The 24m2 (258 sq ft) Zoku Loft is designed as a living/working hybrid for ‘global nomads’ who typically seek temporary residence for between five days and several months. The designers add:

“In a regular hotel room or studio apartment, the bed always dominates. At Zoku, a big kitchen table serves as focal point. Use it to work across time zones, host dinner parties or gently rest your head after making a deadline. You decide. Then feel free to change your mind. The same goes for swapping the art on your walls, after which you can enjoy the view from your comfy Muuto design furniture.”

The loft has space-saving features like a retractable staircase and hide-away storage areas. It also includes a king size bed, dishwasher and commonly used home/office supplies. The first Zoku lofts are set to open in August in the eastern Canal District of Amsterdam. You can find much more information at the links below.

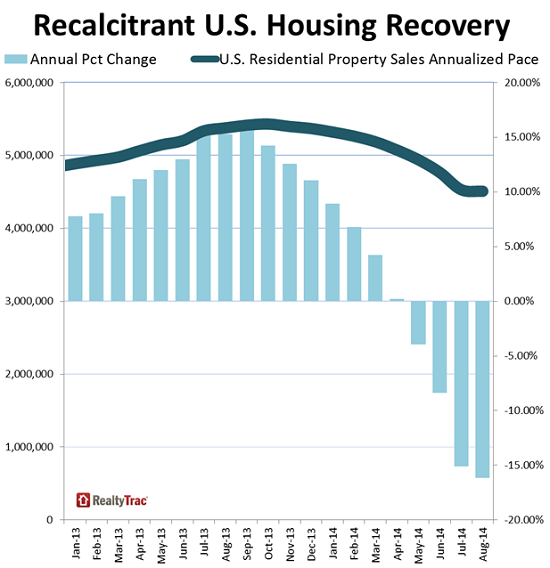

Seven years ago, the American home ownership “dream” was shattered when a housing bubble built on a decisively shaky foundation burst in spectacular fashion, bringing Wall Street and Main Street to their knees.

In the blink of an eye, the seemingly inexorable rise in the American home ownership rate abruptly reversed course, and by 2014, two decades of gains had disappeared and the ashes of Bill Clinton’s National Home ownership Strategy lay smoldering in the aftermath of the greatest financial collapse since the Great Depression.

In short, decades of speculative excess driven by imprudence, greed, and financial engineering and financed by the world’s demand for GSE debt had come crashing down and in relatively short order, a nation of homeowners was transformed into a nation of renters.

It wasn’t difficult to predict what would happen next.

As demand for rentals increased and PE snapped up foreclosures, rents rose, just as a subpar jobs market, a meteoric rise in student debt, tougher lending standards, and critically important demographic shifts put further pressure on home ownership rates. Now, America faces a rather dire housing predicament: buying and renting are both unaffordable. Or, as WSJ put it last month, “households are stuck between homes they can’t qualify for and rents they can’t afford.”

We’ve seen evidence of this across the country with perhaps the most telling statistic coming courtesy of The National Low Income Housing Coalition who recently noted that in no state can a minimum wage worker afford a one bedroom apartment.

In this context, Bloomberg is out with a list of 13 cities where single-family rents have risen by double-digits in just the last 12 months. Note that in Iowa, rents have risen more than 20% over the past year alone.

Landlords have been preparing to raise rents on single-family homes this year, Bloomberg reported in April. It looks like those plans are already being put into action.

The median rent for a three-bedroom single-family house increased 3.3 percent, to $1,320, during the second quarter, according to data compiled by RentRange and provided to Bloomberg by franchiser Real Property Management. Median rents are up 6.1 percent over the past 12 months. Even that kind of increase would have been welcome in 13 U.S. cities where single-family rents increased by double digits.

It’s more evidence that rising rents have affected a broad scope of Americans. Sixty percent of low-income renters spend more than 50 percent of their income on rent, according to a report in May from New York University’s Furman Center. High rents have also stretched the budgets of middle-class workers and made it harder for young professionals to launch careers and start families.

“You’re finding that people who wouldn’t have shared accommodations in the past are moving in with friends,”says Don Lawby, president of Real Property Management. “Kids are staying in their parents’ homes for longer and delaying the formation of families.”

And for those with short memories, we thought this would be an opportune time to remind you of who became America’s landlord in the wake of the crisis…

Examining the reasons to buy a house today may give us some idea where the housing market is heading in the future.

There are three reasons to buy a house:

Reason 1 – Utility

A house (any dwelling) is a shelter. It provides enjoyment, a home to raise one’s family, or just a place to watch that big screen TV. Utility is not quantifiable and it differs from household to household.

Reason 2 – Savings

If financed, a mortgage is a way of saving something every month until the mortgage is paid in full. If paid for, the savings come in the form of “owners’ equivalent rent”, which is what the census bureau uses to measure inflation in housing.

Reason 3 – Asset appreciation

At 5% appreciation per year, a $100k house today will be worth $412k in 30 years. Even a more modest 3% appreciation would result in better than a double.

Why Not to Buy a House Today

Based on the reasons above, it appears to be a slam dunk decision. Why would anyone not want to buy a house? There are three obstacles:

Obstacle 1 – Affordability

Housing, as a percentage of household income, is too expensive. A decade of ill-conceived government intervention and Federal Reserve accommodations prevented natural economic forces from driving house prices to equilibrium. As a result, not only is entry difficult, but many are struggling and are stuck in dire housing traps. Corelogic estimated that as of the 1st quarter of 2015, 10.2% of mortgages are still under water while 9.7 million households have less than 20% equity.

Obstacle 2 – High Risk

Say you are young couple that purchased a home two years ago, using minimal down financing. The wife is now pregnant and the husband has an excellent career opportunity in another city. The couple has insufficient savings and the house has not appreciated enough to facilitate a sale, which results in negative equity after selling expenses. The house can become a trap that diminishes a life time of income stream.

