Real estate agents work very hard and deal with a wide array of emotions on a day to day basis. Sometimes, it’s an hour by hour basis! Sometimes, we need a little something to unwind, or to perk up, or to celebrate, or to drown our sorrows in. Basically, there’s always a reason for an agent to need a drink, so here’s the top ten list of drinks for real estate agents.. Drink responsibly!

1. The Broker Blues – The time when you don’t have any pending deals. You’re feeling sorry for yourself and wondering why the hell you work in real estate.

Ingredients:

½ oz. Blue Curaco

½ oz. Vodka

A squeeze of lime juice

Shake with ice and strain into a shot gloss. Repeat, as necessary.

2. The New Listing Lemon Drop – When you get a new listing and you’re feeling your inner Superhero coming back, baby!

Ingredients:

1 ½ oz. Vodka

½ oz. Triple Sec

1 tsp. sugar

1 tsp. lemon juice

Maraschino cherry

Mix Vodka,Triple Sec,sugar,and lemon juice in a cocktail shaker half-filled with ice; shake well until sugar is well blended. Pour strained liquor into sugar-rimmed martini glass and don’t forget to garnish with a cherry on top! Note: To create a sugar-rimmed glass, take a lemon wedge and rub the rim of the glass. Dip the edge of the glass into superfine sugar.

3. The Red Hot Realtor – You’re dominating the market. You have homes flying off the streets and clients lining up wanting your help. You’re on fire! This drink is simple, because you don’t have time to make anything complicated.

Ingredients:

1 8oz. glass of 7-up

1 shot of Fireball Cinnamon Whisky

4. The All-Nighter – You’ve had a long day. You spent hours on the phone and computer pulling comps, setting up showings and answering calls and emails. You have offers to respond to and draft, and you know you’ll be up late tonight. The All-Nighter drink has your back. It’s also simple and knows you don’t have the time to measure and bust out a ton of ingredients.

Ingredients:

Red Bull Energy Drink

1 shot of Captain Morgan’s spiced rum

1 shot of orange juice

5. The Home Wrecker – The day the inspection or appraisal kills the deal. You need something STRONG! Also called the Long Island Iced Tea, this is one of the strongest and most alcoholic drinks ever created. It’s also delicious. It also helps take away your anger, bitterness, and extreme sorrow!

Ingredients:

1 shot of vodka

1 shot of rum

1 shot of tequila

1 shot of gin

1 shot of triple sec

1 lemon wedge

Coke

Fill a cocktail shaker with ice and add the spirits and the juice from a squeezed lemon and shake like hell. Pour into a tall glass, add ice and slowly pour the coke on top of the ice. The less coke you add, the better you will feel.

6. The Double Agent Dance – This is when you’re acting as both the listing agent and buyer’s agent. You know you have a lot of work ahead of you, and that it requires a delicate dance. This drink is also known as The Dancing Goldfish.

Ingredients:

1 bottle of white wine (chardonnay or white zinfandel are best)

12 oz. of 7-Up

12 oz. Peach Schnapps

1 can of mandarin oranges

Over ice and in a large pitcher, pour in wine and peach schnapps. Stir in mandarin oranges and 7-Up. Serve in tall glass with ice and watch the fishes dance! Keep refilling to keep the fishes alive!

7. The Orgasm – When you’ve worked so long and so hard, and given all you can, and you finally get the satisfaction of a job well done. The build-up has been intense, and then… you get an OFFER! You explode with relief!! Also known as a Screaming Orgasm (if the offer was all cash or over asking)! There’s no better feeling in the world. 😉

Ingredients:

1 oz. Bailey’s

1 oz. Kahlua

1 oz. Vodka

1 oz. Amaretto

Makes one shot. Can be doubled for a Multiple Orgasm.

8. The Hail Mary – When you have a deal hanging by a thread and you need that one last burst of energy or negotiation super power to get the deal done. This is when you need your Hail Mary, also known as a Bloody Mary.

Ingredients:

1 ½ oz. vodka

3 oz. tomato juice

1 tbsp. lemon juice

½ tsp. worcestershire sauce

3 drops of tabasco sauce

½ tbsp. horseradish

salt, pepper

Mix everything together and pour into a tall glass. Garnish with lemon or lime wedge, celery stalk, green onion, pickled green bean, rotisserie chicken or anything you have laying around the kitchen.

9. The Superman – It’s closing day! You did your job, did it very well, and made it look easy. You finally got your hard-earned paycheck and saved the world for your client. You feel like a Superhero, and if this isn’t your drink of choice, then a beer will never taste better than after a closing! Cheers!

Ingredients:

1/2 oz Stoli Blueberi vodka

1/2 oz Absolut vanilla vodka

1/2 oz Bacardi white rum

1/2 oz Malibu coconut rum

1/2 oz Blue Curacao liqueur

1 1/2 oz pineapple juice

Cranberry Juice

Sprite

Fill shaker with ice and add all of the alcoholic ingredients and pineapple juice and shake till frothy. Pour mixture into a tall glass, then add a quick pour of Sprite and top with a splash of cranberry juice. This will layer red, white, and blue into the glass and will rejuvenate your super-hero powers!

10. Love Potion – When your happy clients refer you to a friend or family member and you get to start all over again, and your love for the wacky world of real estate is renewed.

Ingredients:

1 oz Grey Goose Vodka

1 oz amaretto almond liqueur

1 oz peach schnapps

1 oz orange juice

1 oz cranberry juice Pour ingredients into a shaker with ice, shake and serve on the rocks. Now get to work and go party!

Losing a listing can be a huge hit to a realtor’s psyche, reputation, and pocket book. It is common for a seller to switch real estate agents if their house does not sell in the time frame of the listing agreement. Sometimes the realtor does a poor job at marketing the property and other times the house is just overpriced. Neither situation was the case for Jason Bruce, a 34-year-old real estate salesman in Cincinnati. During a general inspection, Jason stepped out to the backyard to have a cigarette. “I only smoke when I’m drinking or if I’m stressed,” Jason claimed. “I had a showing across town and the inspector was taking forever. I thought I might have to push back my appointment, so I decided to rip a heater.”

According to the Cincinnati Fire Department, Jason flicked his cigarette into some native foliage that flowed into the wooden deck out back. After his smoke, Jason went upstairs and ended up having a lengthy conversation about the air conditioning unit with the inspector. “I had no idea what the hell he was even talking about. He went on for like an hour about the dirty filter or some sh** and before I knew it the den was in flames,” said Jason. The pair immediately called the fire department, but it was too late. The house burnt to the ground in less than two hours as the firemen managed to save the guest house. Nobody was injured. The seller has remained silent, but is taking legal action on Jason, who blamed the incident on the inspector. It is safe to say that Jason will not be getting an extension on the listing agreement.

A Movement Of Staunch Conservatives And Doomsday-Watchers To The Inland North-West Is Quietly Gaining Steam

ASKED by an out-of-stater where the nearest shooting range is, Patrick Leavitt, an affable gunsmith at Riverman Gun Works in Coeur d’Alene, says: “This is Idaho—you can shoot pretty much anywhere away from buildings.” That is one reason why the sparsely populated state is attracting a growing number of “political refugees” keen to slip free from bureaucrats in America’s liberal states, says James Wesley, Rawles (yes, with a comma), an author of bestselling survivalist novels. In a widely read manifesto posted in 2011 on his survivalblog.com, Mr Rawles, a former army intelligence officer, urged libertarian-leaning Christians and Jews to move to Idaho, Montana, Wyoming and a strip of eastern Oregon and Washington states, a haven he called the “American Redoubt”.

Thousands of families have answered the call, moving to what Mr Rawles calls America’s last big frontier and most easily defendable terrain. Were hordes of thirsty, hungry, panicked Americans to stream out of cities after, say, the collapse of the national grid, few looters would reach the mostly mountainous, forested and, in winter, bitterly cold Redoubt. Big cities are too far away. But the movement is driven by more than doomsday “redoubters”, eager to homestead on land with lots of water, fish, and big game nearby. The idea is also to bring in enough strongly conservative voters to keep out the regulatory creep smothering liberty in places like California, a state many redoubters disdainfully refer to as “the C-word”.

Estimates of the numbers moving into the Redoubt are sketchy, partly because many seek a low profile. Mr Rawles himself will not reveal which state he chose, not wanting to be overrun when “everything hits the fan”. But Chris Walsh of Revolutionary Realty says growing demand has turned into such a “massive upwelling” that he now sells about 140 properties a year in the north-western part of the Redoubt, its heart. To manage, Mr Walsh, a pilot, keeps several vehicles at landing strips to which he flies clients from his base near Coeur d’Alene.

Many seek properties served not with municipal water but with a well or stream, ideally both, just in case. More than nine out of every ten Revolutionary Realty clients either buy a home off the grid or plan to sever the connection and instead use firewood, propane and solar panels, often storing the photovoltaic power in big forklift batteries bought second-hand. They also plan to educate their children at home. The remoter land preferred by lots of “off-the-gridders” is often cheap. Revolutionary Realty sells sizeable plots for as little as $30,000. After that, settlers can mostly build as they please.

