As wereported in January, approximately 40 percent of student loans taken out in 2014 are projected to default by 2023 according to the Brookings Institute.

However, anew game show on TruTVoffers millennial contestants a chance to answer trivia questions – and if they win, the game show will pay off their student debt.

“Paid Off,” a new trivia game show that premiered this week tries to illuminate the student debt crisis that has entrapped countless millennials. To get the balance right, the show’s producers partnered with a nonprofit group called Student Debt Crisis.

Its executive director and founder, Natalia Abrams, gave this adviceto producers: “Every step of the way, from signing up for college to paying back their loans, it’s been a confusing process. So make sure that there’s some heart to this show.”

Video: Paid Off with Michael Torpey Season 1 Trailer

Michael Torpey, a New York-based actor (“Orange is the New Black”) who is the host of the show, acknowledges that student debt is a crisis and one of the most difficult financial issues plaguing millennials in the gig economy.

“We’re playing in a weird space of dark comedy,” said Torpey, who developed the show with TruTV producers and various nonprofit groups. “As a comedian, I think a common approach to a serious topic is to try to laugh at it first.”

Video: Paid Off with Michael Torpey – The Story Behind Paid Off with Michael

The rules of game show are simple: Three millennial contestants, all of whom have an exorbitant amount of student debt, go head-to-head in a few rounds of trivia questions, hoping that their useless liberal arts degree enables them to answer enough questions right. If they win, well, the show will cover 100 percent of their outstanding student loans.

“One of the mantras is ‘an absurd show to match an absurd crisis,’” Torpey told The Washington Post. “A game show feels really apt because this is the state of things right now.”

Earlier this year, the show had a casting call in Atlanta – this is what the casting flyer stated: “truTV’s new comedy games show PAID OFF is going to do something the government won’t – help people get out of student loan debt! If you’re smart, funny, live in the Atlanta area and have student loan debt, We Want You!”

Video: Paid Off with Michael Torpey – Finger The Masters

Torpey told NBC that “he strives to balance the light hearted trappings of a game show with an earnest, empathetic look at the student debt issue.”

“I want to be very respectful of the folks who come on our show, who opened their hearts and shared their struggles with us,” Torpey said. “I hope this show de-stigmatizes debt. I mean, there are 45 million borrowers out there. It is a huge number of people!”

Google searches for “paid off game show” have been rising since June.

Meanwhile, “student loans forgiveness” searches have been surging over the cycle.

The computer-generated image of Mr Kalt greets clients on screen and can talk customers through the bank’s latest research as well as answer queries ( UBS )

An investment bank has digitally “cloned” one of its top staff members, allowing clients to get financial advice without the need to speak to a real-life banker.

UBSis testing the use of a lifelike avatar of Daniel Kalt, its chief investment officer for customers inSwitzerland.

The computer-generated image of Mr Kalt greets clients on screen and can talk customers through the bank’s latest research as well as answer queries. Another digital assistant called Fin is also available to carry out transactions.

The new service, called UBS Companion is driven by artificial intelligence and voice-recognition technology developed by IBM. Another company, FaceMe, animated and visualised the avatars. UBS hopes the new tech will increase efficiency and allow it to advise more customers.

But are bankers set to be the latest group to fall victim to the much heralded about “rise of the robots”?

No, says UBS. The bank says it aims to find the “best possible combination of human and digital touch”.

The clone will give clients quicker answers to some questions but the option to speak to a human being will always be available.

UBS started trials in June at its branch in Zurich where it is testing the new system on 100 clients but it won’t say how they have reacted so far.

At present, there are no plans to unleash an army of cloned bankers on the world.

“It is a project to explore new technology and find out how humans and machines can complement heightened levels of client experience in future,” UBS said.

“The aim is to explore how to create a new frictionless access to UBS’s expertise for our clients and to test the acceptance of digital assistants in a wealth management context.”

There is a group of bankers for whom “better” means “worse” for everyone else: we are talking, of course, about restructuring bankers who advising companies with massive debt veering toward bankruptcy, or once in it, how to exit from the clutches of Chapter 11, and who – like the IMF, whose chief Christine Lagarde recently said “When The World Goes Downhill, We Thrive” – flourish during financial chaos and mass defaults.

Which is to say that the past decade has not been exactly friendly to the world’s restructuring bankers, who with the exception of two bursts of activity, the oil collapse-driven E&P bust in 2015 and the bursting of the retail “bricks and mortar” bubble in 2017, have been generally far less busy than usual, largely as a result of abnormally low rates which have allowed most companies to survive as “zombies”, thriving on the ultra low interest expense.

However, asMoody’s warned yesterday, and as the IMFcautioned a year ago, this period of artificial peace and stability is ending, as rates rise and as a avalanche of junk bond debt defaults. And judging by their recent public comments, restructuring bankers have rarely been more exited about the future.

Ken Moelis

Take Ken Moelis, who last month was pressed about his rosy outlook for his firm’s restructuring business, describing “meaningful activity” for the bank’s restructuring group.

“Your comments were surprisingly positive,” said JPMorgan’s Ken Worthington,quoted by Business Insider. “Is this sort of steady state for you in a lousy environment? Can things only get better from here?”

Moelis’ response: “Look, it could get worse. I guess nobody could default. But I think between 1% and 0% defaults and 1% and 5% defaults, I would bet we hit 5% before we hit 0%.”

He is right, because as we showed yesterday in this chart from Credit Suisse, after languishing around 1%-2% for years, default rates have jumped the most in 5 years, and are now “ticking higher”

Moelis wasn’t alone in his pessimism: in March, JPMorgan investment-banking headDaniel Pinto saidthat a 40% correction, triggered by inflation and rising interest rates, could be looming on the horizon.

These are not isolated cases where a gloomy Cassandra has escaped from the asylum: already the biggest money managers are positioning for a major economic downturn according to recent research from Bank of America. And while nobody can predict the timing of the next collapse, Wall Street’s top restructuring bankers have one message: it’s coming, and it’s not too far off.

However, the most dire warning to date came from Bill Derrough, the former head of restructuring at Jefferies and the current co-head of recap and restructuring at Moelis: “I do think we’re all feeling like where we were back in 2007,” hetold Business Insider:“There was sort of a smell in the air; there were some crazy deals getting done. You just knew it was a matter of time.”

What he is referring to is not just the overall level of exuberance, but the lunacy taking place in the bond market, where CLOs are being created at a record pace, where CCC-rated junk bonds can’t be sold fast enough, and where the a yield-starved generation of investors who have never seen a fair and efficient market without Fed backstops, means that the coming bond-driven crash will be spectacular.

“Even if there is not a recession or credit correction, with the sheer volume of issuance there are going to be defaults that take place,” said Neil Augustine, co-head of the restructuring practice at Greenhill & Co.

The dynamic is familiar: since 2009, the level of global non-financial junk-rated companies has soared by 58% representing $3.7 trillion in outstanding debt, the highest ever, with 40%, or $2 trillion, rated B1 or lower. Putting this in contest, since 2009, US corporate debt has increased by 49%, hitting a record total of $8.8 trillion, much of that debt used to fund stock repurchases. As a percentage of GDP, corporate debt is at a level which on ever prior occasion, a financial crisis has followed.

The recent glut of debt is almost entirely attributable to the artificially low interest-rate environment imposed by the Federal Reserve and its central bank peers following the crisis. Many companies took advantage and refinanced their debt before 2015 when a large swath was set to mature, kicking the can several years down the road.

But going forward “there’s going to be refinancing at significantly higher rates,” said Steve Zelin, head of the restructuring in the Americas at PJT Partners.

And as theIMF first warned last April, refinancing at higher rates will further shrink the margin of error for troubled companies, as they’ll have to dedicate additional cash flow to cover more expensive interest payments.

“When you have highly leveraged companies and even a modest rise in interest rates, that can result in an increase in restructuring activity,” said Irwin Gold, executive chairman at Houlihan Lokey and co-founder of the firm’s restructuring group.

So with a perfect debt storm coming our way, many restructuring firms have been quietly hiring new employees to be ready when, not if, the economy takes a turn for the worse.

“The restructuring business is a good business during normal times and an excellent business during a recessionary environment,” Augustine said. “Ultimately, when a recession or credit correction does happen, there will be a massive amount of work to do on the restructuring side.” Here are some additional details on recent banker moves from Business Insider:

Greenhill hired Augustine from Rothschild in March to co-head its restructuring practice. The firm also hired George Mack from Barclays last summer to cohead restructuring. The duo, along with Greenhill vet and fellow co-head Eric Mendelsohn, are building out the firm’s team from a six-person operation to 25 bankers.

Evercore Partners in May hired Gregory Berube, formerly the head of Americas restructuring at Goldman Sachs, as a senior managing director. The firm also poached Roopesh Shah, formerly the chief of Goldman Sachs’ restructuring business, to join its restructuring business in early 2017.

“It feels awfully toppy, so people are looking around and saying, ‘If I need to build a business, we need to go out and hire some talent,'” one headhunter with restructuring expertise told Business Insider.

“In our world, people are just anticipating that it’s coming. People are trying to position their teams to be ready for it,” Derrough said. “That was the lesson from last cycle: Better to invest early and have a cohesive team that can do the work right away and maybe be a little bit overstaffed early, so that you can execute for your clients when the music ultimately stops.”

