The latest oil price spike may turn out to be a head-fake, because the economy is already slowing. While the oil cartel can try to fix the supply of oil, it can’t really control the demand side, which is dominated by the economic cycle.

This is clear to us at ECRI because of our enduring focus on cyclical relationships and, in this case, sensitive industrial material prices, including oil. We’ve long maintained a daily price index of these commodities that moves in concert with cycles in industrial growth. About half of the price inputs we monitor are traded on various commodity exchanges, while the rest are priced from commodity producers.

For the past few quarters a very unusual gap has opened up between the two groups, with the prices of non-exchange-traded industrial commodities, which most observers don’t watch, falling, and in some cases plunging. This behavior is in sharp contrast to the bullish sentiment shown, until more recently, by the strength in the prices of commonly-watched exchange-traded commodities.

As the chart shows, because of their links to industrial growth, exchange-traded and non-exchange-traded commodity price inflation rates have historically moved very much in sync.

But the right-side of the chart shows exchange-traded commodity price inflation spiking up through early this year, driven by widely-watched industrial inputs like oil and copper, while non-exchange traded commodity inflation went straight down into negative territory, as the prices of raw materials like rubber and hides dropped precipitously. This is very unusual.

This undeniable weakness in the non-exchange traded commodity prices is in line with our March Bloomberg View Op-ed,The Global Economy’s Wile E. Coyote Moment, about the end of the 2016-17 synchronized global growth upturn. The current downturn in global industrial growth has caught many people off guard because they focus on exchange-traded commodities only. Doing so made it easier to think that demand wasn’t slowing because surging oil and primary metals prices had camouflaged what was really happening.

ECRI’s insight was that the rise in exchange-traded prices was not about demand, which we knew was slowing. Rather, it was about the confluence of a variety of supply shocks, which weren’t cyclical, and thus unsustainable.

Of course, Saudi Arabia and Russia had deliberately kept oil production in check to support oil prices. But also, aluminum and nickel prices had shot up on fears of U.S. sanctions on Russia. Copper prices had surged due to labor problems at major mines, and rule changes regarding Indonesian tin export permits had also caused supply shortages. Meanwhile, zinc prices were pushed up by the shutdown of major Australian, Irish and Canadian mines and China’s environmental clampdown, which had lifted lead prices. What’s more, those pollution controls also hurt the production of synthetic fabrics, which therefore couldn’t make up for the shortfall in Indian cotton exports caused by pink bollworms eating into the cotton supply. It really was this perfect storm of supply constraints – not the strength of global demand – that drove the earlier run-up in these exchange-traded commodity prices.

Stepping back, the real tip-off came from the earlier downturns in ECRI’s leading indexes of global industrial growth, which were then followed by the yawning gap between exchange-traded and non-exchange-traded commodity price inflation that opened up months ago. It’s only in recent weeks that exchange-traded commodity price inflation has turned down. It’s no coincidence that the Eurozone manufacturing PMI just dropped to a 1½-year low and its U.S. counterpart fell to a seven-month low.

Today, growth in the non-exchange-traded commodity prices remains negative, and growth in the exchange-traded commodity prices is closing the gap by dropping to an 11-month low. With the global industrial slowdown manifesting in all these very short-leading indicators, the market may soon start asking if global demand is all it’s cracked up to be.

Good news within a strenuously spunReuters article. Don’t get lost looking at the granules; apparently all of the prior Canadian strategy against President Trump has failed.

For well over a year Justin from Canada and Foreign Minister Chrystia Freeland were confident they could leverage theU.S. Chamber of Commerce, purchased DC politiciansand ideological allies against President Trump in NAFTA negotiations. The result?Fail, failandmore fail.

Running out of options, Canada now attempts to save their NAFTA construct by turning to the executives within the auto industry:

OTTAWA (Reuters)– Canada’s trade minister last week met senior officials from General Motors Co and Fiat Chrysler Automobiles NV in Detroit, as Ottawa takes its lobbying effort directly to the Big Three car makers to avert potential U.S. auto tariffs.

The Liberal government is relying on industry partners to press Canada’s cause in the White House and elsewhere, using their influence to protect Canadian interests, sources with direct knowledge of the discussions told Reuters.

The auto industry, Canada’s biggest exporter, represents about 500,000 direct and indirect jobs and contributes C$80 billion ($60.1 billion) a year to the economy.

“Instead of us galloping all over the United States talking to everybody, it’s really focused right now on the automobile manufacturers, the automobile suppliers,” said one source, who requested anonymity given the sensitivity of the situation.

The Canadian message was “now is the time to speak up, now is the time to exercise whatever influence you might be able to bring to bear,” added the source. (read more)

Or put another way…. “Halp”!

Each sequential step in the Trump trade strategy is designed to head-off any counter position by positioning individual best-interests ahead of any defensive group formation.

The Canadian and Mexican economy (due to NAFTA) cannot survive without importing cheap durable goods from China to use in their assembly-based economies, and then trans-ship into the U.S market. However, the U.S. economy can survive, it can actually expand BIGLY and thrive, without accepting trans-shipped assembled goods from Mexico and Canada.

Put simply, without NAFTA, the assembly processes just moves INTO the U.S because the market *is* the United States. We are the $20 trillion customer. We hold the leverage.

NOTE: “Donnelly said in his opening remarks that there was already a rise in product being diverted to Canada in recent years and signs of even more since the U.S. tariffs began this year.”..

This is evidence of multinationals exploiting the NAFTA loophole to avoid U.S. tariffs. This fatal flaw is at the very heart of the issue within the U.S. trade policy inside NAFTA. As long as Mexico and Canada remain gateways for foreign good assembly and shipment into the U.S. there will never be a way for the U.S. to demand fair and reciprocal trade.

Canada knows their decades-long designed economic position as shipment/assembly trade-brokers is the central issue at the heart of the confrontation with USTR Lighthizer, Commerce Secretary Ross and President Trump. As multinational corporations seek to avoid Trump tariffs they only exacerbate the issue.

If Canada and Mexico don’t try to stop their duplicitous NAFTA benefit scheme, they will end up with even bigger trade surpluses and become even bigger targets for President Trump. In essence, the reason for Canada and Mexico being subject to even more encompassing Trump tariffs’ grows.

If Canada and Mexico do nothing to stop this influx; Trump will levy more than just steel and aluminum tariffs;he’ll likely tax their auto-sector.

As a consequence Canada moves do back down the Red Dragon:

The Canadian government is preparing new measures to prevent a potential flood of steel imports from global producers seeking to avoid U.S. tariffs, according to people familiar with the plans. The Canadian dollar weakened and shares inStelco Holdings Inc.soared.

The measures are said to be a combination of quotas and tariffs aimed at certain countries including China, said the people, asking not to be identified because the matter isn’t public. The moves follow similar “safeguard” measuresbeing consideredby the European Union aimed at warding off steel that might otherwise have been sent to the U.S. It comes alongside Canadian counter-tariffs on U.S. steel, aluminum and other products set to kick in on July 1. (read more)

The bottom line is U.S. market access is what all production countries need for their goods and the sustainability of their economies.

***

The depths of depravity to which both the Clinton and Obama Administrations dove to in their perversely industrious efforts to self-enrich while simultaneously demeaning, undermining, and selling-out all of America to foreign interests is incredibly stunning. And, they even had the entire DOJ rigged to get away with it all scot-free. It is practically surreal.

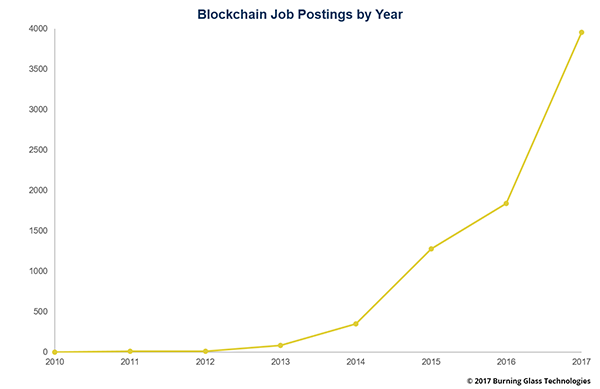

The Digital Currency Research Lab at the People’s Bank of China has filed more than 40 patent applications so far – all as part of an aim to create a digital currency combining the core features of cryptocurrency and the existing monetary system.

A national digital fiat currency, say what?

Data from China’s State Intellectual Property Office (SIPO) revealed two new patent applications on Friday, pushing the total number submitted by the lab to 41 over the 12 months since itslaunch.

Each of the 41 patent applications focuses on a certain aspect of a digital currency system, and, when combined, would create a technology that issues a digital currency, as well as provides a wallet that stores and transacts the asset in an “end-to-end” fashion.