Lance Etche, a Floridian, recently moved his family into the Redoubt after the writings of Mr Rawles stirred in him “the old mountain-man independence spirit—take care of yourself and don’t complain.” He chose a plot near Canada outside Bonners Ferry, Idaho, cleared an area with a view, put down gravel, “and they dropped the thing [a so-called “skid house”, transported by lorry] right on top of it”, he says—no permit required.

Some newcomers are Democrats keen to get back to nature, grow organic food or, in Oregon and Washington, benefit from permissive marijuana laws. Not all conservatives dislike this as much as Bonny Dolly, a Bonners Ferry woman in her 60s who says: “We don’t want liberals, that’s for sure,” and carries a .45-calibre handgun “because they don’t make a .46”. But lefties who move in and hope to finance tighter regulations with higher taxes often get the cold shoulder. Mr Walsh weeds out lefties from the start, politely declining to show them property, noting that they wouldn’t fit in anyway. This discrimination is legal, he says, because political factions, unlike race or sexual orientation, are not legally protected classes.

A Red Dawn:

Todd Savage, who runs Survival Retreat Consulting in Sandpoint, Idaho, works with the more usual sort of client: political migrants who rail against “morally corrupt” nanny government elsewhere. He does a brisk business helping them set up their food-producing fortress-homesteads. Staff train clients in defensive landscaping, how to repel an assault on their property with firearms, and the erection of structures “hardened” to withstand forced entry and chemical, biological, radiological or explosive attack.

Very few redoubters, however, wish to secede from the United States. The Confederacy’s attempt fared badly, notes Mr Rawles. He did, however, exclude the politically conservative but mostly flat Dakotas from the Redoubt because mechanised units could manoeuvre easily there. The same went for swathes of Utah, a state also left out because it has little water.

Purists have criticized him for including eastern Oregon and Washington in the Redoubt, since their larger liberal populations near the west coast dominate state politics. But he believes that the designation will quicken efforts in the eastern reaches to form new, freedom-minded states within a generation. As Mr Walsh puts it, easterners’ taxes get them “nothing back except for a bunch more rules” from socialist bureaucrats.

As for doomsday itself, redoubters differ. Mr Rawles considers the most likely cause to be a geomagnetic solar storm like the Carrington Event in 1859, when a coronal mass ejection from the sun generated sparks in telegraph lines, setting some buildings on fire. Had the nearly 3,000 transformers that underpin America’s grid existed then, a quarter of them would have burned up, according to Storm Analysis Consultants in Duluth, Minnesota. Some redoubters have signed up to receive a National Oceanic and Atmospheric Administration alert of any approaching solar storm like the big one that blew across Earth’s path on July 23rd 2012, missing the planet by days.

Alternatively, a nuclear explosion 450km above the central United States would produce enough high-energy free electrons in the atmosphere below to fry the grid and unshielded electronics in all states except Alaska and Hawaii. Conceivably, and unpredictably, North Korea or Iran might dare to launch such a missile.

A more likely catastrophe, Mr Rawles believes, would be a pandemic virulent enough to cause the breakdown of the national sewerage system as well as the grid. Mr Savage, for his part, worries most about a “slow slide into socialism” akin to “death by a thousand cuts, right, you just keep whittling away at liberty” by, for example, restricting gun sales. Some of his firm’s clients fear that bankers may deliberately collapse the financial system in order to introduce a single global currency.

The dominant view is simply that institutions and infrastructure are more fragile than most believe, says Dave Westbrook, an American Redoubt consultant homesteading north-west of Sandpoint. Videos sold by his firm, Country Lifestyle Solutions, show redoubters how to assess the viability of off-grid properties, plant orchards and tend crops. But paranoia is out there, says Ben Ortize, the pastor of Grace Sandpoint Church. Terrorism, and the widespread belief that President Barack Obama’s progressive agenda is naive, have fuelled strong support for Donald Trump in the Redoubt, which has a disproportionately large population of former policemen, firemen and soldiers. To calm them down, he tells his flock that the Bible advises them to trust in the Lord, rather than in shotguns and Tasers.

The area’s bad rap is sometimes undeserved. “Hate in America: A Town on Fire”, a recent Discovery Channel broadcast about Kalispell, Montana, attempted to conflate gun-lovers who recoil at big government with the few white supremacists shown at the start. In fact, there is much less racism in the inland north-west than in the South, says Alex Barron, founder of the libertarian Charles Carroll Society blog and self-proclaimed “Bard of the American Redoubt”. Some are quick to label ideological opponents as white supremacists, he says. Liberal bloggers have called him one; but Mr Barron is black.

The Redoubt does give refuge to more than its fair share of outlaws, whether ageing draft-dodgers or crooks on the lam. So says Mike “Animal” Zook, a bounty hunter in Spirit Lake, Idaho with a gunslinger image enhanced by his sidearm’s faux-scrimshaw handle. Pointing east from the Riverman Gun Works car park, he notes that a man can trek that way for nearly 150 miles and see nothing but majestic forest and game. Turn south, and the wilderness extends more than double that.

Wanted men can and do disappear here, Mr Zook says. Some pan for gold, hunt, trap game and quietly slip into a town once a year or so for supplies. Nationwide, perhaps only one in 1,000 indicted felons skip bail and run for it, he says, but the percentage is higher in the Redoubt and especially in Lincoln County, in nearby north-western Montana. That provides enough work, he says, for more than 2,000 fugitive-recovery agents—as bounty hunters are also known—who, like himself, operate at least part-time, typically as private contractors for bondsmen in the Redoubt. All in all, the frontier spirit of America’s Old West is still alive and well.

The second installment of Cook County property tax bills were due August 1. That includes the city of Chicago, where property owners got their first taste of a record increase the city council passed last year. Some property owners are facing double-digit increases.

After paying the highest property taxes ever levied in the city, many Chicago homeowners had the same complaint.

“For the amount of taxes that my neighbors and myself are paying, we’re not getting the proper services like other neighborhoods get,” West Side resident Steve Lucas said.

That’s because the taxes are not paying for added services. The Chicago portion of the property tax bill – which was increased by nearly 70 percent -will pay for police and firefighter pensions and school construction. Add that to what’s become an annual hike in the CPS operating budget levy.

“Increased every year. (Every year they’re increasing?) Yes, every year,” North Side resident David Chang said.

“(00:15:35)We are much better off today than we were five years ago,” said Alexandra Holt, Chicago budget director.

At Chicago’s City Club, Holt said Chicago’s looming $137 million deficit looks a lot better than $654 million projected at this time five years ago. Mayor Rahm Emanuel said the city had no choice but to raise money for pensions to spare the operating budget.

“There is a real financial cost and economic cost to the city if you don’t address the problem,” Emanuel said.

Former Gov. Pat Quinn has a petition drive underway to appoint a consumer advocate to help homeowners appeal their tax charges.

“The best way to do it is at the ballot box by gathering signatures on petitions like this one,” said former Illinois Gov. Pat Quinn.

The city has scheduled three more tax increases for police and fire pensions and still has not addressed a deficit in the retirement fund for city workers, not to mention a newly-authorized property tax hike to pay for teacher pensions.

“The city says they might have to go up again. Yes, and I might not be able to stay where I’m staying. I’ve been there 40 years and I don’t know if I can stay any longer,” South Chicago resident Doris Hood said.

The city council has approved a plan to rebate a few hundred dollars to the lowest-income homeowners if they apply. It should also be noted that the Chicago School Board is expected to approve a $250 million property tax increase for teacher pensions at its meeting later this month.

Chicago Property Taxes To Increase By 12.8 Percent

The Cook County Clerk’s office released the 2015 property tax rates on Monday for the entire county. While the northern and southern suburbs of Cook County can expect a slight tax bill increase of 1.7 percent and 2.1 percent, respectively, Chicago’s property tax bills will rise by 12.8 percent.

According to the Clerk’s office, citizens of Chicago who paid an average tax bill of $3,220.32 in 2014, will pay an average of $3,633.19 on their 2015 bills, an increase of $412.87.

Cook County property taxes are paid in arrears, meaning the bill for 2015 is paid during 2016.

The Clerk’s office says that this substantial increase is due the city being reassessed in 2015, which resulted in a 9.3 percent increase in the equalized assessed value citywide. The equalized assessed value, or EAV, is a multiplier used in calculating property taxes to bring the total assessed value of all properties in Cook County to a level that is equal to 33.3 percent of the total market value of all the real estate in the county.

The Clerk’s office is quick to note that a majority of Chicago’s tax increase is due to the city increasing the pension portion of its levy by $318 million. As a result of the reassessment, the Clerk’s office says the city tax rate actually increased less than one percent compared to 2014.

Cook County is divided into three areas, Chicago, northern suburbs, and southern suburbs, which are reassessed every three years. The southern suburbs were reassessed in 2014. Chicago was reassessed in 2015. The northern suburbs will be reassessed in 2016.

Tax bills for Cook County property owners are due August 1, 2016.