Of course, if the IMF is right (for once), Derrough and his peers will soon see a windfall unlike anything before: last April, the International Monetary Fund predicted that some 20%, or $3.9 trillion, of the total global corporate debt is in danger of defaulting once rates rise.

Although if and when that day comes, perhaps a better question is whether companies will be doing debt-for-equity swaps, or fast forward straight to debt-for-lead-gold-and canned food…

July 6, 2016 marks the point when the US government’s condition became irretrievably terminal. On that date the US Treasury’s 10-year note yield hit its low, 1.34 percent, and has been trending irregularly higher ever since. Historically, debt has been the life support for regimes in extremis. No regime has ever been more in debt than the US government. Its annual deficit and debt service expense are growing, old-age pension and medical programs face a demographic crunch, and now interest rates are rising. One way or the other, the government walking away from some or all of its promises is as set in stone as anything in this life can be.

Dakota Access Pipeline protesters chant outside of the Wells Fargo Bank at Westlake Center in January 2017. The city of Seattle has renewed its contract with Wells Fargo, after it could get no other takers for its banking business. (Lindsey Wasson / The Seattle Times)

Seattle split with Wells Fargo a year ago in protest over the bank’s investments in the Dakota Access Pipeline and fraud scandals. But the two are together again after the city could find no other bank to take its business.

The city of Seattle will keep banking with Wells Fargo & Co. after it could get no other takers to handle the city’s business.

The City Council in February 2017 voted 9-0 to pull its account from Wells Fargo, saying the city needs a bank that reflects its values.

Council members cited the bank’s investments in the Dakota Access Pipeline, as well as a roiling customer fraud scandal, as their reasons to sever ties with the bank.

Some council members declared their vote as a move to strike a blow against not only Wells Fargo, but “the billionaire class.”

“Take our government back from the billionaires, back from [President] Trump and from the oil companies,” Council member Kshama Sawant said at the time.

The contract was set to expire Dec. 31, but as finance managers for the city searched for arrangements to handle the city’s banking,it got no takers, said Glen Lee, city finance director. That was even after splitting financial services into different contracts to try to attract a variety of bidders, including smaller banks.

In the end, there were none at all.

It became clear this was our best and only course of action,” Lee said of the city’s decision to stick with Wells Fargo after all.

The first sign that it would be hard to make the council’s wish a realitycame soon after the votewhen Wells Fargo too-hastily informed the city it could sever its ties immediately with no penalty for breaking the contract. The bank even promised to help the city find a new financial partner.

But it quickly became clear how hard that would be as the city reworked its procurement specifications and searched for months.

One month ago, when discussing the most recent trends in the US subprime auto loan space,ZH revealedhow despite a virtual halt in direct loans by depositor banks to subprime clients following the financial crisis, the US banking sector now has over a third of a trillion dollars in indirect subprime exposure, in the form of loans to non-banks financial firms which in the past decade have become the most aggressive lenders to America’s sub-620 FICO population.

As we further explained, the banks’ total indirect exposure to subprime loans – not just auto loans, but also subprime mortgages, and subprime consumer loans – could be pieced together through public filings, and according to FDIC reports, bank loans to non-banks subprime lenders soared this decade, with the following 5 names standing out:

Wells Fargo: $81 billion, up from $13.4 billion in 2010

Citigroup: $30 billion, up from $4.1 billion in 2010

Bank of America: $30 billion, up from $2.8 billion in 2010

JP Morgan: $28 billion, up from $10.4 billion in 2010

Goldman Sachs: $22 billion

Morgan Stanley: $16 billion

Visually:

But while the supply side of the subprime equation is clearly firing on all cylinders – as only the next crash/crisis will stop desperate yield chasers – things on the demand side are going from bad to worse, and according to thelatest Fitch Autoloan delinquency data, consumers are defaulting on subprime auto loans at a higher rate than during the 2008–2009 financial crisis.

The highly seasonal rate for subprime auto loans more than 60 days past due reached the highest in 22 years – since 1996 – at 5.8%, according to March data; this is well over 2% higher than the comparable March default rate in the low 3%s hit during the peak of the financial crisis a decade ago.

The more recent April data, showed a delinquency rate of 4.3%, higher than the 4.1% last year, and the second highest April on record. Keep in mind, April is the “best” month of the year from a seasonal perspective as that is when the bulk of tax refunds hit, which are then promptly used to repay outstanding bills – it’s all downhill from there… or rather uphill as the chart shows ever higher default rates.

And while delinquencies have been rising, the number of auto loans and leases to subprime borrowers has continued to shrink, falling 10% Y/Y according to Equifax. However, as we showed at the top, it’s not due to supply constraints at the non-bank subprime lenders, the slide in subprime loan volume is all on the demand side: auto-lease origination by subprime customers tumbled by 13.5%.

Meanwhile, asBloomberg reports, the volume of bond sales backed by these loans are likely to remain the same because banks and credit unions don’t turn most of their loans into securities: “ABS is a fraction of the total auto credit market, which is mainly funded on balance sheets,” Wells Fargo analyst John McElravey told Bloomberg in an interview. “If the pullback from subprime is more from the balance-sheet lenders, banks, then maybe securitization keeps moving along.”

Not maybe: definitely. As the following chart show, the percentage of subprime securitization of all auto ABS as a share of total loans has not only surpassed the pre-crisis peak, it is at a new all time high.

Call it the latest “new (ab)normal” paradox: the underlying auto subprime loan market is shrinking fast, and yet the market for subprime auto ABS securitizations has never been stronger.

Subprime-auto asset-backed security sales are on pace with last year at about $9.5 billion compared to $9.6 billion a year ago, according to data compiled by Bloomberg. With new transactions from Santander, GM Financial, Flagship, and Credit Acceptance expected to hit the market this week, volume may exceed 2017’s total of about $25 billion.

And while it is safe to say it will all end in tears – again – as it did a decade ago, with the next recession the catalyst, the shape of the next crash will be very different. As we explained last month, this subprime bond market is vastly different from what it was even a few years ago, let alone during the last crisis as an influx of generally riskier, smaller lenders flooded into it in the post-crisis years, bankrolled by private-equity moneyand funded by big bank loans, pursued the riskiest borrowers in order to stay competitive.

“Neither banks nor credit unions have done ‘deep subprime’ lending,” Gunnar Blix, deputy chief economist at Equifax told Bloomberg. “That’s mainly done by smaller dealer-finance and independent finance companies” who rely almost solely on ABS for funding. According to Bloomberg, only about 10% of $437 billion of outstanding subprime auto loans have been securitized into ABS, according to Wells Fargo, which means that underwriters are generally massively exposed to the subprime auto loan crunch that is already playing out before our eyes, and which will be magnified exponentially in the next recession.

* * *

The latest subprime delinquency data seemed confusing, almost a misprint to Hylton Heard, Senior Director at Fitch Ratings who said that “it’s interesting that [smaller deep subprime] issuers continue to drive delinquencies on the index in an unemployment environment of around 4%, low oil prices, low interest rates — even though they are rising — and a positive economic story overall.” In other words, there is no logical explanation why in a economy as strong as this one, subprime delinquencies should be soaring.

Unless, of course the real, unvarnished, and non-seasonally adjusted economy is nowhere near as strong as the government’s “data” suggests.

Making matters worse, rising interest rates have made interest payment increasingly unserviceable for those subprime borrowers who are currently contractually locked up – hence the surge in delinquency rates – or those consumers with a FICO score below 620 who are contemplating taking out a new loan to buy a car, and suddenly find they could no longer afford it, an ominous development we first described one month ago in “Subprime Auto Bubble Bursts As “Buyers Are Suddenly Missing From Showrooms.“

And even if the subprime bubble hasn’t burst just yet, every incremental 0.25% increase in rates assures it is only a matter of time. For once, St. Louis Fed president James Bullard was not wrong when he warned this morning that he sees Fed policy as the reason behind the flattening of the yield curve, saying that “it’s been the Fed, I think, that has flattened the curve more than worries by investors on the state of the global economy.“

“My personal opinion is the Fed does not need to be so aggressive that we invert the yield curve” he noted, adding that “I do think we’re at some risk of an inverted yield curve later this year or early in 2019,” and “if that happens I think it would be a negative signal for the U.S. economy.”

If he’s correct, it begs the question: why is the Fed seeking to crash the economy and, by implication, the market?

We’ll close with a quote from the last Comptroller of the Currency, Thomas Curry, who during an October 2015 speech said that “what is happening in [the subprime auto lending] space today reminds me of what happened in mortgage-backed securities in the run up to the crisis.” It’s only gotten worse since then.

Wayne Jett, author of “Fruits of Graft”, interviewed by Sarah Westall in an eight part (video) series to discuss in depth the amazing history of events and actions leading up to the Great Depression. They also discuss the activities and actions taken during the Great Depression that caused increased misery for millions of Americans. This is an epic historical view of the Great Depression you have not heard before; that also serves to explain what is really driving most current events we are living through today.

This settlement is on top of the recent $1 billion fine for mortgage lending and auto insurance abuses.

