The Fed’s “temporary” liquidity injections are starting to look rather permanent…

Anyone who expected that the easing of the quarter-end funding squeeze in the repo market would mean the Fed would gradually fade its interventions in the repo market, was disappointed on Friday afternoon when the NY Fed announced it would extend the duration of overnight repo operations (with a total size of $75BN) for at least another month, while also offering no less than eight 2-week term repo operations until November 4, 2019, which confirms that the funding unlocked via term repo is no longer merely a part of the quarter-end arsenal but an integral part of the Fed’s overall “temporary” open market operations… which are starting to look quite permanent.

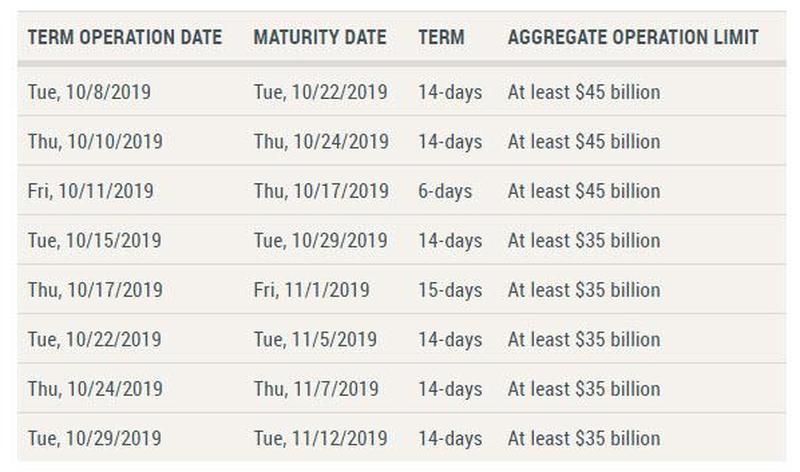

In accordance with the most recent Federal Open Market Committee (FOMC) directive, the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York will conduct a series of overnight and term repurchase agreement (repo) operations to help maintain the federal funds rate within the target range.

Effective the week of October 7, the Desk will offer term repos through the end of October as indicated in the schedule below. The Desk will continue to offer daily overnight repos for an aggregate amount of at least $75 billion each through Monday, November 4, 2019.

Securities eligible as collateral include Treasury, agency debt, and agency mortgage-backed securities. Awarded amounts may be less than the amount offered, depending on the total quantity of eligible propositions submitted. Additional details about the operations will be released each afternoon for the following day’s operation(s) on the Repurchase Agreement Operational Details web page. The operation schedule and parameters are subject to change if market conditions warrant or should the FOMC alter its guidance to the Desk.

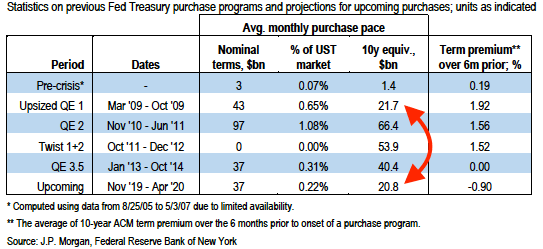

What this means is that until such time as the Fed launches Permanent Open Market Operations – either at the November or December FOMC meeting, which according to JPMorgan will be roughly $37BN per month, or approximately the same size as QE1…

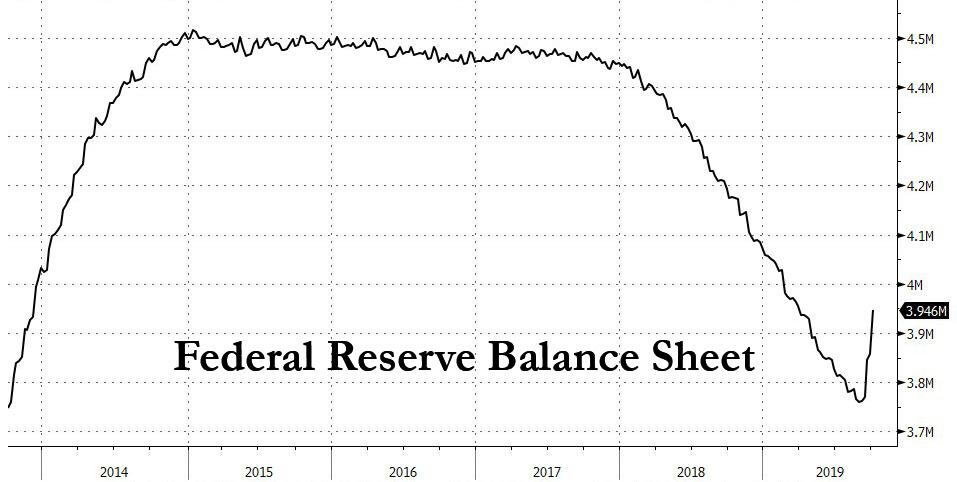

… the NY Fed will continue to inject liquidity via the now standard TOMOs: overnight and term repos. At that point, watch as the Fed’s balance sheet, which rose by $185BN in the past month, continues rising indefinitely as QE4 is quietly launched to no fanfare.

As the exodus gathers momentum, all the reasons people clung so rabidly to urban meccas decay.

The lifestyle you ordered is not just out of stock, the supplier closed down.

(Charles Huge Smith) If there is any trend that’s viewed as permanent, it’s the enduring attraction of coastal urban meccas: despite the insane rents and housing costs, that’s where the jobs, the opportunities and the desirable urban culture are.

Nice, but like many other things the status quo considers permanent, this could reverse very quickly, and all those pricey urban meccas could become crime-ridden ghost towns. How could such a reversal occur?

1. Those in the top 10% who can leave reach an inflection point and decide to leave. The top 1% who live in enclaves filled with politicians, celebrities and the uber-wealthy see no reason to leave, as the police make sure no human feces land on their doorstep.

It’s everyone who lives outside these protected enclaves, in neighborhoods exposed to exasperating (and increasingly dangerous) decay who will reach a point where the “urban lifestyle” is no longer worth the sacrifices and costs.

It might be needles and human feces on the sidewalk, it might be petty crime such as your mail being stolen for the umpteenth time, it might be soul-crushing commutes that finally do crush your soul, or in Berkeley, California, it might be getting a $300 ticket for not bringing your bicycle to a complete stop at every empty intersection on a city bikeway. (I’ve personally witnessed motorcycle officers nailing dozens of bicyclists with these $300 tickets.)

It might be something that shreds the flimsy facade of safety and security complacent urban dwellers have taken for granted, something that acts as the last grain of sand on the growing pile of reasons to get the heck out that triggers the decision.

Not everyone can move, but many in the top tier can, and will. Living in a decaying situation is not a necessity for these lucky few, it’s an option.

2. Those who have to leave when they lose their job. A funny thing happens in all economies, even those with central banks: credit-cycle / business-cycle recessions are inevitable, regardless of how many times financial pundits say, “the Fed has our back” and “don’t fight the Fed.”

As I’ve noted here numerous times, a great many small businesses in these pricey urban meccas are one tiny step from closing: one more rent increase, one more bad month, one more regulatory burden, one more health issue and they’re gone. They will move to greener pastures for the same reason as everyone else–they can’t afford to live in urban meccas.

Once enough of the top 10% leave (by choice or because they can no longer afford it), the food/beverage service industry implodes. Wait staff and bartending have been a major source of jobs in these urban meccas, and when hundreds of struggling establishments fold due to a 10% decline in their sales, thousands of these employees will lose their jobs and the prospects of getting hired elsewhere decline with every new closure.

The vast majority of these service employees are renters, paying sky-high rents that unemployment can’t cover. They will hang on for a few months and then cash in their chips and move to more affordable climes.

3. Once the stock market returns to historic norms, the gargantuan capital gains that supported local tax revenues and spending dry up. WeWork is the canary in the coal mine; from a $50 billion IPO to insolvency in six weeks.

Once tax revenues plummet (no more IPOs, hundreds of restaurants closing, etc.), cities and counties will have to trim their work forces to maintain their ballooning pension payments for retirees. This will leave fewer police and social workers available to deal with everyone with little motivation (or option) to leave: thieves, those getting public services and the homeless.

4. Housing prices and rents are sticky: sellers and landlords won’t believe the good times have ended, and so they will keep home prices and rents at nosebleed valuations even as vacancies soar and the market is flooded with listings.

Neighborhoods that had fewer than 100 homes for sale will suddenly have 500 and then 1,000, as sellers realize the boom has ended and they want out–but only at top-of-the-bubble prices.

Ironically, this stubborn attachment to boom-era prices for homes and rents accelerates the exodus. As incomes decline, costs remain sky-high, so the only option left is to move away, the sooner the better.

By the time sellers grudgingly reduce prices, it’s too late: the market has soured. The Kubler-Ross dynamic is in full display, as sellers go through the stages of denial, anger, bargaining and acceptance: they grudgingly drop the price of the $1.2 million bungalow or flat to $1.15 million, then after much anger and anguish, to $1.1 million, but the market has imploded while they processed a reversal they didn’t think possible: now sales have dried up, and prices are sub-$800,000 while they ponder dropping their asking price to $995,000.

Vacant apartments pile up, as the number of laid-off and downsized employees who can still afford high rents collapses. (Recall that tens of thousands of recent arrivals in urban meccas rely heavily on tips for their income, and as service and gig-economy business dries up, so do their tips.)

5. As the exodus gathers momentum, all the reasons people clung so rabidly to urban meccas decay: venues and cafes close, street life fades, job opportunities dry up, and yet prices for everything remain high: transport, rent, taxes, employees, etc.

Friends move away, favorite places close suddenly, streets that were safe now seem foreboding, and all the friction, crime, grime and dysfunction that was once tolerable becomes intolerable.

6. In response to deteriorating city and county finances, local government jacks up fees, tickets, permits and taxes, accelerating the exodus. How many $300 tickets, fees and penalties does it take to break the resolve to stick it out?

7. Those on the cusp cave in and abandon the mecca. Once those who had the option to leave have left, and those who can no longer afford to stay leave, the decay causes those on the cusp of bailing out to abandon ship.

Renters move out in the middle of the night, homeowners who have watched their equity vanish as prices went into free fall jingle-mail the keys to the house to the lender and small businesses that had clung on, hoping for a turn-around close their doors.

8. Each of these dynamics reinforce the others. Soaring taxes, decaying services, declining business, rising insecurity and stubbornly high costs all feed on each other.

And that’s how pricey urban meccas turn into ghost towns inhabited by those who can’t leave and those living on public services, i.e. those too poor to support the enormously costly infrastructure of public spending in the urban mecca.

Not only do nearly half of America’s homeless people live in California, but four of the five American cities with the greatest incidences of un-sheltered homelessness are in the Golden State.

As California becomes a mecca for socialism, their quality of life diminishes along with it in a characteristic dystopian decline.

San Francisco, Los Angeles, Santa Rosa, and San Jose are four of the five cities with the highest amount of homelessness. Seattle joins the California municipalities in the top five.According to Market Watch,the rates of homelessness are the highest in Washington D.C. The District of Columbia’s homeless rate is at 5.8 times the United States rate. New York is next, followed by Hawaii, Oregon, and California. These five states together comprise 20% of the overall U.S. population but 45% of the country’s homeless population.

All of these states are incredibly liberal with several already having instituted tight socialist policies.

A White House report teased out certain trends in homelessness across the country. Communities along both coasts have much larger homeless populations than those in the middle of the country. One driver of this trend is likely the more notable rise in housing prices along the coasts than in much of the Midwest.