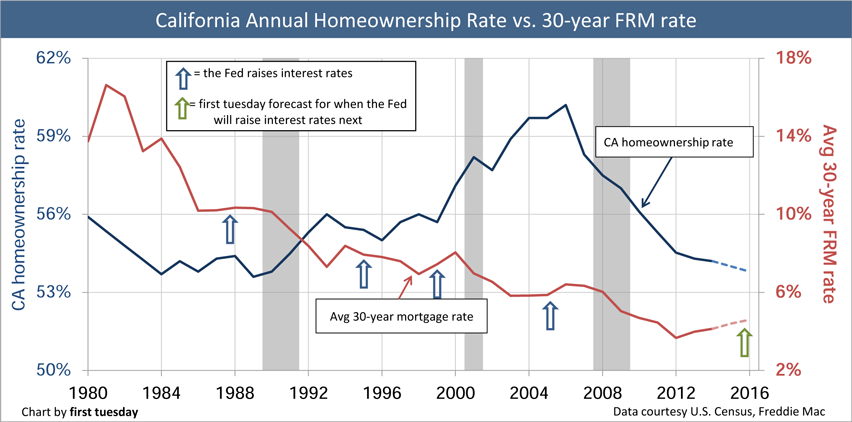

The national average 30-year fixed home mortgage rate in the U.S. recently fell to 3.36 percent, matching the record low first reached in December 2012, according to Bankrate.com. Would-be home-buyers and homeowners looking to refinance existing mortgages at lower rates have benefited from a drop in U.S. Treasury yields since U.K. voters decided in June to leave the European Union. A comparable Freddie Mac mortgage gauge watched by the industry is near a record low, at 3.48 percent.

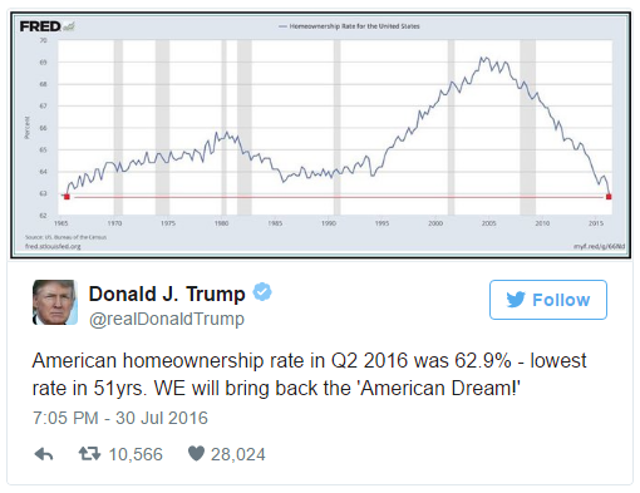

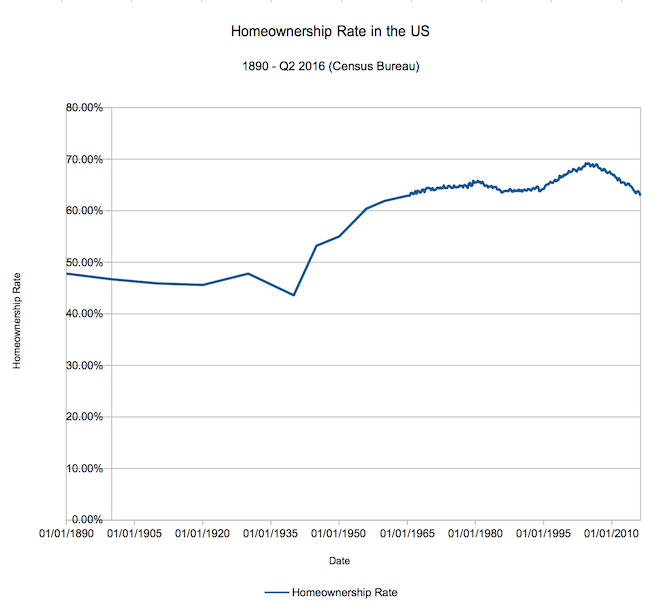

As you probably assumed anyway, due to Betteridge’s Law, we aren’t currently in a homeownership trough. The recent homeownership rate posting of 62.9% for the second quarter of 2016 is not the lowest in history, nor is it even the lowest in recorded US history. However, it is the lowest post in 51 years(!) – not since the third quarter of 1965 have we seen homeownership rates this low.

And why are we at DQYDJ bothering to look now?

Donald Trump, the Republican nominee for President sent this Tweet a couple days back:

The History of the Home Ownership Rate

A while back, we did a two-part deep dive into the history of the 30 year mortgage and the history of the (recorded) home ownership rate in America. That research dug up some very interesting information.

First, long-dated mortgages of 15, 20 and longer years started in the mid 1930s. Second, private mortgage insurance (which was mostly done in by the Great Depression) started up in 1957 with the Mortgage Guaranty Insurance Company.

Those innovations brought homeownership to the masses – no longer did you have to be able to afford a huge, short-term loan with a massive down payment. Extending Mr. Trump’s graph back to 1890 you can see the effect of the innovations (and of the Great Depression and Recession) on homeownership rates:

(Note that until the 60s there wasn’t as much resolution in the series – see our historical research for details).

The longer dated series lets us state a few interesting facts:

The lowest homeownership rate since 1957’s PMI innovation was a 61.9% rate in 1960.

The lowest homeownership recorded since 1890 was 43.6% in 1940 – in the midst of the Great Depression.

Why Is the Home Ownership Rate Dipping?

Oh, you won’t accept ‘people are renting more’ as an answer?

Yes, the run up in real estate prices in many areas of the country (so soon after the Great Recession!) is a huge factor. But, so too are the massive demographic changes underway in our country.

As we have pointed out many times, the millennials (of which I count myself as an older member) now makeup roughly 25% of the workforce. Millennials have different living arrangements than past generations – a greater propensity to live at home, a seeming desire to be free to change jobs (and areas!) more often, and, yes, more expensive housing options. That last point, of course, prices many millennials out of the market – renting makes much more sense when you look at the home prices in many metros in the United States.

Can It Change? Will We See the Rate Rise Again?

Yes – as of right now, I don’t see the drive towards renting (and living at home) to be a sort of permanent desire. Already there are countering trends – the so-called “Tiny House” movement one of them (and, yes, I have been searching for a place to name-drop it!). It’s safest, at this point in time, to assume millennials will tend to be similar to their parents – eventually leaving the city to marry, have kids and buy homes. You know, like yours truly.

However, we’re looking into the future here. Marriage is trending towards being an institution for older and older couples, along with kids. If these trends keep up, we might start to get into uncharted territory here – I’d love your input on whether you think homeownership rates will recover, or high-60s was an anachronism.

Will we see an increase in homeownership led by the millennials?

Condos along Vancouver’s waterfront. (Photo: Getty Images)

Summary

U.S. investors betting on an epic U.S. style housing bust occurring in Canada have been doing so for a considerable period with no clear proof.

Claims of a broad-economy wide housing bubble that is ready to burst are significantly overstated with no clear evidence that a bubble exists.

The majority of price growth is coming from Vancouver and Toronto and there are specific reasons supporting higher prices in those markets.

The conditions in Canada’s housing market are strikingly different compared to those that existed in the U.S. during the lead-up to the 2007 housing meltdown.

It appears that ‘group think‘, ignorance and cognitive dissonance have come to dominate the argument around whether Canada’s housing market is in bubble territory and poised to burst sometime soon. Struggling U.S. hedge funds, many of which missed out on the ‘big short‘ of book and movie fame, have been betting heavily on an epic Canadian housing meltdown by shorting Canada’s major banks, but to date have incurred considerable losses.

Then you have the chorus of economists, analysts and investors who have been claiming that not only has a massive real estate bubble formed in Canada but that it is poised to burst. In many cases, these proclamations go back as far as 2009 and despite being reiterated by naysayers now for close on seven years, a housing bust has yet to occur. Many including acclaimed investor Canada’s own Prem Watsa have stated that Canada’s housing market resembles that which existed in the U.S. during the run-up to the subprime crisis.

These claims rest upon a broad-range of assertions that a number of one-off, disruptive and unsustainable factors are driving Canadian housing prices ever higher, creating the perfect storm that will cause the bubble to burst in a spectacular manner. These claims, many of which have been voiced for some years now, include:substantial amounts of foreign (read Asian) investment;

lax lending standards;

large volumes of subprime mortgages;

growing financial stress being placed on households; and

the growing risk of external economic shocks.

However, it appears that many investors, particularly those based in the U.S. are ignoring the fundamental differences between the two markets and local attributes that will not only prevent an epic meltdown but backstop prices for some time to come. Let’s take a detailed look at some of the major myths that are regularly wheeled out by those who claim that a massive housing bubble exists in Canada and is poised to burst any time.

#1 There is a massive economy wide housing bubble

One of the main drivers of the massive U.S. housing meltdown was that frothy prices were not restricted to specific regional markets or segments but instead constituted an economy-wide housing bubble that was highly speculative in nature. And the risk that this posed to the U.S. financial system and economy was magnified by the prevalence of non-traditional and substandard lending practices as well as considerable volumes of inferior mortgage backed securities.