The bank announced Friday afternoon that it reached a new settlement over its sales practices and will pay $480 million to a group of shareholders who accused the bank of making “certain misstatements and omissions” in the company’s disclosures about its sales practices.

The settlement stems from actions originally taken in 2016 by the Consumer Financial Protection Bureau, the Office of the Comptroller of the Currency, and the city and county of Los Angeles to fine the bank$150 millionfor more than 5,000 of the bank’s former employees opening as many as 2 million fake accounts in order to get sales bonuses.

The action led to a class action lawsuit brought on behalf of the bank’s customers who had a fake account opened in their name.

That lawsuit led to a$142 million fake accounts class action settlementthat covers all people who claim that Wells Fargo opened a consumer or small business checking or savings account or an unsecured credit card or line of credit without their consent from May 1, 2002 to April 20, 2017.

But that wasn’t the only legal battle that Wells Fargo was facing.

According to the bank, a putative group of the bank’s shareholders also sued the bank in U.S. District Court for the Northern District of California, alleging the bank committed securities fraud by not being wholly honest in its statements about its sales practices.

Despite stating that it denies the claims and allegations in the lawsuit, Wells Fargo is choosing to settle the case and will pay out $480 million, assuming the settlement amount is approved by the court.

According to the bank, it reached the agreement in principle to “avoid the cost and disruption of further litigation.”

This settlement is also separate from the recent$1 billion finehanded down against the bank by the CFPB and the OCC for mortgage lending and auto insurance abuses.

The bank stated that the new settlement amount of $480 million has been fully accrued, as of March 31, 2018.

“We are pleased to reach this agreement in principle and believe that moving to put this case behind us is in the best interest of our team members, customers, investors and other stakeholders,” Wells Fargo CEO Tim Sloan said in a statement. “We are making strong progress in our work to rebuild trust, and this represents another step forward.”

Two weeks after Deutsche Bank wasted no time at all to lay off 400 US bankers, or roughly 10% of total, as the bank’s post-disastrous earnings purge began, today the purge is accelerating and according to Bloomberg, the biggest European bank is considering a sweeping restructuring, a less scary phrase than “mass termination” in the U.S. “that could result in cutting about 20% of staff in the region” although Bloomberg caveats that a formal decision has not yet been made, the total figure may end up lower.

Deutsche Bank isn’t targeting a specific level of cuts at the U.S. unit and the final figure will depend on each business line’s decisions, according to another person briefed on the matter. The company had about 10,300 employees in the U.S. at the end of 2017, or about a tenth of its global workforce.

The news follows an earlier report that Deutsche Bank’s Barry Bausano, a senior banker in charge of overseeing the company’s relations with hedge fund clients, was leaving as the firm shakes up its U.S. operations.

When Bloomberg asked the bank about its mass termination plans, bank spokesman Joerg Eigendorf said “There are no such plans,” although considering the billions Deutsche has spent on rigging and manipulation, they may be excused if they are not seen as exactly credible.

Separately, Bloomberg also reports that under its new CEO, Christian Sewing, Deutsche Bank is considering cuts to businesses including prime brokerage, rates and repo,according to a bank statement last month and people familiar with the matter. As reported previously, the firm is already planning to close an office in Houston and shrink its presence in New York City, moving from Wall Street to a midtown Manhattan space that’s 30 percent smaller.

The Turkish government has withdrawn its reserves of gold from the Federal Reserve. Erdogan clearly is positioning himself to be able to seek its own power that will be contrary to international policy. Erdogan is one of those politicians who still think in the old days of Empire. As a member of NATO, he has constantly been threatening Greece. So what happens if we see a war between two NATO members? Who does NATO then support? When in doubt, bring the gold home in preparation for in time of war, a currency will not suffice.

Anecdotal evidence suggests that corporate borrowers may be due for a reckoning.

A growing spider web of evidence suggests a credit reckoning may be near.

For years, the naysayers have been warning about the precariousness of the corporate credit market. In an environment where balance sheets have become more and more bloated from excess borrowing stoked by the Federal Reserve’s easy-money policies, shrinking bond yield premiums don’t make sense. At some point, they argue, there will have to be a reckoning.

Could we be nearing that point?

On the surface, it’s hard not to like corporate bonds, despite yields being at some of their lowest levels relative to U.S. Treasuries since before the financial crisis. After all,corporate earnings are booming, thanks to an expanding economy and tax cuts, and the default rate is miniscule at less than 3 percent. On top of that, the number of companies poised for an upgrade at S&P Global Ratings is the highest in a decade.

All that said, there’s mounting anecdotal evidence of possible cracks in the credit facade. One place you can see them is in the latest monthly survey put out by the National Association of Credit Management. This organization surveys 1,000 trade credit managers in the manufacturing and service industries across the U.S. Like most surveys of its kind lately, the main index number was down a bit from its recent highs. But some Wall Street strategists are focusing on a more alarming data point showing a collapse in a category called “dollar collections.” The index covering that part of the survey – which measures the ability of creditors to collect the money they are owed from their customers – tumbled to 46.7 in April from 59.6 in March, putting it at its lowest level since early 2009, the height of the financial crisis.

The folks at the NACM aren’t quite sure what to make of the big plunge, which could turn out to be an anomaly. What they do know, however, is that credit conditions are getting weaker. As they describe it, the strengthening economy has forced more companies to boost borrowings to keep pace with their competitors. Now, they may be struggling to keep on top of that debt.

“It looks like creditors are having more challenges as far as staying current, which may be contributing to the very weak dollar collection numbers,” NACM economist Chris Kuehl wrote in a report accompanying the monthly survey results.

There may be something to that. The Institute of International Finance noted in a report last month that U.S. non-financial corporate debt rose to $14.5 trillion in 2017, an increase of $810 billion from 2016 and a figure that equates to 72 percent of the country’s gross domestic product (a post-crisis high). About 60 percent of the rise in debt stemmed from new bank loan creation, which is worrisome since those borrowings roll over more frequently than bonds and are tied to short-term interest rates, which are rising at a much faster clip than long-term rates. As an example, the three-month London Interbank Offered Rate for dollars has jumped to 2.35 percent from 1 percent at the start of 2017. While that’s still low historically, any small increase gets magnified across such a big amount of borrowings.

“Rising interest rates will add pressure on corporates with large refinancing needs,” the Washington-based Institute of International Finance wrote in its report. It estimates about $3.8 trillion of loan repayments will be coming due annually.

Credit is the lifeblood of the economy and financial markets. As such, it has a reputation for being a sort of early-warning system for investors and leading indicator for riskier assets such as equities. The equity strategists at Bloomberg Intelligence say they are noticing that stock performance is starting to correlate strongly with corporate balance sheet health as well as profitability. In an April report, they wrote that over the prior year, stocks of Standard & Poor’s 500 Index members with higher cash ratios outperformed low-ratio counterparts. Also, stocks of companies with higher net-debt ratios relative to both cash flow and market capitalization under performed lower-debt counterparts, with average monthly return differentials of 1.1 percentage points.

A growing number of influential Wall Street firms, from Guggenheim Partners to Pacific Investment Management Co., and from BlackRock Inc. to Greg Lippmann – who helped design the “Big Short” trade against subprime mortgages – are raising the alarm about the dangers growing in credit markets. It may well be that the reckoning is closer than we think.

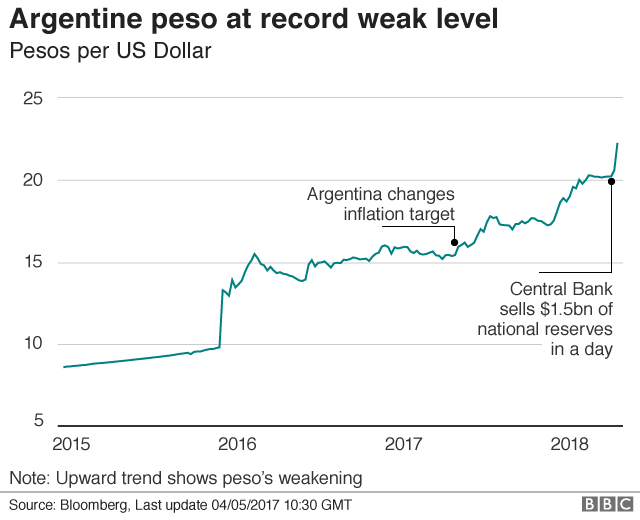

Argentina’s central bank has raised interest rates for the third time in eight days as the country’s currency, the peso, continues to fall sharply.

On Friday, the bank hiked rates to 40% from 33.25%, a day after they were raised from 30.25%. A week ago, they were raised from 27.25%. The rises are aimed at supporting the peso, which has lost a quarter of its value over the past year.

Analysts say the crisis is escalating and looks set to continue.

Argentina is in the middle of a pro-market economic reform programme under President Mauricio Macri, who is seeking to reverse years of protectionism and high government spending under his predecessor, Cristina Fernandez de Kirchner. Inflation, a perennial problem in Argentina, was at 25% in 2017, the highest rate in Latin America except for Venezuela. This year, the central bank has set an inflation target of 15% and has said it will continue to act to enforce it.