Obstacle 3 – “Dead zones”

Say you live in the middle of the country, in Kane County Illinois. For the privilege of living there, you pay 3% in property taxes. That is like adding 3% to a mortgage that never gets paid down. Your property would have to appreciate 3% per year just to break even. By the way, “appreciation” is unheard of in Kane County, good times or bad. There are many Kane Counties in the US. Real estate in these counties should be named something else and should not be co-mingled with other housing statistics. Employment is continuing to trend away from these areas. What is going to happen to real estate in these markets?

The Kane County court house: where real estate goes to vegetate

The factors listed above are nothing new. They provide some perspective as to where are are heading. Looking at each of the reasons and obstacles, they are all trending negatively.

The country is spending too much on housing, a luxury that is made possible by irresponsible Fed policies. 50% debt to income ratios are just insane and Ms. Yellen has the gall to call mortgage lending restrictive. Can we not see what is happening to Greece?

Mortgage backed securities held by the Federal Reserve System, a non-market central economic planning institution that is the chief instigator of house price inflation. Still growing, in spite of QE having officially ended – via Saint Louis Federal Reserve Research, click to enlarge.

Real estate is an investment that matures over time. The first few years are the toughest, until equity can be built up. With appreciation slowing, not to mention the possibility of depreciation, it is taking much longer to reach financial safety. The current base is weak, with too high a percentage of low equity and no equity ownership. The stress of a recession, or just a few years of a flat market, can impact the economy beyond expectations. The risks that might have been negligible once upon a time are much higher today. Many who purchased ten years ago are still living with the consequences of that ill-timed decision today.

By stepping back and looking at the big picture, we can see that real estate should be correcting and trending down. The reasons why our grandparents bought their homes have changed. Government intervention cannot last forever. It will change from accommodation to devastation, when they finally run out of ideas.

Conclusion

In summary, my working life had its origins in real estate and I am not trying to bite the hand that fed me. However, the reality is that the circumstances that prevailed when I entered the market are non-existent today. I seriously doubt that I would chose real estate as a career, or as an investment avenue, if I were starting over. As for buying a house, I would consider it more of a luxury as opposed to an investment, and one has to be prepared for the possibility of it being a depreciating asset, especially if one decides to move.

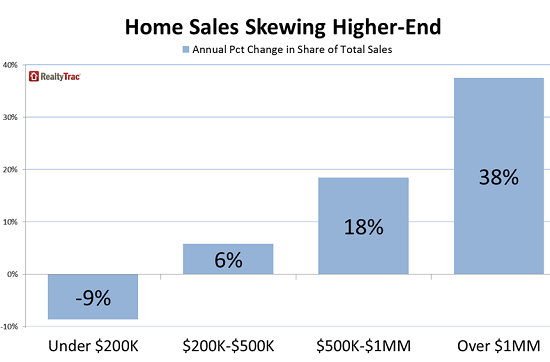

RealtyTrac has released its June and Midyear 2015 U.S. Home Sales Report, which shows distressed sales, cash sales and institutional investor sales in June were all down from a year ago to multi-year lows even as sales to first-time home buyers and other buyers using FHA loans increased compared to a year ago in June and reached a two-year high in the second quarter. Buyers using Federal Housing Administration (FHA) loans—typically low down payment loans utilized by first-time home buyers and other buyers without equity to bring to the closing table—accounted for 23 percent of all single family home and condo sales with financing—excluding all-cash sales—in the second quarter of 2015, up from 20 percent in the first quarter and up from 19 percent in the second quarter of 2014 to the highest share since the first quarter of 2013.

The report also shows 914,291 single family and condo sales through April 2015—the most recent month with complete sales data available—at the highest level through the first four months of a year since 2006, a nine-year high.

“As the investor-driven housing recovery faded in the first half of 2015, first-time home buyers, boomerang buyers and other traditional owner-occupant buyers started to step into the gap and pick up the slack,” said Daren Blomquist, vice president at RealtyTrac. “This is good news for sellers in many markets, providing them with strong demand from a larger pool of buyers, and U.S. sellers so far in 2015 are realizing the biggest gains in home price appreciation since 2007. In June sellers sold for above estimated market value on average for the first time in nearly two years.”

Cash buyers down nationwide, up in New York City and 20 other markets All-cash buyers accounted for 22.9 percent of all single family home and condo sales in June, down from 24.7 percent of all sales in the previous month and down from 29.1 percent of all sales in June 2014 to the lowest share of monthly cash sales nationwide since August 2008. The June cash sales share was almost half the peak of 42.1 percent in February 2011. Metros with highest share of cash sales in June were Homosassa Springs, Florida (53 percent), Naples-Marco Island, Florida (52 percent); Miami (50 percent); Sebastian-Vero Beach, Fla. (50 percent); and New York (49 percent).

“The first six months of sales in South Florida have been at a record pace. The millennials are entering the market along with many home buyers who had difficulty during the last recession while the investor market has quieted,” said Mike Pappas, CEO and president of Keyes Company, covering the South Florida market. “It is a real market with real buyers and sellers. The buyers have many lending options and are still enjoying low interest rates and many sellers are selling at their peak prices.”

In New York and 20 other markets analyzed for the report, the share of cash sales increased from a year ago, counter to the national trend. The New York metro share of cash sales increased from 40 percent in June 2014 to 49 percent in June 2015. Other markets with an increasing share of cash sales included Raleigh, North Carolina; Greenville, South Carolina; Bellingham, Washington located between Seattle and Vancouver, Canada; Knoxville, Tennessee; Providence, Rhode Island; and San Jose, Calif.