Yet in the case of Canada, overheated or bubbly housing markets are restricted to a small number of regional markets and market segments, with the growth of housing prices either slowing or falling across other regions. By the end of June 2016 it was only a handful of markets including Toronto, Vancouver and Hamilton-Burlington that experienced double-digit growth.

In fact, it was the considerable increase of house prices in those markets which for June rose by 16.8%, 11.4% and 14.2% year-over-year respectively, which was responsible for the Canadian national average growing by 11%. Other regional markets such as New Brunswick and Quebec grew at more modest rates of around 3%, whereas Novia Scotia remained flat. Then you have Alberta and Saskatchewan, which are among the most affected by the prolonged slump in crude, where house prices fell by 1.4% and 1.6% respectively.

It is these points which indicate that Canada’s housing market on whole, is starting to cool with the growth in the national average house price predominantly being driven by Toronto and Vancouver. This does not necessarily mean that either of those housing markets have entered bubbles with a range of market specific dynamics responsible for the ongoing price growth.

#2 A massive influx of foreign investment is responsible for higher housing prices

Probably one of the biggest myths regularly bandied about by those that claim the market is in rarefied bubble territory and ready to burst, is that the tremendous inflow of foreign investment, particularly from China, is driving prices to unrealistic levels, particularly in Toronto and Vancouver. While it is certainly undeniable that these markets are attracting considerable amounts of attention from foreign investors this is not the only or most important factor in causing prices to surge in those markets.

Even naysayers such as Capital Economics economist Paul Ashworth believes that surging house prices are not being caused by foreign investment but rather by Canadians taking advantage of cheap credit and relaxed lending standards.

In fact, according to a range of reports and research conducted by a number of economists there is very little evidence to support the assertion that foreign money is driving up housing prices. According to an article from Canada’s National Post earlier this year, vacancy rates in Vancouver are on average 2% which then increases to 7.5% for condos, with very few of those vacant properties being foreign owned. The same article goes onto state that it is the laws of supply and demand that are responsible for higher housing prices rather than foreign money.

Recent data from the B.C. government shows that between June 10 and June 29 only 3.3% of all real estate deals in Vancouver involved foreign nationals and as a share of sales by value they only amounted to 5.1% of all sales. This is a far cry from the figures to be expected from a market where foreign money is responsible driving property prices into a bubble.

Indeed, if we take a closer look at the property markets of Vancouver and Toronto it is possible to identify specific market dynamics that are responsible for higher prices and these factors will continue to push them higher for some time to come.

#3 Toronto and Vancouver are in bubble territory

According to the naysayers, Canada’s housing market is now truly defying common sense and that a colossal housing crash is on its way, with the housing markets in Vancouver and Toronto caught in massive bubbles. This they claim is supported by factors such as Canada being judged to have the most overvalued housing market among developed economies and that global investors are increasingly betting against Canadian housing in record numbers.

Nonetheless, there are also a range of factors that indicate that these claims are alarmist and inaccurate, with no evidence to support the view that housing bubbles exit in either market. Will Dunning, chief economist of industry group Mortgage Professionals Canada, believes that prices are sustainable and not representative of a property bubble, stating that this talk has been going on since 2008 with no evidence of one existing. He even went on to state:

Housing bubbles do not exist in Canada, . . .

If we turn to what defines an economic or market bubble it becomes apparent that Dunning could certainly be right. For a housing bubble to exist people have to be buying houses for purely speculative reasons and this has to be across a considerable portion of the market. Then to illustrate that a bubble exists there has to be expectations of self-fulfilling price growth and that those unrealistic expectations are leading to increased and excessive activity in the housing market.

The theories postulated by Nobel award winning economist Joseph Stiglitz also supports these notions, he defines a bubble as where the reason that the price is high today, is only because investors believe that the selling price will be higher tomorrow.

None of these factors in their entirety apply to Canada’s housing market nor those of Vancouver or Toronto. If anything it is far more mundane market specific factors that are driving housing prices ever higher. A group of academics from the University of British Colombia while proposing placing a tax on vacant properties in order to reduce the level of foreign investment in Vancouver have stated that the fundamental drivers of higher prices are higher demand and limited supply. Upon taking a closer look at the markets of Vancouver and Toronto this becomes very apparent.

You see, Toronto and Vancouver are defined as global gateway cities that sees them cast in the same light as global cities such as London, New York, Paris and Hong Kong that have far more expensive real estate markets. This makes them important destinations for immigrants, with them accepting around half of all external immigrants to Canada.

The reasons for this are predominantly economic with both cities, particularly because of the prolonged slump in oil prices, have the greatest concentration of jobs in Canada, with around 25% of total employment in Canada. And according to economists’ from Bank of Montreal these two cities accounted for all of Canada’s job growth in 2015.

It is these factors which according to National Bank economist Stefane Marion are responsible for the working age population in Toronto and Vancouver to be growing at a rate that is 70% faster than the national average.

The prolonged slump in oil has magnified this phenomenon, with the deep economic slump in Canada’s oil patch significantly impacting the economies of Alberta and Saskatchewan. This has not only made those regions less appealing to immigrants but triggered a marked uptick in the number of households seeking to relocate because of higher unemployment and falling wages.

Meanwhile, The Economist has theorized that this rapidly growing demand is placing considerable pressure on housing supplies particularly because of their unchanging supplies, stating:

The supply of housing is rather inelastic, so in the short term house-price inflation is driven more by demand factors, such as the number of households, disposable income, interest rates and the yield available on other assets. In recent years all of these have helped to push house prices steadily upwards, especially in big cities.

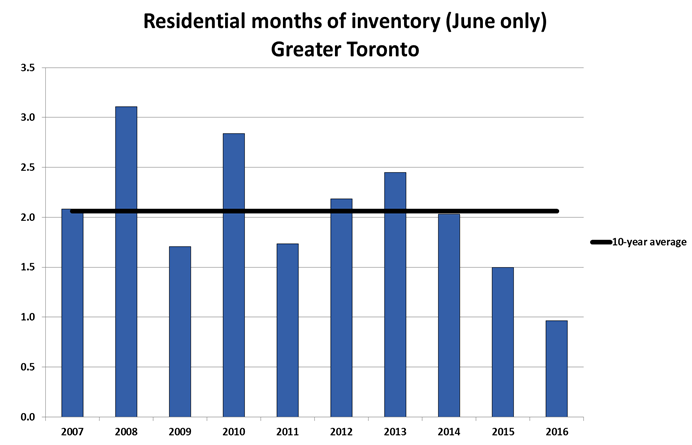

The constrained supply situation caused by limited inventories in both cities is easy to see. As the chart below illustrates, Toronto’s housing inventory by June of this year was at less than half of its 10 year average and a third lower than the previous year.

Source: Canadian Real Estate Association.

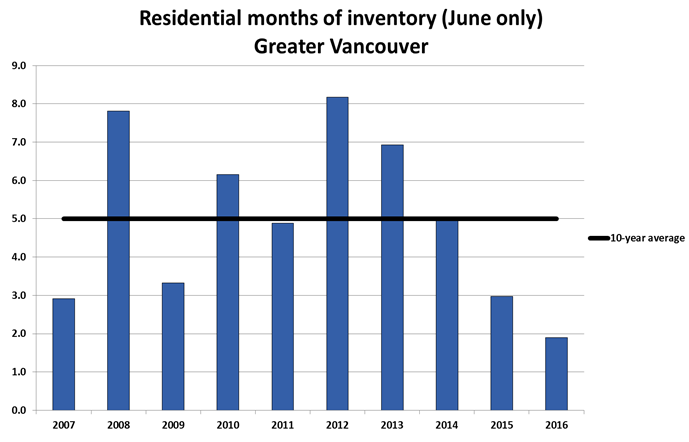

When turning to Vancouver it is possible to see that for the same period inventories are around 60% lower than the 10 year average and a third lower than a year earlier.

Source: Canadian Real Estate Association.

With expanding populations, driven by growing internal and external migration, causing demand to swell coupled with extremely limited housing supplies in Toronto and Vancouver there is considerable support for higher prices, which means there won’t a correction in those markets anytime soon.

#3 The Conditions in Canada are similar to those in the U.S. prior to the financial crisis

One of the biggest myths concerning Canada’s housing market is that the conditions that exist are similar to, if not the same as those that existed in the U.S. in the lead-up to the massive housing meltdown that almost caused the U.S. financial system to collapse in 2007.

. . rising levels of Canadian household debt relative to income, along with rapidly increasing house prices, have created conditions similar to those in the United States prior to the financial crisis of 2008.

Then there is Steve Eismann who rose to fame betting against the U.S. housing market in the lead-up to the subprime crisis. He is making similar claims to Moody’s but was doing so way back in 2013 and has been recommending that investors bet against Canada’s mortgages lenders and banks.

It is this which has attracted the attention of short-sellers and now sees Toronto-Dominion Bank (NYSE:TD) and Bank of Nova Scotia (NYSE:BNS) being the first and third most shorted stocks on the TSX.

However, there are a range of reasons why Canada is not a repeat of what was occurring in the U.S. back in 2006, key among these is far higher underwriting standards for loans and a distinct lack of subprime mortgages.