‘Aggressive steps’

Despite the twin rate rises, the peso, which was fixed by law at parity with the US dollar before Argentina’s economic meltdown in 2001-02, is now trading at about 22 to the dollar.

“This crisis looks set to continue unless the government steps in to reassure investors that it will take more aggressive steps to fix Argentina’s economic vulnerabilities,” said Edward Glossop, Latin America economist at Capital Economics. “Risks to the peso have been brewing for a while – large twin budget and current account deficits, a heavy dollar debt burden, entrenched high inflation and an overvalued currency.

“The real surprise is how quickly and suddenly things seem to be escalating.”

Mr Glossop said “a sizeable fiscal tightening” was planned for 2018, but it might now need to be larger and prompter. “Unless or until that happens, the peso is likely to remain under pressure, and there remains a real risk of a messy economic adjustment.” Argentina’s president Mauricio Macri is a controversial figure in a country that is still strongly divided ideologically. But among international investors he is unanimously praised. Since coming to office, he moved swiftly to end capital controls and re-establish trust in economic data coming from Argentina. However, he is not winning a crucial battle in the country – the one against inflation. Markets are taking notice and there has been a sell-off of the peso. The opposition wants to stop Macri from removing subsidies in controlled prices, such as energy and utility tariffs, which may bring more inflation in the short term but could help bring it down from above 20% now to about 5% by 2020.

Friday was a day for emergency measures – a massive hike to 40% in interest rates and another promise to bring down government spending.

Investors still believe Macri has a sound plan to recover Argentina, but they are not convinced he can see it through.

Argentina Raises Interest Rates To 40% To Support Their Currency

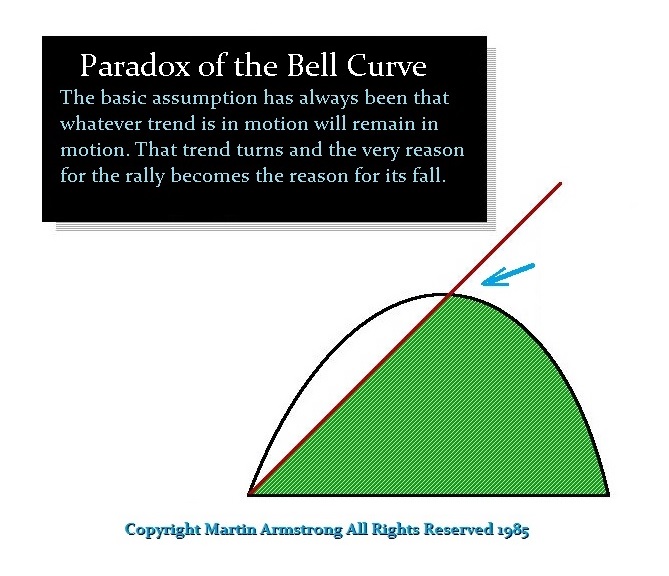

Argentina has just raised interest rates to40% trying to support the currency. I have explained many times that interest rates follow a BELL-CURVE and by no means are they linear. This is one of the huge problems behind attempts by central banks to manipulate the economy by impacting demand-side economics. Raising interest rates to stem inflation will work only up to a point and even that is debatable. The entire interrelationship between markets and interest rates has three main phase transitions and each depends upon the interaction with CONFIDENCE of the people in the survivability of the state.

PHASE TWO: Raising interest rates will flip the economy as Volcker did in 1981 ONLY when they exceed the expectation of profits in asset inflation provided there is CONFIDENCE that the government will survive as in the USA back in 1981 compared to Zimbabwe, Venezuela, Russia during 1917 or China back in 1949. In other words, if the nation is going into civil war, then tangible assets will collapse and the solution becomes assets flee the country.

In the case of the USA back in 1981, the high interest rates worked because we were only in Phase Two where there was no civil war or revolution so the survivability of the government did not come into question. Hence, Volcker created DELATION as capital then ran away from assets and into bonds to capture the higher interest rates. Then and only then did rates begin to decline between 1981 into 1986 reflecting the high demand for US government bonds, which in turn drove the US dollar to record highs and the British pound to $1.03 in 1985 resulting in the Plaza Accord and the creation of the G5 (now G20).

So many people want to take issue with me over how the stock market will rise with higher interest rates. It is a BELL-CURVE and you better begin to understand this. If not, just hand-over all your assets to the New York bankers now, go on welfare and just end your misery.

Here are charts of the Argentine share market the currency in terms of US dollars. You can see that the stock market offers TANGIBLE assets that rise in local currency terms because assets have an international value. Here we can see the dollar has soared against the currency and the stock market has risen in proportion the decline in the currency. I do not think there is any other way that is better to demonstrate the BELL-CURVE effect of interest rates than these two charts.

To those who doubt that the stock market can rise with rising interest rates, I really do not know what to say. Keep listening to the talking heads of TV and all the pundits who claim only gold will rise and everything else will fall to dust. Then we have the sublime blind idiots who never look outside the USA and proclaim the dollar will crash and burn not the rest of the world so buy gold and cryptocurrency you cannot spend and certainly with no power grid.

PHASE THREE

Is when no level of interest rate will save the day. Capital simply flees the political state for the risk of revolution or civil war means that tangible assets which are immovable will not hold their value such as companies and real estate. This is the period that Goldbugs envision. At that point, the value of everything will even move into the extreme PHASE FOUR where even gold will decline and the only thing to survive is food. There, the political state completely collapses and a new political government comes into being.

Meanwhile, the following is an analysis update on the pending 2021 LIBOR reset that will affect trillions in debt and derivative instruments across the globe…

When ZH reported Wells Fargo’s Q4 earningsback in January, they drew readers’ attention to one specific line of business, the one they dubbed the bank’s “bread and butter“, namely mortgage lending, and which as they then reported was “the biggest alarm” because “as a result of rising rates, Wells’ residential mortgage applications and pipelines both tumbled. Specifically in Q4 Wells’ mortgage applications plunged by $10bn from the prior quarter, or 16% Y/Y, to just $63bn, while the mortgage origination pipeline dropped to just $23 billion”, and just shy of the post-crisis lows recorded in late 2013.

Fast forward one quarter when what was already a grim situation for Warren Buffett’s favorite bank, has gotten as bad as it has been since the financial crisis for America’s largest mortgage lender, because buried deep in its presentation accompanyingotherwise unremarkable Q1 results(modest EPS and revenue beats), Wells just reported that its ‘bread and butter’ is virtually gone, and in Q1 2018 the amount in the all-important Wells Fargo Mortgage Application pipeline failed to rebound, and remained at $24 billion, the lowest level since the financial crisis.

Yet while the mortgage pipeline has not been worse since in a decade despite the so-called recovery, at least it has bottomed. What was more troubling is that it was Wells’ actual mortgage applications, a forward-looking indicator on the state of the broader housing market and how it is impacted by rising rates, that was even more dire, slumping from $63BN in Q4 to $58BN in Q1, down 2% Y/Y and the the lowest since the financial crisis (incidentally, a topic we covered just two days ago in “Mortgage Refis Tumble To Lowest Since The Financial Crisis, Leaving Banks Scrambling“).

Meanwhile, Wells’ mortgage originations number, which usually trails the pipeline by 3-4 quarters, was nearly as bad, plunging $10BN sequentially from $53 billion to just $43 billion, the second lowest number since the financial crisis. Since this number lags the mortgage applications, we expect it to continue posting fresh post-crisis lows in the coming quarter especially if rates continue to rise.

Adding insult to injury, as one would expect with the yield curve flattening to 10 year lows just this week, Wells’ Net Interest margin – the source of its interest income – failed to rebound from one year lows, and missed consensus expectations yet again. This is what Wells said about that: “NIM of 2.84% was a stable LQ as the impact of hedge ineffectiveness accounting and lower loan swap income was offset by the repricing benefit of higher interest rates.” But we’re not sure one would call this trend “stable” as shown visually below:

There was another problem facing Buffett’s favorite bank: while NIM fails to increase, deposits costs are rising fast, and in Q1, the bank was charged an average deposit cost of 0.34% on $938MM in interest-bearing deposits, exactly double what its deposit costs were a year ago.

And finally, there was the chart showing the bank’s consumer loan trends: these reveal that the troubling broad decline in credit demand continues, as consumer loans were down a total of $9.5BN sequentially across all product groups, far more than the $1.7BN decline last quarter.

What these numbers reveal, is that the average US consumer can not afford to take out mortgages at a time when rates rise by as little as 1% or so from all time lows. It also means that if the Fed is truly intent in engineering a parallel shift in the curve of 2-3%, the US can kiss its domestic housing market goodbye.

I am going to break from regular market commentary to step back and think about the big picture as it relates to debt and inflation. Let’s call it philosophical Friday. But don’t worry, there will be no bearded left-wing rants. This will definitely be a market-based exploration of the bigger forces that affect our economy.

One of the greatest debates within the financial community centers around debt and its effect on inflation and economic prosperity. The common narrative is that government deficits (and the ensuing debt) are bad. It steals from future generations and merely brings forward future consumption. In the long run, it creates distortions, and the quicker we return to balancing our books, the better off we will all be.