For instance, the most recently revealed patent application explains how the envisioned digital wallet would allow users to check any transactions made through the service, while earlier documents offered details on how the wallet can facilitate transactions.

The ultimate goal, according to PBoC’s patents, is to “break the silo between blockchain-based cryptocurrency and the existing monetary system” so that the digital currency can sport cryptocurrency-like features, while being widely used in the existing financial structure.

Last week’s patents further explain that the envisioned wallet would not be limited, like a typical cryptocurrency wallet, to merely storing the private key to a certain asset. Nor would it be like another mobile payment service that only reflects a number on an application’s front-end interface without users actually holding the assets in a peer-to-peer manner.

Instead, the patents indicates the wallet would store a digital currency issued by the central bank or any authorized central entity that is encrypted like a cryptocurrency with private keys, offers multi-signature security and is held by users in a decentralized way.

The research lab said in one of the documents that it believes it is building a mechanism that makes a crypto-featured digital currency more applicable in the financial world.

The hybrid approach is also in line with opinions shared by the PBoC’s vice governorFan YifeiandYao Qian, the head of the research lab, who have both argued for a balance between the two polars of centralization and decentralization.

Overall, the patent applications filed so far signal the continuous efforts made by China’s central bank to develop its own central bank digital currency, as well as to potentially widen the application’s role among other central institutions.

The lab notably commented in a patent application released in November 2017:

“The virtual currencies issued by private entities are fundamental flaws given their volatility, low public trust, and limited useable scope. … Therefore, it’s inevitable for the central bank to launch its own digital currency to upscale the existing circulation of the fiat currency.”

Read one of the most recent patent applications below:

Plaintiffs charged that BofA lent the scheme an air of legitimacy and provided critical support

Bank of America Corp.was accused in a lawsuit of providing more than 100 accounts used to perpetrate what the U.S. regulators called a $102 million Ponzi scheme.

The class-action suit filed on behalf of people who lost money follows a complaint last week by the Securities and Exchange Commission alleging that five men and three companies defrauded more than 600 investors.

One of the alleged ringleaders once commissioned a song about himself for a party in Las Vegas with lyrics celebrating his $10,000 suits and his partner’s affinity for champagne, according to Monday’s complaint in federal court in Ocala, Florida.

The brother and sister who sued to recover losses from their late father’s investment claim the fraudsters “could not have perpetuated their scheme without the knowing assistance of their primary banking institution, Bank of America, which lent the scheme an air of legitimacy and provided critical support, including at times when the scheme would have otherwise collapsed,” according to the complaint.

Bank of America spokesman Bill Halldin had no immediate comment on the suit.

The lender is accused of failing to spot suspicious activity, including deposits of hundreds of thousands of dollars into accounts with relatively small, negative or nonexistent balances, followed by transfers within the same week to other accounts or investors seeking to cash out.

The architects of the scheme promised they would put investor funds into profitable and perhaps dividend-paying companies, according to the SEC. But they spent $20 million from the investment pool to enrich themselves, made $38.5 million in “Ponzi-like payments” and transferred much of the rest away from the companies that were supposed to receive the money, the regulator said.

(Bloomberg) — The billionaire George Soros has found a new way to make money from personal-injury lawsuits.

Soros Fund Management is pushing into a branch of litigation finance that few hedge funds have entered. His family office is bankrolling a company that’s creating investment portfolios out of lawsuits, according to a May regulatory filing.

The development is the latest twist on the litigation funding market, which has drawn criticism for monetizing and encouraging the lawsuit culture in the U.S. The firm Soros is backing,Mighty Group, bundles cash advances that small shops extend to plaintiffs in personal injury suits in return for a cut of future settlements. Mighty Group’s approach opens the door to another potential development: securitizing individual lawsuit bets for sale to other investors.

“There are all the ingredients there to securitize these things,” said Adrian Chopin, a managing director at legal finance firm Bench Walk Advisors. “A diversified, granular pool with predictable outcomes. The problem is, you can’t yet get these things rated” by credit agencies.

20% Returns

Wall Street has been betting for a while on commercial litigation, which provides financing of big corporate suits with millions or even billions of dollars at stake. Soros is focused on the consumer side, where plaintiffs receive advances of $2,000 on average for legal claims typically tied to auto and construction accidents. The advances are used to cover personal expenses, such as medical bills and rent.

Soros along with Apollo Capital Management are among the first money managers to jump into this niche of the lawsuit-funding market. It offers steady and predictable returns, which historically have averaged about 20 percent a year at relatively low risk, said Chopin of Bench Walk.

“Everybody is looking for yield, and people are also looking for assets that are not correlated with the major equity and debt markets,” said Christopher Gillock, a managing director at Colonnade Advisors, an investment bank that specializes in financial services. “Litigation funding falls into that category.”

Joshua Schwadron, a co-founder of Mighty, declined to comment on the firm’s investors. Michael Vachon, a spokesman for Soros Fund Management, the billionaire’s New York-based family office, declined to comment.

Political Risk

The investments come with risk from both sides of the political spectrum. The U.S. Chamber of Commerce and the insurance industry criticize litigation financing for clogging the courts with frivolous lawsuits and driving up the costs of settlements. Regulators, on the other hand, have taken the side of consumers, moving to rein in the advances, casting them as loans subject to usury laws.

Industry proponents say the funding helps people win appropriate payouts instead of settling for pennies on the dollar under the pressure of medical bills or missed income from work. In addition, plaintiffs don’t have to pay back the advances if they lose their cases.

“These funding companies are allowing the folks who are injured through some accident to be able to stick around long enough to get paid,” said Joel Magerman, chief executive officer of Bryant Park Capital, an investment bank.

The funding companies don’t always get fully paid since other claims on settlements, such as attorney fees, have priority. This risk of underpayment makes advances difficult to bundle into securities, said Eric Schuller, president of the Alliance for Responsible Consumer Legal Funding, an industry trade group. In contrast to advances, most securitizations are backed by tangible items like a home or car.

“If the case goes south, there is nothing there to go after,” Schuller said. “It’s just a piece of paper.”

Apollo’s Investment

Mighty, originally a software provider, announced in March it had raised more than $100 million from major institutional investors to help litigation finance firms access capital. The May filing shows that a Soros affiliate agreed to provide Mighty with financing, which can also be used to back lawyers’ contingency fees and medical bills slated to be paid when cases settle.

Soros’s move into consumer legal funding is somewhat akin to another investment his family office made last year. It participated in a joint deal to buy as much as $5 billion of loans from Prosper Marketplace, a pioneer in peer-to-peer lending.

Although this form of litigation financing dates back to the mid-1990s, hedge funds had mostly steered clear because the advances and firms that issued them are so small. Only the largest players have been able to obtain financing from big investment firms. For example Leon Black’s Apollo Capital, through its MidCap Financial affiliate, backs Golden Pear Funding of New York, one of the biggest providers of advances.

Magerman anticipates that more investors will jump in the market. “It’s a small niche asset class,” he said. “There is a lot of additional money that can come in.”

***

Here’s your need to know about George Soros…

Host

You’re a Hungarian Jew who escaped the holocaust by posing as a Christian.

Soros

Right.

Host

And you watched lots of people get shipped off to the death camps?

Soros

Right, I was 14 years old and I would say that’s when my character was made.

Host

In what way?

Soros

That one should understand and anticipate events… It was a tremendous threat of evil. It was a very personal experience of evil.

Host

My understanding is that you went out with this “protector” of yours who swore that you were his adopted godson.

Soros

Yes.

Host

… went out, in fact, and helped in the confiscation of property of the Jews.

Soros

That’s right. Yes.

Host

That sounds like an experience that would send lots of people to the psychiatric couch for many, many years. Was it difficult??

Soros

Uh. Not at all, not at all. Maybe as a child you don’t see the connection but it created no problem at all.

Host

No feeling of guilt?

Soros

No.

Host

For example, “I’m Jewish and here I am watching these people go. I could just as easily be there. I should be there.” None of that?

Soros

Well. Of course I could be on the other side. I could be the one from whom the thing is being taken away, uh, but there was no sense I shouldn’t be there because there was – Well, actually, (in a) funny way it’s just like in markets that if I weren’t there (of course I wasn’t doing it) somebody else would be taking it away anyhow. Whether I was there or not (I was only a spectator) the property was being taken away. So – I had no role in taking away that property so I had no sense of guilt.

President Trumpdoubled-down on his planfor “immediate” deportation of illegal immigrants this morning, explaining in a tweet that “hiring many thousands of judges, and going through a long and complicated legal process, is not the way to go,” adding that this deterrence approach “is the way to go to stop illegal immigration in its tracks.”