It appeared that way back in 2006, anyone with a pulse could obtain a mortgage with mortgage underwriting standards relaxed to levels that were ridiculously low. Then there was the huge influx of fraudulent applications and an extremely lax approach to checking applications for accuracy. This easy money helped to fuel ever rising house prices and give a leg up to the next round of frenzied speculation. No one, from mortgage brokers, to the major banks wanted the merry-go-round to end as they all sort to cash in on the growing frenzy.

Clearly, Canada has not reached this stage yet and in fact it is doubtful that it ever well, with its property market certainly not caught in the same type of speculative frenzy.

Furthermore, it was the presence of considerable volumes of subprime mortgages that essentially precipitated the U.S. housing meltdown. It is estimated that they made up somewhere between 18% and 21% of all mortgages originated in the run-up to the housing crash. Whereas, in Canada subprime mortgages are estimated to make-up less than 5% of the market, and that was when the market was at its peak. With Bank of Canada pushing for tighter mortgage underwriting standards since this figure was released, it will certainly have fallen.

Aside from these key differences there are also a range of other Canada specific factors to consider including:

the lack of non-recourse mortgages, a greater prevalence of mortgage insurance;

the fact that borrowers on average have higher levels of equity in their homes; and

lower loan-to-valuation ratios for non-insured mortgages.

As a result, these differences mean that the market is not exposed to the same degree of risk nor the same volume of rapid defaults that forced U.S. lenders in 2006 and 2007 to flip repossessed properties as quickly as possible, causing prices to cascade ever lower.

Final musings

The differences between Canada’s housing market and that which existed in the U.S. in the run-up to the housing meltdown, which almost caused the U.S. financial system to collapse, are strikingly important. They highlight that not only is a sharp correction or housing meltdown unlikely but that in marked contrast to the claims of naysayers that there is in fact no evidence of a housing bubble. If anything while some regional markets are cooling, Vancouver and Toronto’s ever higher housing prices can be attributed to demographic pressures, higher demand and constrained supply. These factors will push prices higher in those markets for some time to come and backstop prices if there is a sharp economic downturn. For all of these reasons it is difficult to envision an epic Canadian housing meltdown occurring any time soon.

Houston lost its locally famous Bullock-City Federation Mansion in 2014 to a developer who plans to erect townhouses on the site.

The house may not have been worthy of a place on a list of historically significant structures. But the 5,000-square-foot structure that was erected in 1906 on a 30,000-square-foot lot was the first in the sweltering Texas city to have air conditioning. And its demise was mourned by more than a few people.

“It’s a beautiful building,” Ernesto Aguilar, general manager of KPFT Radio, which sits next door, told the Houston Chronicle at the time. “It is sad to see a piece of Houston history going the same way as many others do.”

Tear downs — in which builders or private individuals purchase an aging, outmoded house, then demolish it and replace it with a modern home that will suit today’s homeowners — are currently on a tear in Houston. Permits for tear downs are up by 22% in the city this year.

And that phenomenon isn’t limited to Houston. Barry Sulphor, a real estate agent in the Los Angeles area, counts no less than 100 tear down sites in the so-called beach cities where he plies his trade: Hermosa Beach, Redonda Beach and Manhattan Beach. “And I’m sure there are just as many in Venice, Santa Monica and Beverly Hills,” Sulphor says.

According to the National Association of Home Builders’ best count, nearly 8% of all single-family housing starts in 2015 were attributable to tear down-related construction. That’s roughly 55,000 older houses gone forever, and that’s on top of the 31,800 single-family tear down starts in 2014.

In some instances, the houses that are destroyed are outmoded, functionally obsolete relics that no longer serve a useful purpose. But in other cases, they work just fine and simply lack up-to-date amenities. And some have historical significance that may or may not be worthy of saving.

Usually, the places that replace a tear down are larger, covering more of the lot and rising higher than the old place — often to the maximum height allowable under local zoning rules.

Sulphor recently sold two lots where the old houses were taken down. One was bought for $1.35 million by a builder who plans to put up a house with a nearly $4 million price tag. The other was purchased for $2.15 million by a retired couple who “love the creativity of working with architects to design luxury beach properties,” according to Sulphor. “When the new place is completed, it will fetch close to $5 million.”

Not everyone sees the benefit of tear downs. The leading opponent is the National Trust for Historic Preservation, which argues that they are an “epidemic” that is “wiping out historic neighborhoods one house at a time. As older homes are demolished and replaced with dramatically larger, out-of-scale new structures, the historic character of the existing neighborhood is changed forever.”

Richard Moe, a former president of the National Trust, said, “From 19th-century Victorian to 1920s bungalows, the architecture of America’s historic neighborhoods reflects the character of our communities. Tear downs radically change the fabric of a community. Without proper safeguards, historic neighborhoods will lose the identities that drew residents to put down roots in the first place.”

But the NAHB, which admits that tear downs “have become a significant modus operandi” for its members in some parts of the country, counters that the new houses often “breathe new life into older communities.”

Because tea rdowns are sometimes controversial, folks considering buying an older place with the idea of taking it down and putting up a new house should proceed cautiously. Often, these old homes are not advertised for sale on the open market or in the multiple listing service, so the challenge begins with finding out about one, says Sulphor. And once you do, the agent suggests making absolutely sure the condition of the current home is such that it cannot be salvaged.

Would-be buyers should also determine, before making an offer, whether what they plan to build conforms to local restrictions. Preservationists often use — or try to change — local building codes to push back against tear downs.

On the other hand, people trying to sell old properties that are tear down candidates should make sure whatever offers they receive are legit, Sulphor advises. Look for the proof that they have the funds to close the deal, especially if they say they will pay with cash and have no need of a mortgage.

Sellers should also realize that selling a property “as-is” does not insulate them from their obligation to disclose any issues that might impact value. The term “as-is” means only that the house is being offered and sold in its present condition.

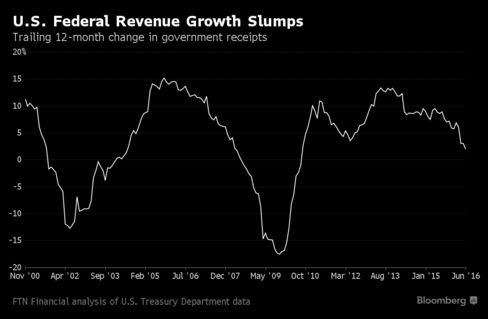

Net issuance seen rising after steady declines since 2009

Fed seen adding to supply as Treasury ramps up debt sales

Negative yields. Political risk. The Fed. Now add the U.S. deficit to the list of worries to keep beleaguered bond investors up at night.

Since peaking at $1.4 trillion in 2009, the budget deficit has plunged amid government spending cuts and a rebound in tax receipts. But now, America’s borrowing needs are rising once again as a lackluster economy slows revenue growth to a six-year low, data compiled by FTN Financial show. That in turn will pressure the U.S. to sell more Treasuries to bridge the funding gap.

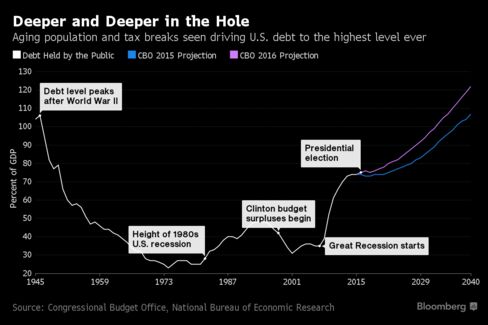

No one predicts an immediate jump in issuance, or a surge in bond yields. But just about everyone agrees that without drastic changes to America’s finances, the government will have to ramp up its borrowing in a big way in the years to come. After a $96 billion increase in the deficit this fiscal year, the U.S. will go deeper and deeper into the red to pay for Social Security and Medicare, projections from the Congressional Budget Office show. The public debt burden could swell by almost $10 trillion in the coming decade as a result.

All the extra supply may ultimately push up Treasury yields and expose holders to losses. And it may come when the Federal Reserve starts to unwind its own holdings — the biggest source of demand since the financial crisis.

“It’s looking like we are at the end of the line,” when it comes to declining issuance of debt that matures in more than a year, said Michael Cloherty, head of U.S. interest-rate strategy at RBC Capital Markets, one of 23 dealers that bid at Treasury debt auctions. “We have deficits that are going to run higher, and at some point, a Fed that will start allowing its Treasury securities to mature.”

After the U.S. borrowed heavily in the wake of the financial crisis to bail out the banks and revive the economy, net issuance of Treasuries has steadily declined as budget shortfalls narrowed. In the year that ended September, the government sold $560 billion of Treasuries on a net basis, the least since 2007, data compiled by Bloomberg show.

Coupled with increased buying from the Fed, foreign central banks and investors seeking low-risk assets, yields on Treasuries have tumbled even as the overall size of the market ballooned to $13.4 trillion. For the 10-year note, yields hit a record 1.318 percent this month. They were 1.57 percent today. Before the crisis erupted, investors demanded more than 4 percent.

Net Issuance of U.S. Treasuries, Fiscal-Year Basis

One reason the U.S. may ultimately have to boost borrowing is paltry revenue growth, said Jim Vogel, FTN’s head of interest-rate strategy.