“Cash buyers have been a significant player in the Seattle housing market over the past 18 months, but the modest drop in this buyer segment doesn’t come as a surprise given the aggressive rise in home prices in recent months,” said Matthew Gardner, chief economist at Windermere Real Estate, covering the Seattle market. “Higher prices are forcing these buyers to dig deeper into their pockets and this process has started to push some out of the market. The same can be said for first time buyers; many of them are having a hard time qualifying for a loan also due to the rise in home prices in Seattle.”

Institutional investor share in June matches record low Institutional investors—entities purchasing at least 10 properties during a calendar year—accounted for 1.7 percent of all single family and condo sales in June, the same share as in May but down from 3.5 percent of all sales in June 2014. The 1.7 percent share of institutional investor sales in May and June was the lowest monthly share going back to January 2000—the earliest data is available—and was less than one-third of the monthly peak of 6.1 percent in February 2013.

Metro areas with the highest share of institutional investor sales in June 2015 were Macon, Georgia (10.2 percent); Columbia, Tenn. (9.5 percent); Memphis, Tenn. (8.7 percent); Detroit (7.8 percent); and Charlotte (5.3 percent).

Other major metros with a high percentage of institutional investor sales included Tampa (4.3 percent); Atlanta (4.0 percent); Tulsa, Oklahoma (3.9 percent); Oklahoma City (3.7 percent); and Nashville (3.7 percent).

The share of institutional investors increased from a year ago in just four markets: Detroit; Macon, Georgia; Lincoln, Nebraska; and Birmingham, Alabama.

Distressed sales drop to new record low Distressed sales—properties in the foreclosure process or bank-owned when they sold—accounted for eight percent of all single family and condo sales in June, down from 10.6 percent of all sales in May and down from 19.0 percent of all sales in June 2014 to the lowest monthly share since January 2011—the earliest that data is available. The share of distressed sales reached a monthly peak of 45.9 percent of all single family and condo sales in February 2011.

Metro areas with the highest share of distressed sales in June were Salisbury, North Carolina (30.6 percent); Gainesville, Ga. (23.8 percent); Jacksonville, N.C. (22.2 percent); Boone, N.C. (22.1 percent); and Marion, Ohio (21.9 percent).

Major metro areas with a high share of distressed sales in June included Chicago (14.7 percent); Baltimore (14.4 percent); Orlando (13.8 percent); Jacksonville, Fla. (13.6 percent); and Memphis (13.4 percent).

Markets with highest and lowest share of FHA loan purchases in first half of 2015 Nationwide, buyers using FHA loans accounted for 22 percent of all financed sales in the first half of 2015, up from 19 percent of all sales in 2014 and up from 20 percent of all sales in 2013.

Among markets with a population of 1 million or more, those with the highest share of buyers using FHA loans in the first six months of 2015 were Riverside-San Bernardino-Ontario in inland Southern California (35 percent); Las Vegas (32 percent); Oklahoma City (31 percent); Salt Lake City (30 percent); and Phoenix (29 percent).

Major markets with the lowest share of buyers using FHA loans in the first six months of 2015 were San Jose, California (7 percent); Hartford, Connecticut (10 percent); San Francisco (12 percent); Boston (12 percent); and Milwaukee (13 percent).

First-half 2015 sellers realized highest home price gains since 2007 Single family home and condo sellers in the first half of 2015 sold for an average of 13 percent above their original purchase price, the highest average percentage in home price gains realized by sellers since 2007, when it was 30 percent.

Major markets where sellers in the first half of 2015 realized the biggest average home price gains were San Jose, Calif. (41 percent); San Francisco (37 percent); Denver (29 percent); Portland (25 percent); Los Angeles (25 percent); and Seattle (20 percent).

There were six major markets where sellers in the first half of 2015 on average sold below their original purchase price: Chicago (seven percent below); Cleveland (seven percent below); Hartford, Conn. (three percent below); Jacksonville, Fla. (two percent below); St. Louis (one percent below); and Orlando (one percent below).

Homes sold in June sold above estimated market value on average Single family homes and condos in June sold for an average of $291,450 compared to an average $287,634 estimated market value for those same homes at the time of sale—a 101 percent price-to-value ratio. June was the first time since July 2013 that the national price-to-value ratio exceeded 100 percent.

Major metro areas with the highest price-to-value ratios—where homes sold the most above estimated market value—were San Francisco (106 percent); Hartford, Conn. (105 percent); Baltimore (105 percent); Rochester, N.Y. (104 percent); and Providence, R.I. (103 percent).

Other major markets with price-to-value ratios above 100 percent in June included Washington, D.C. (103 percent); Phoenix (103 percent); Sacramento (103 percent); Portland (103 percent); Seattle (102 percent); San Jose (102 percent); and St. Louis (102 percent).

Sales volume at highest level since 2006 in 16 percent of markets analyzed The number of single family homes and condos sold in the first four months of 2015 were at the highest level in the first four months of any year since 2006 in 43 out of 264 (16 percent) metropolitan statistical areas with sufficient home sales data. Markets at nine-year highs included Tampa; Denver; Columbus, Ohio; Jacksonville, Fla. and San Antonio.

There were 23 markets where sales volume in the first four months of 2015 was at 10-year highs, including Denver; Columbus, Ohio; San Antonio; Tucson, Ariz.; and Palm Bay-Melbourne-Titusville, Fla.

Among major metro areas with a population of one million or more, 22 out of 51 markets (43 percent) were at eight-year highs for single family home and condo sales in the first four months of the 2015, including New York, Dallas, Houston, Seattle and Portland.

New York City, Los Angeles, Honolulu: They’re all places you would think would be popular destinations for Americans. So it might come as a surprise that these are among the cities U.S. residents are fleeing in droves.

The map below shows the 20 metropolitan areas that lost the greatest share of local people to other parts of the country between July 2013 and July 2014, according to a Bloomberg News analysis of U.S. Census Bureau data. The New York City area ranked 2nd, losing about a net 163,000 U.S. residents, closely followed by a couple surrounding suburbs in Connecticut. Honolulu ranked fourth and Los Angeles ranked 14th. The Bloomberg calculations looked at the 100 most populous U.S. metropolitan areas.