Hiring manythousands of judges, and going through a long and complicated legal process, is not the way to go – will always be disfunctional. People must simply be stopped at the Border and told they cannot come into the U.S. illegally. Children brought back to their country……

….If this is done, illegal immigration will be stopped in it’s tracks – and at very little, by comparison, cost. This is the only real answer – and we must continue to BUILD THE WALL!

But,as NBC News reports,that hasn’t stopped civil rights attorneys from flocking to the Texas border to ‘protect’ the rights of illegal immigrant parents not to be separated from their children – the exact same policy that is utilized on American parents when they commit a crime with children in tow.

Attorneys have become a lifeline for migrants in detention, responding as would clergy to a disaster or tragedy, as the legal labyrinth of immigration has become more complicated.

Although many are accustomed to the immigration system’s complexities, attorneys are finding the situation created by the Trump “zero-tolerance” prosecutions full of never-before-seen hurdles and restrictions that hamper their access to children and parents and are making their work to ensure those with valid asylum and other claims get to stay more difficult.

Ali Rahnama, an immigration attorney from Washington, D.C. who works on public policy and high impact litigation, said he woke up last Monday and felt he needed to be on the border. He found a private donor to pay for him and a few colleagues to fly to the border.

Another attorney, Sirine Sheboya, is choking back emotion over the lengths mothers and fathers are going to be reunited with their children.

“We have people in there who are considering not continuing on with really strong asylum claims,” she said stopping to catch her breath as the emotion breaks through, “because they think that maybe they will get reunified with their kids faster if they give up their claim. That’s just wrong.“

“We have men and women saying, ‘My 5- and 6-year-old was holding my leg and was taken away,'” said Rahnama, who visited parents and guardians being held in the Port Isabel Detention Center. “They go to court and are told their child will be there when they come back and they come back and there is no child,” he said.

Of course, it’s not just attorneys, Democratic politicians are descending for their moment of social justice and never-Trump warrior glory.

Sen. Elizabeth Warren, D-Mass., spent 2½ hours in the Port Isabel Detention Center on Sunday night. After the visit, she told reporters stationed outside the center that officials of Immigration and Customs Enforcement told her that the center isn’t where parents and children will come together as federal officials have said.

“The [immigration] officials made clear this is not a reunification center. There will be no children brought here. There will be no families brought together in this place,” Warren said. “All that’s happening here is the detention of mothers and fathers who lost their children.”

Warren said she spoke to nine mothers and none the whereabouts of their children or had spoken to them.

“They are crying they are weeping,” she said. “They have said they will do anything … just, please, let them have their babies back.”

One quick question to Ms.Warren – what would you do with the children of an American parent, who took his children along with him as he committed a crime? Do they deserve better or worse treatment under the law than an illegal immigrant – who crosses the border not at a port of entry and then proclaims they are seeking asylum?

NBC News reportsthat DHS said late Saturday that some of the more than 2,000 children – about 522 – have been reunited with parents. Officials said Port Isabel would be its reunification center.

Sometimes it’s not just children who attorneys have to locate, but some of the parents as well. Efrén Olivares of the Texas Civil Rights Project can no longer find three clients who were part of a group of five parents who complained in a petition filed with the Inter-American Human Rights Commission, part of the Organization of American States, about the child separations.

“They were either released to the U.S. with notice to appear (at a court at a later date) or were deported. We are looking diligently to contact them. We gave them a number and asked them to contact us if they were released,” Olivares said.

“We have not heard from them.”

Surprise!

Here is immigration expert Steve Cortes corrected host Fredricka Whitfield on the reality of family separation at the U.S. southern border during CNN’s Newsroom Sunday (via The Daily Caller)…

The U.S. Border Patrol does not separate immigrant families who claim asylum if they appear at a legal point of entry to the U.S., Cortes, the former head of President Donald Trump’s Hispanic Advisory Council, said.

Until recently, only the families that tried to come into the country outside a point of entry – making them illegal immigrants – were separated.

Trump issued an executive order Wednesday that directed the Border Patrol to detain illegal immigrant families together and to begin reuniting children with their detained parents.

Whitfield asked Cortes how he thought Trump’s plan to reunite “immigrant families” would work out.

“Look, it will be a difficult process, but here’s the thing. The best way for — when you say immigrant families, by the way, it’s important to say illegal immigrant families,” Cortes responded, pointing out the omission. “That’s a very, very important adjective to add in there. Immigrant families have never been separated.”

“Illegal immigrant families have been separated, and I would say separated for a very good reason,” Cotez continued. “Why? Because their parents, unfortunately, or guardians … decided to commit a crime with children in tow. Much like an American committing a crime with children in tow, you get separated from you children. And that’s a terrible consequence for the kids.”

Whitfield defended her characterization of immigrants crossing the border illegally, pointing out that many were crossing the border seeking asylum.

“If you show up to a port of entry in the United States with your children and request asylum lawfully, you are not separated from your family,” Cortes shot back, referring to the difference between applying for affirmative and defensive asylum.

Affirmative asylum applies to immigrants entering the U.S. at a port of entry, or immigrants who apply within a year of entering the U.S., whether or not their entry was legal. Immigrants entering the country illegally can apply for defensive asylum while they are being processed for deportation.

“It’s not [legal]. You have to come to a check point, raise your hand and say, ‘I’m here for asylum,’” Cortes said.

“You can’t sneak across the border and then say, once you’re caught, ‘Oh, I meant to apply for asylum. That’s just not correct.”

Finally, we note another of President Trump’s tweets this morning that sums the state of America and its media up very well…

Such a difference in the media coverage of the same immigration policies between the Obama Administration and ours. Actually, we have done a far better job in that our facilities are cleaner and better run than were the facilities under Obama. Fake News is working overtime!

And while we are well aware that comprehending the facts behind this sudden maelstrom of migrant misery headlines, here is the reality of how this all started courtesy of‘The Last Refuge’ excellent twitter thread…

1.Once you see the strings on the marionettes you can never watch the pantomime the same way you did before you noticed them.

2. DATELINE – May 2011 – President Obama travels to the Rio Grande sector of the border to push for his immigration platform (ie. Amnesty). He proclaims the border is safe and secure and famously attacks his opposition for wanting an “alligator moat”.

3. November 2012 – Election year campaign(s). Using wedge issues like “War on Women”, and “Immigration / Amnesty”, candidate Obama promises to push congress for “amnesty”, under the guise of “Comprehensive Immigration Reform”, if elected.

President Obama wins reelection.

4. December 2012 – Immediately following reelection President Barack Obama signs an Executive Ordercreating the “Deferred Action Program“, or DACA. Allowing millions of illegal aliens to avoid deportation.

5. According to White House own internal documents and research, this Deferred Action Program is what the Central American communities immediately began using as the reason for attempted immigration.

7. May 2013 – President Barack Obama visits South America. Following a speech for Mexican entrepreneurs, Obama then traveled to Costa Rica, his first visit as president.

9. The regional network includes the leaders of Belize, El Salvador, Guatemala, Honduras, Nicaragua and Panama. President Obama meets with the leaders of the Central American Countries.

10. Summer 2013 – Numbers of Illegal Unaccompanied Minors reaching the Southern U.S. border from El Salvador, Guatemala, Honduras, Nicaragua doubles. 20,000+ reach U.S. Southern border by travelling through Mexico. Media primarily ignores.fpc.state.gov/documents/orga…

11. October 2013 – At the conclusion of the immigrant travel season. White House receives notification that tens of thousands of illegal Unaccompanied Minors should be anticipated to hit the Southern U.S. border the following Summer [2014].

12. An estimated 850% increase in the number of Unaccompanied Alien Children (UAC’s) were reported to the White House.fpc.state.gov/documents/orga…

[In 2012 less than 10,000 were projected]

13. January 2014 – In response to the projections, the Department of Homeland Security (DHS) posts a jobs notification seeking bids to facilitate 65,000 Unaccompanied Alien Children.fbo.gov/index?s=opport…

14. IMPORTANT. This job posting was January 2014.The Obama administration was *planning for* 65,000 childhood arrivals. In January 2014 they were taking contractor bids for services to be used later in year. Almost no-one noticed.

15. On January 29, 2014, the federal gov. posted an ad seeking bids for a vendor contract to handle “Unaccompanied Alien Children“. Not just any contract mind you, a very specific contract – for a very specific number of unaccompanied minors: “65,000.”fbo.gov/index?s=opport…

17. Spring 2014 – With a full year of DACA, successful transport and border crossing without deportation – DHS begins to notice a significant uptick in number of criminal elements from El Salvador, Guatemala, Honduras and Nicaragua; which have joined with UAC’s to gain entry.

19. June 2014 – Tens-of-thousands of UAC’s from El Salvador, Guatemala, Honduras and Nicaragua hit the border and the headlines. Despite the known planning, and prior internal notifications, the White House claims it did not see this coming.