The White House report identified local laws and policing practices as a potential differentiator. “Some [states] more than others engage in more stringent enforcement of quality of life issues like restrictions on the use of tents and encampments, loitering, and other related activities,” the report noted. –Market Watch

The Trump administration has floated plans to fix the homeless crisis in liberal areas by deregulation. Many states and municipalities have zoning rules regarding the construction of both single-family and multi-family homes. These laws have impeded the builders’ ability to meet the demand for housing resulting in scarcity which has driven up prices. Experts and politicians across the political spectrum have suggested that relaxing such regulations could provide a boost to building activity.

Chinese police searched the house of Zhang Qi, 57, the former mayor of Danzhou, and found a large amount of cash, as well as 13.5 tons of gold in ingots in a secret basement of his home, according tolocal media.

In addition to the mayoral post, Qi held others including Secretary of the Communist Party.

According to unofficial reports, in addition to the $625 million worth of gold, cash worth 268 billion yuan ($37 billion) was discovered[ZH: seems highs to us].

The video prompted some witty social media responses…

Luxurious real estate with a total area of several thousand square meters, which the former city manager had been reportedly hiding, was the icing on the cake in this massive haul for the Chinese Anti-Corruption Committee.

Qi was investigated by the Central Commission for Discipline Inspection (CCDI), the party’s internal disciplinary body, and the National Supervisory Commission, the highest anti-corruption agency of China, in September 2019.

According to China’s anti-corruption laws, Qi will be executed.

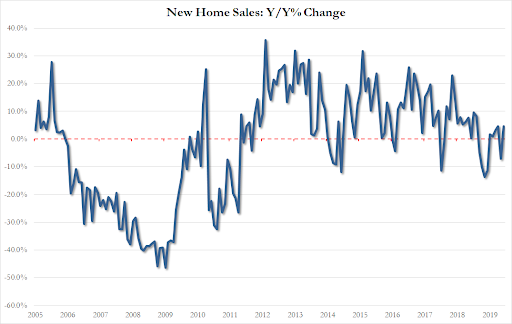

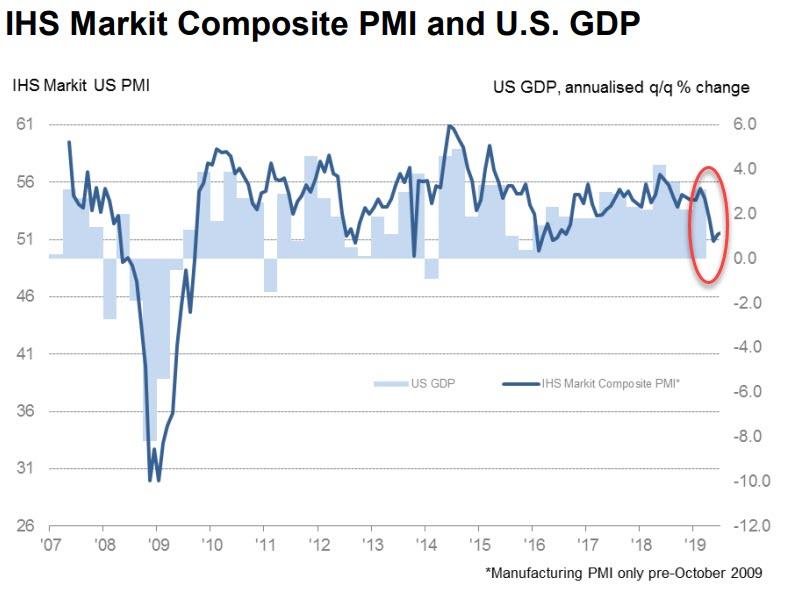

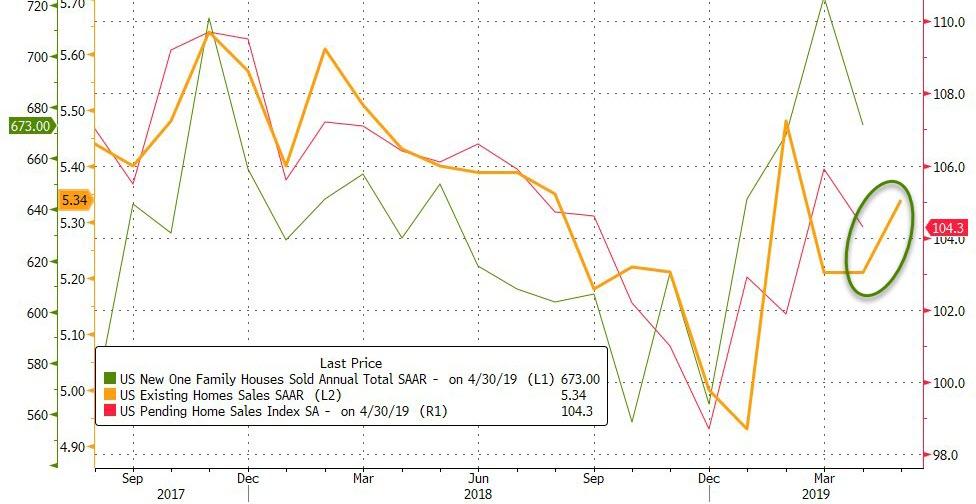

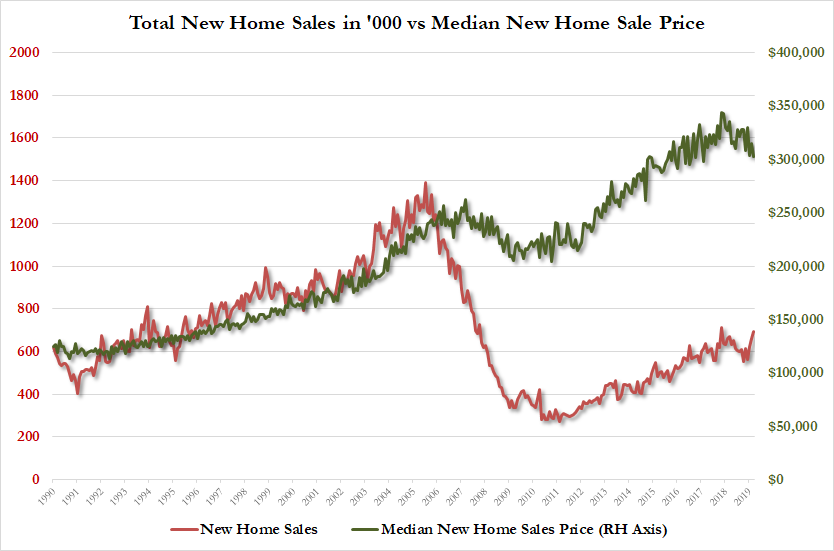

After new- and existing-home-sales rebounded notably in August, expectations were that pending sales would complete the trifecta and sure enough it did (rising 1.3% MoM, better than the 1.0% expected jump)

Source: Bloomberg

Pending home sales rose 2.48% YoY – the biggest annual jump since April 2016…

Source: Bloomberg

All regions saw an increase in sales in August:

Northeast up 1.4%; July fell 1.6%

Midwest up 0.6%; July fell 2.4%

South up 1.4%; July fell 2.4%

West up 3.1%; July fell 3.4%

But we note that The Northeast (-1.1%) and Midwest (-1.6%) both fell year-over-year.

The question is – what happens next? As mortgage rates have rebounded higher and mortgage applications have already tumbled since this sales data…

The Fed is scheduled to pump ‘at least’ $75B in Emergency Capital Injections every day, between today and October 10th, to presumably keep the entire banking system from locking up.

This means at a minimum, the Fed is prepared to inject nearly three times more money into the system in two weeks than during the entire TARP program between 2008-2012.

Just like That: Roughly 600,000 travelers are stranded around the world after the British travel provider Thomas Cook declares bankruptcy…

StudioPortoSabbia/Shutterstock

Thomas Cook, a 178-year-old British travel company and airline, declared bankruptcy early Monday morning, suspending operations and leaving hundreds of thousands of tourists stranded around the world.

The travel company operates its own airline, with a fleet of nearly 50 medium- and long-range jets, and owns several smaller airlines and subsidiaries, including the German carrier Condor. Thomas Cook still had several flights in the air as of Sunday night but was expected to cease operations once they landed at their destinations.

Condor posted a message to its site late Sunday night saying that it was still operating but that it was unclear whether that would change. Condor’s scheduled Monday-morning flights appeared to be operating normally.

About 600,000 Thomas Cook customers were traveling at the time of the collapse, of whom 150,000 were British, the company toldCNN.

The British Department for Transport and Civil Aviation Authority prepared plans, under the code name “Operation Matterhorn,” to repatriate stranded British passengers. According to the British aviation authority, those rescue flights would take place until October 6, leading to the possibility that travelers could be delayed for up to two weeks.

Initial rescue flights seemed poised to begin immediately, with stranded passengers posting on Twitter that they were being delayed only a few hours as they awaited chartered flights.

The scale of the task has reports calling it the largest peacetime repatriation effort in British history, including the operation the government carried out whenMonarch Airlines collapsedin 2017.

Costs of the flights were expected to be covered by theATOL, or Air Travel Organiser’s License, protection plan, a fund that provides for repatriation of British travelers if an airline ceases operations.

Airplanes from British Airways and EasyJet would be among those transporting stranded passengers home, according toThe Guardian, as well as chartered planes from leasing companies and other airlines. Thomas Cook Airlines’ destinations included parts of mainland Europe, Africa, the US, the Caribbean, and the Middle East. Airplanes were being flown to those destinations on Sunday night, according to theBBC.

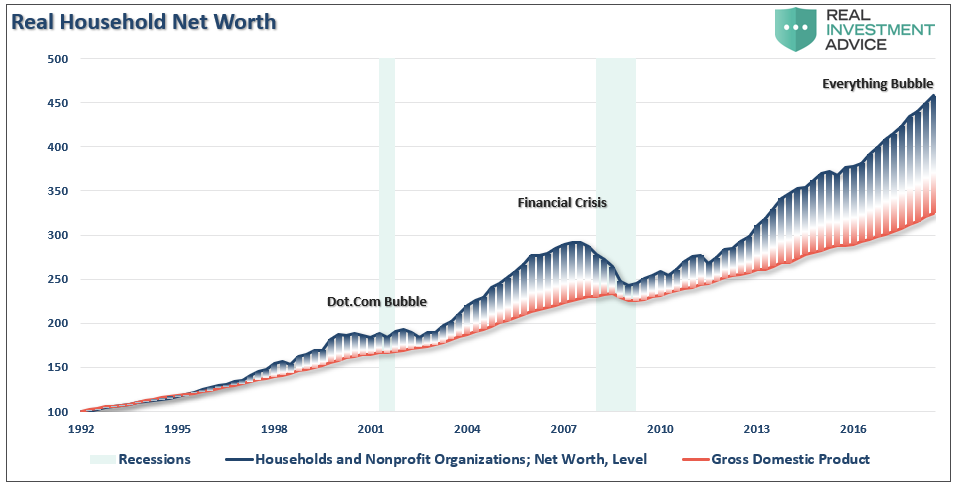

We are living in an age of records in the financial world. The stock market is in its longest bull market in history and near all-time highs. The world has more debt than ever before while interest rates are near record lows, and some are negative in many countries for the first time ever. Nick Barisheff, CEO of Bullion Management Group (BMG), is seeing a dark ending for the era of financial records. Barisheff explains,

“I have been in the business for 40 years, and this is the first time we have had a simultaneous triple bubble, a bubble in real estate, stocks and bonds all at the same time. In 1999, it was a stock bubble. In 2007, it was a real estate bubble. This time, we’ve got a triple simultaneous bubble. So, when we have the correction, it’s going to be massive. Value calculations on equities say it’s worse than 1999, and in some cases worse than 1929. The big problem is this triple bubble is sitting on a mountain of debt like never before.”