Interestingly, these are also the cities with some of the highest net inflows of people from outside the country. That gives many of these cities a steadily growing population, despite the net exodus of people moving within the U.S.

So what’s going on here? Michael Stoll, a professor of public policy and urban planning at the University of California Los Angeles, has an idea. Soaring home prices are pushing local residents out and scaring away potential new ones from other parts of the country, he said. (Everyone knows how unaffordable the Manhattan area has become.)

And as Americans leave, people from abroad move in to these bustling cities to fill the vacant low-skilled jobs. They are able to do so by living in what Stoll calls “creative housing arrangements” in which they pack six to eight individuals, or two to four families, into one apartment or home. It’s an arrangement that most Americans just aren’t willing to pursue, and even many immigrants decide it’s not for them as time goes by, he said.

In addition, the growing demand for high-skilled workers, especially in the technology industry, brought foreigners who possess those skills to the U.S. They are compensated appropriately and can afford to live in these high-cost areas, just like Americans who hold similar positions. One example is Washington, D.C., which had a lot of people from abroad arriving to soak up jobs in the growing tech-hub, Stoll said.

Other areas weren’t so lucky. Take some of the Rust Belt cities that experienced fast drops in their American populations, like Cleveland, Dayton and Toledo, even though they are relatively inexpensive places to live. These cities didn’t get enough international migrants to make up for the those who left, a reflection of the fact that locals were probably leaving out of a lack of jobs.

This is part of a multiple-decade trend of the U.S. population moving away from these manufacturing hubs to areas in the Sun Belt and the Pacific Northwest, Stoll said. Retiring baby boomers are also leaving the Northeast and migrating to more affordable places with better climates.

This explains why the majority of metropolitan areas in Florida and Texas, as well as west-coast cities like Portland, had an influx of people.

El Paso, Texas, the city that residents fled from at the fastest pace, also saw a surprisingly small number of foreigners settling in given how close it is to Mexico.

“A lot of young, reasonably educated people are having a hard time finding work there,” Stoll said. “They’re not staying in town after they graduate,” leaving for the faster-growing economies of neighboring metro areas like Dallas and Austin, he said.

Methodology: Bloomberg ranked 100 of the most populous U.S. metropolitan areas based on their net domestic migration rates, from July 1, 2013 to July 1, 2014, as a percentage of total population as of July 2013. Domestic migration refers to people moving within the country (e.g. someone moving from New York City to San Francisco). A negative rate indicates more people leaving than coming in. International migration refers to a local resident leaving for a foreign country or someone from outside the U.S. moving into the U.S.

WASHINGTON (AP) — Americans bought homes in June at the fastest rate in over eight years, pushing prices to record highs as buyer demand has eclipsed the availability of houses on the market.

The National Association of Realtors said Wednesday that sales of existing homes climbed 3.2 percent last month to a seasonally adjusted annual rate of 5.49 million, the highest rate since February 2007. Sales have jumped 9.6 percent over the past 12 months, while the number of listings has risen just 0.4 percent.

Median home prices climbed 6.5 percent over the past 12 months to $236,400, the highest level reported by the Realtors not adjusted for inflation.

Home-buying has recently surged as more buyers are flooding into the real estate market. Robust hiring over the past 21 months and an economic recovery now in its sixth year have enabled more Americans to set aside money for a down payment. But the rising demand has failed to draw more sellers into the market, causing tight inventories and escalating prices that could cap sales growth.

“The recent pace can’t be sustained, but it points clearly to upside potential,” said Ian Shepherdson, chief economist at Pantheon Macroeconomics.

A mere five months’ supply of homes was on the market in June, compared to 5.5 months a year ago and an average of six months in a healthy market.

Some markets are barely adding any listings. The condominium market in Massachusetts contains just 1.8 months’ supply, according to a Federal Reserve report this month. The majority of real estate agents in the Atlanta Fed region – which ranges from Alabama to Florida- said that inventories were flat or falling over the past year.

Some of the recent sales burst appears to come from the prospect of low mortgage rates beginning to rise as the Federal Reserve considers raising a key interest rate from its near-zero level later this year. That possibility is prompting buyers to finalize sales before higher rates make borrowing costs prohibitively expensive, noted Daren Blomquist, a vice president at RealtyTrac, a housing analytics firm.

The premiums that the Federal Housing Administration charges to insure mortgages are also lower this year, further fueling buying activity, Blomquist said.

It’s also possible that home buyers are checking the market for listings more aggressively, making it possible for them to act fast with offers despite the lack of new inventory.

“Buyers can more quickly be alerted of new listings and also more conveniently access real estate data to help them pre-search a potential purchase before they even step foot in the property,” Blomquist said. “That may mean we don’t need such a large supply of inventory to feed growing sales.”

Properties typically sold last month in 34 days, the shortest time since the Realtors began tracking the figure in May 2011. There were fewer all-cash, individual investor and distressed home sales in the market, as more traditional buyers have returned.

Sales improved in all four geographical regions: Northeast, Midwest, South and West.

Still, the limited supplies could eventually prove to be a drag on sales growth in the coming months.

Ever rising home values are stretching the budgets of first-time buyers and owners looking to upgrade. As homes become less affordable, the current demand will likely taper off.

Home prices have increased nearly four times faster than wages, as average hourly earnings have risen just 2 percent over the past 12 months to $24.95 an hour, according to the Labor Department.

Some buyers are also bristling at the few available options on the market. Tony Smith, a Charlotte, North Carolina real estate broker, said some renters shopping for homes are now choosing instead to re-sign their leases and wait until a better selection of properties comes onto the market.

New construction has yet to satisfy rising demand, as builders are increasingly focused on the growing rental market.