21. June 20th 2014 – Congressional leadership and key Latino Democrats from the Democrat Hispanic Caucus meet with representatives from El Salvador, Guatemala, Honduras and Mexico.kfgo.com/news/articles/…

23. July 3rd, 2014 – President Obama requests $3,700,000,000 ($3.7 billion) in supplemental budget appropriations to deal with the border crisis. Only $109 million is for actual border security or efforts to stop the outflow from El Salvador, Guatemala, Honduras, and Nicaragua.

24. Hidden inside the massive budget request is Obama seeking legal authorization to spend taxpayer funds for lawyers and legal proceedings on behalf of UAC’s and their families. Congress is being asked to approve/fund executive branch’s violation of immigration law (DACA).

26. July 10th, 2014 – Facing pushback from congress as well as sticker shock at the amount he is requesting, President Obama sends his DHS team to Capitol Hill to ramp up anxiety, and threats of consequences:politico.com/story/2014/07/…

27. “We are preparing for a scenario in which the number of unaccompanied children apprehended at the border could reach up to 90,000 by the end of fiscal 2014,” Johnson’s testimony reads:politico.com/story/2014/07/…

28. Not only did the White House know what was going to happen (as far back as 2012), but White House actually constructed events to fall into a very specific pattern and intentionally did NOTHING to stop the consequences from the DACA executive order issued in December 2012.

29. This is the origin of the crisis.It all started with DACA. Having tracked this issue so closely through the years it often feels futile to discuss. It is an ongoing insufferable political game/scheme within the issue of illegal immigrants and “children”.

30. Massive illegal immigration is supported by both sides of the professional political machine. There are few issues more unifying for the K-Street purchased voices of DC politicians than keeping the borders open and the influx of illegal aliens as high as possible.

31. The U.S. Chamber of Commerce pays politicians to keep this system in place. All Democrats and most Republicans support mass immigration. Almost no DC politicians want to take action on any policy or legislation that stops the influx.

32. There are billions at stake. None of the GOP leadership want to actually stop illegal immigration; it’s a lucrative business. Almost all of the CONservative groups and politicians lie about it.

33. The religious right is also part of the problem. In the past 15 years illegal immigration and refugee settlement has been financially beneficial for them.

34. There is no greater disconnect from ordinary Americans on any singular issue than the policy positions of Democrats and Republicans in Washington DC surrounding immigration.

President Donald Trump is confronting their unified interests.

35. All political opposition to the Trump administration on this issue is structured, planned & coordinated. The issue is a valuable tool for the professional political class to sow chaos amid politicians. The resulting crisis is useful for them; therefore they fuel the crisis.

36. Washington DC and the activist media, are infested with illegal immigration supporters; the issue is at the heart of the UniParty. Follow the money. It’s the Acorn business model:

37. Southwest Key has been given $310,000,000, in taxpayer funds so far in 2018. And that’s just one company, in one part of a year. Prior CTH research showed this specific “Private Company” nets 98.76% of earnings from government grants.taggs.hhs.gov/Detail/RecipDe…

38. Lutheran Immigration and Refugee Service, which provides foster care and other child welfare services to migrant children. “Faith Based Immigration Services” is a code-speak for legalized human smuggling.taggs.hhs.gov/Detail/RecipDe…

39. The “faith-based” crew don’t want it to stop, because facilitating illegal alien import is now the financial bread and butter amid groups in their base of support.taggs.hhs.gov/Detail/RecipDe…

40. The man/woman in the pew might not know; but the corporation minister, preacher or priest (inside the process) surely does. BIG BUSINESS !!taggs.hhs.gov/Detail/RecipDe…

41. These immigration groups, get *MASSIVE* HHS grants and then pay-off the DC politicians and human smugglers. Billions of dollars are spent, and the business end of immigration has exploded in the past six years.

42. It’s a vicious cycle. Trafficked children are more valuable than adults because the organizations involved get more funding for a child than an adult. Each illegal alien child is worth about $56,000 in grant money. The system is full of fraud.

43. Approximately 65% of the money HHS provides is spent on executive pay and benefits, opaque administrative payrolls, bribes, kick-backs to DC politicians and payoffs to the South American smugglers who bring them more immigrants.

45. All of those advocates gnashing their teeth and crying on television have no idea just who is controlling this process; and immigration idiots like Ted Cruz are only adding more fuel, more money, to the bottom line:

"This has to stop," Texas Sen. Ted Cruz said when asked about the separation of migrant families at the border in his state.

He'll also be introducing legislation "that will mandate that kids must stay with their parents." pic.twitter.com/2j0Z515d88

46. By threatening to secure the border, President Trump is threatening a Washington DC-based business model that makes money for a lot of connected interests.

47. Beyond enrichment schemes, the entire process of immigration, and Washington-DC legalized human smuggling, has side benefits for all the participants; child sexploitation, child labor, and yes, much worse (you can imagine).

48. So the next time you see this type of terribly misplaced “crying girl” corporate propaganda:

49. Maybe, just maybe, we can remember the *real* consequences of actual legalized human smuggling that has been created -within the business- by U.S. political policy. This “crying girl”:

In April, an op-ed in The Wall Street Journal titled “So Long, California. Sayonara, New York,” published by conservative economists Arthur Laffer and Stephen Moore, warned about a provision within the brand- new tax bill that could trigger a mass migration of roughly 800,000 people — fleeing California and New York for low-tax states over the next several years.

Now that the SALT subsidy is passed, how bad will it get for high-tax blue states, and more specifically New York?

New evidence suggests that New York City could be the first visible region where the mass migration could begin. Take, for example, the number of homes listed for sale in Manhattan, Brooklyn, and Queens had a parabolic spike in May, with inventory across 60 percent of the boroughs reaching all-time highs, according to the latestStreetEasy Market Report. While residential inventory traditionally peaks at the end of May, this year — the supply set new record highs and could continue through summer.

Laffer and Moore’s prophecy (above) of the great migration from New York – triggered by Trump’s new tax bill could be the most logical explanation of why NYC homeowners are rushing all at once to sell their homes.

Housing inventory in Manhattan rose 16.7 percent compared to last year, the largest y/y increase on StreetEasy record. Brooklyn and Queens saw similar spikes, with inventory up 23.4 percent and 42.8 percent, respectively.

With housing inventory piling up across much of the boroughs, the total number of sales declined for the third consecutive month. StreetEasy said sales plummeted in every submarket across Brooklyn, Manhattan, and Queens; with more significant declines visible in the Upper East Side, Midtown and the Rockaways. Despite the flood of new inventory threatening to stall the market, the StreetEasy Price Index advanced in all three boroughs since last year.

“Sellers are betting on a wave of demand from the peak shopping season, but this summer’s market has turned out to be a crowded one,” says StreetEasy Senior Economist Grant Long.

“However, prices are high and continue to rise. More affordable homes are the hardest to find, and are sure to sell quickly. But higher-end homes, particularly those joining the market from the ongoing stream of new development, will be pressured to lower prices or linger on the market.

This summer is poised to offer an excellent negotiating opportunity for buyers with big budgets.”

As Bloomberg notes, the abnormal amount of supply hitting the NYC residential markets is not sufficiently being met with demand, which could eventually be problematic for prices and serve as a potential turning point. Recently, the mainstream media cleverly changed their narrative and called the ‘housing shortage,’ a ‘housing affordability crisis,’ as it sure seems that the housing bubble, or whatever you want to call it, is in the later innings.

May 2018 Key Findings — Manhattan

Sale prices rose in all submarkets but one. The StreetEasy Manhattan Price Index increased 0.6 percent to $1,157,995. Prices rose in four of the five submarkets, led by an increase in the Upper East Side, where the median home price rose 1.9 percent to $1,038,046. Prices in Downtown Manhattan remained flat at $1,691,204.

Inventory rose at a record pace. Sales inventory in Manhattan rose 16.7 percent year-over-year. The Upper East Side experienced the largest increase, with inventory up 20.2 percent since last year.

One out of every six homes received a discount. Sixteen percent of homes for sale were discounted, an increase of 3.6 percentage points year-over-year.

For-sale homes spent less time on the market. Units in the borough spent a median of 55 days on the market, a three-day dip from last year. The Upper East Side and Upper West Side were the only submarkets where homes lingered longer — up 10 days and 17 days, respectively.

Rents rose in every Manhattan submarket. The StreetEasy Manhattan Rent Index [iv] rose 1.4 percent to $3,183. Rents in Upper Manhattan rose the most — up 2.5 percent to $2,307.

Fewer rentals offered a discount. Sixteen percent of rentals in Manhattan were discounted in May, a decrease of 1.6 percentage points from last year.