I will not bother arguing about this logic. Chances are you have your own views about how important it is to balance the books, and no matter my argument, you won’t change your opinion. I will say this though. I am no disciple of the Krugman “any stimulus is good stimulus” logic.

Thebroken window fallacyis real and digging ditches to fill them back in is a net drain on the economy. Full stop. You won’t hear any complaints from me there.

Yet, the obsession with balancing the government’s budget is equally damaging. In a balance sheet challenged economy the government is often the last resort for creating demand. Trying to balance a government deficit in this environment (like the Troika imposed on Greece during the recent Euro-crisis) is a disaster waiting to happen.

Have a look at these charts from the NY Times outlining the similarity of the Greece depression to the American Great Depression of the 1930s.

Now you might look at these charts and say, “Greece spent too much and suffered the consequences. Ultimately they will be better off taking the hit and reorganizing in a more productive economic fashion.” If so, you probably also still have this poster hanging in your room at your parent’s house where you grew up.

Personally, I don’t want to even bother discussing the possibility of this sort of Austrian-style-rebalancing coming to Western democracies. Yeah, it might be your dream, but it’s just a dream. I have Salma Hayek on myfreebie list, but what do I think of my chances? About as close to zero without actually ticking at the perfect zero level. It’s not a “can’t happen,” but it’s certainly a “it’s not going to happen in a million years.”

Governments were faced with a choice during the 2008 Great Financial Crisis. Credit was naturally contracting, and the economy wanted to go through a cleansing economic rebalancing where debt would be destroyed through a severe recession. Yet, governments had practically zero appetite to allow this sort of cathartic cleansing to happen. Instead, they stepped up and stopped the credit contraction through government spending and quantitative easing.

I believe that government spending is not all bad, and at times, it plays an important role in our economy. I am a huge fan ofRichard Koo’swork. When economies’ interest-rate policies become zero bound, governments are crucial in engaging in anti-cyclical spending. All debt is not bad. Take debt your company might issue for instance. Borrowing a million dollars to invest in capital equipment to make your firm more productive is a much different prospect than taking out a loan to engage in a Krugman-inspired-all-you-can-drink-party-headlined-by-the-Killers. Sure, the party sounds like fun, but it’s not going to benefit your firm past one night of excitement. Governments shouldn’t perpetuate unproductive pension grabs by workers, but instead actually spend money on infrastructure that will make the economy more productive. During the 1950s Eisenhower invested in the American highway system, helping America secure its place as the world’s most economically dominant country. Today that sort of infrastructure spending would be shouted down as irresponsible. Well, not continuing to invest in your country’s productive capacity is the irresponsible part.

The point is that not all spending is bad, but nor is all spending good. And even more importantly, government spending should be anti-cyclical. No sense spending more when your economy is rocking. Better to save the bullets to ebb the natural flow of the business cycle.

But I digress. Let’s get back to debt.

Creating debt is inflationary, while paying down debt is deflationary. That’s pretty basic.

The easiest way for me to demonstrate this fact is to look at an area where debt has been created for spending in a specific area. No better example than student loans.

Over the past fifteen years, inflation in college tuition has exploded. It’s been absolutely bonkers. Here is the chart of regular CPI versus tuition CPI.

But it should really be no surprise. If we add the student loan debt versus Federal debt series, it becomes clear that a tremendous amount of credit has been extended to students.

So let’s agree that credit creation is inflationary, and by definition, credit destruction should be deflationary.

Therefore when the market pundits that I like to affectionately call deflationistas argue that this next chart is ultimately deflationary, I understand where they are coming from.

If you assume that this debt needs to be paid back, then it’s easy to understand their argument. When debt starts to contract and this chart heads lower, this will be deflationary. And if you assume that governments start to balance their books, then there is every reason to expect that future deflation is the worry, not inflation. After all, the money has already been spent. The inflation from that spending is already in the system.

I can already hear the deflationistas argument – over 100% of GDP is unsustainable therefore credit growth will at worst go sideways, but most likely actually contract in coming years.

Really? How about Japan?

The same argument was made at the turn of the century when Japan was running a debt that was over 150% of GDP, yet they somehow managed to push that up another 80% to 230% without causing some sort of apocalyptic collapse.

Now before you send me an angry email about the moral irresponsibility of suggesting debt can go higher, save your clicks. I understand your argument. I am not interested in debating what should be done, but rather I am trying to determine what will be done. You might believe governments and Central Banks will gain religion and start conducting prudent and responsible policies. So be it. If you believe that, then by all means – load up on long-dated sovereign bonds as they will continue to be the trade of the century.

I, on the other hand, believe that Central Banks will continue printing until, as my favourite West Coast skeptic Bill Fleckenstein says, “the bond market takes away the keys.” And even when Central Banks are mildly responsible, politicians are sitting in the wings waiting to spend at any chance they get. Take Trump’s recent stimulus program. We are now more than eight years into an economic recovery, and he just pushed through one of the most stimulative fiscal policies of the past couple of decades. Regardless of where you stand politically regarding these tax cuts, there can be no denying they were much more needed in 2008 than today.

This is a long-winded way of saying that although I agree that the creation of debt is inflationary, and that the destruction of debt is deflationary, I don’t buy the argument that any sort of absolute amount of debt means the trend has to change. I don’t look at the 100% debt-to-GDP figure and worry that the US government will somehow institute deflationary policies to pay that back. Nope, I don’t see anything but a sea of growing deficits and debts. And in fact, the larger debts grow, the less likely they are to be paid back.

How will Japan pay back their debt that is 230% of GDP? The answer is that they can’t. It will be inflated away.

It’s foolish to believe that the end-game is anything but inflation. And even though increasing debt seems scary, if there is one thing that I am sure of, it’s that they will figure out a way to make even more of it.

Rant over. And no more big picture philosophy for a while – I promise.