Approved building permits rose increased 7.4 percent to an annual rate of 1.34 million in June, the highest level since July 2007, the Commerce Department said last week. Almost all of the gains came for apartment complexes, while permits for houses last month rose only 0.9 percent.

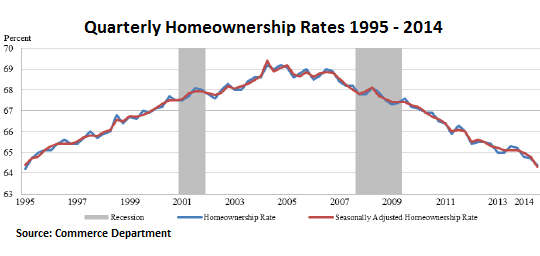

The share of Americans owning homes has fallen this year to a seasonally adjusted 63.8 percent, the lowest level since 1989.

Real estate had until recently lagged much of the six-year rebound from the recession, hobbled by the wave of foreclosures that came after the burst housing bubble.

But the job market found new traction in early 2014. Employers added 3.1 million jobs last year and are on pace to add 2.5 million jobs this year. As millions more Americans have found work, their new paychecks are increasingly going to housing, both in terms of renting and owning.

Low mortgage rates have also helped, although rates are now starting to climb to levels that could slow buying activity.

Average 30-year fixed rates were 4.09 percent last week, according to the mortgage giant Freddie Mac. The average has risen from a 52-week low of 3.59 percent.

The Southern California housing market, known for its dramatic swings, is settling into a more normal, healthy pattern.

Home sales are up. All-cash and investor purchases are down. And home prices are rising at a more sustainable pace than in the last few years.

Economists said those factors put the regional housing market on a path for growth that won’t wash away in a tsunami of foreclosures and ruined credit scores.

“The healing continues,” said Stuart Gabriel, director of UCLA’s Ziman Center for Real Estate.

On Thursday, fresh evidence of that trend emerged in a report from CoreLogic. Home sales posted a sizable 18.1% pop in June from a year earlier, while the median price rose 5.7% from June 2014 to $442,000, the real estate data firm said.

The sales increase, the largest in nearly three years, put the number of sales just 9.6% below average, CoreLogic said. A year ago, sales were nearly 24% below average.

Notably, it appears more families are entering the market as the economy improves. Although still elevated in comparison to long-term averages, the share of absentee buyers — mostly investors — slid to 21.1%, the lowest percentage since April 2010, CoreLogic said.

“This is the real recovery,” Christopher Thornberg, founding partner of Beacon Economics, said of a market where increasingly buyers actually want to live in the houses they purchase. “The last was the investor recovery.”

Sustained job growth has given more people the confidence to buy houses, CoreLogic analyst Andrew LePage said. California added a robust 54,200 jobs in May, one of the strongest showings in the last year.

The housing market improvement extends nationally, with sales of previously owned homes up in May to the highest pace in nearly six years, partly because more first-time buyers entered the market, according to data from the National Assn. of Realtors.

One factor driving deals is an expected decision from the Federal Reserve to raise its short-term interest rate later this year, real estate agents say.

In response, families rushed to lock in historically low rates this spring, agents say. CoreLogic’s sales figures represent closed deals, meaning most went into escrow during May.

Leslie Appleton-Young, chief economist for the California Association of Realtors, cautioned that the market still has too few homes for sale and that prices have risen to a point where many can’t afford a house.

Unless that changes, sales are unlikely to reach levels in line with historical norms, she said.

“I am not saying the housing market isn’t robust,” she said.

“I think housing affordability is a big issue…The biggest problem is losing millennials to places like Denver and Austin and Seattle.”

For now, deals are on the rise and people are paying more.

Sales and prices climbed in all six south land counties: Los Angeles, Orange, Riverside, San Bernardino, San Diego and Ventura. In Orange County, the median price rose 4.9% from a year earlier to $629,500.

In Los Angeles County, prices climbed 8.7% to $500,000.

Russian buyers are scrambling to buy bargain properties in Greece as the financial meltdown has eroded luxury real-estate prices, Damien Sharkov reported for Newsweek.

Just to give you an idea of the scale of sales: The Greek real-estate agency IRM Aegean Estate has put properties in package deals, with two villas in Corfu —private beach and all — selling together for $4.9 million.

According to the German magazine Bild, the number of luxury Greek villas bought by Russians has more than doubled in the past year, Newsweek reported.

That’s partially because of Russia’s own currency crisis — rich people are looking for safe places to park cash — but also because real-estate prices in Greece have fallen roughly 50% since 2009, Bild reported.

“If a villa on the Greek island of Syros still cost €1.6m a few years ago, it is now selling for just €800,000,” IRM founder Isabelle Razi told Newsweek. That’s a fall to roughly $870,000 from $1.74 million with today’s exchange rates.

The strengthening relationship between Russian buyers and their Greek holdings is mirrored by ties between their national governments.

Last month the two countries agreed to build a $2.27 billion gas pipeline, Sharkov reported for Newsweek, and some critics are concerned the move signifies a tug-of-war between the West and Russia, as Athens may be inching toward the Kremlin’s umbrella of influence.

Along Manhattan’s 57th Street, stretching from Columbus Circle on the west side to Park Avenue on the east, you’ll soon find more than a half-dozen glittering, ultra-exclusive condominium towers that will offer unparalleled views of Central Park — and virtually the entire city. Welcome to Manhattan’s Billionaires’ Row, the current trophy real estate of the 1%.

The mega projects, with some penthouse floor plans such as those at 432 Park Ave. expanding to more than 8,200 square feet, are expected to list on average for more than $14.5 million (or $4,375 a square foot). Some even have living rooms bigger than most condominium units in Manhattan (the average size of a condo unit in Manhattan being 1,100 square feet.)

