make matters worse, Reis told the Journal that a “number of owner-occupied Sears stores were excluded from the numbers, since they don’t have leases.”

That means the real numbers are even worse.

And as the exodus from malls accelerates, many stores are reevaluating their brick and mortar strategy and instead investing in their online businesses. In Q2, e-commerce sales accounted for 9.6% of total retail sales after adjusting for seasonal variations, from 9.5%, in Q1.

Alexander Goldfarb, a senior analyst at Sandler O’Neill + Partners LP, told the Journal: “Any mall that is worried about a Sears or Macy’sclosing has bigger issues.” Goldfarb, defending malls, noted that not all shopping malls are under pressure and that malls in more affluent areas still draw higher end shoppers and continue to attract tenants. “New uses like restaurants and theaters” can still bring in customers.

Home sales in the metro Denver region collapsed in September, forcing sellers to heavily discount asking prices which boosted inventory of properties available for purchase at an unprecedented rate, according to the Denver Metro Association of Realtors (DMAR), as perThe Denver Post.

“The housing inventory and home price adjustments are normal and expected,” said Steve Danyliw, chairman of the DMAR Market Trends Committee, in the report. “What’s not normal? Sales of single-family homes priced over $500,000 dropping 33% from August to September. For those sellers, that’s real turbulence.”

Earlier this summer, DMAR Market Trends Committee saw indications the housing market was cooling but was shocked when it completely froze in September:

“The number of single-family homes sold in September, across all price ranges, dropped 30.5% from August and is down 21.4% compared to September 2017. Condo sales fell a dramatic 42.9 % on the month and are down 17.3% year-over-year,” said The Denver Post.

For years, millennial buyers in metro Denver were plagued with the lack of affordability. When home sales dropped in September, the Denver Post notes that very little buyers showed up.

The inventory of condos and homes available for sale at the end of September shot up to 8,807, an increase of 7.04% from August and about 16% move y/y.

The median price of a single-family home in metro Denver declined to 3.8% from August to $428,000 but remains up 6.1% y/y. Condos, which are popular with millennials, continued to show gains, as its median price rose 1.73% to $301,625 last month and is up 12.8 YTD.

Most of the carnage hit the luxury end of the market. Sales of those homes worth more than $1 million collapsed 44.4% between August and September.

Last month,Bank of America rang the proverbial bell on the US real estate market, saying existing home sales have peaked, reflecting declining affordability, greater price reductions and deteriorating housing sentiment. The report was published by BofA chief economist Michelle Meyer, who warned: “the housing market is no longer a tailwind for the economy but rather a headwind.”

“Call your realtor,” the BofA report proclaimed: “We are calling it: existing home sales have peaked.”

Chart 1 shows there is a leading relationship between the trend in affordability and in home sales — a simple regression suggests the lead is about three months. In major cities, affordability continues to be a significant problem for many Americans amid a rising interest rate environment and elevated home prices, existing home sales should remain under pressure for the foreseeable future.

Chart 2 indicates that the share of properties with price discounts is on the rise, suggesting that sellers are unloading into weakening demand. The data from Zillow reveals that 15% of listings have price reductions, the highest since mid-2013 when home sales tumbled last.

The University of Michigan survey reveals a worsening mood in the perception of buying conditions for homes. Respondents noted that home prices have become too high while rates have become restrictive.

While BofA makes clear the housing market is starting to stall, the Federal Reserve is conducting quantitative tightening and rapidly increasing interest rates to get ahead of the next recession. In other words, liquidity is being removed from the system and the cost of borrowing is headed higher – an environment that is not friendly to real estate and could be the key factor explaining the weakness in metro Denver housing and abroad.

Following therecent dreadful auto sales numbersout of the United States, both Germany and Brazil have posted extremely weak auto production and sales numbers, prompting more questions about the state of the global economy.