What is going to be the reaction to this record bubble in everything crashing? Barisheff says, “I think you are going to be getting riots in the streets. It’s already happening in California. CalPERS is the pension fund administrator for a lot of the pension funds in California. So, already retired teachers, firefighters and policemen that are sitting in retirement getting their pension checks all got letters saying sorry, your pension checks from now on are going to be reduced by 60%. How do you get by then?”

What happens if the meltdown picks up speed and casualties? Barisheff says,

“I think the only option will be for the government is to print more money and postpone the problem yet a little bit longer, but that leads to massive inflation and eventually hyperinflation. Every fiat currency that has ever existed has always ended in hyperinflation, every single one. Since 1800, there have been 56 hyper inflations. Hyperinflation is defined as 50% inflation per month. That’s where we are going and what other choice is there?”

So, what do you do? Barisheff says,

“In the U.S. dollar since 2000, gold is up an average of 9.4% per year. In some countries, it’s up 14% and so on. If you take the overall average of all the countries, the average increase is 10% a year. Every time Warren Buffett is on CNBC, he seems to go out of his way to disparage gold, but if you look at a chart of Berkshire Hathaway and gold, gold has outperformed Berkshire Hathaway. . . Everybody worships Warren Buffett as the best investor in the world, and gold has outperformed his fund in U.S. dollars. I would not disparage gold if I were him. I’d keep quiet about it.”

There is a first for Barisheff, too, in this financial environment. He says for the first time ever, he’s “100% invested in gold” as a percentage of his portfolio. He says the bottom “is in for gold,” and “the bottom is in for silver, too.”

Barisheff contends that with the record bubbles and the record debt, both gold and silver will be setting new all-time high records as well in the not-so-distant future.

Join Greg Hunter of USAWatchdog.com as he goes One-on-One with Nick Barisheff, CEO of BMG and the author of the popular book“$10,000 Gold.”

It’s now official: central banks’ stated policy is to take interest rates and the value of the US dollar to zero. …But not until they’ve managed to tie up the world’s real estate and other hard assets, leaving the vast majority of people in poverty.

Wayne Jett, constitutional attorney, who has argued cases up to and including the US Supreme Court, author of “The Fruits of Graft, Great Depressions Then and Now,” and founder of ClassicalCapital.com, returns to Reluctant Peppers to expound on his latest article “MONETARY POLICY END GAME – Central Banks To Fight Fake ‘Deflation’.”

If you’re not outraged by the end of this interview, you’re not paying attention. You’ll want to share this widely!

Are you a rich guy who wants to bang debt-laden college girls with all your extra money?

Are you a struggling college girl facing decades of six-figure debt so you can follow your unsinkable dreams?

Great news; thanks to the internet, your bases are covered! As we’ve previously reported (hereandhere), ‘soft prostitution’ may have been going on for a long time – but its normalization is relatively new – and undoubtedly linked to the $1.5 trillion+ student debt problem.

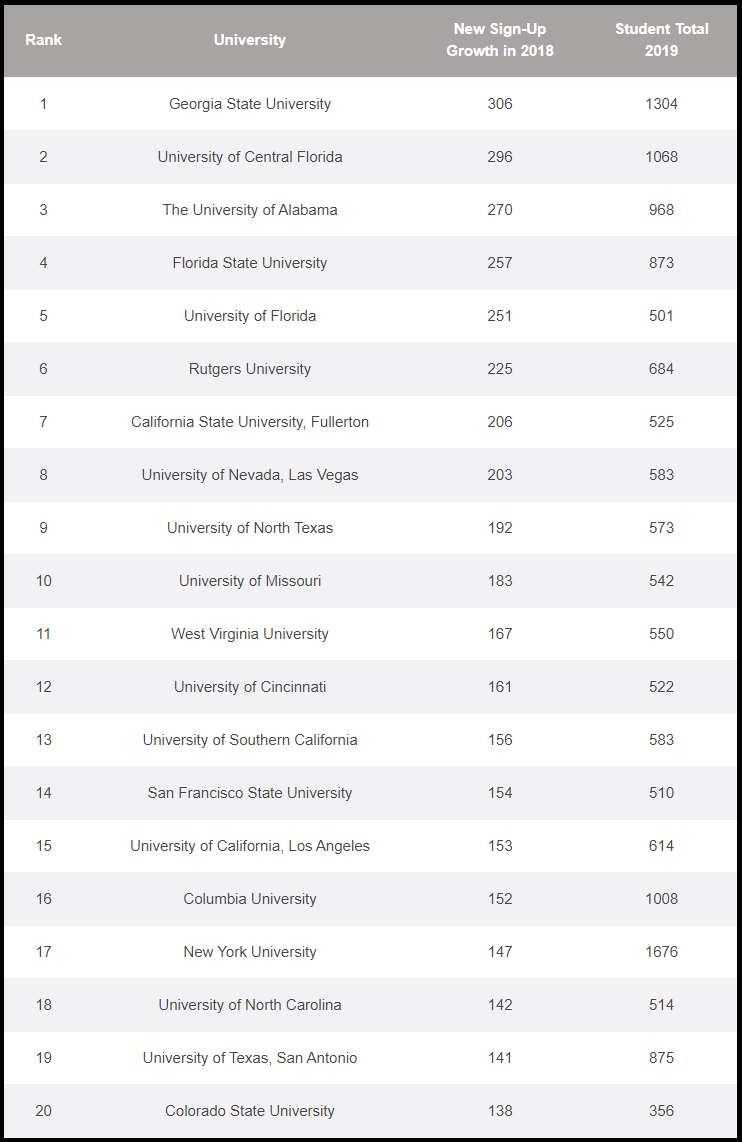

As an example, according to ‘sugar daddy / sugar baby’ website SeekingArrangement, there are 1,304 students at Georgia State Universitysigned up to be Sugar Babiesright now – up from just 306 in 2018.

Given that there are15,277 female studentsat Georgia State, –nearly one in ten girls at Georgia State are willing to whore themselves out to make ends meet.

Of this list, several universities are considered top-tier – such as UCLA, University of Southern California, Columbia and New York University.

According to Seeking.com, “Sugar Babiesdo not want to be in monotonous, traditional relationships prescribed by society — that no longer works today. Rather, she is seeking a modern relationship — one that is different and matches her ambition and drive — with a romantic partner who can play the traditional role of provider or gentleman, without placing unreasonable limitations on personal growth,” according to the website.

Overall, there are 2.7 million US students signed up and 4.7 million worldwide.

According to the website, “Students registered on SeekingArrangement get help paying for tuition and even more benefits.Finding the right Sugar Daddy can help students gain access to the right network and opportunities. College Sugar Babies can also get help paying for other college-related costs, such as books and housing.”

And while the site claims 4.5 million students across the globe, SeekingArrangement says it has 20 million members worldwide – of which students are most common.

What do they Sugar Babies do with the money they earn with their vaginas? 30% is spent on tuition and other school related expenses, while 25% goes towards living expenses.

Meanwhile, the average Sugar Daddy is 41-years-old and has an annual income of $250,000. Most common professions are Tech Entrepreneur and CEO are their two top occupations, followed by Developer, Financier, Lawyer and Physician.

As for cities – New York tops the list, followed by London, Toronto and Los Angeles.

Are we about to see the stock market crash this year? That is what Goldman Sachs seems to think, and it certainly wouldn’t be the first time that great financial chaos has been unleashed during the month of October. When the stock market crashed in October 1929, it started the worst economic depression that we have ever witnessed. In October 1987, the largest single day percentage decline in U.S. stock market history rocked the entire planet. And the nightmarish events of October 2008 set the stage for a “Great Recession” that we still haven’t fully recovered from. So could it be possible that something similar may happen in October 2019?

The storm clouds are looming and disaster could strike at any time. This is one of the most critical times in the history of our nation, and most Americans are completely unprepared for what is going to happen next.

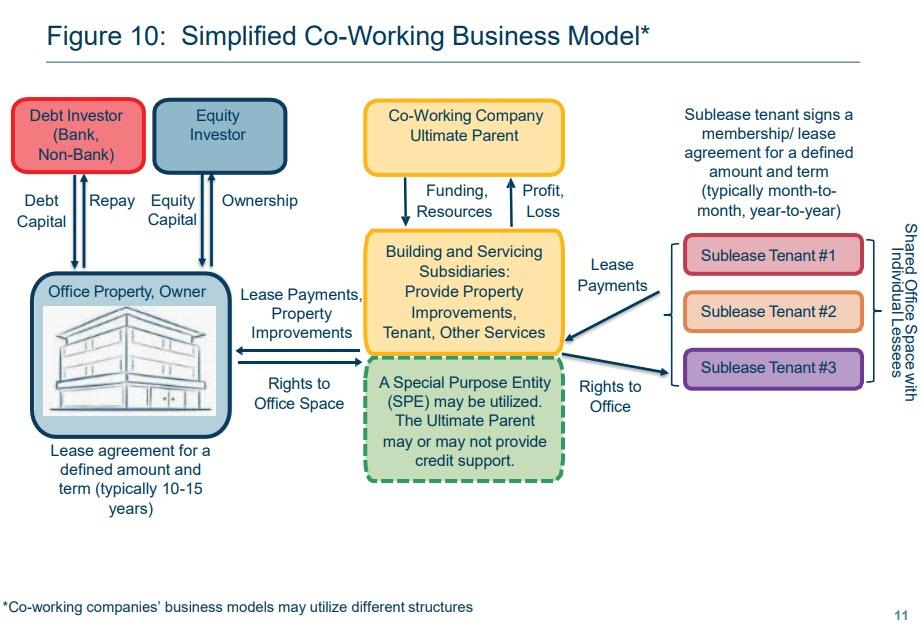

(ZeroHedge) In a stunning rebuke, echoing very closely our own concerns, Boston Fed President Eric Rosengren has – without naming-names – called out the WeWork business model as being a systemic risk to the US economy.

Two weeks ago we asked (rhetorically)…

What happens to the US CRE market when We files for bankruptcy

While the collapse and/or bankruptcy of WeWork would hardly lead to a personal finance disaster – SoftBank’s Masayoshi Son is already Japan’s richest man and with a net worth of over $20 billion can easily stomach losing billions on WeWork (and Uber) – it would send shockwaves across US commercial real estate, as the company is already the single biggest tenant in New York City, as well as Chicago, Denver and central London.

In fact, with over $47 billion in lease liabilities, WeWork is already one of the world’s largest lessees, trailing only oil exploration giants Petrobras and Sinpec, an astonishing feat for the flexible office space provider “which was founded less than a decade ago, bleeds cash, and doesn’t plan to become profitable any time soon.”

As Bloomberg recently noted, “anyone weighing whether to buy shares in WeWork’s IPO cannot ignore the fact that the company will have to find $47 billion from somewhere in coming years to meet its contractual obligations – including about $10 billion in just the next five years. Right now, its own very negative cash flows won’t cut it.”