The sky-high prices on Billionaires’ Row will also help push the average price for a unit at new developments in Manhattan to $7 million (or $2,787 a square foot) by 2017, according to Gabby Warshawer, head of research for CityRealty, a New York real-estate research firm. Manhattan condo units on average were just $1 million as recently as 2005, says Warshawer.

An inside look at ‘Billionaires’ Row’

For the Manhattan, and global, elite, trophy apartments in the sky, overlooking Central Park, will set new marks for luxury and price.

Aside from the luxuriously appointed apartments and the central location, there’s something else that’s appealing about the apartments: As Noble Black, a real-estate agent who has marketed condominium units in One57, points out, unlike many city co-ops — whose boards are famously picky and have turned down such notables as pop singer Madonna and former President Richard Nixon as potential residents — buyers on Billionaires’ Row don’t need to open up their financial books to co-op boards or even submit to interviews.

Here’s a look at what $14 million–plus will buy you along Billionaires’ Row …

These sky-high trophy homes overlooking Central Park set new marks for both luxury and price

157 West 57 St.

One57, built by developer Extell, was the first on the Billionaires’ Row strip to be built and is 75 stories tall and more than 1,000 feet high. The building, which includes a Park Hyatt hotel with services catering to owners’ every whim, with room service, maid service and a spa and gym, saw its penthouse apartment sell for a record $100.5 million in December 2014 to a yet-unnamed buyer. All told, the entire building’s 92 condo units were worth an estimated $2 billion and will sell for an average of $6,300 a square foot, according to CityRealty.

111 West 57th St.

Built by JDS Development Group, this extraordinarily slender skyscraper will rise 80 stories and more than 1,400 feet. That’s taller than the Empire State Building. The 60 apartments will start at $14 million according to the developer’s website and rise to $100 million, according to CityRealty. Completion is expected in 2018.

550 Madison Ave.

The rehab of the 37-story Sony Building will include a $150 million penthouse and possibly a five-star hotel. The skyscraper, completed in 1983, was sold to Joseph Chetrit, a real-estate developer for more than $1 billion in 2013. The sell-out price for the property will likely approach $2 billion, or more than $4,400 a square foot, CityRealty says.

432 Park Ave.

Currently the tallest residential building in the city at 1,396 feet, the condominium development by CIM Group/Macklowe Properties recently sold its penthouse for $99.5 million.The building’s total sales will be worth an estimated $3 billion (or nearly $6,300 a square foot), according to CityRealty, assuming the 144-unit building is sold out. Closings on the remaining units — which range from $17 million to $81 million — are expected to start at the end of the year.

53 W. 53rd St.

Hines Development’s 77-story condominium has been in the works for 10 years but has only recently started marketing its 100-plus units. The 1,050-foot-high trapezoidal tower with geodesic elements is set to be completed in 2018 and to include a unit priced at $70 million, according to CityRealty. All told, the sell-out price is anticipated at upward of $2 billion.

According to the National Association of Realtors (NAR), the U.S. housing market will continue its gradual pace of recovery as more home buyers enter a tight housing market for the balance of 2015, being nudged by rising mortgage rates and improving consumer confidence.

NAR’s chef economist Lawrence Yun has released the following observations for the US economy at large, and for the U.S. housing market specifically:

The U.S. Economy

GDP growth was slightly negative in the first quarter but will pick up in the second half. For the year as whole, GDP will expand at 2.1 percent. Not bad but not great. A slow hum.

Consumer spending will open up because of lower gasoline prices. Personal consumption expenditure grew at 2.1 percent rate in the first quarter. Look for 3 percent growth rate in the second half.

Auto sales dropped a bit in the first quarter because of heavy snow, but will ramp up nicely in the second half.

Spending for household furnishing and equipment has been solid, growing 6 percent in the first quarter after clocking 6 percent in the prior. Recovering housing sector is the big reason for the nice numbers.

Spending at restaurants was flat. That is why retail vacancy rates are not notching down.

Online shopping is up solidly. That is why industrial and warehouse vacancy rates are coming down.

Spending for health care grew at 5 percent in the first quarter, marking two consecutive quarters of fast growth. The Affordable Care Act has expanded health care demand. The important question for the future is will the supply of new doctors and nurses expand to meet this rising demand or will it lead to medical care shortage?

Business spending was flat in the first quarter but will surely rise because of large cash holdings and high profits.

Spending for business equipment rose by 3 percent in the first quarter. Positive and good, but nothing to shout about.

Spending for business structures (building of office and retail shops, for example) fell by 18 percent. The freezing first-quarter weather halted some construction. This just means pent-up construction activity in the second half.

In the past small business start-ups spent and invested. It was not uncommon to experience double-digit growth rates for 3 years running for business equipment. Not happening now. But business spending will inevitably grow because of much improved business financial conditions of lower debt and more profits and rising GDP.

What has been missing is the “animal spirit” of entrepreneurship. The number of small business start-ups remains surprisingly low at this phase of economic expansion.

Residential construction spending increased 6 percent in the first quarter. Housing starts are rising and therefore this component will pick up even at a faster pace in the second half.

Government spending fell by 1 percent. At the federal level, non-defense spending grew by 2 percent, while national defense spending fell by 1 percent. At the state and local level, spending fell by 1 percent.

The federal government is still running a deficit. Even though it is spending more than what it takes in from tax revenue, the overall deficit level has been falling to a sustainable level. It would be ideal to run a surplus, but a falling deficit nonetheless does provide the possibility of less severe sequestration.

U.S. government finances are ugly. Interestingly though, they are less ugly than other countries. That is why the U.S. dollar has been strengthening against most other major currencies. It’s like finding the least dirty shirt from a laundry basket.