According to JP Morgan, auto production in Germany has been surprisingly weak in recent months, with the prospects of a recovery delayed until “at least October.” This was unveiled with the German July Industrial Production data for July which was “a disappointment,” as manufacturing slumped 1.9%m/m and 6% annualized below 2Q18. Of this, automotive was the biggest weakness.

The shifting timing and pattern of holidays across the German states over the summer likely knocked the latest IP data around a lot, but this year the new emissions testing regime is adding a real drag. Since 1st September, all new cars need to be certified under the new testing regime, but some German producers appeared to have fallen far behind this deadline. Some car models have temporarily been removed from sales, while others have had to be modified to meet the new standards, resulting in reduced production levels to manage the changeover.

Meanwhile, according to more concurrent car production data from the German Automobile Association (VDA) which is now available for the month of September – and which counts the number of cars rolling out of factories – production has collapsed even further. An additional problem, is that the VDA data had already slumped in July (almost -20%m/m), while the IP data showed a fall of 6.7%m/m.

While the VDA may be overstating the weakness, it is also possible that IP has much further to fall, adding to concerns about Europe’s slowing economy.

Not to be outdone by the United States or Germany, Brazil also posted plunging numbers for September. Auto production in the country was down 23.5% in September M/M, according to Reuters, while sales were down 14.2% over the same period according to the National Automakers Association. Brazil has traditionally been one of the world’s five largest auto markets until the country’s recent economic downturn. Companies like General Motors, Ford and Chrysler all have major operational facilities in Brazil.

And then there is the US, where earlier this week wereported the latest surprisingly poor auto sales numbers for September.

Results from Ford, Honda, Nissan, Toyota and Fiat all tell the story of an industry that had a terrible month, with few silver linings. Three of these names posted double digit percentage declines in YOY sales and three of them missed analyst estimates.

Some details:

Ford posted an 11% drop, missing analyst estimates of 9.1%. The F-Series pickup line ended a 16-month streak of sales gains. Mustang sales were down 1.3%.

Nissan posted a 12.2% drop in September. Nissan and Infiniti brand car sales fell by 36%, including a 28% drop for the Altima sedan as the company prepared to start selling an all-new version this week.

Toyota sales were down 10.4%, far below estimates of 6.7% for the month. Combined sales for Toyota and Lexus brand cars fell 25.3%.

Fiat posted the only true “beat”, as sales rose 15% versus analyst estimates of 8%. However, the Chrysler brand fell 7% to 14,683 vehicles and the Fiat brand fell 46% to 1,185 vehicles. The deficit was made up on Jeep sales, which were up 14%, as well as sales of Ram pickups and minivans.

Volkswagen of America car sales were down 4.8%

GM third quarter total sales were down 11%. The company stopped reporting monthly numbers earlier this year, with many suspecting that weakness in the production pipeline is responsible; they were right.

As discussedpreviously, the lack of auto incentives was the primary driver for the poor US auto numbers, prompting the question: absent carmaker subsidies, just how strong is the US auto market in particular, and the overall economy in general.

Yet another shopping mall project looks to have fallen victim to “the Amazon effect”, serving as evidence that brick and mortar retail, in the conventional sense, is doomed.

The latest victim is the New Horizon Mall in Calgary. The construction of the “multicultural mega-mall” is nearly complete, but tepid interest forced its developer to push back its planned grand opening to next year. The mall was initially set to open in October of this year. Only 9 of the 517 spaces in the mall have opened for business since May, when owners were first allowed to take possession according to a newreportby Global News.

“It’s surreal. It’s not normal – we’re in the Matrix,” one shopper told Global News.

The developer, Eli Swirsky, president of The Torgan Group of Toronto, told Global News:

“I love the mall. I think the mall will be fine,” he said in an interview. “I wish it was faster, of course, but every time I go there I’m awed by its size and potential and I think we’ll get there.