Mr. Rosengren noted the risks posed by commercial real estate, which have long been a concern of his, as a possible vector to amplify trouble.

Without naming any firms, Mr. Rosengren noted the particular concerns posed by co-working companies. He made this comment as the parent of office-sharing firm WeWork postponed its initial public offering amid investor doubts about its valuation and concerns about its corporate governance.

Office-sharing firms are particularly exposed to risks should the economy run into trouble, and could wound landlords in the process, Mr. Rosengren said.

“In a downturn the co-working company would be exposed to the loss of tenant income, which puts both them and the property owner at risk if they cannot make lease payments to the owner of the building,” he said.

“I am concerned that commercial real estate losses will be larger in the next downturn because of this growing feature of the real estate market, which could ultimately make runs and vacancies more likely due to this new leasing model,” Mr. Rosengren said.

“The fact that the shared office model relies on small-company tenants with short-term leases, combined with the potential lack of recourse for the property owner, is potentially problematic in a recession. This also raises the issue of whether bank loans to property owners in cities with major penetration by co-working models could experience a higher incidence of default and greater loss-given-defaults than we have seen historically.”

Of course, he is right.As we concluded more explicitly,in a bankruptcy, all those obligations would be frozen and squeezed among all the other pre-petition claims, which of course means that the commercial real estate market of cities where WeWork is especially active – like New York and London (and Rosengren’s Boston) – would suddenly find itself paralyzed, as a deflationary tsunami is unleashed among one of the strongest performing markets since the financial crisis.

Doubleline Capital CEO and founder Jeffrey Gundlach joins ‘Fast Money Halftime Report’ to discuss the Fed rate decision, if there is a recession risk and his market call.

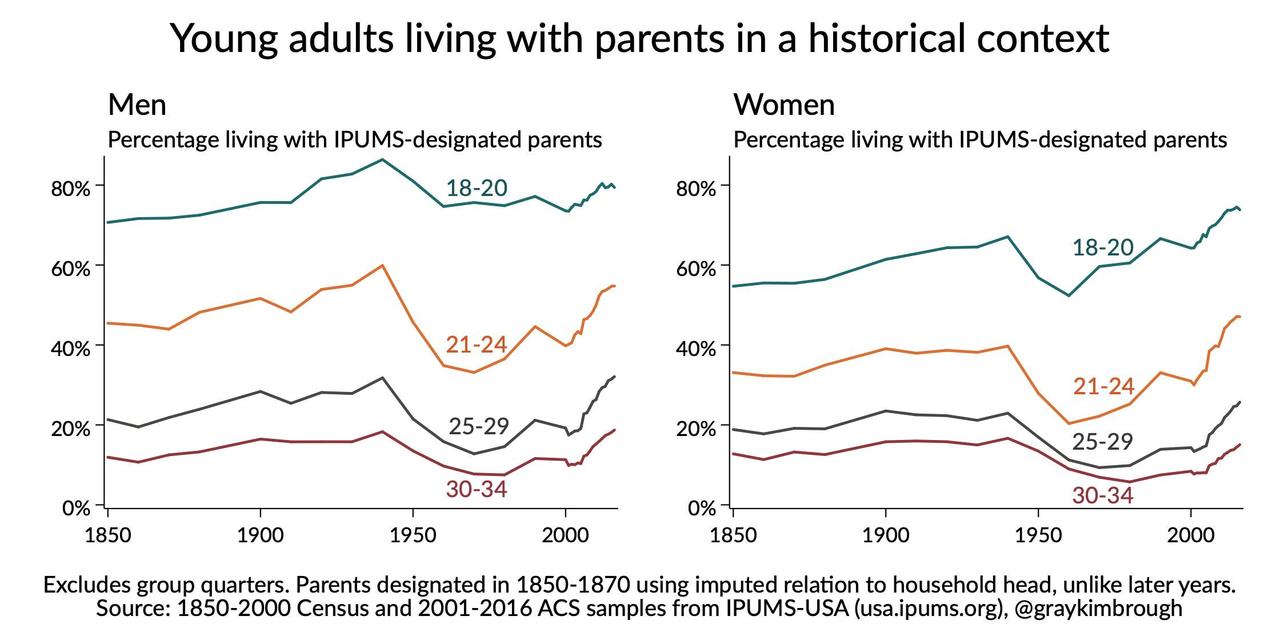

With nearly40% of young adultsin California living with their parents and a$1.6 trillion student debtcrisis taking more than just a little bite out of disposable income (and any hope of saving for many), economist Gary Kimbrough of the University of North Carolina at Greensboro hasthrown togethera ton of interesting data to answer the question: “What are the economic realities for young adults, and how have they changed from prior decades?“

While much of Kimbrough’s analysis was done in February, he’s revisited his work ahead of a January presentation on the topic of young adults living at home.

Living at home

Household formation is way down for 20-34 year olds.

In 1960 and 1970, over 70% of men and women age 20-34 (excluding those in group quarters) were heads of household/householders or spouses of householders.

What’s more, when broken down by categories “living with parents, household head or spouse of household head, living in group quarters (mostly prisons for these ages), and other arrangements like cohabiting and living with roommates,” it’s startling to watch how young adults have been living at home vs. starting their own families over time.

Another suggestion, from @DParrish: maps of the state-level rates of living with parents for 20-34 year olds, by gender. pic.twitter.com/nN5HuFx0A9

When it comes to “job hopping” – young adults are largely staying put – and “aren’t even switching jobs at anything close to the levels of those in their age groups before 2001” according to Kimbrough.

Let's be clear: millennials are not "job hopping." Young adults aren't even switching jobs at anything close to the levels of those in their age groups before 2001. pic.twitter.com/YyteHquu6K

“In 1992, middle-aged men were significantly more likely to have a bachelor’s degree than women or younger men. Now members of every group age 25-34 are more likely to have degrees than those men were,” writes Kimbrough, adding “Women’s college degree rates have shot up significantly more than men’s.”

In 1992, middle-aged men were significantly more likely to have a bachelor's degree than women or younger men. Now members of every group age 25-34 are more likely to have degrees than those men were. Women's college degree rates have shot up significantly more than men's. pic.twitter.com/WpcDaAxcPi

Since the Great Recession, Kimbrough noticed that “the propensity to work part time is about the same for women as pre-recession, but is up quite a bit for men under 35. Men 25-29 are still more likely to work PT than any time pre-2009.”

While examining economic realities for young adults since the Great Recession, I noticed: the propensity to work part time is about the same for women as pre-recession, but is up quite a bit for men under 35. Men 25-29 are still more likely to work PT than any time pre-2009. pic.twitter.com/VDD56DkF21

As more women have chosen careers over homemaking, Kimbrough provides an illustration of prime-age employment as a percentage of population, by gender. What’s more, young adult marriages have declined markedly over the last decade, continuing a trend which began mid-century.

With decennial Census and ACS data, I can examine marriage rates by age and gender over an even longer period. Young adult marriage rates have declined over the last decade, but they've been declining since mid-century. https://t.co/OZF2u3smnn

While not an “economic reality” per-se, it’s interesting to note that young men have been swapping TV-watching time for gaming.

Just looking at time spent watching TV/movies/streaming video, young adults are watching less while older adults are watching considerably more. https://t.co/v9sD2N9M9x

Of note, and unsurprisingly – young men living at home constitute the bulk of gamers watching less TV.

This is particularly interesting because, circling back to that increase in gaming time, for young adult men the increase in gaming is concentrated among those living with parents. pic.twitter.com/4mUwfAvSEH

Also unsurprising, with lower marriage rates and higher female employment, women in their 20s are “significantly less likely to have a child than a decade ago,” while those over the age of 32 are slightly more likely to have a kid.

Given the economic realities young adults have faced and the delays in marriage and homeownership we've seen, it should come as little surprise that women in their 20s are significantly less likely to have children in recent years than a decade or so ago. https://t.co/EQyKsBlxjx

Looking at five decades of prime age adults in the CPS ASEC:

1) Rates of women working increased until about 20 years ago, then stagnated 2) Men's working rates declined until about a decade ago, then stagnated 3) Parents (of children under 18) became older and less common pic.twitter.com/vRbTYPKOUg

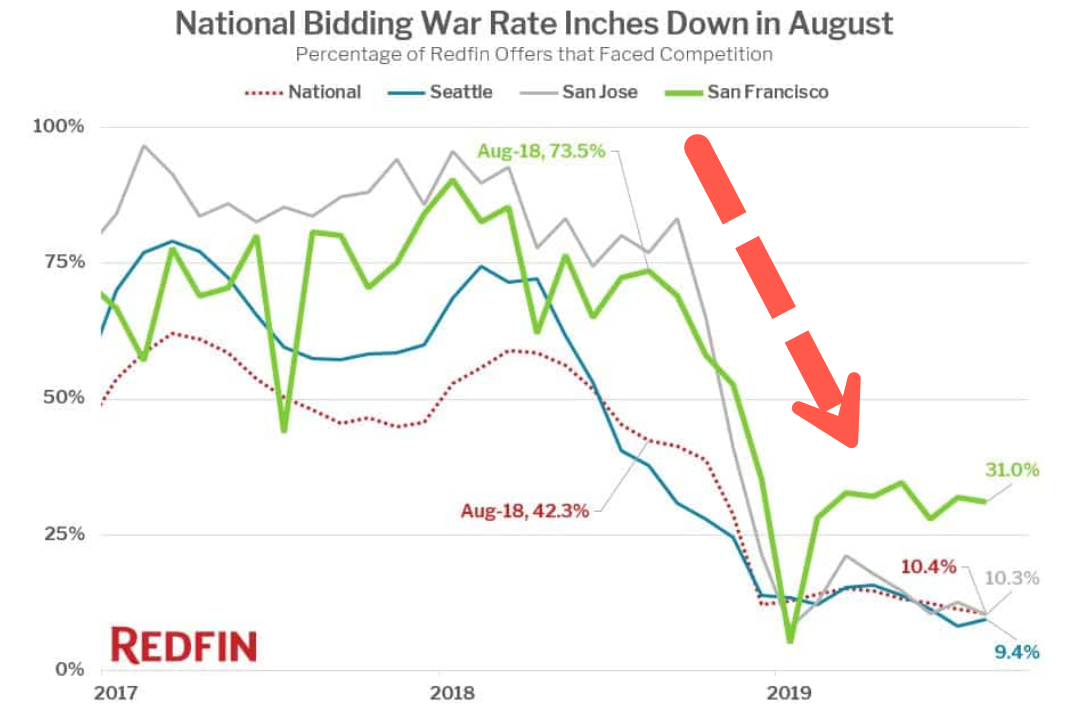

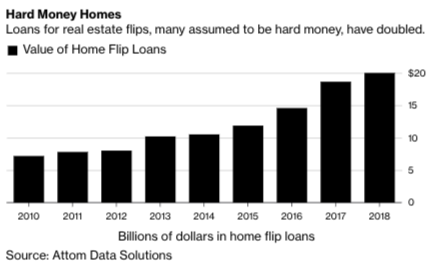

Bidding wars for homes in Seattle, San Jose, and San Francisco have crashed in the past year, reflecting an alarming national trend,according to a new report from Redfin.

The report found that the national bidding-war rate in August was 10.4%, down from 42% a year earlier. The rate printed at the lowest level since 2011.