With the economy forecast to grow only about 2 percent a year for the foreseeable future as Americans save more and spend less, there just won’t enough tax revenue to cover the burgeoning costs of programs for the elderly and poor. Those funding issues will ultimately supersede worries about Fed policy, regardless of who ends up in the White House come January.

As a percentage of the gross domestic product, revenue will remain flat in the coming decade as spending rises, CBO forecasts show. That will increase the deficit from 2.9 percent this fiscal year to almost 5 percent by 2026.

“As the Fed recedes a little bit into the background, all of these other questions need to start coming back into the foreground,” Vogel said.

The potential for a glut in Treasuries is emerging as some measures show buyers aren’t giving themselves any margin of safety. A valuation tool called the term premium stands at minus 0.56 percentage point for 10-year notes. As the name implies, the term premium should normally be positive and has been for almost all of the past 50 years. But in 2016, it’s turned into a discount.

Some of the highest-profile players are already sounding the alarm. Jeffrey Gundlach, who oversees more than $100 billion at DoubleLine Capital, warned of a “mass psychosis” among investors piling into debt securities with ultra-low yields. Bill Gross of Janus Capital Group Inc. compared the sky-high prices in the global bond market to a “supernova that will explode one day.”

Despite the increase in supply, things like the gloomy outlook for global growth, an aging U.S. society and more than $9 trillion of negative-yielding bonds will conspire to keep Treasuries in demand, says Jeffrey Rosenberg, BlackRock Inc.’s chief investment strategist for fixed income.

What’s more, the Treasury is likely to fund much of the deficit in the immediate future by boosting sales of T-bills, which mature in a year or less, rather than longer-term debt like notes or bonds.

“We don’t have any other choice — if we’re going to increase the budget deficits, they have to be funded” with more debt, Rosenberg said. But, “in today’s environment, you’re seeing the potential for higher supply in an environment that is profoundly lacking supply of risk-free assets.”

Deutsche Bank AG also says the long-term fiscal outlook hinges more on who controls Congress. And if the Republicans, who hold both the House and Senate, retain control in November, it’s more likely future deficits will come in lower than forecast, based on the firm’s historical analysis.

FED HOLDINGS OF TREASURIES COMING DUE

2016 ────────────── $216 BILLION

2017 ────────────── $197 BILLION

2018 ────────────── $410 BILLION

2019 ────────────── $338 BILLION

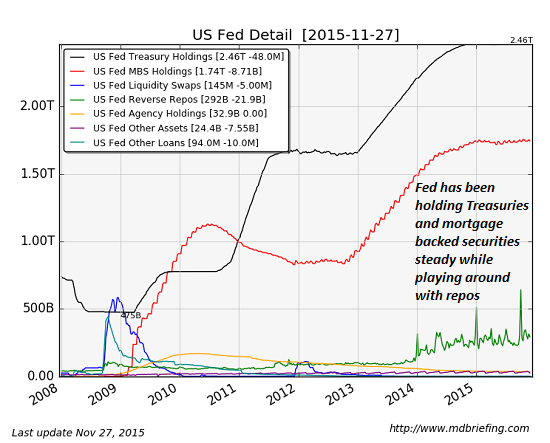

However things turn out this election year, what the Fed does with its $2.46 trillion of Treasuries may ultimately prove to be most important of all for investors. Since the Fed ended quantitative easing in 2014, the central bank has maintained its holdings by reinvesting the money from maturing debt into Treasuries. The Fed will plow back about $216 billion this year and reinvest $197 billion in the next, based on current policy.

While the Fed has said it will look to reduce its holdings eventually by scaling back re-investments when bonds come due, it hasn’t announced any timetable for doing so.

“It’s the elephant in the room,” said Dov Zigler, a financial markets economist at Bank of Nova Scotia. “What will the Fed’s role be and how large will its participation be in the Treasury market next year and the year after?”

Homes are selling an average of a week faster than they did a year ago, meaning home shoppers should be prepared to move quickly in a competitive housing market, according to the June Zillow Real Estate Market Report.

Tight inventory continues to be a major factor for home shoppers. The supply of homes for sale is nearly 5 percent lower than it was a year ago, and 38 percent lower than its peak level in 2011. With fewer available options, home shoppers are moving quickly to buy homes, with the average U.S. home closing after 78 days on the market.

The 78-day average includes the time it takes to close, which is usually one or two months after the home goes under contract. This means that homes are pending within about a month of being listed.

The length of time homes stay on the market before selling has been steadily decreasing since 2010, when homes took an average of five months to sell. The average time home buyers had in Pittsburgh, Philadelphia and Charlotte, N.C. dropped by at least two weeks, the biggest change among the largest U.S. metros.

The low inventory and quick-moving market combine to create a competitive home shopping market, especially for potential buyers looking for less expensive homes. The most expensive third of the market has experienced the smallest drop in available inventory compared to the rest of the market.

“Homes are selling faster than ever as the home shopping season hits its peak,” said Zillow Chief Economist Dr. Svenja Gudell. “If you’re looking for a home, be prepared to move quickly. Adding to this difficult buying environment is low inventory—there simply aren’t many homes to choose from. And while this looks like a good time to be a seller, potential move-up buyers may hesitate to list their homes and become buyers. Until the supply increases, it will remain a tough market to find a home.”

Confidential briefing for CRA auditors outlines strategy to tackle suspected tax cheats who do not report global income or who ‘flip’ homes – but reveals that last year, there was only one successful audit of global income for all of British Columbia

A backhoe destroys a C$6 million mansion in Vancouver’s Shaughnessy neighbourhood this year. The destruction of the well-kept home prompted community outrage and was cited in a briefing for Canadian tax auditors looking into Vancouver real estate transactions. Photo: Twitter / @DeborahAMG

A secret strategy briefing for Canada Revenue Agency auditors has revealed plans to crack down on real estate tax cheats in Vancouver, with 50 auditors being assigned to investigate purchases funded by unreported foreign income.

Presentation notes for the seminar, delivered to auditors on June 2 and leaked to the South China Morning Post, show that only one successful audit of worldwide income was conducted in British Columbia in the past year, in spite of Vancouver’s reputation as a hotspot for immigrant “astronaut families” whose breadwinners often work in mainland China and Hong Kong.

The plans, which come amid a furore over the role of Chinese money in Vancouver’s runaway housing market, were provided by a Canada Revenue Agency employee who attended the June 2 briefing. The briefing is identified as a “protected B” confidential document on the cover.

The cover for a confidential CRA briefing for auditors. Photo: SCMP Pictures

But the employee feared the sweep would prove inadequate. “Sure, they’ve upped the numbers because it’s hitting the papers,” they said. But on average, they estimated, each redeployed income auditor would only be able to conduct 10 to 12 audits per year – about 500 or 600 in total. “This is nothing,” compared to the likely scale of the cheating, they said.

Confidential briefing notes for CRA auditors reveal how the Canadian tax agency is targeting unreported global income and other issues related to real estate sales in the Vancouver region. Photo: SCMP Pictures

That estimate is in keeping with the briefing text which says the crackdown will “review the top 500 highest risk files within our region”.

The briefing lists four areas being targeted for audit under the CRA’s “real estate projects”, launched in response to “significant media attention”: unreported worldwide income, property “flipping”, under-reporting of capital gains from home sales, and under-reporting of Goods and Services Tax (GST) on sales of new homes.

‘High-end homes, minimal income’

The time-consuming global income audits will tackle “individuals living in high-valued areas in BC who are reporting minimal income not supporting their lifestyle”, as well as those who buy “high-end homes with minimal income being reported.”

The supposed case of a C$5.8 million home bought by someone who claimed a tax break intended for the poor is cited in the CRA briefing. Photo: SCMP Pictures

The presentation includes a photo of a luxury home supposedly bought for C$5.8million whose owner claimed the “working income tax benefit” for low earners. It also lists the tuition fees of Vancouver private schools.

Confidential briefing notes for CRA auditors show that 50 income tax auditors are being redeployed to tackle real estate cheats in BC. Photo: SCMP Pictures

Property flippers who swiftly resell homes for profit will meanwhile be audited to see if their properties truly qualify for exemption from capital gains tax, granted to people selling their principal residence.

The briefing describes various excuses given by owners who moved out of newly purchased homes, including a negative feng shui report, the “bad omen” of tripping over a crack in the sidewalk, and a painter dying in the home.

It cites the highly publicized case of a well-kept 20-year-old, C$6million mansion that was simply torn down after being bought, prompting community outrage.

Yes, we are getting a response now, but the government has known about this issue for a few years. They held back

CRA employee

The briefing does not say the owners of this home, or the $5.8 million home, are tax cheats and nor does the SCMP suggest so.

The CRA employee said the briefing, which was streamed online, was delivered by CRA’s Pacific region business intelligence director, Mal Gill.

The CRA briefing lists various excuses given by people who moved out of new homes, apparently claimed as principal residences. Photo: SCMP Pictures

Gill declined to discuss the briefing. “I cannot confirm anything to you,” he said, referring the SCMP to a CRA communications manager.