Swirsky told Global News that he expects 20 stores will be open by the end of September, but he still wouldn’t commit to a final grand opening date. Instead, he said that it will likely happen when 80 to 100 stores have opened. That is seen to push back the grand opening well into spring of next year.

The optimistic outlook stands in the face of eerie reality of the project, which shows “For Lease” signs and empty glass spaces traditionally reserves for stores.

Those who have already taken up shop in the mall, including Rami Tawil of Silk Road Importers, think that pushing the grand opening off until there are more tenants is a good idea: “I think now it’s better if we push it a couple of months because we need more stores here to open. We need the people coming to see more stores.”

The mall style is based on a similar mall that the developer opened in the Toronto area – about 20 years ago. The mall is different from traditional malls in the sense that it doesn’t exclusively lease to tenants. Rather, investors can purchase retail space and then have the option of leasing it to others or operating it themselves. The developer also holds large chunks of space in hopes of enticing anchor tenants. None of these have been announced yet.

The few tenants of the mall are at varying stages of readiness. Some are still trying to figure out what type of product or service may be best to offer at the location. Others are trying to re-sell or lease their spaces, according to the mall’s general manager, Jason Babiuk.

The mall was a $200 million project that broke ground in June 2016. Some believe that the difficulty in filling the mall has to do with its condominium-like ownership model, which could attract the wrong type of investors to such a project.

Retail analyst Maureen Atkinson, a senior partner at J.C. Williams Group stated: “The challenge with the condo model is that the people who run the stores are typically not the people who own them. So they would have sold these to investors … who see it as an investment and they may have trouble finding somebody who wants to run a business.”

Earlier this week we learned that mall rents in the United States were plunging as vacancies were shooting toward record highs. According to a WSJ report, the average rent for malls in the third-quarter fell 0.3% to $43.25 a square foot. This is down from $43.36 in the second quarter and is the first time this number has fallen sequentially since 2011, according to research firm Reis.

At the same time, vacancy rates are on the ascent, rising to 9.1% in the third quarter from 8.6% in the second quarter.

Our take? Instead of trying to re-invent an industry that is already on its deathbed by opening a “multi-cultural” mall, maybe Canada should have, at very least, taken a page out of the United States’ once successful mall playbook: bankrupt retail brands and greasy Asian food court samples.

TheAssociated Press(AP) has revealed a troubling story of the largest ever homeless encampment site mostly made up of Native Americans has quickly erected just south of downtown Minneapolis, Minnesota.

City officials are scrambling to contain the situation as two deaths in recent weeks, concerns about disease and infection, illicit drug use and the coming winter season, have sounded the alarm of a developing public health crisis.

“Housing is a right,” Mayor Jacob Frey said. “We’re going to continue working as hard as we can to make sure the people in our city are guaranteed that right.”

The AP said approximately 300 people are living in the camp that is situated beside 16th Ave S & E Franklin Ave.

Earlier this month, a team of AP reporters visited the camp and found dozens of tents lining the city street.

To their amazement, most of the residents were Native American.

The homeless camp — called the “Wall of Forgotten Natives” because it lined a highway sound barrier, is in a section of the city with a large concentration of American Indians that are suffering from extreme wealth, health, and education inequality. The AP said the tents stand on what was once considered Dakota land.

“They came to an area, a geography that has long been identified as a part of the Native community. A lot of the camp residents feel at home, they feel safer,” said Robert Lilligren, vice chairman of the Metropolitan Urban Indian Directors.

The camp illuminates the inequalities (mentioned above) that face American Indians in the state. AP provides a shocking statistic that American Indians make up 1.1% of Hennepin County’s residents, but 16% of the homeless population, according to government data from April.

It is also a community that is being decimated by opioids. Minneapolis officials in July sued a group of opioid manufacturers and distributors, alleging their actions to promote prescription opioid drugs, such as OxyContin, have caused an addiction crisis straining the city’s resources.