Imports have been rising while exports have been falling. The strong dollar makes it so. Imports grew by 7 percent while exports fell by 6 percent. The net exports (at minus $548 billion) were the worst in seven years. Fortunately, with the West Coast longshoremen back at work, the foreign trade situation will not worsen, which means it will help GDP growth.

All in all, GDP will growth by 2.5 to 3 percent in the second half. That translates into jobs. A total of 2.5 million net new jobs are likely to be created this year.

Unemployment insurance filings have been rising in oil-producing states of Texas and North Dakota.

Unemployment insurance filings for the country as a whole have been falling, which implies lower level of fresh layoffs and factory closings. That assures continuing solid job growth in the second half of the year.

We have to acknowledge that not all is fine with the labor market. The part-time jobs remain elevated and wage growth remains sluggish with only 2 percent annual growth. There are signs of tightening labor supply and the bidding up of wages. Wages are to rise by 3 percent by early next year. The total income of the country and the total number of jobs are on the rise.

The U.S. Housing Market Mid-2015 Trends

Existing home sales in May hit the highest mark since 2009, when there had been a homebuyer tax credit … remember, buy a home and get $8,000 from Uncle Sam. This tax credit is no longer available but the improving economy is providing the necessary incentive and financial capacity to buy. Meanwhile new home sales hit a seven-year high and housing permits to build new homes hit an eight-year high. Pending contracts to buy existing homes hit a nine-year high.

Buyers are coming back in force. One factor for the recent surge could have been due to the rising mortgage rates. As nearly always happens, the initial phase of rising rates nudges people to make decision now rather than wait later when the rates could be higher still.

The first-time buyers are scooping up properties with 32 percent of all buyers being as such compared to only 27 percent one year ago. A lower fee on FHA mortgages is helping.

Investors are slowly stepping out. The high home prices are making the rate of return numbers less attractive.

Buyers are back. What about sellers? Inventory remains low by historical standards in most markets. In places like Denver and Seattle, where a very strong job growth is the norm, the inventory condition is just unreal – less than one month supply.

The principal reason for the inventory shortage is the cumulative impact of homebuilders not being in the market for well over five years. Homebuilders typically put up 1.5 million new homes annually. Here’s what they did from 2009 to 2014:

550,000

590,000

610,000

780,000

930,000

1.0 million

Where is 1.5 million? Maybe by 2017.

Building activity for apartments has largely come back to normal. The cumulative shortage is on the ownership side.

Builders will construct more homes. By 1.1 million in 2015 and 1.4 million in 2016. New home sales will follow this trend. This rising trend will steadily relieve housing shortage.

There is no massive shadow inventory that can disrupt the market. The number of distressed home sales has been steadily falling – now accounting for only 10 percent of all transactions. It will fall further in the upcoming months. There is simply far fewer mortgages in the serious delinquent stage (of not being current for 3 or more months). In fact, if one specializes in foreclosure or short sales, it is time to change the business model.

In the meantime, there is still a housing shortage. The consequence is a stronger than normal home price growth. Home price gains are beating wage-income growths by at least three or four times in most markets. Few things in the world could be more frustrating and demoralizing than for renters to start a savings program but only to witness home prices and down payment requirements blowing past them by.

Housing affordability is falling. Home prices rising too fast is one reason. The other reason is due to rising mortgage rates. Cash-buys have been coming down so rates will count for more in the future.

The Federal Reserve will be raising short-term rates soon. September is a maybe, but it’s more likely to be in October. The Fed will also signal the continual raising of rates over the next two years. This sentiment has already pushed up mortgage rates. They are bound to rise further, particularly if inflation surprises on the upside.

Inflation is likely to surprise on the upside. The influence of low gasoline prices in bringing down the overall consumer price inflation to essentially zero in recent months will be short-lasting. By November, the influence of low gasoline prices will no longer be there because it was in November of last year when the oil prices began their plunge. That is, by November, the year-over-year change in gasoline price will be neutral (and no longer big negative). Other items will then make their mark on inflation. Watch the rents. It’s already rising at near 8-year high with a 3.5 percent growth rate. The overall CPI inflation could cross the red line of above 3 percent by early next year. The bond market will not like it and the yields on all long-term borrowing will rise.

Mortgage rates at 4.3% to 4.5% by the year end and easily surpassing 5% by the year end of 2016.

The rising mortgage rates initially rush buyers to decide but a sustained rise will choke off as to who can qualify for a mortgage. Fortunately, there are few compensating factors to rising rates.

Credit scores are not properly aligned with expected default rate. New scoring methodology is being tested and will be implemented. In short, credit scores will get boosted for many individuals after the new change.

FHA mortgage premium has come down a notch thereby saving money for consumers. By the end of the year, FHA program will show healthier finances. That means, there could be additional reduction to premiums in 2016. Not certain, but plausible.

Fannie and Freddie are owned by the taxpayers. And they are raking-in huge profits as mortgages have not been defaulting over the past several years. The very high profit is partly reflecting too-tight credit with no risk taking. There is a possibility to back a greater number of lower down payment mortgages to credit worthy borrowers without taking on much risk. In short, mortgage approvals should modestly improve next year.

Portfolio lending and private mortgage-backed securities are slowly reviving. Why not? Mortgages are not defaulting and there is fat cash reserves held by financial institutions. Less conventional mortgages will therefore be more widely available.

Improving credit available at a time of likely rising interest rates is highly welcome. Many would-be first-time buyers have been more focused about getting a mortgage (even at a higher rate) than with low rates.

All in all, existing and new home sales will be rising. Combined, there will be 5.8 million home sales in 2015, up 7 percent from last year. Note the sales total will still be 25 percent below the decade ago level during the bubble year. Home prices will be rising at 7 percent. For the industry, the business revenue will be rising by 14 percent in 2015. The revenue growth in 2016 will be additional 7 to 10 percent.