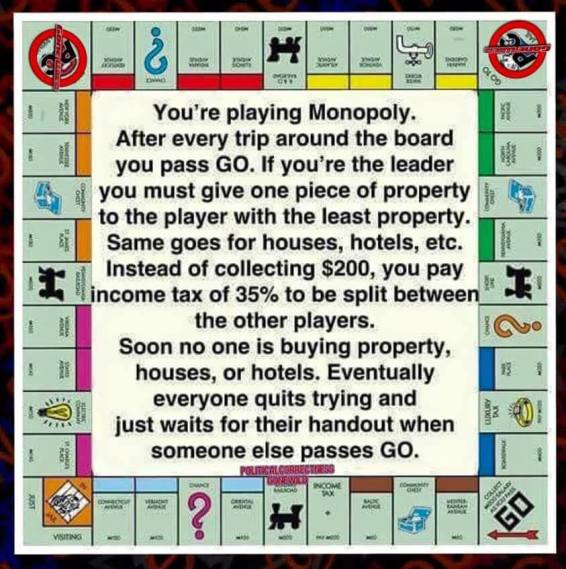

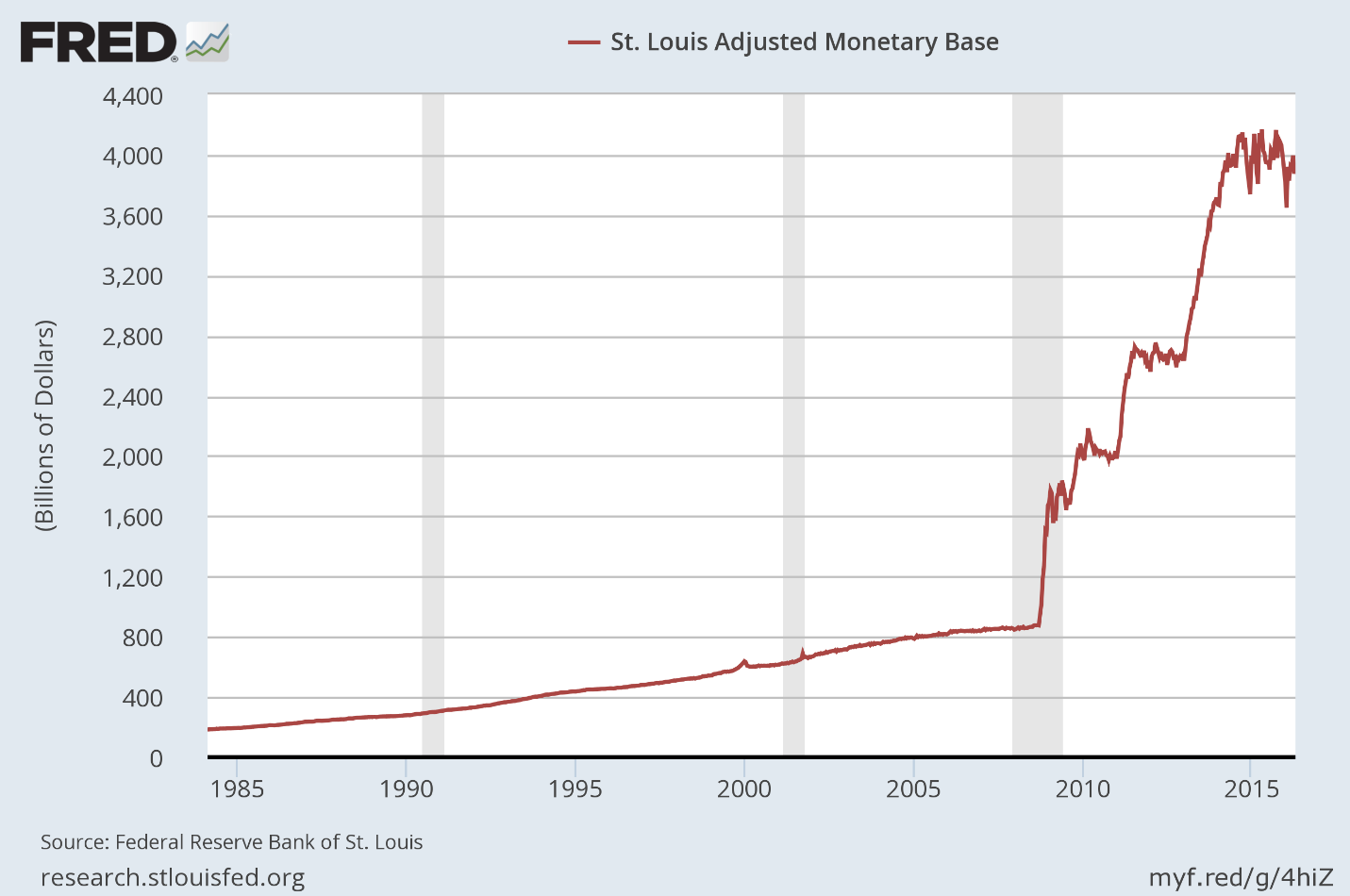

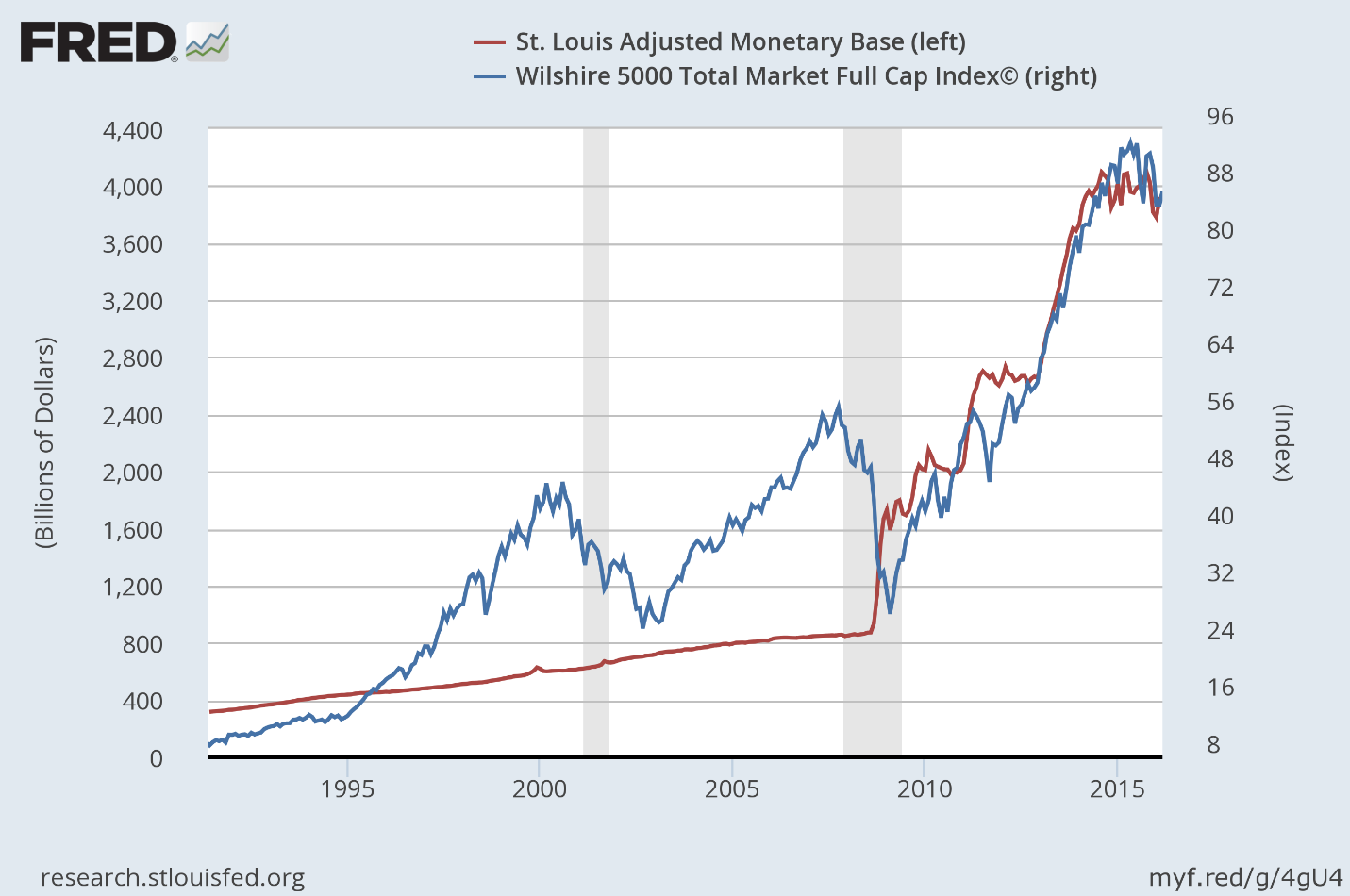

The global economy has been living through a period of central bank insanity, thanks to a little-understood expansion strategy known as quantitative easing, which has destroyed main-street and benefited wall street.

Central Banks over the last decade simply created credit out of thin air. Snap a finger, and credit magically appears. Only central banks can perform this type of credit magic. It’s called printing money and they have gone on therecord saying they are magic people.

Increasing the money supply lowers interest rates, which makes it easier for banks to offer loans. Easy loans allow businesses to expand and provides consumers with more credit to buy goods and increase their debt. As a country’s debt increases, its currency eventually debases, and the world is currently athistoric global debt levels.

Simply put, the world’s central banks are playing a game of monopoly.

With securities being bought by a currency that is backed by debt rather than actual value,we have recently seen $9.7 trillionin bonds with a negative yield. At maturity, the bond holders will actually lose money, thanks to the global central banks’ strategies.The Federal Reserve has already hintedthat negative interest rates will be coming in the next recession.

These massive bond purchases have kept volatility relatively stable, but that can change quickly. High inflation is becoming a real possibility. China, which is planning to dethrone thedollar by backing the Yuan with gold, may survive the coming central banking bubble. Many other countries will be left scrambling. Some central banks are attempting to turn the current expansion policies around. Both the Federal Reserve, the Bank of Canada, and the Bank of England have plans to hike interest rates. The European Central Bank is planning to reduce its purchases of bonds. Is this too little, too late?

The recentglobal populist movementis likely to fuel government spending and higher taxes as protectionist policies increase. The call to end wealth inequality may send the value of overvalued bonds crashing in value. The question is, how can an artificially stimulated economic boom last in a debtors’ economy?

Central bankers began to embrace their quantitative easing strategies as a remedy to the 2007 economic slump. Instead of focusing on regulatory policies, central bankers became the rescuers of last resort as they snapped up government bonds, mortgage securities, and corporate bonds. For the first time, regulatory agencies became the worlds’ largest investment group. The strategy served as a temporary band-aid as countries slowly recovered from the global recession. The actual result, however, has been a tremendous distortion of asset valuationas interest rates remain low, allowing banks to continue a debt-backed lending spree.

It’s a monopoly game on steroids.

The results of the central banks’ intervention were mixed. While a small, elite wealthy segment was purchasing assets, the rest of the population felt the widening income gap as wage increases failed to meet expectations and the cost of consumer goods kept rising. The policies of the Federal Reserve were not having the desired effect. While the Federal Reserve Bank began to reverse its quantitative easing policy, other central banks, such as the European Central Bank, the Swiss National Bank, and the European National Bank have become even more aggressive in the quantitative easing strategies by continuing to print money with abandon. By 2017, the Bank of Japan was the owner of three-quarters of Japan’s exchange-traded funds, becoming the major shareholder trading in the Nikkei 225 Index.

The Swiss National Bank is expanding its quantitative easing policy by including international investments. It is now one of Apple’s major shareholders,with a $2.8 billion investment in the company.

Centrals banks have become the world’s largest investors, mostly with printed money. This is inflating global asset prices at an unprecedented rate. Negative bond yields are just one consequence of this financial distortion.

While the Federal Reserve is reducing its investment purchases, other global banks are keeping a watchful eye on the results. Distorted interest rates will hit investors hard, especially those who have sought out riskier and higher yields as a consequence of quantitative easing (malinvestment).

The policies of the central banks were unsustainable from the start. The stakes in their monopoly game are rising as they are attempting to rectify their negative-yield bond purchasing with purchases of stocks. This is keeping the game alive for the time being. However, these stocks cannot be sold without crashing the market. Who will end up losers and winners? Middle America certainly isn’t going to be happy when the game ends. If central banks continue in their role as stockholders funded by fiat currency, it will change the game completely.