AP said one end of the camp had been designated for families, while adults — some of whom were high on drugs — were on the other end. In the middle, an organization called Natives Against Heroin, a tent where volunteers handed out bottles of water, food, and clothing. The group also provides addicts with clean needles, and most volunteers carry naloxone to treat overdoses.

“People are respectful,” said group founder James Cross. “But sometimes an addict will be coming off a high… We have to de-escalate. Not hurt them, just escort them off. And say “Hey, this is a family setting. This is a community. We’ve got kids, elders. We’ve got to make it safe.”

With hundreds of people living in close quarters, health officials fear an outbreak of infectious diseases like hepatitis A. Local support groups have started administering vaccines. Earlier this month, a woman died when she did not have an asthma inhaler, and one man died from a drug overdose.

Local government agencies have set up areas to provide medical assistance, antibiotics, hygiene kits or other supplies. There are tents advertising free HIV testing, a place to apply for housing, and temporary showers. Portable restrooms and hand-sanitizing stations had also been positioned around the camp.

The Minneapolis City Council voted Wednesday to move the camp to a 1.5-acre commercial property owned by the Red Lake Nation. The decision came five days after Mayor Jacob Frey and representatives of ten tribes said the industrial site was the best place to relocate the tent city.

The new site at 2105-2109 Cedar Ave. South will not be ready until December because demolition work will take several months, according to David Frank, the city’s Community Planning and Economic Development director.

“We will go as quick as we can to have the interim navigation center operational and ready,” Frank said. “We have our permitting people standing by. We have our housing team, our facilities team and our projects management all lined up to do this work.”

The cost of preparing the site with living accommodations for dozens of people will be between $2 million and $2.5 million, Frank added.

Minneapolis’ homeless explosion comes as no surprise. The much larger trend at play is the nation’s homeless population increasing for the first time since 2010 — driven by housing affordability issues, and widening inequalities. But do not tell President Trump the real economy continues to deteriorate.

In 40 different venues over the last three months, President Trump declared the economy is the greatest, the best or the strongest in US history.

— Trump, in a speech at a steel plant in Illinois, July 26

“This is the greatest economy that we’ve had in our history, the best.”

— Trump, in a rally in Charleston, W.Va., Aug. 21

“You know, we have the best economy we’ve ever had, in the history of our country.”

— Trump, in an interview on “Fox and Friends,” Aug. 23

“It’s said now that our economy is the strongest it’s ever been in the history of our country, and you just have to take a look at the numbers.”

— Trump, in remarks on a White House vlog, Aug. 24

“We have the best economy the country’s ever had and it’s getting better.”

In a recent, Bank of America note titled “The Thundering World,” a major theme in development for the 2020s could be “the epic wealth inequality” that is plaguing the economy.

BofA says quantitative easing amplified income and wealth inequality over the last decade. The distribution of wealth is the widest ever. The top 1% own 40% of the global wealth; the bottom 80% own 7%.

What does this all mean? Well, decades of failed economic and social policies are about to come home to roost. The explosion of homelessness in Minneapolis over a short period, is an example of the breakdown of the social fabric that will strain many more municipalities across the country in the years ahead. The America that we knew will not be the same by 2030.

Bank of Canada Gov. Stephen Poloz including “home prices”on his list of risk factors that “keep me up at night”,which he shared with an audience of economists at the prestigious Canadian Club earlier this year. But Poloz’s words of caution have not stopped housing costs for Canadians form climbing to precarious new highs. Signs of this stress are already apparent – for example, in Vancouver, where a chasm between bids and asks has caused the local housing market to grind to a halt.

The latest warning about an impending implosion in the Canadian housing bubble comes courtesy of a quarterly RBC report, which found that the aggregate costs of homeownership in Canada, a category that includes mortgage fees, interest, property taxes and utilities and other miscellaneous costs, have reached their highest levels since 1990.

The most alarming aspect of this trend, according to the bank, is that rising mortgage costs, not home prices, have been the biggest contributing factor over the past year, with mortgage rates rising in each of the last four quarters.