May 2018 Key Findings — Brooklyn

Prices reached new highs in North Brooklyn. The StreetEasy North Brooklyn Price Index increased 11.1 percent to $1,229,838, a record high for the submarket despite the looming L train shutdown. Borough-wide, prices rose by just 1.1. percent since last year, to $720,555.

The number of homes with a price cut reached an all-time high. The share of sales with a price cut reached an all-time high of 12.4 percent, a rise of 3.3 percentage points from May 2017.

Sales inventory continued to climb, except in North Brooklyn. Sales inventory in the borough reached a record high — up 23.4 percent over last year. Inventory rose the most in South Brooklyn, which saw a 44.7 percent increase over last year. North Brooklyn was the only submarket where inventory dropped, by 6.7 percent since last year.

Brooklyn homes spent more time on the market. Homes stayed on the market for a median of 53 days in the borough, 6 more days than last year. North Brooklyn homes are coming off the market after an average of 43 days — 26 days faster than last year.

Rents rose in all submarkets except North Brooklyn. The StreetEasy Brooklyn Rent Index increased 1.4 percent year-over-year to $2,562. South Brooklyn experienced the largest spike: up 2.6 percent to a median rent of $1,885. North Brooklyn was the only submarket where rents stagnated, likely because of the L train shutdown starting in April 2019. Rents in the submarket remained flat at $3,062.

May 2018 Key Findings — Queens

Price cuts rose to an all-time high. The share of homes with a price cut reached a new high in Queens at 11.1 percent, an increase of 3.5 percentage points over last year.

Sales inventory swelled. Queens saw the largest year-over-year increase in inventory, rising 42.8 percent. All five submarkets in the borough saw a surge in inventory.

Queens homes are selling slightly faster than last year. The median number of days on market for Queens homes was 56, down 2 days from last year. Homes in Northeast Queens and Northwest Queens took longer to sell than last year, with an increase of 12 days and 6 days on the market, respectively.

Rents remained flat. The StreetEasy Queens Rent Index held at $2,113. But rents in South Queens rose 6.9 percent year-over-year, to a median of $1,775.

Queens was the only borough with an increase in the share of discounted rentals. Seventeen percent of Queens rentals offered discounts: up 2.9 percentage points over last year, and the highest share of the three boroughs analyzed.

Rick Hilton, who is the father of Paris Hilton and chairman of Hilton & Hyland, is all set to sell a 16th-centuryRoman mansion for cryptocurrencies. The auction for the property will be held on June 28, and it will make history as the first ever property to be auctioned onblockchain.

The 11-bedroom house is, reportedly, worth upwards of $35 million. The sale will go online on Propy.com, which is a global property store with decentralized title registry.

Realtors Love Cryptocurrencies and Blockchains

In 2017, at least 20 homes were sold forcryptocurrenciesglobally. This year, the bar could be set much higher.

Hilton said: “The auction shows real estate’s growing trust in blockchain and provides crypto investors an opportunity to diversify and solidify their portfolio with a trophy asset.”

The priciest home ever sold using cryptocurrencies was a seven-bedroom Miami estate. It was sold for455 Bitcoinsor approximately $6 million. The Roman mansion could easily break this record and set a record high.

A Listing Beyond Compare

The Palazzetto, which is a grand mansion designed and built by Michelangelo’s collaborator Giacomo Della Porta, is an Italian landmark. Della Porta was also involved in the building of St. Peter’s Dome, which is another famous landmark in Rome, Italy.

The mansion is composed of two independent but connected luxury units. The property boasts of multiple entrances, an in-house theater, a secret garden, a wellness spa, and a gym.

The rooftop offers 360-degree views of the city and bird’s eye view of the neighborhood along with the Altar of the Fatherland. It has 11 bedrooms, 15 and a half bathrooms, three kitchens and multiple living and dining rooms, complete with four parking spots.

Truffles, the darling of the food scene, are not the chocolate treats that bear the same name. Not dessert truffles, true truffles are a rare delight and not an opportunity to be missed. While they are typically considered expensive food, there are ways to get your truffle fix in the United States through avenues such as truffle oil.

There are white and black truffles, and they’re as different as night and day. There are some similarities – they’re both a subterranean fungus that grows in the shadow of oak trees. However, there are over seven different truffle species found all over the world, from the Pacific Northwest to China to North Africa and the Middle East.

Truffles can be found concentrated in certain areas around the world, with the Italian countryside and French countryside being rich places of growth. Black truffles grow with the oak and hazelnut trees in the Périgord region in France. Burgundy truffles can be found throughout Europe in general, like the black summer truffle.

White truffles are typically found in the Langhe and Montferrat areas of northern Italy around the Piedmont region. Additionally, the countrysides of Alba and Asti are popular truffle hunting areas. White truffles are also found in the hill regions of Tuscany in Italy near certain trees.

Not just localized to Europe, however, New Zealand Australia also see truffles growing. The first black truffle produced in theSouthern Hemispherewas in New Zealand in 1993. In Australia, Tasmania was the origin of the first truffle harvests and the largest truffle from Australia, weighing in at 2 pounds, 6 ounces) was harvestedbyMichael and Gwynneth Williams.

In the Pacific Northwest of the U.S., four species of truffles are commercially harvested: the Oregon black truffle, the Oregon spring white, Oregon winter white truffle, and the Oregon brown truffle.

In the South, the pecan truffle is often found alongside fallen pecans. While farmers once discarded them, the gourmet food scene is slowly starting to incorporate them into seasonal dishes.

Depending which country they hail from, they’re sniffed out by specially trained dogs or pigs, then dug up by the “hunter”. They’re located through the natural aroma they release when they interact with certain plants, mammals, and insects. These interactions also encourage new colonies of the truffle fungus to appear through spore dispersal.

White Truffle fresh from the hunt

Both white and black truffles share the same appearance, that of a lumpy potato, but it’s in taste and shelf-life they differ.

Each kind of truffle is firmly in the “umami” category of taste – very earthy and doesn’t need a lot of salt to trip your tastebuds.

The black truffle is far more common, even in haute cuisine. Available for six to nine months a year, it has a stronger taste and pungent aroma that often needs acquiring. I’ve experienced a black truffle-and-olive tapenade, a perfect use for it, because it evokes a black olive-type taste.

Because of the long season and easier odds of being found, black truffles are more affordable. They’re also freezable, making a less-risky purchase for a restaurant, further enabling them to keep prices down.

On the flip-side are white truffles, Earth’s gold. Typically valued at as much as $3,000 per pound, they inspire a big black market. Even legally, they can be outrageous in price.The Atlantic writes, “In 2010, Macau casino tycoon Stanley Ho spent $330,000 on two pieces that weighed 2.87 pounds.”

Internationally, white truffles are big industry. Autumn may yield a truffle experience for you even here. The USA is currently third world-wide for truffle harvest volumes. Stick to truffle towns where restaurants hunt their own, and you maybe be surprised at bargains you find. I was shocked to only spend $20 for my white truffle meal in Croatia.

White truffles cannot be frozen and have a short shelf-life, up to about 10 days. They’re best devoured as soon as possible. Their season is short too – only three to four months each year, September through to as late as January.

I’ve heard of their seasons ending as early as November, though. They’re more elusive to find, often in different forest clusters than their black counterparts. All this computes to costing big bucks.

Even if you dislike black truffles, try fresh white truffles if you ever can. They’re a completely different flavor profile. Instead of black olives, think Parmesan cheese meets mushrooms. It’s a delicate, aromatic flavor – still earthy, but far from overbearing.

Wine and food pairings must let the white truffle take center stage, lest they overpower it. Think polenta with lots of Parmesan and excessive shavings on top.

If you can’t have the real truffle experience, you can buy truffle products flooding the market. These include truffle-infused oils, jams, tapenades, and so forth. Some will use extracts, which are as authentic to the real thing as any extract is. Think orange or lemon or almond extracts. Are they true to the real experience? Not really, but they have their own appeal.

With a growing popularity on the world market, cunning agriculturalists and truffle hunters are trying to farm truffles with mixed results. So far it seems truffles are Earth’s alchemy – a rare treat to remain rare.

Speaking for myself, I was sure I’d hate the pungent fungus, but I felt obligated to try them. Black truffles were a taste I could grow to appreciate, but I’m not a big fan of black olives either. I had decadently expensive dark chocolate-and-black truffle ice cream, though, and that was tasty.

Still, I long for the day I cross paths with white truffles again. The simple dish of polenta and white truffles stands as one of the greatest meals of my life.

There’s a reason they’re sometimes literally worth more than their weight in gold.

The CFPB had two primary,albeit unspoken, functions. First, it was structured as a holding center for fines and assessments against any financial organizations opposed by progressives. Second, it was a distribution hub for the received funds to be transferred to political allies and groups supportive of progressive causes.