At the start of 2018, the national bidding-war rate was 59%, then plunged as home buyers became uncomfortable with sky-high housing prices, increasing mortgage rates, and economic uncertainty surrounding the trade war. The housing market started to cool in late 2018, as the competition among home buyers collapsed by 4Q18, this is an ominous sign for the national housing market that could soon face a steep correction in price.

Even with eight months of declining mortgage rates in 2019, bidding-wars among home buyers continue to drop. This is somewhat troubling because the government’s narrative has been declining rates will boom housing, but as of Wednesday, mortgage applications continue to fall. Home buyers aren’t coming off the sidelines, and there’s too much uncertainty surrounding the economy with recession risks at the highest levels in more than a decade.

“Despite remaining near three-year lows, mortgage rates have failed to bring enough buyers to the market to rev up competition for homes this summer,” said Redfin chief economist Daryl Fairweather. Recession fears have been enough to spook some would-be buyers from making the big financial commitment of a home purchase. But assuming a recession doesn’t arrive this fall or winter, consumers will likely adjust to the new ‘normal’ of continued volatility in the stock and global markets, and the people who need and want to make a move will take advantage of low mortgage rates.”

As for one of the hottest real estate markets in the country, that being San Francisco, the bidding-war rate was 31% in August, down from 73.5% a year earlier. The lack of demand has certainly cooled housing prices, now expected to fall 1% YoY.

The rate in San Jose was 10.3% in August, down from 77% a year earlier, and in Seattle, another hot city for real estate, it saw its rate at 9.4%, down from 37.8% last August.

“Competition in the Seattle area has certainly slowed down since the second half of 2018. Last year, five out of five offers I submitted faced competition; now, it’s one in five,” said local Redfin agent Michelle Santos.

“Now, for desirable homes, competition is still fierce, and the winning offer is one that’s above the list price and waives contingencies. At the same time, average homes sit on the market for quite some time before they get any offers.”

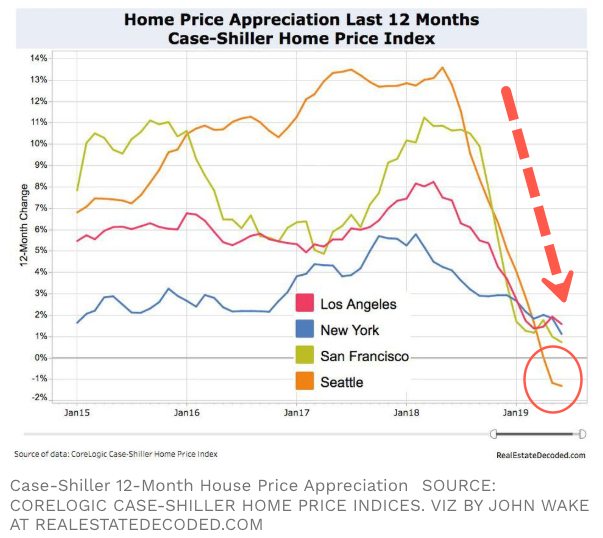

With the rapid decline of competition among home buyers and a flood of inventory entering the market, real home prices are starting to correct in major cities. Real price change over the last 12 months is falling in Seattle, San Francisco, and New York, according to new CoreLogic Case-Shiller Home Price Index data.

With competition among home buyers evaporating in a very short period of time, this could mean a downturn in the real estate market is imminent.

(City Journal) America’s big cities are, without exception, politically blue cities, with a new class of progressive politicians doing real damage to public order. When it comes to urban development, however, the blue monolith breaks down: socialists, city planners, cyclists, environmentalists, pragmatists, and social-justice activists are often at odds with one another. They might all support more housing, more density, and more public transportation, but they disagree sharply on the means for getting there.

In recent years, a new faction has emerged in city politics: what one might call the new Left urbanists. These activists believe that local governments must rebuild the urban environment—housing, transit, roads, and tolls—to produce a new era of city flourishing, characterized by social and racial justice and a net-zero carbon footprint. The urbanists rally around provocative slogans like “ban all cars,” “raze the suburbs,” and “single-family housing is white supremacy”—ironically, since they’re generally white, affluent, and educated themselves. They’re often employed in public or semipublic roles in urban planning, housing development, and social advocacy. They treat public housing, mass transit, and bicycle lanes as a kind of holy trinity—and they want to impose their religion on you.

Housing is the central political battleground for these progressive activists. As David Madden and Peter Marcuse write in their book, In Defense of Housing: “The residential is political—which is to say that the shape of the housing system is always the outcome of struggles between different groups and classes.” Their goal is not simply to get new housing built but to build new housing owned, operated, and controlled by the state. If they can dictate how cities construct new housing, their logic goes, they can dictate how people live—and set right society’s economic, social, and moral deficiencies.

The urbanists laid out their plans in a widely circulated report from the People’s Policy Project, a crowd-funded organization founded in 2017 that seeks to “fill the holes left by the current think tank landscape with a special focus on socialist and social democratic economic ideas.” They envision the construction of 10 million “municipal homes” over the next ten years. Under this proposal, government would become the nation’s largest landlord and residential construction firm, building more housing units than the entire private construction industry. The abysmal record of public housing in the United States, from the Cabrini-Green Homes in Chicago to the Foote Homes in Memphis, where crime and blight prevailed, makes no difference to these urbanists. They have simply rebranded “housing projects” to “municipal homes,” arguing that public housing has been “unjustly stigmatized” and that these new units will somehow avoid the fate of American public-housing ventures over the past half-century. They believe that the new “municipal homes” will resemble neighborhoods in Stockholm, Vienna, or Helsinki rather than in Detroit, Newark, or Oakland.

The question for the activists is not just how much new housing gets built but who builds it and who will live in it. That is, new developments must also tick off the boxes of identity politics. In cities like San Francisco, some activists have taken the hardline position of opposing all private housing construction, regardless of how it might reduce the cost of housing for middle-class residents. In an essay in the San Francisco Examiner, public-housing activists Andrew Szeto and Toshio Meronek called advocates for more private-market housing part of a “libertarian, anti-poor campaign to turn longtime sites of progressive organizing into rich-people-only zones” and compared them with alt-right white nationalists.

One might dismiss this as radical posturing in a local alt-weekly, but public-housing advocates have seized real power in city hall. They have learned how to use the zoning and permitting bureaucracy to achieve their goals of no new private development. In San Francisco’s Mission District, activists forced Laundromat owner Bob Tillman to spend $1.4 million and nearly five years to gain permission to convert his business into an apartment building. Activists and their enablers in city hall claimed that Tillman’s project would cause gentrification and displace minority residents, and forced him through a gauntlet of Kafkaesque legal proceedings. At one point, the planning commission even hired a “shadow consultant” to offer an expert opinion on whether the shadows cast by the proposed building would create social and racial inequities. To the new Left urbanists, housing isn’t just housing; it must be evaluated on social-justice standards. If it fails to measure up, it must go.

In New York City, progressive urbanists have seized on public transportation as a primary instrument of “social, environmental, immigrant, and economic justice.” New York’s subway system was designed in the early twentieth century to serve the practical needs of city residents, but today’s activists have come to see its tunnels and trains as grand mechanisms for cosmic justice. In its annual “Transportation and Equity” report, for example, the Straphangers Campaign argues that “the most vulnerable New Yorkers suffer disproportionately from high fares, long commutes, polluted air, and dangerous streets,” and therefore, “equity demands that state leaders prioritize transit in the public budget and policymaking process.”

The Straphangers estimate that an additional $30 billion in tax revenues would be needed to complete its desired overhaul of the mass-transit system, with a ten-year goal of upgrading 11 subway lines, building 130 new accessible subway stations, and purchasing 3,000 new subway cars and 5,000 new buses. While state and local leaders haven’t signed up for such an ambitious plan, they do support some of the Straphangers’ funding proposals to expand the transit system—including congestion pricing, a “millionaire’s tax,” marijuana tax, stock-transfer tax, and even a $3-per-package tax on Amazon deliveries.

Most New Yorkers would agree that investment in mass transit is a necessity, and there is a reasonable argument for congestion pricing in traffic-glutted Manhattan—but the activists don’t formulate their arguments on these practical grounds. A close reading of their reports reveals that the long-term vision involves elimination of the automobile, which remains a staple for middle-class residents in New York’s outer boroughs. In the Straphangers’ plan, activists want to restrict curbside space for cars dramatically by building “protected bike lanes on all major arterial streets across the five boroughs,” “giving developers incentives to contribute toward sustainable transportation over private vehicle usage,” and eliminating parking requirements for new housing projects. Activists deploy euphemisms like “transportation alternatives” and “transportation choices”; but at heart, their vision for mass transportation is not about choice but control. They want to remake the urban infrastructure in their own image: green, moral, healthy, just, and in solidarity with the masses—at least as those masses exist in their imagination.

The new Left urbanists’ fatal mistake is their failure to absorb the reality that cities are not just buildings, roads, tunnels, and bike lanes, but living entities. The urbanists can demolish and rebuild the physical environment, but they cannot pave over the people who make up our cities. Life in a metropolis is simply too complex, too variable, and too ephemeral—it will evade even the most careful planning. If we want better, more beautiful, cities, we must bring neighbors, developers, employers, and governments into the conversation. Our cities must be built through cooperation, not compulsion.

(Volfefe begins today) One day before the ECB is expected to cut rates further into negative territory and restart sovereign debt QE, moments ago president Trump resumed his feud with the Fed piling more pressure on Powell to cut rates “to ZERO or less” because the US apparently has “no inflation”, while also crashing the conversation over whether the US should issue ultra-long maturity debt (50, 100 years), saying the US “should then start to refinance our debt. INTEREST COST COULD BE BROUGHT WAY DOWN, while at the same time substantially lengthening the term.”

At least we now know who is urging Mnuchin to launch 50 and 100 year Treasuries. What we don’t know is just what school of monetary thought Trump belongs to – aside from Erdoganism of course – because while on one hand Trump claims that “we have the great currency, power, and balance sheet” on the other the US president also claims that “the USA should always be paying the lowest rate.” In a normal world, the strongest economy tends to pay the highest interest rate, but in this upside down world, who knows anymore, so maybe the Fed has just itself to blame.

Trump’s conclusion: “It is only the naïveté of Jay Powell and the Federal Reserve that doesn’t allow us to do what other countries are already doing. A once in a lifetime opportunity that we are missing because of “Boneheads.”

….The USA should always be paying the the lowest rate. No Inflation! It is only the naïveté of Jay Powell and the Federal Reserve that doesn’t allow us to do what other countries are already doing. A once in a lifetime opportunity that we are missing because of “Boneheads.”

Expect even more badgering of the Fed once the ECB cuts rates tomorrow.

One parting thought: if Bolton was fired for disagreeing with Trump over the Taliban, we wonder just how stable Powell’s job will be once the market actually does drop.

Foodbank South Australia has been approached by banks wanting to refer their clients to the charity, in the hope it will prevent people from defaulting on mortgage payments.

Foodbank South Australia is now working on a new agreement which would enable clients to access its food services directly, with a voucher funded by the major bank.

However, Foodbank South Australia chief executive Greg Pattinson told ABC Radio Adelaide it was still exploring how the program would work.

“That’s what we are exploring with some of the banks at the moment … it hasn’t started yet because we are still working through the process.

“We’ve never been approached by financial institutions in the past and the banks, to their credit, are doing the right thing in trying to find a way of keeping people in their houses.”

He said traditionally, Foodbank worked through charities and the welfare sector but it had seen an increase in the number of people who require food assistance that are working.