Rising mortgage rates have, of course, been spurred by the BoC’s rate hikes. Today, the average Canadian would need to spent roughly 54% of their income to buy a home.That’s up sharply from 43.2% three years ago.

But in Canada’s most unaffordable housing markets, these figures are considerably higher.

“From overheating to correction to the onset of recovery, we’ve seen pretty much everything in the past three years in Canada’s housing market,” economists at the Toronto-based bank said in the report. “Yet an eye-watering loss of affordability has been a constant.”

In Vancouver, Toronto and even Victoria, RBC’s index of home prices relative to average income has reached 88%, 76% and 65%, respectively. The bank’s data includes costs for condos and detached single-family homes.

And with the BoC widely expected to continue raising interest rates…

“We expect the Bank of Canada to proceed with further rate hikes that will raise its overnight rate from 1.50 percent currently to 2.25 percent in the first half of 2019,” the report said. “This will keep mortgage rates under upward pressure and boost ownership costs even more across Canada in the period ahead.”

…its analysts have warned that a momentous housing implosion looks increasingly likely. Adding a dash of irony to this scenario, the BoC has expressed caution about the housing bubble and cited raising interest rates as a necessary measure to combat it.

The bloom is off the rose for home builders. Yes, it had been a great run, fueled by The Fed’s zero-interest rate policy (ZIRP) and asset purchases (QE). But despite a roaring economy, SPDR S&P Home builders ETF have been falling since January as The Federal Reserve Open Market Committee (FOMC) sticks to their guns and keeps normalizing interest rates.

Yes, the Fed Dots Plot project indicates that there is still upside momentum to short-term interest rates.

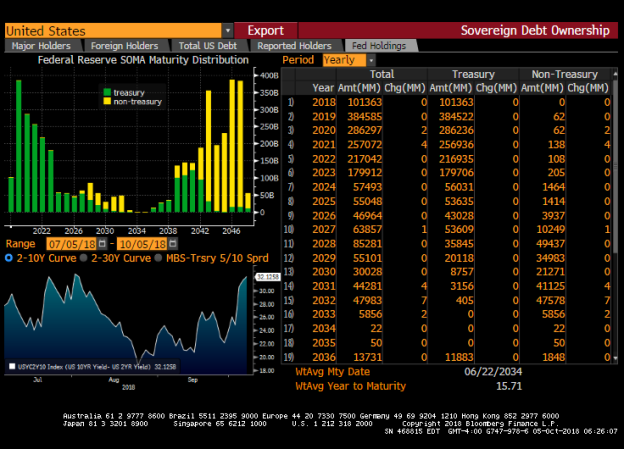

And the Fed’s System Open Market Accounts (SOMA) show a declining inventory of Treasury Notes and Bonds to let mature.

Today’s non-farm payrolls miss, 134k total jobs created in September, sealed the deal on the job creation political debate before the November midterms. That is all things being equal — during President Trump’s first 20 employment reports versus President Obama’s last 20 — the Trump economy created 347k fewer total non-farm payroll jobs, and 137k fewer private sector jobs, than President Obama’s economy.

The differential will move even more against President Trump when October non-farm payrolls are reported, the Friday before the election, as the May 2015 326k jobs comp will be a bar too high to conquer.

These are the facts, spin them as you wish.

On the eve of the midterm elections it is likely that the Democrats will be able to argue that President Obama’s economy created 500k more jobs than President Trump’s economy over a similar period. Reality clashes with virtual reality and bombastic rhetoric.

Perspective

However, all things are never equal. The Trump economy is running up against labor constraints with shortages breaking out almost everywhere, which is reflected in today’s 3.7 percent unemployment rate print, a49-year low. It’s difficult to create the marginal job on this side of the inelastic labor supply curve.

Data should always be placed in the proper context. But, hey, we are talking politics here, and,“politics ain’t beanbag,” folks.