The CFPB defenders then appealed the decision to a select appellate court in Washington DC to continue the construct. The Warren crew won the appeal; but today, in an unrelated jurisdictional ruling a New York judge affirmed the minority opinion setting up a possible supreme court pathway to get a final decision.

NEW YORK (AP)– The U.S. government’s beleaguered consumer finance watchdog agency is unconstitutionally structured, a judge said Thursday as she disqualified the agency from serving as a plaintiff in a lawsuit.

Her ruling related to a lawsuit brought against companies loaning money to former National Football League players awaiting payouts from the settlement of a concussion-related lawsuit and to individuals slated to receive money for injuries sustained when they helped in the World Trade Center site cleanup after the Sept. 11, 2001, terrorist attacks.

She let claims brought by the New York State attorney general proceed, but dismissed those that were brought by the CPFB, saying it “lacks authority to bring this enforcement action because its composition violates the Constitution’s separation of powers.”

In ruling, Preska sided with three judges who dissented from the six-judge majority in a January ruling by the U.S. Court of Appeals in Washington. The majority found that the agency director’s power is not excessive and that the president should not have freer rein to fire that person. (read more)

CFPB Interim Director Mick Mulvaney hasalready saidthe CFPB needs to be disassembled.

Taking the agency down is perfectly ok with the Trump administration.

Chinese capital controls and a slump in foreign buyers? Check.

Trade war with the US? Check.

Things are not looking good for Canada’s national housing market, which as VCG reports, continued its sluggish performance in the month of May. Despite the warmer weather and usually busy spring selling season, buying activity has been awfully quiet. New mortgage regulations which are now in full swing have stymied fringe buyers, particularly millennials. According tonew data from credit bureau TransUnion, new mortgage originations among millennials in Canada fell by 19.5% between the last quarter of 2017 and the first three months of 2018.

That has also been showing up sales data.

As shown in the chart below, national home sales in Canada plunged by 16% Y/Y for the month of May. This was the worst decline since the great financial crisis in 2008 when home sales dipped 17% that May. Furthermore, total home sales of 50,604 marked the lowest total since May 2011.

Seasonally adjusted home sales edged 0.1% lower on a month over month basis, and 15% on a year over year basis. Or, as Steve Saretsky put it, “either way you slice it not a great month for one of the worlds most resilient housing markets.”

And as sales continue to slide inventory is beginning to build. For sale inventory crept up by 4% year over year, increasing for the first time in three years, and the highest May increase since 2010.

In light of the above, it is not surprising that the average sales price dipped 6% year over year in May, which however was not nearly as bad as April when year over year declines registered a head turning 11% decline.

But more troubling is that when looking at the smoothed out index of the MLS HPI prices showed the smallest possible increase of just 1% year over year in May, the lowest since September 2009. Not only did this mark the 13th consecutive month of decelerating year over year gains per theCanadian Real Estate Association, but at the current rate of slowdown, next month Canada will record the first annual drop in home prices since the global financial crisis.

The silver lining: condos continue to hold up well as buyers tumble down the housing ladder; here prices posted a 13% increase from May 2017.

CREA’s chief economist Gregory Klump shouldered much of the blame on tighter borrowing conditions, “This year’s new stress-test became even more restrictive in May, since the interest rate used to qualify mortgage applications rose early in the month. Movements in the stress test interest rate are beyond the control of policy makers. Further increases in the rate could weigh on home sales activity at a time when Canadian economic growth is facing headwinds from U.S. trade policy frictions.”

Klump’s theory stacks up well with recent data which suggests fringe borrowers are being pushed towards the private lending space, particularly in Ontario. Mortgage originations at private lenders in the Q1 2018rose to $2.09 billion in Ontario, a 2.95% increase from last year. The market share of private lending went from 5.71% of originations in Q1 2017, to 7.87% in Q1 2018, despite originations at other channels dropping.

In other words, there is a surge in unregulated, non-bank lending, just as the housing bubble pops, precisely what happened the last time there was a full-blown financial crisis.

When you plant your tree in another man’s orchard, you might end up paying for your own apples; it’s a risk you take…

….and President Trump knows how to use that leverage better than anyone could possibly fathom; because in this metaphor Beijing relies upon the U.S. for both the seeds and the harvest. President Trump drops the $200b M.O.A.T (Mother of All Tariffs):

White House – On Friday, I announced plans for tariffs on $50 billion worth of imports from China. These tariffs are being imposed to encourage China to change the unfair practices identified in the Section 301 action with respect to technology and innovation. They also serve as an initial step toward bringing balance to our trade relationship with China.

However and unfortunately, China has determined that it will raise tariffs on $50 billion worth of United States exports. China apparently has no intention of changing its unfair practices related to the acquisition of American intellectual property and technology. Rather than altering those practices, it is now threatening United States companies, workers, and farmers who have done nothing wrong.

This latest action by China clearly indicates its determination to keep the United States at a permanent and unfair disadvantage, which is reflected in our massive $376 billion trade imbalance in goods. This is unacceptable. Further action must be taken to encourage China to change its unfair practices, open its market to United States goods, and accept a more balanced trade relationship with the United States.

Therefore, today, I directed the United States Trade Representative to identify $200 billion worth of Chinese goods for additional tariffs at a rate of 10 percent. After the legal process is complete, these tariffs will go into effect if China refuses to change its practices, and also if it insists on going forward with the new tariffs that it has recently announced. If China increases its tariffs yet again, we will meet that action by pursuing additional tariffs on another $200 billion of goods. The trade relationship between the United States and China must be much more equitable.

I have an excellent relationship with President Xi, and we will continue working together on many issues. But the United States will no longer be taken advantage of on trade by China and other countries in the world.

We will continue using all available tools to create a better and fairer trading system for all Americans.

Historic Chinese geopolitical policy, vis-a-vis their totalitarian control over political sentiment (action) and diplomacy through silence, is evident in the strategic use of the space between carefully chosen words, not just the words themselves.

Each time China takes aggressive action (red dragon) China projects a panda face through silence and non-response to opinion of that action;…. and the action continues. The red dragon has a tendency to say one necessary thing publicly, while manipulating another necessary thing privately. The Art of War.

President Trump is the first U.S. President to understand how the red dragon hides behind the panda mask.

It is specifically because he understands that Panda is a mask that President Trump messages warmth toward the Chinese people, and pours vociferous praise upon Xi Jinping, while simultaneously confronting the geopolitical doctrine of the Xi regime.

In essence Trump is mirroring the behavior of China while confronting their economic duplicity.

President Trump will not back down from his position; the U.S. holds all of the leverage and the issue must be addressed. President Trump has waiting three decades for this moment. This President and his team are entirely prepared for this.

We are finally confronting the geopolitical Red Dragon, China!

The Olive branch and arrows denote the power of peace and war. The symbol in any figure’s right hand has more significance than one in its left hand. Also important is the direction faced by the symbols central figure. The emphasis on the eagles stare signifies the preferred disposition. An eagle holding an arrow also symbolizes the war for freedom, and its use is commonly referred to the liberation fight of righteous people from abusive influence. The eagle on the original seal created for the Office of the President showed the gaze upon the arrows.

The Eagle and the Arrow – An Aesop’s Fable

An Eagle was soaring through the air. Suddenly it heard the whizz of an Arrow, and felt the dart pierce its breast. Slowly it fluttered down to earth. Its lifeblood pouring out. Looking at the Arrow with which it had been shot, the Eagle realized that the deadly shaft had been feathered with one of its own plumes.

Moral:We often give our enemies the means for our own destruction.