“Increasingly we are being approached now by organisations other than traditional charities, so schools for example, where the schools have identified the children of parents who are doing it tough,” he said.

“Each year we’ve seen an increase in South Australia of anywhere up to 20 per cent in the number of people seeking food assistance.”

‘Cost of living’ is causing a shift

Mr Pattinson said the stereotype of a person or family that required food assistance was diminishing.

He said more people must be suffering from mortgage stress because more of those needing help were from working families.

“We certainly do provide services to the unemployed and to people who are homeless,” he said.

“But we are seeing an increase in the numbers of working families and working Australians who are needing to seek food assistance because of cost of living increases.

“We see an increase in demand, for example every three months, when people get their electricity bills.

“It’s a case of those weeks where people are saying, ‘we’ll make sure the kids are fed, the roof is over our head but mum and dad don’t eat this week’.”

Trying to help clients ‘balance their budget’

Mr Pattinson said the fact it had been approached by the banks had shown a significant shift and Foodbank was working on a project to support those in need.

“We’re getting inquiries from schools, pastoral care workers, from principals at various schools around the state,” he said.

“And increasingly, we are now seeing inquiries from banks and financial institutions who are looking to try and find a way of helping their clients balance their budget.”

He said the program was still in its early stages, but he hoped Foodbank would have a concrete program in place within the next two to three months.

“It may even be as simple as the banks referring their clients to the Foodbank food hubs,” he said.

“But there would obviously be conditions to that which would have to be assessed by the bank to make sure those people … are genuinely in need of those services.

“We don’t want to shift the food away from people who are genuinely needing it.”

Recently, one big name money manager after another is on record telling people to buy hard assets. Why? Financial writer and precious metals expert Bill Holter says they all know what is coming. Holter contends,

“They understand that this is going to be the biggest monetary debasement in the history of history. They understand it’s hyperinflation that is on its way. They are late to the game, and they do manage billions and billions of dollars, and I don’t see how people talking about buying gold and buying silver are going to be able to get actual physical silver and physical gold in their hands or in their vaults.”

Holter is warning of a failure to deliver metal because demand is out-running supply. Holter says, “So far, this year . . . for gold, they have already EFP (Exchange for Physical) 4,200 tons just for the first eight months. . . . They don’t have the inventories to deliver. . . . The point being that is 4,200 tons in eight months. The world only produces 3,300 tons (of gold a year) and if you take out Russia and China, which do not export (gold), the whole total for the year is 2,800 tons. So, it looks like we are going to end up with 6,000 tons of gold EFP demand for delivery in a world that is only producing 2,800 tons. In silver, it’s worse. In silver in the first eight months, there has been 1.6 billion ounces EFP. That number is going to end up to about 2.4 billion of silver ounces (EFP) and the world produces less than 800 million ounces a year. The bottom line to what all this means is there is going to be a failure to deliver. Once there is a failure to deliver, only the Lord knows what kind of prices we are going to be looking at for gold and silver.”

Holter says a failure to deliver is not a maybe but a sure thing. Holter says, “Whether it is this year or the first few months of next year, it doesn’t matter. It is going to happen. . . . I can basically guarantee there is going to be a failure to deliver, and that failure to deliver is going to unmask and scare the crap out of the entire fractional reserve banking system and the fractional reserve commodity system. The whole thing is going to come down in a panic because somebody gets a failure to deliver. . . . If you listen to what Trump is saying, he wants a lower dollar. How much of a lower dollar does he want? He’s talking about debasing the currency to make the debt payable. . . . That is the most palatable way for any government to pay debt and that is to debase the currency and pay it off in monkey money.”

Join Greg Hunter as he goes One-on-One with precious metals expert Bill Holter

Max and Stacy discuss the synchronized markets causing pension fund managers to lose money in every single asset class. As trillions and trillions of freshly minted fiat money sloshes around the financial system looking for any return, Japan’s pension fund manager warns this time is different. Max continues his interview with Craig Hemke ofTFMetalsReport.comabout gold markets and how negative interest rates, hyperinflating at a rate of $1 trillion per week, will impact fiat currencies.

Having destroyed discipline, central banks have no way out of the corner they’ve painted us into.

It was such a wonderful fantasy: just give a handful of bankers, financiers and corporations trillions of dollars at near-zero rates of interest, and this flood of credit and cash into the apex of the wealth-power pyramid would magically generate a new round of investments in productivity-improving infrastructure and equipment, which would trickle down to the masses in the form of higher wages, enabling the masses to borrow and spend more on consumption, powering the Nirvana of modern economics: a self-sustaining, self-reinforcing expansion of growth.

But alas, there is no self-sustaining, self-reinforcing expansion of growth; there are only massive, increasingly fragile asset bubbles, stagnant wages and a New Gilded Age as the handful of bankers, financiers and corporations that were handed unlimited nearly free money enriched themselves at the expense of everyone else.

When credit is nearly free to borrow in unlimited quantities, there’s no need for discipline, and so a year of university costs $50,000 instead of $10,000, houses that should cost $200,000 now cost $1 million and a bridge that should have cost $100 million costs $500 million. Nobody can afford anything any more because the answer in the era of central bank “growth” is: just borrow more, it won’t cost you much because interest rates are so low.

And with capital (i.e. saved earnings) getting essentially zero yield thanks to central bank ZIRP and NIRP (zero or negative interest rate policies), then all the credit has poured into speculative assets, inflating unprecedented asset bubbles that will destroy much of the financial system when they finally pop, as all asset bubbles eventually do.

Nobody knows what the price of anything is in the funny-money era of central banks. And since capital earns next to nothing, the only way to earn a return is join the mad frenzy chasing risk assets ever higher, with the plan being to sell at the top to a greater fool, a strategy few manage as it requires selling into a rally that seems destined to climb to the stars.

Having destroyed discipline–why scrimp and save when you can always borrow to buy or invest?– central banks have no way out of the corner they’ve painted us into. If they “normalize” interest rates to historical averages (3% above real-world inflation), then all the zombie companies and households that are surviving only because rates are near-zero will go bankrupt, wiping out the “wealth” of all the loans that can no longer be paid.

“Normalized” rates would also bring down the global housing bubble, an implosion that would trigger trillions in losses, reversing the vaunted wealth effect into a realization that we’re all getting poorer, not richer, and collapsing the risky mountain of mortgage debt that’s been piled on absurdly overvalued properties globally.

In effect, central banks added a zero to “money” and anticipated that this trickery would generate ten times more of everything: ten times more productive investments, ten times more consumption, ten times more people borrowing ten times more money, and so on.

But the trickery failed, and all we have is $200,000 houses that cost $1 million, a year in college that costs $50,000 instead of $10,000, and so on.Having destroyed discipline and price discovery, central banks attempted to replace reality with fantasy, and now the absurd fantasy is imploding. The financial system and the real-world economy have both been destabilized by this fantasy, and now both are fragile in ways few understand.

The only “policies” central banks have is to issue more credit at negative interest rates, i.e. doing more of what’s failed spectacularly, until the entire rickety travesty of a mockery of a sham collapses.

That collapse is currently underway in slow motion, but given the increasing instability of asset bubbles, it could accelerate at any time.

The Federal Reserve Resistance: A recent official urges the central bank to help defeat Donald Trump.

Perhaps you’ve seen former Chairs of the Federal Reserve defending the central bank’s independence and fore swearing all political intentions. Fair enough. But then what are we to make of former Fed monetary Vice Chair William Dudley ’s marker that the Fed should help defeat President Trump in 2020? That’s the extraordinary message from the former, and perhaps future, Fed grandee in Bloomberg.

“Officials could state explicitly that the central bank won’t bail out an administration that keeps making bad choices on trade policy, making it abundantly clear that Trump will own the consequences of his actions,” Mr. Dudley asserts. We also think monetary policy should focus on prices rather than trade. But Mr. Dudley seems to be saying the Fed should do nothing to assist the economy even if it heads into recession. Then he goes further and essentially says the Fed should join The Resistance.

“There’s even an argument that the election itself falls within the Fed’s purview,” Mr. Dudley writes. “After all, Trump’s reelection arguably presents a threat to the U.S. and global economy, to the Fed’s independence and its ability to achieve its employment and inflation objectives. If the goal of monetary policy is to achieve the best long-term economic outcome, then Fed officials should consider how their decisions will affect the political outcome in 2020.”

Wow. Talk about stripping the veil. These columns wondered if Mr. Dudley was politically motivated while he was at the Fed, favoring bond buying to finance Barack Obama ’s deficit spending, urging the Fed to intervene in markets to boost housing, and keeping interest rates low for as long as possible. And now here Mr. Dudley is confirming that he views the Fed as an agent of the Democratic Party.

A key lesson of the Trump era is that every single allegedly neutral, nonpartisan, super-professional institution has turned out to be, in fact, a bunch of partisan hacks shilling for the permanent political party. Voters can be forgiven for adopting a “burn it all down” attitude in response.

The main problem with the US economy is that globalism has been deconstructing it. The offshoring of US jobs has reduced US manufacturing and industrial capability and associated innovation, research, development, supply chains, consumer purchasing power, and tax base of state and local governments. Corporations have increased short-term profits at the expense of these long-term costs. In effect, the US economy is being moved out of the First World into the Third World.

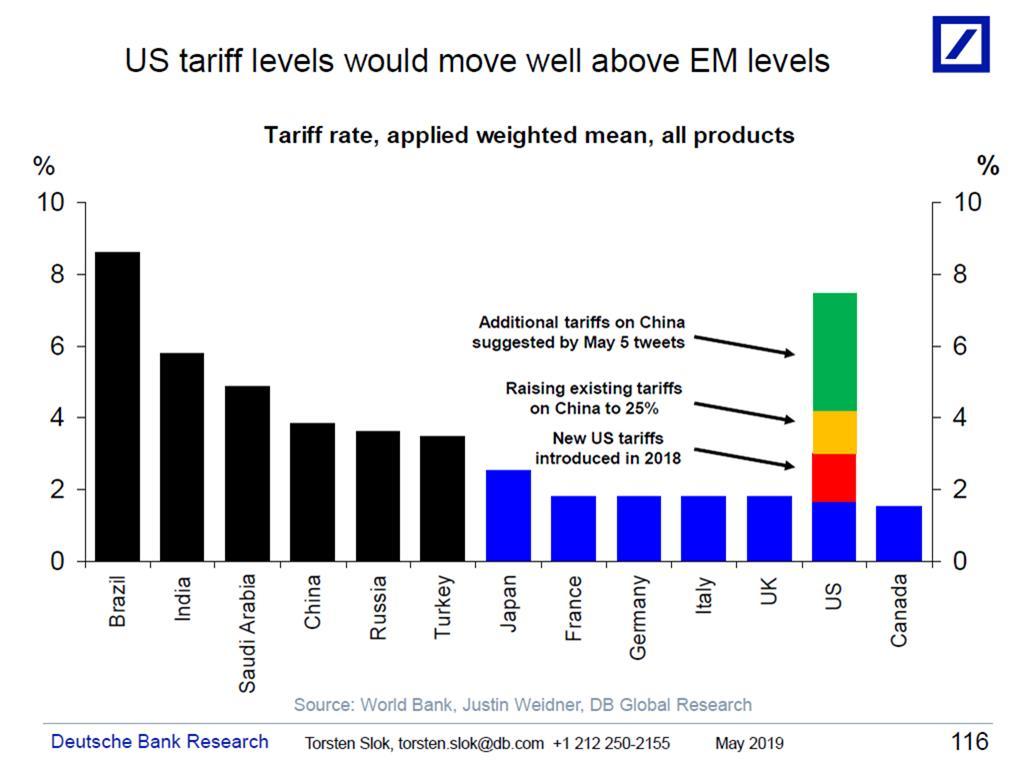

Tariffs are not a solution. The Trump administration says that the tariffs are paid by China, but unless Apple, Nike, Levi, and all of the offshoring companies got an exemption from the tariffs, the tariffs fall on the off shored production of US firms that are sold to US consumers. The tariffs will either reduce the profits of the US firms or be paid by US purchasers of the products in higher prices. The tariffs will hurt China only by reducing Chinese employment in the production of US goods for US markets.