For 8 years, we took every opportunity to point out that under Barack Obama’s administration, US debt was rising at a alarmingly rapid rate,having nearly doubled, surging by $9.3 trillion during Obama’s 8 years. It now appears that the trajectory of US debt under the Trump administration will be no different, and in fact based on Trump’s ambitious fiscal spending visions, may rise even faster than it did under Obama.

We note this because as of close of Friday, theUS Treasury reportedthat total US debt has risen above $21 trillion for the first time; or $21,031,067,004,766.25 to be precise.

Putting this in context, total US debt has now risen by over $1 trillion in Trump’s first year… and the real spending hasn’t even begun yet.

What is amusing is that Trump – who has a tweet for every occasion – and who no longer even pretends to care about the unsustainability of US spending was extremely proud as recently as a year ago by how little debt has increased during his term.

The media has not reported that the National Debt in my first month went down by $12 billion vs a $200 billion increase in Obama first mo.

We doubt today’s milestone will be celebrated on Trump’s twitter account.

And while some can argue – especially adherents of the socialist Magic Money Tree, or MMT, theory – that there is no reason why the exponential debt increase can’t continue indefinitely…

… one can counter with the followingchart from Goldman, which shows that if one assumes a blended interest rate of roughly 3.5% as the Fed does, and keeps America’s debt/GDP ratio constant, in a few years the US will be in what Goldman dubbed “uncharted territory” and warned that “the continued growth of public debt raises eventual sustainability questions if left unchecked.”

The bad news, however, is that debt/GDP will not be constant, as the CBO recently forecast in what was actually an overly optimistic prediction.

Yesterday ZeroHedge explainedthat one of the reasons why Deutsche Bank stock had tumbled to the lowest level since 2016, is because its top shareholder, China’s largest and most distressed conglomerate, HNA Group, had reportedly defaulted on a wealth management product sold on Phoenix Finance according to thelocal press reports. While HNA’s critical liquidity troubles havebeen duly noted here and have been widely known, the fact that the company was on the verge (or beyond) of default, and would be forced to liquidate its assets imminently, is what sparked the selling cascade in Deutsche Bank shares, as investors scrambled to frontrun the selling of the German lender which is one of HNA’s biggest investments.

Now, one day later, we find that while Deutsche Bank may be spared for now – if not for long – billions in US real estate will not be, and in a scene right out of the Wall Street movie Margin Call, HNA has decided to be if not smartest, nor cheat, it will be the first, and has begun its firesale of US properties.

According to Bloomberg, HNA is marketing commercial properties in New York, Chicago, San Francisco and Minneapolis valued at a total of $4 billion as the indebted Chinese conglomerate seeks to stave off a liquidity crunch. The marketing document lists six office properties that are 94.1% leased, and one New York hotel, the 165-room Cassa, with a total value of $4 billion.

One of the flagship properties on the block is the landmark office building at 245 Park Ave., according to a marketing document seen by Bloomberg.

245 Park Avenue, New York

HNA bought that skyscraper less than a year ago for $2.21 billion, one of the highest prices ever paid for a New York office building. The company also is looking to sell 850 Third Ave. in Manhattan and 123 Mission St. in San Francisco, according to the document. The properties are being marketed by an affiliate of brokerage HFF.

This is just the beginning as HNA’s massive debt load – which if recent Chinese reports are accurate the company has started defaulting on – is driving the company to sell assets worldwide.

According to Real Capital Analytics estimates, HNA owns more than $14 billion in real estate properties globally. The problem is that the company has a lot more more debt. As of the end of June, HNA had 185.2 billion yuan ($29.3 billion) of short-term debt — more than its cash and earnings can cover. The company’s total debt is nearly 600 billion yuan or just under US$100 billion. Which means that the HNA fire sale is just beginning, and once the company sells the liquid real estate, it will move on to everything else, including its stake in all these companies, whose shares it has already pledged as collateral.

So keep a close eye on Deutsche Bank stock: while HNA may have promised John Cryan it won’t sell any time soon but companies tend to quickly change their mind when bankruptcy court beckons.

Finally, the far bigger question is whether the launch of HNA’s firesale will present a tipping point in the US commercial (or residential) real estate market. After all, when what until recently was one of the biggest marginal buyers becomes a seller, it’s usually time to get out and wait for the bottom.

In the last major move of Chairwoman Janet Yellen’s reign at the central bank, the Fed said it won’t let Wells FargoWFC, -6.21%add assets beyond the level of the end of 2017 until it improves governance and controls. Wells Fargo ended 2017 with $1.95 trillion in assets.

Wells Fargo will be able to continue current activities including accepting customer deposits or making consumer loans, the Fed said.

“We cannot tolerate pervasive and persistent misconduct at any bank and the consumers harmed by Wells Fargo expect that robust and comprehensive reforms will be put in place to make certain that the abuses do not occur again,” Yellen said in a statement. “The enforcement action we are taking today will ensure that Wells Fargo will not expand until it is able to do so safely and with the protections needed to manage all of its risks and protect its customers.”

The asset cap is unprecedented, according to Federal Reserve officials.

Federal Reserve officials didn’t say it was specifically planned for Yellen’s last day — and they said the bank agreed to the terms on Friday afternoon.

The Fed cited not only the millions of customer accounts Wells Fargo opened without authorization but also more recent revelations that the bank charged hundreds of thousands of borrowers for unneeded guaranteed auto protection or collateral protection insurance for their automobiles.

Wells Fargo will replace three current board members by April and a fourth board member by the end of the year, the Fed said. Sen. Elizabeth Warren, the Massachusetts Democrat, had requested the Fed oust Wells Fargo board members. The Fed didn’t identify which board members will have to leave.

The Fed also singled out Stephen Sanger, the former lead independent director, and former CEO John Stumpf with letters excoriating them for the abuses.

The vote for the sanctions was 3-0, with the incoming chairman, Jerome Powell, joining Yellen and Gov. Lael Brainard. The new vice chairman for regulation, Randal Quarles, abstained.

Quarles previously said he would recuse himself from Wells Fargo matters because he and his family previously had a financial interest in the bank.

In after-hours trade late Friday, Wells Fargo shares dropped over 5%.

Hackers able to make ATMs spit cash like winning slot machines are now operating inside the United States, marking the arrival of “jackpotting” attacks after widespread heists in Europe and Asia, according to the world’s largest ATM makers and security news website, Krebs on Security.

Thieves have usedskimming deviceson ATM machines to steal debit card information, but “jackpotting” augurs more sophisticated technological challenges that American financial firms will face in coming years.

“This is the first instance of jackpotting in the United States,” said digital security reporter Brian Krebs, a former Washington Post reporter. “It’s safe to assume that these are here to stay at this point.”

On his website, KrebsreportedSaturday that the Secret Service has warned financial institutions about “jackpotting” attacks in the past few days, though specifics have not been revealed.

He cites an alert sent by ATM maker NCR Corp. to its customers:

“This represents the first confirmed cases of losses due to logical attacks in the U.S.,” the alert read. “This should be treated as a call to action to take appropriate steps to protect their ATMs against these forms of attack and mitigate any consequences.”

Krebsreportedthat criminal gangs are targeting Diebold Nixdorf ATM machines — the stand-alone kind you might see in a drive-through or pharmacy. He shared the ATM giant’ssecurity notice. It described similar attacks in Mexico, in which criminals used a modified medical endoscope to access a port inside the machines and install malware. Diebold is also one of the largest manufactures of eVoting machines, based upon the same software as their casino slot machines and ATM’s used throughout the Americas and Western Europe.

Both ATM makers confirmed toReutersthat they sent out alerts.

Diebold Nixdorf spokesman Mike Jacobsen declined to provide the number of banks targeted in Mexico and the United States or comment on losses, according toReuters.

Hackers have also been reported to remotely infect ATMs or completely swap out their hard drives. The Secret Service could not be immediately reached for comment about the nature of the reported U.S. attacks.

Whichever method is used, the results are about the same. At a hacker conference in 2010,Wired reported, a researcher brought two infected ATMs to the stage and gave a demonstration.

Over the span of 2000-2016, the amount of money spent on food by the average American household increased from $5,158 to $7,203, which is a 39.6% increase in spending.

Despite this,as Visual Capitalist’s Jeff Desjardins notes, for most of the U.S. population, food actually makes up a decreasing portion of their household spending mix because of rising incomes over time. Just 13.1% of income was spent on food by the average household in 2016, making it a less important cost than both housing and transportation.

That said, fluctuations in food prices can still make a major impact on the population. For lower income households, food makes up a much higher percentage of incomes at 32.6% – and how individual foods change in price can make a big difference at the dinner table.

FLUCTUATING GROCERY PRICES

Today’s infographic comes from TitleMax, and it uses data from the Bureau of Labor Statistics to show the prices for 30 common grocery staples over the last decade.

CBS Local — Many Wells Fargo customers got a terrifying shock after finding their checking accounts drained due to a series of errors by the embattled bank. The Jan. 17 glitch reportedly emptied several customers’ accounts after processing their online bill payments twice and doubling transaction fees.

According toCBS News, the banking error also triggered overdraft fees on many checking accounts as customers around the country were mistakenly informed they had a zero balance. The bank’s phone lines were reportedly jammed through the night as angry customers demanded answers for the embarrassing mistake. Wells Fargo later put out a brief statement on Twitter explaining the situation.