Other Notables

The shrinking labor supply is illustrated in the inflation differentials during the two periods – 4.14 percent under Trump, and 2.12 percent during Obama’s last 20 months in office.

Trump’s nominal Average Hourly Earnings are running about 70 bps higher than Obama

Real Average Hourly Earnings under Trump is about 1.3 percent lower than during President Obama’s last 20 employment reports

Real GDP growth under Trump is almost double President Obama’s last six quarters in office, but not reflected in the overall labor market, which reflects the economy continues to reward capital disproportionate to labor

Manufacturing jobs have recovered smartly during President Trump first 20 months, much of it due to the increase in oil prices, especially in the mining sector

Job creation in the government sector, which, on average, generates higher income paying jobs than the private sector, is much lower under President Trump

Where The Jobs Were In June: Who’s Hiring And Who Isn’t

As noted earlier, September was a hurricane-affected month for payrolls, resulting in lower than expected jobs across several categories, among which Leisure and Hospitality jobs were the hardest hit.

However, a deeper dive reveals that other industries were also severely impacted, with the 2nd worst September in contraction in Retail (-20K), Telecom (-3K), Education (-12K), Child Care (-4K) and Food Services (-23K).

This, according to Southbay Research, was remarkable because while last year’s layoffs surged 100K above trend due to 2 major Hurricanes that displaced millions and destroyed 10s of thousands of homes, with jobless claims across Texas, Florida and Puerto Rico soaring by 100K+, this year, one hurricane came but was very mild and had minimal impact, with Initial Jobless Claims rose a combined 12K. Yet somehow, “the impact was the same.”

Here’s one example: Food Services. As Southbay notes, somehow a mild storm led to layoffs at a scale only seen last year when 2 major Hurricanes shut down Puerto Rico and Florida and pummeled Texas.

One note here is that if one were to revise last month’s data to incorporate the “missing” jobs, the impact on hourly earnings would be adverse as these are mostly lower paying jobs, and while the result would have been higher jobs, it would have also pushed down on hourly earnings.

Odd BLS estimates of layoffs aside, we know the following:

Employment in professional and business services increased by 54,000.

Health care employment rose by 26,000 as hospitals added 12,000 jobs, and employment in ambulatory health care services continued to trend up (+10,000).

Employment in transportation and warehousing rose by 24,000. Job gains occurred in warehousing and storage (+8,000) and in couriers and messengers (+5,000).

Construction employment continued to trend up in September (+23,000).

Employment in manufacturing continued to trend up in September (+18,000)

Employment in mining, employment in support activities for mining rose by 6,000

And visually:

Looking over the past year, the following charts fromBloombergshow the industries with the highest and lowest rates of employment growth for the prior year. The latest month’s figures are highlighted.

One final observation from Southbay Research, who notes that overtime pay dropped as staffing increases.

Overtime is a temporary solution to strong demand. While a drop in overtime can signal a fall in demand, it can signal that employers no longer think the strong demand is temporary.

Whatever the reason, after 1+ years of above-trend overtime, employers have turned to hiring. Because it’s also cheaper than paying double rates for overtime. This, to Soutbay, “is another metric supporting continued hiring growth.”

Fannie Mae and Freddie Mac, the mortgage giants in seemingly perpertual conversatorship with the FHFA, have mortgage loans that are even more risky in terms of loan-to-value (LTV) ratios than during the catastrophic housing bubble of the 2000s.

The “good” news is that the average FICO (credit) score for Fannie and Freddie loan purchases is above those from the housing bubble. But the trend is worrisome.

In terms of Debt-to-income ratios (or Detes as Tom Haverford would say), the Detes are below housing bubble levels, but have been rising since the end of 2008.

Home buyers may soon get at least a little relief. After years of steadily worsening housing shortages, more homes are finally going up for sale.