The financial media is full of dire predictions of the consequences of a US/China “trade war.” There is no trade war. A trade war is when countries try to protect their industries by placing tariff barriers on the import of cheaper products from foreign countries. But half or more of the imports from China are imports from US companies. Trump’s tariffs, or a large part of them, fall on US corporations or US consumers.

One has to wonder that there is not a single economist anywhere in the Trump administration, the Federal Reserve, or anywhere else in Washington capable of comprehending the situation and conveying an understanding to President Trump.

One consequence of Washington’s universal economic ignorance is that the financial media has concocted the story that “Trump’s tariffs” are not only driving Americans into recession but also the entire world. Somehow tariffs on Apple computers and iPhones, Nike footwear, and Levi jeans are sending the world into recession or worse. This is an extraordinary economic conclusion, but the capacity for thought has pretty much disappeared in the United States.

In the financial media the question is: Will the Trump tariffs cause a US/world recession that costs Trump his reelection? This is a very stupid question. The US has been in a recession for two or more decades as its manufacturing/industrial/engineering capability has been transferred abroad. The US recession has been very good for the Asian part of the world. Indeed, China owes its faster than expected rise as a world power to the transfer of American jobs, capital, technology, and business know-how to China simply in order that US shareholders could receive capital gains and US executives could receive bonus pay for producing them by lowering labor costs.

Apparently, neoliberal economists, an oxymoron, cannot comprehend that if US corporations produce the goods and services that they market to Americans offshore, it is the offshore locations that benefit from the economic activity.

Offshore production started in earnest with the Soviet collapse as India and China opened their economies to the West. Globalism means that US corporations can make more money by abandoning their American work force. But what is true for the individual company is not true for the aggregate. Why? The answer is that when many corporations move their production for US markets offshore, Americans, unemployed or employed in lower paying jobs, lose the power to purchase the off shored goods.

I have reported for years that US jobs are no longer middle class jobs. The jobs have been declining for years in terms of value-added and pay. With this decline, aggregate demand declines. We have proof of this in the fact that for years US corporations have been using their profits not for investment in new plant and equipment, but to buy back their own shares. Any economist worthy of the name should instantly recognize that when corporations repurchase their shares rather than invest, they see no demand for increased output. Therefore, they loot their corporations for bonuses, decapitalizing the companies in the process. There is perfect knowledge that this is what is going on, and it is totally inconsistent with a growing economy.

As is the labor force participation rate. Normally, economic growth results in a rising labor force participation rate as people enter the work force to take advantage of the jobs. But throughout the alleged economic boom, the participation rate has been falling, because there are no jobs to be had.

In the 21st century the US has been decapitalized and living standards have declined. For a while the process was kept going by the expansion of debt, but consumer income has not kept pace and consumer debt expansion has reached its limits.

The Fed/Treasury “plunge protection team” can keep the stock market up by purchasing S&P futures. The Fed can pump out more money to drive up financial asset prices. But the money doesn’t drive up production, because the jobs and the economic activity that jobs represent have been sent abroad. What globalism did was to transfer the US economy to China.

Real statistical analysis, as contrasted with the official propaganda, shows that the happy picture of a booming economy is an illusion created by statistical deception. Inflation is under measured, so when nominal GDP is deflated, the result is to count higher prices as an increase in real output, that is, inflation becomes real economic growth. Unemployment is not counted. If you have not searched for a job in the past 4 weeks, you are officially not a part of the work force and your unemployment is not counted. The way the government counts unemployment is so extraordinary that I am surprised the US does not have a zero rate of unemployment.

How does a country recover when it has given its economy away to a foreign country that it now demonizes as an enemy? What better example is there of a ruling class that is totally incompetent than one that gives its economy bound and gagged to an enemy so that its corporate friends can pocket short-term riches?

We can’t blame this on Trump. He inherited the problem, and he has no advisers who can help him understand the problem and find a solution. No such advisers exist among neoliberal economists. I can only think of four economists who could help Trump, and one of them is a Russian.

Steve Bannon, former White House Chief Strategist, sits down with hedge fund giant Kyle Bass to discuss America’s current geopolitical landscape regarding China. Bannon and Bass take a deep dive into Chinese infiltration in U.S. institutions, China’s aggressiveness in the South China sea, and the potential for global conflict in the next few years. Filmed on October 5, 2018 at an undisclosed location, remains absolutely relevant today.

California Statist Supremacist and authoritarian governor, Gavin Newsom, recently blamed the state of Texas for California’s homeless crisis; rather than taking blame for long established policies California has instituted that stifle free enterprise with excessive regulation and taxation on those working hard to create private wealth.

Former California assemblyman turned Texas resident Chuck DeVore reacted to Newsom pushing the blame onto others. The vice president of the Texas Public Policy Foundation, Chuck DeVore, said Wednesday thatGavin Newsomis “responsible for the policies that have createdCalifornia’shomeless crisis,” in the wake of the governor blaming Texas for San Francisco’s homeless crisis. “What you’re seeing here are the words of a desperate man that we should almost feel sorry for,” DeVore, who served as a California assemblyman for six years, told “Fox & Friends.”

“Governor Gavin Newsom has been in office now for 22 straight years, starting at the San Francisco board of supervisors,” DeVore added. Homelessness has been rampant across the state of California in the past few years and merchants and homeowners have become increasingly vocal and incredibly irate at how things are going in the socialist dystopia.

Though San Francisco has more billionaires per capita than anywhere else in the world, its homeless problem hasrivaledthird-world nations, according toFox News. So much for all that “wealth inequality” the socialists are constantly pushing down the throats of the ignorant. Government policies are the most to blame for San Francisco’s wealth inequality.

“There’s more freedom in places like Texas, more opportunity to do what you want to do,” he said.

The sad truth is that socialism doesn’t work and it never has in all the times it’s been tried. Humans are not meant to be slaves and eventually, they figure out that no one has a higher claim over their lives than they do.

(Brandon Smith) One thing that is important to understand about the mainstream media is that they do tell the truth on occasion. However, the truths they admit to are almost always wrapped in lies or told to the public far too late to make the information useful. Dissecting mainstream media information and sifting out the truth from the propaganda is really the bulk of what the alternative media does (or should be doing). In the past couple of weeks I have received a rush of emails asking about the sudden flood of recession and economic crash talk in the media. Does this abrupt 180 degree turn by the MSM (and global banks) on the economy warrant concern? Yes, it does.

The first inclination of a portion of the liberty movement will be to assume that mainstream reports of imminent economic crisis are merely an attempt to tarnish the image of the Trump Administration, and that the talk of recession is “overblown”. This is partially true; Trump is meant to act as scapegoat, but this is not the big picture. The fact is, the pattern the media is following today matches almost exactly with the pattern they followed leading up to the credit crash of 2008. Make no mistake, a financial crash is indeed happening RIGHT NOW, just as it did after media warnings in 2007/2008, and the reasons why the MSM is admitting to it today are calculated.

Before we get to that, we should examine how the media reacted during the lead up to the crash of 2008.

Multiple mainstream outlets ignored all the crash signals in 2005 and 2006 despite ample warnings from alternative economists. In fact, they mostly laughed at the prospect of the biggest bull market in the history of stocks and housing (at that time) actually collapsing. Then abruptly the media and the globalist institutions that dictate how the news is disseminated shifted position and started talking about “recession” and “crash potential”. From the New York Times to The Telegraph to Reuters and others, as well as the IMF, BIS and Federal Reserve officials – Everyone suddenly started agreeing with alternative economists without actually deferring to them or giving them any credit for making the correct financial calls.

In 2007/2008, the discussion revolved around derivatives, a subject just complicated enough to confuse the majority of people and cause them to be disinterested in the root trigger for the economic crisis, which was central bankers creating and deflating bubbles through policy engineering. Instead, the public just wanted to know how the crash was going to be fixed. Yes, some blame went to the banking system, but almost no one at the top was punished (only one banker in the US actually faced fraud charges). Ultimately, the crisis was pinned on a “perfect storm” of coincidences, and the central banks were applauded for their “swift action” in using stimulus and QE to save us all from a depression level event. The bankers were being referred to as “heroes”.

Of course, central bank culpability was later explored, and Alan Greenspan even admitted partial responsibility, saying the Fed knew there was a bubble, but was “not aware” of how dangerous it really was. This was a lie. According to Fed minutes from 2004, Greenspan sought to silence any dissent on the housing bubble issue, saying that it would stir up debate on a process that “only the Fed understood”. Meaning, there was indeed discussion on housing and credit warning signs, but Greenspan snuffed it out to prevent the public from hearing about it.

Today we have a very similar dynamic. Use of the “R word” in the mainstream media and among central banks has been strictly contained for the past several years. In the October 2012 Fed minutes, Jerome Powell specifically warned of what would happen if the Federal Reserve tightened liquidity and raised interest rates into economic weakness. He warned that this would have negative effects on the stimulus addicted investment environment that the central bank had fostered. This discussion was held back from the public until only a year-and-a-half ago. As soon as Powell became chairman, he implemented those exact actions.

Only in the past year has talk of recession begun to break out, and only in the past couple of weeks have outlets become aggressive in pushing the notion that a financial crash is just around the corner. The reality is that if one removes the illusory support of central bank stimulus, our economy never left the “Great Recession” of 2008. Signals of renewed sharp declines in economic fundamentals have been visible since before the 2016 elections. Alarms have been blaring on housing, auto markets, manufacturing, freight and shipping, historic debt levels, the yield curve, etc. since at least winter of last year, just as the Fed raised rates to their neutral rate of inflation and increased asset cuts from the balance sheet to between $30 billion to $50 billion or more per month.

The media should have been reporting on economic crisis dangers for the past 2-3 years. But, they didn’t give these problems much credence until recently. So, what changed?

I can only theorize on why the media and the banking elites choose the timing they do to admit to the public what is about to happen. First, it is clear from their efforts to stifle free discussion that they do not want to let the populace know too far ahead of time that a crash is coming. According to the evidence, which I have outlined in-depth in previous articles, central banks and international banks sometimes engineer crash events in order to consolidate wealth and centralize their political power even further. Is it a conspiracy? Yes, it is, and it’s a provable one.

When they do finally release the facts, or allow their puppet media outlets to report on the facts, it seems that they allow for around 6-8 months of warning time before economic shock events occur. In the case of the current crash in fundamentals (and eventually stocks), the time may be shorter. Why? Because this time the banks and the media have a scapegoat in the form of Donald Trump, and by extension, they have a scapegoat in the form of conservatives, populists, and sovereignty activists.