Some customers may be having an issue with their Bill Pay transactions. We are working to fix the issue and resolve this tonight. Thanks for your patience.

The social media outrage was immediate as customers replied to the statement, many who were left without a way to pay for any goods.

Utterly ridiculous, overdraft and in negative, four payments taken out twice…at gas station to be told that WF card has been rejected only then found out by logging into online wellsfargo account. SERIOUSLY!!! I wonder who will compensate the customers for the stress of this!!!

Wells Fargo gave an update on the situation on Jan. 18 as the issue is apparently still unresolved.

“We are aware of the online Bill Pay situation which was caused by an internal processing error. We are currently working to correct it, and there is no action required for impacted customers at this time. Any fees or charges that may have been incurred as a result of this error will be taken care of. We apologize for any inconvenience,” Wells Fargo’s Steve Carlson said, via KCCI.

The glitch is the latest black eye for the company, which was involved in a massive scandal in 2016 after it was discovered Wells Fargo employees opened millions offake accountsto meet sales goals. Several high-level executives at the banking giant have lost their jobs since the scandal broke.

In 1791, the first Secretary of the Treasury of the US, Alexander Hamilton, convinced then-new president George Washington to create a central bank for the country.

Secretary of State Thomas Jefferson opposed the idea, as he felt that it would lead to speculation, financial manipulation, and corruption. He was correct, and in 1811, its charter was not renewed by Congress.

Then, the US got itself into economic trouble over the War of 1812 and needed money. In 1816, a Second Bank of the United States was created. Andrew Jackson took the same view as Mister Jefferson before him and, in 1836, succeeded in getting the bank dissolved.

Then, in 1913, the leading bankers of the US succeeded in pushing through a third central bank, the Federal Reserve. At that time, critics echoed the sentiments of Messrs. Jefferson and Jackson, but their warnings were not heeded. For over 100 years, the US has been saddled by a central bank, which has been manifestly guilty of speculation, financial manipulation, and corruption, just as predicted by Mister Jefferson.

From its inception, one of the goals of the bank was to create inflation. And, here, it’s important to emphasize the term “goals.” Inflation was not an accidental by-product of the Fed – it was a goal.

Over the last century, the Fed has often stated that inflation is both normal and necessary. And yet, historically, it has often been the case that an individual could go through his entire lifetime without inflation, without detriment to his economic life.

Yet, whenever the American people suffer as a result of inflation, the Fed is quick to advise them that, without it, the country could not function correctly.

In order to illustrate this, the Fed has even come up with its own illustration “explaining” inflation. Here it is, for your edification:

If the reader is of an age that he can remember the inventions of Rube Goldberg, who designed absurdly complicated machinery that accomplished little or nothing, he might see the resemblance of a Rube Goldberg design in the above illustration.

And yet, the Fed’s illustration can be regarded as effective. After spending several minutes taking in the above complex relationships, an individual would be unlikely to ask, “What did they leave out of the illustration?”

Well, what’s missing is the Fed itself.

As stated above, back in 1913, one of the goals in the creation of the Fed was to have an entity that had the power to create currency, which would mean the power to create inflation.

It’s a given that all governments tax their people. Governments are, by their very nature, parasitical entities that produce nothing but live off the production of others. And, so, it can be expected that any government will increase taxes as much and as often as it can get away with it. The problem is that, at some point, those being taxed rebel, and the government is either overthrown or the tax must be diminished. This dynamic has existed for thousands of years.

However, inflation is a bit of a magic trick. Now, remember, a magician does no magic. What he does is create an illusion, often through the employment of a distraction, which fools the audience into failing to understand what he’s really doing.

And, for a central bank, inflation is the ideal magic trick. The public do not see inflation as a tax; the magician has presented it as a normal and even necessary condition of a healthy economy.

However, what inflation (which has traditionally been defined as the increase in the amount of currency in circulation) really accomplishes is to devalue the currency through oversupply. And, of course, anyone who keeps his wealth (however large or small) in currency units loses a portion of their wealth with each devaluation.

In the 100-plus years since the creation of the Federal Reserve, the Fed has steadily inflated the US dollar. Over time, this has resulted in the dollar being devalued by over 97%.

The dollar is now virtually played out in value and is due for disposal. In order to continue to “tax” the American people through inflation, a reset is needed, with a new currency, which can then also be steadily devalued through inflation.

Once the above process is understood, it’s understandable if the individual feels that his government, along with the Fed, has been robbing him all his life. He’s right—it has.

And it’s done so without ever needing to point a gun to his head.

The magic trick has been an eminently successful one, and there’s no reason to assume that the average person will ever unmask and denounce the magician. However, the individual who understands the trick can choose to mitigate his losses. He or she can take measures to remove their wealth from any state that steadily imposes inflation upon their subjects and store it in physically possessed gold, silver and private cryptocurrency keys.

One of the most notable events in Russia’s precious metals market calendar is the annual “Russian Bullion Market” conference. Formerly known as the Russian Bullion Awards, this conference, now in its 10th year, took place this year on Friday 24 November in Moscow. Among thespeakers lined up, the most notable inclusion was probably Sergey Shvetsov, First Deputy Chairman of Russia’s central bank, the Bank of Russia.

In his speech, Shvetsov provided an update on an important development involving the Russian central bank in the worldwide gold market, and gave further insight into the continued importance of physical gold to the long term economic and strategic interests of the Russian Federation.

Firstly, in his speechShvetsov confirmed that the BRICS group of countries are now in discussions to establish their own gold trading system. As a reminder, the5 BRICS countriescomprise the Russian Federation, China, India, South Africa and Brazil.

Four of these nations are among the world’s major gold producers, namely, China, Russia, South Africa and Brazil. Furthermore, two of these nations are the world’s two largest importers and consumers of physical gold, namely, China and Russia. So what these economies have in common is that they all major players in the global physical gold market.

Shvetsov envisages the new gold trading system evolving via bilateral connections between the BRICS member countries, and as a first step Shvetsov reaffirmed that the Bank of Russia has now signed a Memorandum of Understanding with China (see below) on developing a joint trading system for gold, and that the first implementation steps in this project will begin in 2018.

Interestingly, the Bank of Russia first deputy chairman also discounted the traditional dominance of London and Switzerland in the gold market, saying that London and the Swiss trading operations are becoming less relevant in today’s world. He also alluded to new gold pricing benchmarks arising out of this BRICS gold trading cooperation.

BRICS cooperation in the gold market, especially between Russia and China, is not exactly a surprise, because it was first announced in April 2016 by Shvetsov himself when he was on a visit to China.

“We (the Central Bank of the Russian Federation and the People’s Bank of China) discussed gold trading. The BRICS countries (Brazil, Russia, India, China and South Africa) are major economies with large reserves of gold and an impressive volume of production and consumption of the precious metal. In China, gold is traded in Shanghai, and in Russia in Moscow. Our idea is to create a link between these cities so as to intensify gold trading between our markets.”

Also as a reminder, earlier this year in March, theBank of Russia opened its first foreign representative office, choosing the location as Beijing in China. At the time, the Bank of Russia portrayed the move as a step towards greater cooperation between Russia and China on all manner of financial issues, as well as being a strategic partnership between the Bank of Russia and the People’s bank of China.

The Memorandum of Understanding on gold trading between the Bank of Russia and the People’s Bank of China that Shvetsov referred to was actuallysigned in Septemberof this year when deputy governors of the two central banks jointly chaired an inter-country meeting on financial cooperation in the Russian city of Sochi, location of the 2014 Winter Olympics.

Deputy Governors of the People’s Bank of China and Bank of Russia sign Memorandum on Gold Trading, Sochi, September 2017. Photo: Bank of Russia

National Security and Financial Terrorism

At the Moscow bullion market conference last week, Shvetsov also explained that the Russian State’s continued accumulation of official gold reserves fulfills the goal ofboosting the Russian Federation’s national security. Given this statement, there should really be no doubt that the Russian State views gold as both as an important monetary asset and as a strategic geopolitical asset which provides a source of wealth and monetary power to the Russian Federation independent of external financial markets and systems.

And in what could either be a complete coincidence, or a coordinated update from another branch of the Russian monetary authorities, Russian Finance Minister Anton Siluanov also appeared in public last weekend, this time on Sunday night on a discussion program on Russian TV channel “Russia 1”.

Siluanov’s discussion covered the Russian government budget and sanctions against the Russian Federation, but he also pronounced on what would happen in a situation where a foreign power attempted to seize Russian gold and foreign exchange reserves.According to Interfax, and translated here into English, Siluanov said that:

“If our gold and foreign currency reserves were ever seized, even if it was just an intention to do so, that would amount to financial terrorism. It would amount to a declaration of financial war between Russia and the party attempting to seize the assets.”

As to whether the Bank of Russia holds any of its gold abroad is debatable, becauseofficiallytwo-thirds of Russia’s gold is stored in a vault in Moscow, with the remaining one third stored in St Petersburg. But Silanov’s comment underlines the importance of the official gold reserves to the Russian State, and underscores why the Russian central bank is in the midst of one of the world’s largest gold accumulation exercises.

1800 Tonnes and Counting