The case of a well-kept C$6million Vancouver home that was simply demolished after purchase is cited in leaked notes for Canadian tax auditors. Photo: SCMP Pictures

A spokeswoman said: “The CRA cannot comment or release information related to risk assessment or non-compliance strategies.”

However, she said real estate transactions in Toronto have been the subject of greater scrutiny, for some years. “More recently, the CRA has been actively monitoring and auditing real estate transactions in British Columbia,” she said.

“For the year ending March 31, 2016, the CRA completed 2,203 files [in BC and Ontario] related to real estate,” she said.

In addition to the 50 redeployed income auditors, the leaked briefing says CRA is assigning 20 GST auditors and 15 other staff to the real estate project in BC.

The CRA source said they leaked the material because, “like many people, I’m pretty disgusted by what’s happening here [in the Vancouver real estate market], and a lack of enforcement has been a part of the problem. Yes, we are getting a response now, but the government has known about this issue for a few years. They held back.”

The CRA briefing reveals that there was just one successful audit conducted on unreported global income in BC last fiscal year. Photo: SCMP Pictures

The employee said they were surprised to discover that only one successful audit of global income had been conducted in BC in the year to March 31. “That’s the ludicrousness of this. I was shocked when I saw this, and they only got C$27,000 in tax revenue out of it,” they said.

Asked whether this might show a widespread problem with undeclared worldwide income did not exist in BC, the source said: “No, what it shows is that inadequate people and resources have been put to the task. These [tax cheats] are highly sophisticated individuals, with good representation from their lawyers and accountants, and we are sending out our least experienced people to catch them. That’s the problem.”

Source cites CRA’s ‘racism fear’

Census data from 2011 has previously shown that 25,000 households in the City of Vancouver spent more on their housing costs than their entire declared income, with these representing 9.5 per cent of all households.

But far from being impoverished, such households were concentrated in some of the city’s most expensive neighborhoods, where homes sell for multi-million-dollar prices.

The source suggested CRA bureaucrats previously feared being labelled racist if they targeted low-income declarers buying real estate “because the vast majority of these cases, involving high real estate values, involve mainland Chinese”.

The crackdown was not intended for public knowledge, and instead was to satisfy “people from high up” in the CRA and government who wanted to know “what are you guys doing about this…there’s stuff hitting the papers every day”, the source said. Yet the briefing says the crackdown “will not address the major concerns about affordability of real estate”.

“The vast majority of these [undeclared global income] cases, involving high real estate values, involve mainland Chinese”

CRA employee

The source said there had previously been little done to check whether taxpayers were secretly living and working abroad while supporting a family in Vancouver. “There’s virtually no liaising done with immigration. The common auditor would never check when people are actually coming and going, to check whether they might be going back to China or wherever to work. You can be lied to, to your face: ‘Oh no, I live here [in Canada] full-time’.”

The leaked documents show that in in addition to the single audit on global income in the last fiscal year, CRA in BC conducted 93 successful audits on property flips, 20 on capital gains tax and 225 on under-reported GST. The audits yielded C$14.4 million in new tax, of which C$10million was GST. There was C$1.3 million in fines.

As of April 29, there were 40 audits of global income under way, 205 related to flipping, 34 related to capital gains and 428 related to GST.

The average Vancouver house price now sits around C$1.75million for the metropolitan region, while the Real Estate Board of Greater Vancouver’s “benchmark” price for all residential properties is C$889,100, a 30 per cent increase over the past year. However, incomes remain among the lowest in Canada, making Vancouver one of the world’s most un-affordable cities .

The Hongcouver blog is devoted to the hybrid culture of its namesake cities: Hong Kong and Vancouver. All story ideas and comments are welcome. Connect with me by email ian.young@scmp.com or on Twitter, @ianjamesyoung70

This article appeared in the South China Morning Post print edition as:

Bolstered by first-time home buyers, existing-home sales rose for the fourth straight month in June, reaching a nine-year high.

Sales of existing single-family homes, townhomes, condominiums and co-ops increased 1.1% to a seasonally adjusted annual rate of 5.57 million, up from May’s downwardly revised 5.51 million, the National Association of Realtors said Thursday. The June pace was the strongest since 2007.

First-time buyers made up 33% of those transactions, the biggest share in four years. That eased concerns that a shortage of affordable houses has been pushing entry-level buyers out of the market.

The median existing-home price also reached a new high as it surged 4.8% to $247,700 from a year ago, above the former peak of $238,900 in May.

June’s sales exceeded the highest forecast of economists polled by Bloomberg, 5.56 million.

Healthy job gains, record-high stock prices and near-record low mortgage rates stoked June’s positive showings, said Lawrence Yun, chief economist at the National Association of Realtors.

“The modest bump in June sales to first-time buyers can be attributed to mortgage rates near all-time lows and perhaps a hopeful indication that more affordable, lower-priced homes are beginning to make their way onto the market,” he said. “The odds of closing on a home are definitely higher right now for first-time buyers living in metro areas with tamer price growth and greater entry-level supply — particularly areas in the Midwest and parts of the South.”

The Midwest has the lowest median existing-home price among all regions, $199,900, followed by the South, at $217,400. The median price in the West climbed 7.2% from a year ago to $350,800.

Total available existing homes for sale dipped 0.9% to 2.12 million, now 5.8% below a year ago.

“Seasonally adjusted, the month’s supply of homes in June 2016 was the lowest since June 2005, indicating that inventory problems still plague home buyers,” said Ralph McLaughlin, Trulia’s chief economist.

In Central London – the 30 most central postal codes and one of the most ludicrously expensive housing markets in the world – eager home sellers are slashing their asking prices to unload their properties. But even that isn’t working.

In the 12 days after the Brexit vote, cuts to asking prices have soared by 163% compared to the 12 days before the vote, according to the Financial Times. Yet sales have plunged 18% from before the Brexit vote. Sales had already taken a big beating before then and are now down a mind-boggling 43% from where they’d been a year ago!

So Brexit did it?

Um, well, sort of. But it’s more than Brexit. Home prices on a £-per-square-foot basis had peaked in Q2 2014, according to real-estate data provider LonRes. Since then, the market in Central London has been hissing hot air. By Q1 2016, prices for homes above £5 million had dropped 8% from their 2014 peak, and prices for homes from £2 million to £5 million had plunged 10%.

Back in December 2015, we reported that luxury housing in London was getting mauled, based on the LonRes report for the third quarter, released at the time. It pointed the finger at folks who, once “awash with cash, don’t have as much to spend” [read… It Gets Ugly in the Toniest Parts of London].

Then, in its spring review, LonRes called the prime London housing market “challenging.”

It wasn’t just the Brexit referendum and the new stamp duty – In 2014, a change in the stamp duty made buying high-end homes more costly; and in April this year, an additional duty was imposed on purchases beyond a primary residence. Now there’s a third reason, and it originates deep from the bowels of the UK economy. LonRes:

A third is now making itself known to us as it is not something that the chancellor can bury any more. This is the balance of payments which ran at 5.2% of GDP last year and was the largest annual deficit since records began in 1948.

If measures are not taken to bring this under control, then the mini experiment to deflate the London property bubble will seem small change compared to the £32.7bn deficit that exists.

The London residential market has undoubtedly slowed, and this is impacting prices. No one will disagree that London’s prime market needed the steam to be released from it. My guess is that this slower market will be here for some time.

And not just in London…

Last week, the Royal Institution of Chartered Surveyors was spreading gloom with its residential market survey of the UK, conducted after the Brexit vote, that found, as the Telegraph put it, “The number of people wanting to buy a house has fallen to the lowest level since mid-2008 amid post-referendum uncertainty.”

Lucian Cook, head of residential research at Savills, told the Telegraph:

“The current month’s figures suggest countrywide impact on sentiment which is to be expected. However previous months’ results would indicate that a slowdown in London has been on the cards for some time. It looks like the Brexit vote may be the trigger for this to materialize.”

Now all hopes are once again centered on foreigners and their money to bail out the housing bubble before it completely implodes. But this time, it’s different, as they say at the worst possible moment: it’s not the Russians or the Chinese, but people whose investments and incomes are in currencies linked to the US dollar. Over the last 12 months, the pound has lost about 14% against the dollar, most of it since the Brexit vote, which would give these folks an additional discount on UK real estate.

The Financial Times expressed those industry hopes, and its new saviors, citing Anthony Payne, managing director at LonRes:

“We have heard that quite a number of Middle Eastern buyers have been coming back into the market. A lot of them are converting from dollars, and together with any discount they get [plunging prices], the saving in the actual price is quite substantial,” said Mr. Payne. “Some people are concerned by Brexit – others see it as an opportunity.”

London isn’t the only ludicrously overpriced housing market, where prices, once helped along by foreign money, are skidding. And now the industry is hoping for more foreign money to wash ashore, just when the Chinese, by far the largest group of investors in the US housing market, are getting cold feet.

One conundrum stumping investors in recent months has been how, with investors pulling money out of equity funds (at last check for 17 consecutive weeks) at a pace that suggests a full-on flight to safety, as can be seen in the chart below which shows record fund outflows in the first half of the year – the fastest pace of withdrawals for any first half on record…

… are these same markets trading at all time highs? We now have the answer.