“Markets”

… all in deep contrast with what the past American Presidential Administration were focused on (video)

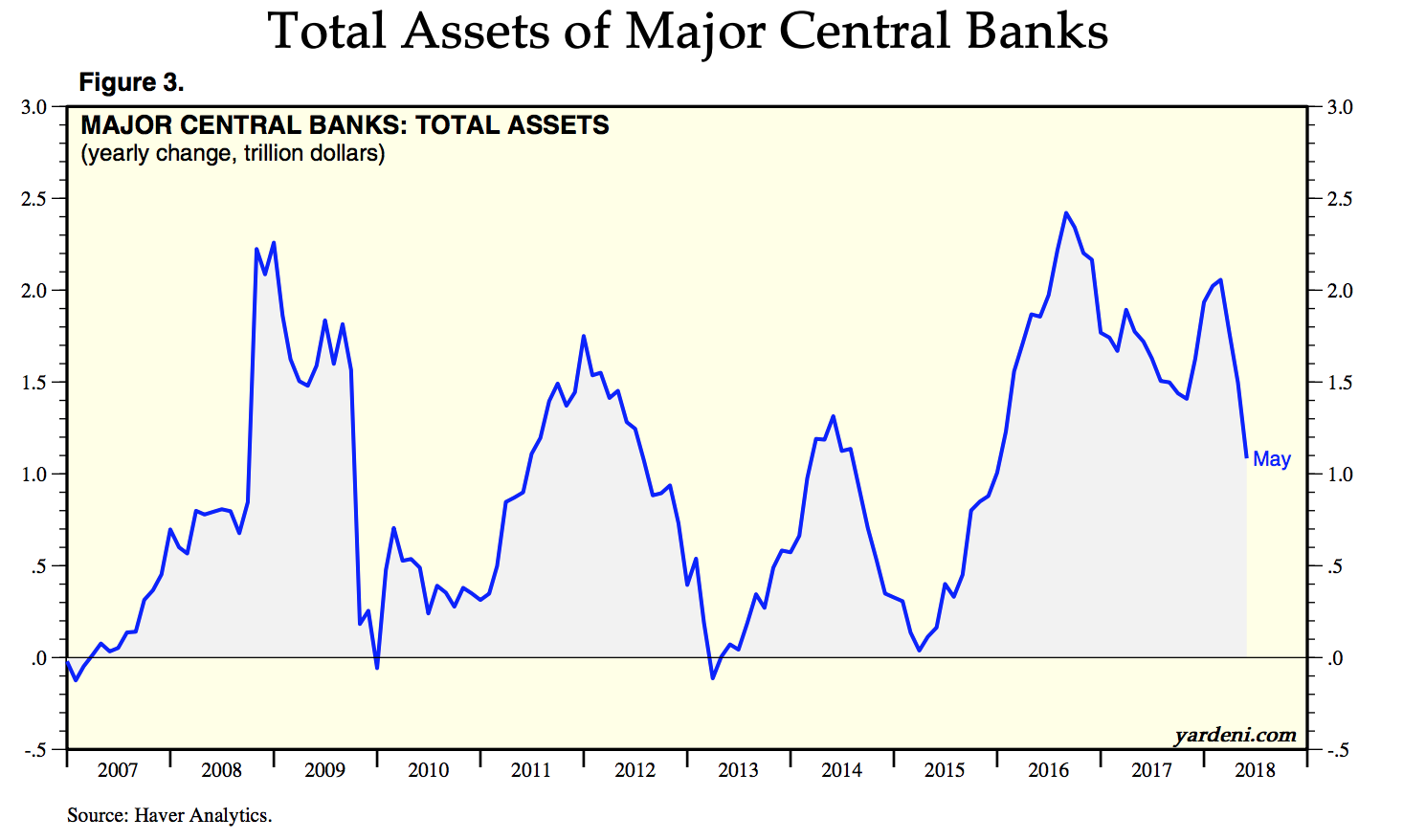

As the Federal Reserve kicked off its second round of quantitative easing in the aftermath of the Great Financial Crisis, hedge fund managerDavid Tepper predictedthat nearly all assets would rise tremendously in response. “The Fed just announced: We want economic growth, and we don’t care if there’s inflation… have they ever said that before?” He then famously uttered the line “You gotta love a put”, referring to the Fed’s declared willingness to print $trillions to backstop the economy and financial markets. Nine years later we see that Tepper was right, likely even more so than he realized at the time.

The other world central banks followed the Fed’s lead. Mario Draghi of the ECB declared a similar “whatever it takes” policy and has printed nearly $3.5 trillion in just the past three years alone. The Bank of Japan has intervened so much that it now owns over 40% of its country’s entire bond market. And no central bank has printed more than the People’s Bank of China.

It has been an unprecedented force feeding of stimulus into the global system. And, contrary to what most people realize, it hasn’t diminished over the years since the Great Recession. In fact, the most recent wave from 2015-2018 has seen the highest amount of injected ‘thin-air’ money ever:

In response, equities have long since rocketed past their pre-crisis highs, bonds continued rising as interest rates stayed at historic lows, and many real estate markets are now back in bubble territory. As Tepper predicted, financial and other risk assets have shot the moon. And everyone learned to love the ‘Fed put’ and stop worrying.

But as King Louis XV and Bob Dylan both warned us, what’s coming next will change everything.

The Deluge Approaches

This halcyon era of ever-higher prices and consequence-free backstopping by the central banks is ending. The central banks, desperate to give themselves some slack (any slack!) to maneuver when the next recession arrives, have publicly committed to ‘tightening monetary policy’ and ‘unwinding their balance sheets’, which is wonk-speak for ‘reversing what they’ve done’ over the past decade.

Most general investors today just don’t appreciate how gargantuanly significant this is. For the past 9 years, we’ve become accustomed to a volatility-free one-way trip higher in asset prices. It’s been all-glory with no risk while the ‘Fed put’ has had our backs (along with the ‘EBC put’, the ‘BOJ’ put, the ‘PBoC put’, etc). Anybody going long, buying the (few, minor) dips along the way, has felt like a genius. That’s all over.

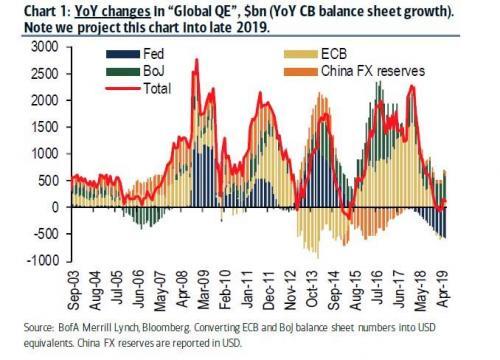

Based on current guidance from the central banks, “global QE” is expected to drop precipitously from here:

With just the relatively tiny amount of QE tapering so far, 2018 has already seen more market price volatility than any year since 2009. But we’ve seen nothing so far compared to the volatility that’s coming later this year when QE starts declining in earnest. In parallel with this tightening, global interest rates are rising after years of flat lining at all-time lows. And it’s important to note that our recent 0% (or negative) yields came at the end of a 35-year secular cycle of declining interest rates that began in the early 1980s.

Are we seeing a secular cycle turn now that rates are creeping back up? Will rising interest rates be the norm for the foreseeable future? If so, the world is woefully unprepared for it. Countries and companies are carrying unprecedented levels of debt, as are many households. Rising interest rates increases the cost of servicing that debt, leaving less behind to invest or to meet basic operating needs.

Simon Black reminds usthat, mathematically, rising interest rates result in lower valuations for stocks, bonds and housing. But so far, Wall Street hasn’t gotten the message (chart courtesy of Charles Hugh Smith):

So we’re presented with a simple question: What happens when the QE that’s grossly-inflating markets stops at the same time that interest rates rise? The answer is simple, too: Prices fall.

They fall commensurate with the distortion within the system. Which is unprecendented at this stage.

But Wait, There’s More!

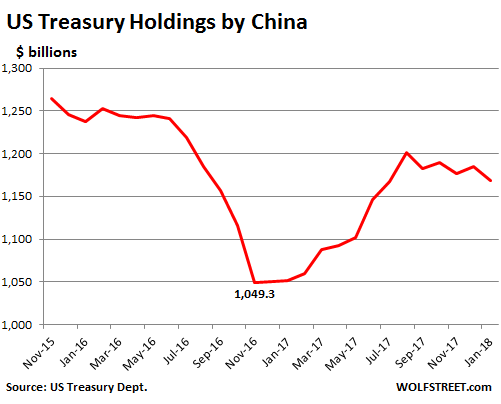

So the situation is dire. But it gets worse. Our debt that’s getting more expensive to service? Well, not only are we (in the US) adding to it at a faster rate with our newly-declared horizon of $1+ trillion annual deficits, but we’re increasingly antagonizing the largest buyers of our debt.

This is most notable with China (the #1 Treasury buyer), whom we’ve dragged into a trade war and just announced$50 billion in tariffsagainst. But Japan (the #2 buyer) is also materially reducing its Treasury purchases. And not to be outdone, Russia recentlydumped half of its Treasury holdings, $47 billion worth, in a single fell swoop. Should this trend lead, understandably, to lower demand for US Treasures in the future, that only will put further pressure on interest rates to move higher.

And this is all happening at a time when the stability of the rest of the world is fast deteriorating. Developing (EM) countries are getting destroyed as central bank liquidity flows slow and reverse — as higher interest rates strengthen the USD against their home currencies, their debts (mostly denominated in USD) become more costly while their revenues (denominated in local currency) lose purchasing power. Fault lines are fracturing across Europe as protectionist, populist candidates are threatening the long-standing EU power structure. Italy’s economy is struggling to remain afloat and could take the entire European banking system down with it. The new tit-for-tat tariffs with the US aren’t helping matters. And China, trade war aside, is seeing its fabled economic momentum slow tomulti-decade lows.