The vast majority of articles flowing through mainstream news feeds on economic recession refer directly to Trump, his supporters and the trade war as the primary villains behind the downturn. The warnings from the Fed, the BIS and the IMF insinuate the same accusation.

Anyone who has read my work for the past few years knows I have been warning about Trump as a false prophet for the liberty movement and conservatives in general. And everyone knows my primary concern has been that the globalists will crash the Everything Bubble on Trump’s watch, and then blame all conservatives for the consequences.

To be clear, Trump is not the cause of the Everything Bubble, nor is he the cause of its current implosion. No president has the power to trigger a collapse of this magnitude, only central banks have that power. When Trump argues that the Fed is causing a downturn, he is telling the truth, but when he claims that recession fears are exaggerated, or “inappropriate”, he is lying. What he is not telling the public is that his job is to HELP the Fed in this process of controlled economic demolition.

Admissions of crisis in the media are coinciding directly with Trump’s policy actions. In other words, Trump is providing perfect cover for the central banks to crash the economy without receiving any of the blame. Trump’s insistence on taking full credit for the bubble in stock markets as well as fraudulent GDP and employment numbers, after specifically warning about all of these things during his election campaign, has now tied the economy like a noose around the necks of conservatives. The tone of warning in the media indicates to me that the banking elites are about to tighten that noose.

Another factor on our timeline beyond Trump’s helpful geopolitical distractions is the possibility of a ‘No-Deal’ Brexit in October. I continue to believe this outcome (or something very similar) has been pushed into inevitability by former Prime Minister Theresa May and EU globalists, and that it will be used as yet another scapegoat for the now accelerating crash in the EU. With Germany on the verge of admitting recession, Deutsche Bank on the edge of insolvency, Italy nearing political and financial crisis, etc., it is only a matter of months before Europe sees its own “Lehman moment”. The Brexit is, in my view, a marker for a timeline on when the crash will hit its stride.

To summarize, the mainstream media and global banking institutions have two goals in informing the public about recession right now – They are seeking to cover their own asses when the next shoe drops so they can say they “tried to warn us”, and, they are conditioning a majority of the public to automatically blame conservatives and sovereignty proponents when the consequences hit them without mercy.

As the truth of a recession smacks the public in the face, the media will likely pull back slightly, just as they did in 2008, and suggest that the downturn is “temporary”. They will claim it’s “not a repeat of the credit crisis”, or that it will “subside after Trump is out of office”. These will all be lies designed to keep the public complacent even as the house of cards collapses around them. The fact is, the hard data shows that economic conditions in the US and in most of the world are far more unstable than they were in 2008. We are not looking at the crash of a credit bubble, we are looking at the crash of the ‘Everything Bubble’.

The pace of the narrative is quickening, and I would suggest that a collapse of the bubble will move rather quickly, perhaps in the next four to six months. If it does, then it is likely that Trump is not slated for a second term as president in 2020. Trump’s highly divisive support for “Red Flag” gun laws, a move that will lose him considerable support among pro-gun conservatives, also indicates to me that it is likely he is not meant to be president in 2020. This is another sign that a massive downturn is closing in.

As events are unfolding right now, it appears that Trump has served his purpose for the globalists and is slated to be replaced next year; probably by an extreme far-left Democrat. There are only a couple of scenarios I can imagine in which Trump remains in office, one of them being a major war which might require him to retain the presidency so the globalists can finish out a regime change agenda in nations like Iran or Venezuela. This could, however, be pursued under a Democrat president almost as easily as long as Trump and his elitist cabinet lay the groundwork beforehand.

As in 2007/2008, it is unlikely that the mainstream would admit to a downturn that is not coming soon. Using the behavior of the media and of banking institutions as a guide, we can predict with some measure of certainty a crisis within the economy in the near term. Clearly, a major breakdown is slated to take place before the election of 2020, if not much sooner.

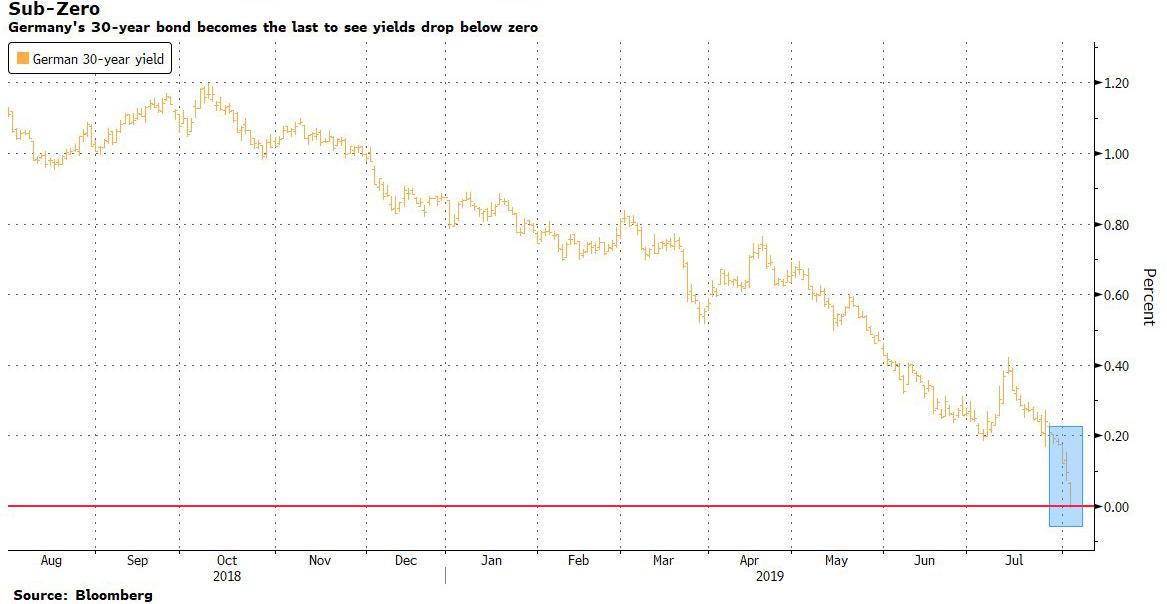

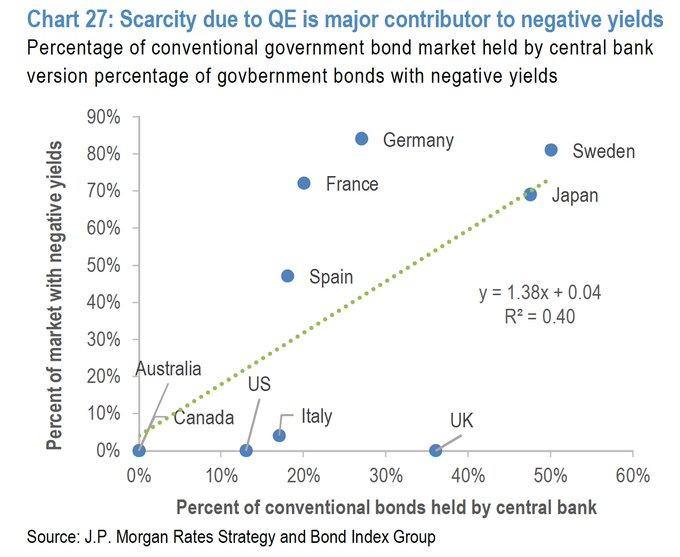

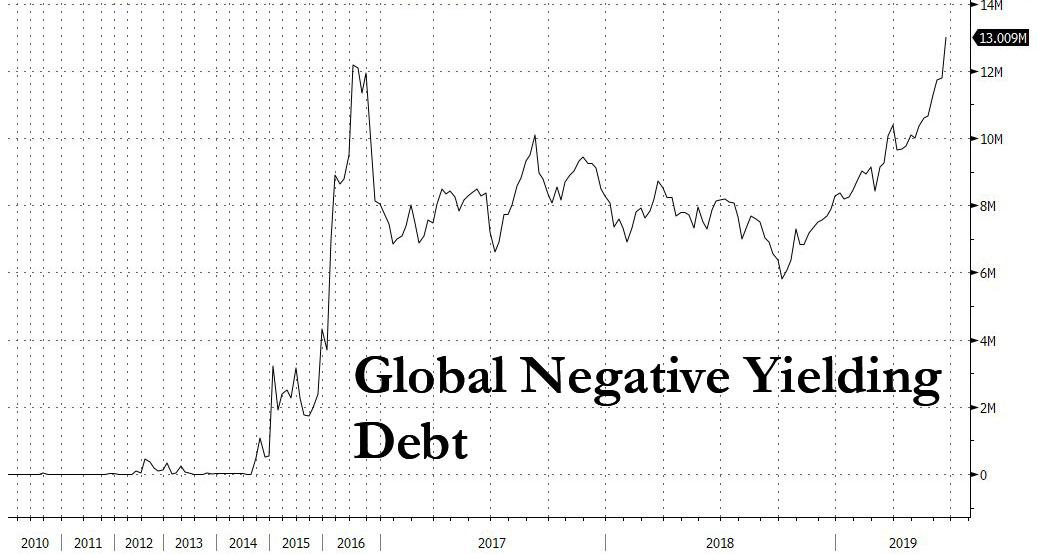

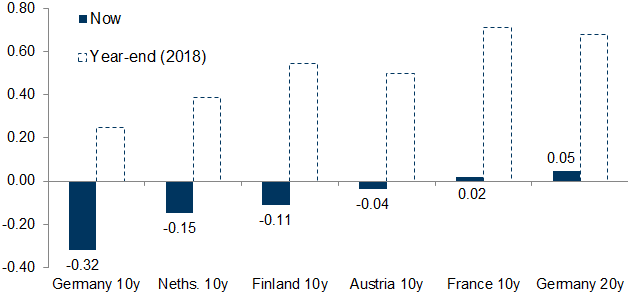

Earlier this weekZeroHedge wrotethat after decades of waiting, for Albert Edwards vindication was finally here – if only outside the US for now – because as per BofA calculations, average non-USD sovereign yields on $19 trillion in global debt had, as of Monday, turned negative for the first time ever at -3bps.

So now that virtually every rates strategist is rushing to out-“Ice Age” the SocGen strategist (who called the current move in rates years if not decades ago) by forecasting even lower yields (forgetting conveniently that just a year ago consensus called for the 10Y to rise well above 3% by… well, some time now), what does the man who correctly called the unprecedented move in global yields – which has sent $17 trillion in sovereign debt negative – think?

In a word: “There is a lot more to come.“

Although the tsunami of negative yields sweeping the eurozone has attracted most attention, yields have also plunged in the US with 30y yields falling to an all-time low just below 2%. For many this represents a bubble of epic proportions, driven by QE and ripe for bursting.

Here Edwards makes it clear that he disagrees , and cautions “that there is a lot more to come.”

What does he mean?

As Albert explains, “when you see the creeping advance of negative bond yields throughout the investment universe, you really start to doubt your sanity. For me it is not so much that 10Y+ government bond yields are increasingly negative, but when European junk bonds go negative I really start to scratch my head.” And as we wrote in “Redefining “High” Yield: There Are Now 14 Junk Bonds With Negative Yields“, there certainly is a lot of scratching to do.

One thing Edwards isn’t scratching his head over is whether this is a bond bubble: as he explains, his “own view is that this government bond rally is not a bubble but an appropriate reaction to the market discounting the next recession hitting the global economy from all over leveraged corners of the world (including China), with close to zero core inflation and precious few working tools left at policymakers’ disposal.”