The number of new listings onrealtor.com®in September shot up 8% year over year, according to a recent report fromrealtor.com. That’s the biggest jump since 2013, when the country was still clawing its way out of the financial crisis. And it gives eager buyers a lot more options to choose from.

“It’s a key inflection point,” says Chief Economist Danielle Hale ofrealtor.com. “There are still more buyers in the market than homes for sale. But in some [parts of the country], the competition is among sellers to attract buyers.”

That’s a big shift from a year ago, when bidding wars and insane offers over asking price were par for the course. But it doesn’t mean the housing shortage has suddenly dissipated.

Nationally, the total inventory of homes for sale was essentially flat compared with the year before—moving down 0.2%. Hale expects the bump in new listings to buoy that inventory.

And while the median home price, at $295,000, was up 7% in September compared with a year ago, the increase in homes hitting the market helped to slow that rise. The median home price in September 2017 was a 10% increase over the previous year.

The new inventory tended to be a little cheaper, by about $25,000, and about 200 square feet smaller than what was already on the market. That could be due to the 3% rise in condo and town home listings.

The influx of homes on the market is partly due to sellers betting that we’ve reached the peak of the market. So they’re rushing to list their homes and get top dollar while they can. But those owners are learning that their home, particularly if it’s priced high, may no longer sell immediately for that price. And homes need to be staged and in tiptop shape.

The increase in inventory is likely to slow wild price growth as well, although prices aren’t likely to fall anytime soon. It all comes back to supply and demand. Folks will pay a premium for something if there’s not enough of it to go around. So while this is fantastic news for buyers, there are bound to be some disappointed sellers who were hoping to get a little more for their abodes.

Of the 45 largest housing markets,San Jose, CA,in the heart of Silicon Valley, saw the biggest boost in new listings, according to the report. It was followed bySeattle; Jacksonville, FL; San Diego; andSan Francisco. That’s a boon to buyers in these ultra expensive markets.

But make no mistake: Prices are still rising, and there aren’t enough homes to go around. Still, the uptick in homes going up for sale “will eventually shift the market from a seller’s market … to a buyer’s market,” says Hale.

It wasn’t a case of flagrant carpetbagging – it was just an honest mistake!

That’s the excuse that one Democratic Congressional candidate in California has offered to justify the fact that he claimed a home in Bethesda Maryland as his primary residence, asthe Fresno Beereported on Tuesday.

Spokesmen for the campaign of TJ Cox – the candidate in question – said last week that the claim was the result of an “honest mistake” and blamed an error by the state for the “oversight.” Cox has offered to repay a roughly $700 tax credit that he received by claiming the home.

Cox owns several businesses in the central San Joaquin Valley and is running against Republican Rep. David Valadao for California’s 21st Congressional District seat.

The Bee had previously reported that Cox owned a three-bedroom, four-bathroom house in Bethesda and had claimed the nearly $1 million home as his principal residence. Cox also claimed a Fresno home as his principal residence, however, federal tax laws prohibit claiming more than one home.

Asked why Cox didn’t notice the oversight, his campaign spokesperson said that Cox’s family was living there.

“It was an honest mistake that he filled out the principal residence not knowing the legal definitions. His family was living there,” said Campaign Spokesman Phillip Vander Klay.

“That’s just kind of the situation,” Vander Klay added. “We are working to get this fixed.”

Cox had reportedly purchased the Bethesda home for his family to live in while his wife, Dr. Kathleen Murphy, studied public health policy at Johns Hopkins University. Cox lived and worked in Fresno while his family lived in Maryland.

Though Cox’s campaign tried to construe the tax credit claim as a mistake on the state of Maryland’s part, the Fresno Bee found that it had been coded as Cox’s principal residence when he first bought the home – meaning that the credit claim was an oversight on Cox’s part.

But we’re sure that Cox’s inability to keep track of basic tax-related upkeep will have no bearing on his ability to properly allocate how the tax dollars of his constituents are spent.