All players on the chessboard are weakening.

The Timing Is Becoming Clear

Yes, the financial markets are currently still near all-time highs (or at the high, in the case of the NASDAQ). And yes, expected Q2 US GDP has jumped to ablistering 4.8%. But the writing is increasingly on the wall that these rosy heights won’t last for much longer.

These next three chartsfrom Palisade Research, combined with the above forecast of the drop-off in global QE, paint a stark picture for the rest of 2018 and beyond. The first shows that as the G-3 central banks have started their initial (and still small) efforts to withdraw QE, the Global Financial Stress Indicator is spiking worrisomely:

Next, one of the best predictors of global corporate earnings now forecasts an imminent collapse. As go earnings, so go stock prices:

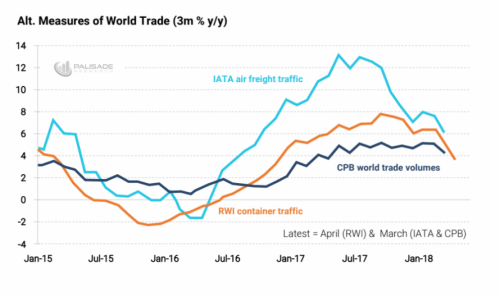

And looking at trade flows — which track the movement of ‘real stuff’ like air and shipping freights — we see clear signs that the global economy is slowing down (a trend that will be exacerbated if oil prices rise as geologistArt Berman predicts):

The end of QE, higher interest rates, trade wars at a time of slowing global trade, China/Europe weakening, EM carnage — it’s like both legs of the ladder you’re standing on being sawed off, as well all of the rungs underneath you.

Conclusion: a major decline in the financial markets is due for the second half of 2018/first half of 2019.

Actions To Take

Gathering clouds deliver a valuable message: Seek shelter before the storm.

Specifically, it’s time to:

Get liquid. When the rug gets pulled out from under today’s asset prices, ‘flat’ will be the new ‘up’. Simply not losing money will make you wealthier on a relative basis — it’s the easiest, least-risky strategy for most investors to prepare for what’s coming. “Cash is king” in the aftermath of a deflationary downdraft, when your dry power can be then used to purchase high-quality income-producing assets at excellent value — fractions of their current prices. And in the interim, the returns on cash are getting better for investors who know where to look. We’ve recently explained how you can now get 2%+ interest on cash stored in short-term T-bills (that’s 30x more than most banks will pay on cash savings). If you’re sitting on cash and haven’t looked seriously yet at that program, you really should review our report. With more Fed tightening expected in the future, T-bill rates are likely headed even higher.

Get your plan for the correction into place now. In addition to your cash, how is the rest of your portfolio positioned? Do you have suitable hedges in place to mitigate your risk? Does your financial advisor even acknowledge the risks detailed in the above article? The last thing you want to do in a market downdraft is make panicked decisions.

Nibble into commodities. The commodities/equities price ratio is the lowest it has been in 47 years. That ratio has to correct some point soon. Much of that correction will be due to stocks dropping; but the rest will be by commodities holding their own or appreciating. While it’s true that commodities could indeed fall as well during a general deflationary rout, that’s not a guarantee — especially given that many commodities are now selling at prices close to — or in some cases, below — their marginal cost of production. The easiest commodities to own yourself, the precious metals, are ‘dirt cheap’ right now (especially silver), as explained in our recent podcast with Ronald Stoeferle. And with Friday’s bloodbath, they just got even cheaper.

Assess and address your biggest vulnerabilities before the next crisis hits. Are you worried about the security of your current job when the next recession hits? Are rising interest rates causing you to struggle in deciding whether to buy or sell a home? Are you trying to come up with a plan for a resilient retirement? Are you assessing the pros and cons of relocating? Do you have homesteading questions? Are you trying to create new streams of income?

We’re lurching through the final steps of familiar territory as the status quo we’ve known for the past near-decade is ending. The mind-mindbogglingly massive central bank stimulus supporting asset prices are disappearing. Interest rates are rising. It’s hard to overemphasize how seismic these changes will be to world markets and the global economy. The coming years are going to be completely different than what society is conditioned for. Time is running short to get prepared. Because when today’s Everything Bubble bursts, the effect will be nothing short of catastrophic as 50 years of excessive debt accumulation suddenly deflates.

Wealthy Americans living in blue states are scrambling to find tax loopholes that will help them get around one of the most controversial (and for some, infuriating) provisions in President Trump’s tax plan:The capping of the so-called SALT deduction.Enter real-estate planner Jonathan Blattmachr, who this week made the mistake of explaining to aBloombergreporter about a plan he’s devised for his clients who are trying to get out of paying the additional taxes on their summer homes in the Hamptons or Cape Cod. According to theBloombergstory, Blattmachr is planning on transferring the interest in his two New York residences – one in Garden City and one in Southampton – into LLCs, which he will then divide up into five separate trusts that will be based in Alaska.He can then use the trusts to take the maximum $10,000 deduction five separate times. In this way, he can deduct $50,000 in mortgage taxes from his federal tax bill instead of $10,000.

“This is an under-the-radar thing and it’s novel,” said Blattmachr. (Or at least it was under-the-radar until you went blabbing to the media).The trusts that Blattmachr and other savvy estate planners are using to take advantage of this loophole are called non-grantor trusts. While trusts are typically used by the wealthiest Americans to preserve their wealth as it’s handed down from generation to generation, the tax law is giving the merely wealthy an incentive to explore setting up these trusts to pay taxes at rates found in low-tax red states. The trusts can help property owners avoid paying an additional $100,000 in taxes across their properties.

However, the plan isn’t practical for everybody, and even those who can reap the benefits over the long term must take an up-front risk because they must pay the maintenance costs for the trusts – which can be as high as $20,000 – up front. If the IRS ever issues guidance invalidating the loophole, there’s no way to recover those costs.

Setting up dozens of non-grantor trusts for those with six-figure plus property taxes can be impractical and burdensome. Plus, those whose taxes are under six figures feel the new cap most acutely, according to Steffi Hafen, a tax and estate planning lawyer at Snell & Wilmer in Orange County, California. Those clients often have monthly mortgage payments that eat up a big chunk of their take-home pay, Hafen said.

More than 10 percent of taxpayers in New Jersey will see a tax hike under the new law – the highest percentage in the U.S. – followed by Maryland and the District of Columbia at 9.4 percent, 8.6 percent in California and 8.3 percent in New York, according to an analysis earlier this year by the Tax Policy Center. Those who’ll pay more are mostly being affected by the state and local tax deduction limit.

Mark Germain, founder of Beacon Wealth Management in Hackensack, New Jersey, said the strategy is “absolutely viable,” adding that he has about a dozen clients who want to create non-grantor trusts.

Building and administering the trusts could cost about $20,000, according to Brad Dillon, a senior wealth planner at Brown Brothers Harriman. But those expenses would be justified after a few years, said Scott Testa, a lawyer who leads the estates and trusts tax practice at Friedman LLP in East Hanover, New Jersey.

Already, it’s unclear just how much longer individuals will be able to take advantage of the loophole. As Bloomberg explains, an existing provision in the US tax code could easily be revived to prohibit Americans from using trusts to avoid paying SALT taxes. Though it would take effort on the IRS’s part.

Still, the Internal Revenue Service could issue guidance that would prevent taxpayers from using the trusts to get around the SALT cap. An existing provision says that multiple non-grantor trusts with identical beneficiaries and identical grantors – and whose primary purpose is to avoid taxes – can potentially be considered a single entity, with just one $10,000 SALT deduction. But the measure has never been bolstered by regulations, leaving it vague.

That IRS provision could potentially derail the whole strategy, Dillon said. But compared to the other workarounds that have been proposed by high-tax states, the non-grantor trust “is the only one that’s come out of the fray that seems like a viable structure,” Dillon said.

Furthermore, people with large mortgages might have difficulty convincing their lender to allow them to transfer ownership over to an LLC.

The strategy isn’t for everybody: People with large mortgages on their homes might not be able to win approval from the bank to transfer ownership to an LLC. Also taxpayers with a primary residence in Florida, which like Alaska doesn’t have an income tax, can’t take advantage of the scheme because of complex rules surrounding the state’s homestead exemption.

But for those who are curious, here’s an in-depth explanation of how the process works:

Here’s how it works: First, you set up an LLC in a no-tax state such as Alaska or Delaware. Then, you transfer fractions of that LLC into multiple non-grantor trusts, which are trusts that are treated as independent taxpayers (unlike grantor trusts, where the person who creates them are generally taxed on the trust income). Each trust can take a deduction up to $10,000 for state and local taxes.

If a spouse is designated as the beneficiary, another “adverse” party – meaning someone who may want the money also — has to approve any distributions.