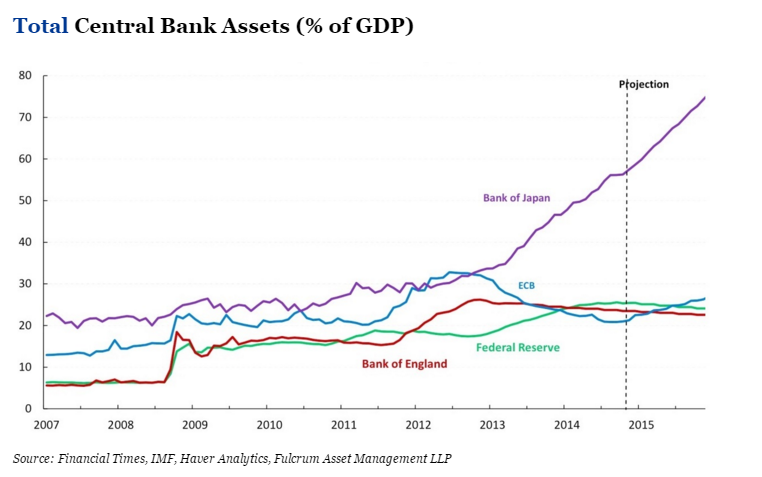

Recall at the end of January when global markets were keeling over, that Citi’s Matt King showed that despite aggressive attempts by the ECB and BOJ to inject constant central bank liquidity into the gunfible global markets, it was the EM drain via reserve liquidations, that was causing a shock to the system, as net liquidity was being withdrawn, and in the process stocks were sliding.

Fast forward six months when Matt King reports that “many clients have been asking for an update of our usual central bank liquidity metrics.”

What the update reveals is “a surge in net global central bank asset purchases to their highest since 2013.”

And just like that the mystery of who has been buying stocks as everyone else has been selling has been revealed.

But wait, there’s more because as King suggests “credit and equities should rally even more strongly than they have done already.”

More observations from King:

The underlying drivers are an acceleration in the pace of ECB and BoJ purchases, coupled with a reversal in the previous decline of EMFX reserves. Other indicators also point to the potential for a further squeeze in global risk assets: a broadening out of mutual fund inflows from IG to HY, EM and equities; the second lowest level of positions in our credit survey (after February) since 2008; and prospects of further stimulus from the BoE and perhaps the BoJ.

His conclusion:

While we remain deeply skeptical of the durability of such a policy-induced rally, unless there is a follow-through in terms of fundamentals, and in credit had already started to emphasize relative value over absolute, we suspect those with bearish longer-term inclinations may nevertheless feel now is not the time to position for them.

And some words of consolation for those who find themselves once again fighting not just the Fed but all central banks:

The problems investors face are those we have referred to many times: markets being driven more by momentum than by value, and most negatives being extremely long-term in nature (the need for deleveraging; political trends towards deglobalization; a steady erosion of confidence in central banks). Against these, the combination of UK political fudge (and perhaps Italian tiramisu), a lack of near-term catalysts, and overwhelming central bank liquidity risks proving overwhelming – albeit only temporarily.

Why have central banks now completely turned their backs on the long-run just to provide some further near-term comfort? Simple: as Keynes said, in the long-run we are all dead.

In another reminder why most of the population is increasingly furious at the “elites”, over the holiday weekend a 31-year-old portfolio manager for Moore Capital, Brett Barna, threw a wild “Wolf of Wall Street”-style Hamptons party, complete with Champagne, scores of bikini-clad women and costumed gun-toting midgets, and in the process trashed a $20 million mansion.

According to Page Six, Barna, “a portfolio manager at Louis Bacon’s Moore Capital Management, hosted the all-day “#Sprayathon” pool party on Sunday, where 1,000 people doused themselves in bubbly as rapper Ace Hood performed.”

Making things more complicated is that Barna is not the owner of the 9-bedroom, 8 acre Hamptons mansion which “comes with tennis court, gym, outdoor pool & jacuzzi” where he celebrated US Independence Day in decadent style, and instead rented it from “Tommy” for $29,000 on AirBNB, a fee he is now disputing.

And now Tommy is angry: “the furious owner of the 14-bedroom estate in Bridgehampton plans to sue Barna, 31, for $1 million, saying the Wall Street hot shot had claimed the party would be a fundraiser for an animal charity for a mere 50 guests.”

The owner, who asked to not be named, told Page Six that , “Brett came to me dropping Louis Bacon’s name and saying he was a big deal with the Robin Hood Foundation. He said there would be 50 people at the event and it was for animal rescue. But the only animals there were the people, a thousand of them. They drowned themselves in Champagne, they had midgets they threw in the pool, they broke into the house, trashed the furniture, art was stolen, we found used condoms. So many people were there that the concrete around the pool crumbled and fell into the water. It was like ‘Jersey Shore’ meets a frat party. We are preparing a massive lawsuit . . . We’re waiting to serve him.”

“Brett was last seen on Sunday chugging Champagne with two midgets.”

Wild social media posts show party goers dousing themselves in booze and dancing wildly.

The videos and photos below, capturing the festivities, will surely be Exhibit A-X in the upcoming lawsuit.

According to the publication, this is an annual bacchanal: Last year #Sprayathon revelers started a brush fire at a Hamptons manse owned by “Hercules” actor Kevin Sorbo.

Page Six adds that a rep for the embarrassed hedge fund didn’t comment, but a source said Moore raised $100,000 for Last Chance Animal Rescue, and they hired cleaners and left the house in good condition.

As CNBC adds this morning, Moore Capital said it has fired Barna. “Mr. [Brett] Barna’s personal judgment was inconsistent with the firm’s values,” the company told CNBC in a statement.

“He is no longer employed by Moore Capital Management.”

Bob Corker and Mark Warner speaking in an interview with Zillow about mortgage-finance reform

“The idea that Wall Street came out of this thing just fine, thank you, is just something that just grates on people. They think you didn’t just come out fine because it was luck. They think you guys just really gamed this thing real well.”

So said then-Senator Edward E. Kaufman, a Democrat from Delaware, at the Congressional hearing in the spring of 2010 where assorted members of Congress lambasted Goldman Sachs’ activity in the run-up to the financial crisis.

But it turns out two members of Congress actually made money from that crisis, according to publicly available documents. During the crisis years, two now-senators, Mark Warner (D-Va.) who was the governor of Virginia until his Senate term began in 2009, and Bob Corker (R-Tenn.), who took office in 2007, were invested in a fund that appears to have made sizable profits from Goldman products that were designed to bet against the real estate market.

There’s no evidence either Senator was aware of the specific strategy, although both have reported millions of dollars of income from the fund. A little bit of ancient history: Back in the spring of 2010, the SEC charged Goldman Sachs with fraud over a deal called Abacus 2007-AC1. Abacus 2007-AC1 was a so-called CDO, which in essence requires investors to wager against each other. One set of investors was betting that homeowners would continue to pay their mortgages. Others, who were short, were betting there would be massive defaults.

In this particular deal, Goldman allowed a hedge fund client, Paulson Capital Management, to take the short position and help choose which securities would go into it. The SEC alleged that Goldman hadn’t told the long investors that Paulson’s team essentially had designed the CDO to fail. According to a report done by the US Senate Permanent Subcommittee on Investigations, three long investors together lost about $1 billion from their Abacus investments, while the Paulson hedge fund profited by about the same amount.

Goldman paid $550 million to settle the SEC’s charges in the summer of 2010. A young vice president who had worked on the deal, Fabrice Tourre, was eventually found liablein a civil suit brought by the SEC, making him one of the few to face any repercussions from the crisis era.

Senate Foreign Relations Committee Chairman Sen. Bob Corker, R-Tenn., listens on Capitol Hill in Washington

But Abacus 2007-AC1 wasn’t unique. In fact, it was merely the last in a series of Abacus CDOs. According to the Senate report, these were “pioneered by Goldman to provide customized CDOs for clients interested in assuming a specific type and amount of investment risk” and “enabled investors to short a selected group” of securities. Many of the Abacus deals were tied in part to the performance of subprime residential mortgage-backed securities, but some were also tied to the performance of commercial mortgage-backed securities.

Because AIG provided insurance on at least some of the Abacus deals, the Abacus deals were also part of the collateral calls that Goldman made to AIG, and part of the reason that taxpayers ended up bailing out AIG. Plenty of well-known hedge funds availed themselves of Goldman’s Abacus deals, according to a document Goldman provided the Financial Crisis Inquiry Commission. The list of those who were short various Abacus deals includes Moore Capital Management, run by billionaire Louis Bacon; Magnetar, an Illinois-based fund run by Alec Litowitz; Brevan Howard, a European hedge fund management company; and FrontPoint Partners (which shows up in the movie “The Big Short”).

There are also some lesser known names in the document, including Pointer Management, a Tennessee-based fund which was founded in 1990 by Joseph Davenport, a Chattanooga area businessman and former Coca-Cola executive, and Thorpe McKenzie, also from Chattanooga, according to the Campaign for Accountability.