As noted previously, we are in a new dark age where college does not pay. At $1.3 trillion, the student debt balance is not getting any smaller. Facing a lifetime of debt slavery, the millennial generation is doing whatever they can to avoid homelessness. Whether it’s stripping or working at Rent A Gent, all options are on the table. Now, they are flocking to Seeking Arrangement to prostitute themselves so they can pay for school. Since 2009, the number of student sugar babies has increased by 1,200%!

The labor force participation rate for college graduates has been on a relentless downtrend.

It is getting even more expensive to go to school. Even after adjusting for inflation, college costs have gone up more than 400% in the last 30 years.

Many young people don’t see any good alternatives to going to school, so they jump in head first. Facing enormous bills, they turn to sites like Seeking Arrangement for help. These aren’t just women either. 15% of student sugar babies are men, and plenty of sugar mommas are on the site too.

Here are the numbers.

And here are the sugar babies by major.

The abundance of nurses on Seeking Arrangement shouldn’t be surprising for regular readers. Personal care aides and nurses are the fastest growing jobs in America.

Here are the perks of Seeking Arrangement.

And here are the sugar babies.

Previously, it was common for students to take food and service jobs, but soon, you will hear college students casually sharing their day with their sugar daddy. Welcome to the modern hooker economy.

A job seeker yawns as he waits in front of the training offices of Local Union 46, a union representing metallic lathers and reinforcing iron workers, in the Queens borough of New York.

WASHINGTON (AP) — Even after another month of strong hiring in June and a sinking unemployment rate, the U.S. job market just isn’t what it used to be.

Pay is sluggish. Many part-timers can’t find full-time work. And a diminished share of Americans either have a job or are looking for one.

Yet in the face of global and demographic shifts, this may be what a nearly healthy U.S. job market now looks like.

An aging population is sending an outsize proportion of Americans into retirement. Many younger adults, bruised by the Great Recession, are postponing work to remain in school to try to become more marketable. Global competition and the increasing automation of many jobs are holding down pay.

Many economists think these trends will persist for years despite steady job growth. It helps explain why the Federal Reserve is widely expected to start raising interest rates from record lows later this year even though many job measures remain far below their pre-recession peaks.

“The Fed may recognize that this is a new labor-market normal, and it will begin to normalize monetary policy,” said Patrick O’Keefe, an economist at accounting and consulting firm CohnReznick.

Thursday’s monthly jobs report from the government showed that employers added a solid 223,000 jobs in June and that the unemployment rate fell to 5.3 percent from 5.5 percent in May. Even so, the generally improving job market still bears traits that have long been regarded as weaknesses. Among them:

— A shrunken labor force.

The unemployment rate didn’t fall in June because more people were hired. The rate fell solely because the number of people who had become dispirited and stopped looking for work far exceeded the number who found jobs.

The percentage of Americans in the workforce — defined as those who either have a job or are actively seeking one — dropped to 62.6 percent, a 38-year low, from 62.9 percent. (The figure was 66 percent when the recession began in 2007.) Fewer job holders typically means weaker growth for the economy. The growth of the labor force slowed to just 0.3 percent in 2014, compared with 1.1 percent in 2007.

“It is highly unlikely that we are going to see our (workforce) participation rate move anywhere near where it was in 2007,” O’Keefe says.

This marks a striking reversal. The share of Americans in the workforce had been steadily climbing through early 2000, and a big reason was that more women began working. But that influx plateaued in the late 1990s and has drifted downward since.

— The retirement of the vast baby boom generation.

The aging population is restraining the growth of the workforce. The pace of retirements accelerated in 2008, when the oldest boomers turned 62, when workers can start claiming some Social Security benefits. Economists estimate that retirements account for about half the decline in the share of Americans in the workforce since 2000.

From that perspective, the nation as a whole is beginning to resemble retirement havens such as Florida. Just 59.3 percent of Floridians are in the workforce.

— Younger workers are starting their careers later.

Employers are demanding college degrees and even postgraduate degrees for a higher proportion of jobs. Mindful of this trend, teens and young people in their 20’s are still reading textbooks when previous generations were punching time clocks.

The recession “basically told everybody that they need an education to get better jobs,” says John Silvia, chief economist at Wells Fargo. “So how would young people respond? They stayed in school.”

Fewer than 39 percent of 18- and 19-year-olds are employed, down from 56 percent in 2000. For people ages 20 to 24, the proportion has fallen to 64 percent from 72 percent.

— The number of part-timers who would prefer full-time work remains high.

About 6.5 million workers are working part time but want full-time jobs, up from 4.6 million before the recession began. This is partly a reflection of tepid economic growth. But economists also point to long-term factors: Industries such as hotels and restaurants that hire many part-timers are driving an increasing share of job growth, researchers at the Federal Reserve Bank of San Francisco have found.

As more young adults put off working, some employers are turning to older workers to fill part-time jobs. Older workers are more likely to want full-time work, raising the level of so-called involuntary part-time employment.

Many economists also point to the Obama administration’s health care reforms for increasing part-time employment. The law requires companies with more than 100 employees to provide health insurance to those who work more than 30 hours.

Michael Feroli, an economist at JPMorgan Chase, says this could account for as much as one-third of the increase in part-time jobs.

— Weak pay growth.

The average hourly U.S. wage was flat in June at $24.95 and has risen just 2 percent over the past year. The stagnant June figure dispelled hopes that strong job growth in May heralded a trend of steadily rising incomes.

In theory, steady hiring is supposed to reduce the number of qualified workers who are still seeking jobs. And a tight supply of workers tends to force wages up.

Yet a host of factors have complicated that theory. U.S. workers are competing against lower-paid foreigners. And automation has threatened everyone from assembly line workers to executive secretaries.

Still, economists at Goldman Sachs forecast that average hourly pay will grow at an annual pace of about 3.5 percent by the end of 2016. That is a healthy pace. But it will have taken much longer to reach than in previous recoveries.

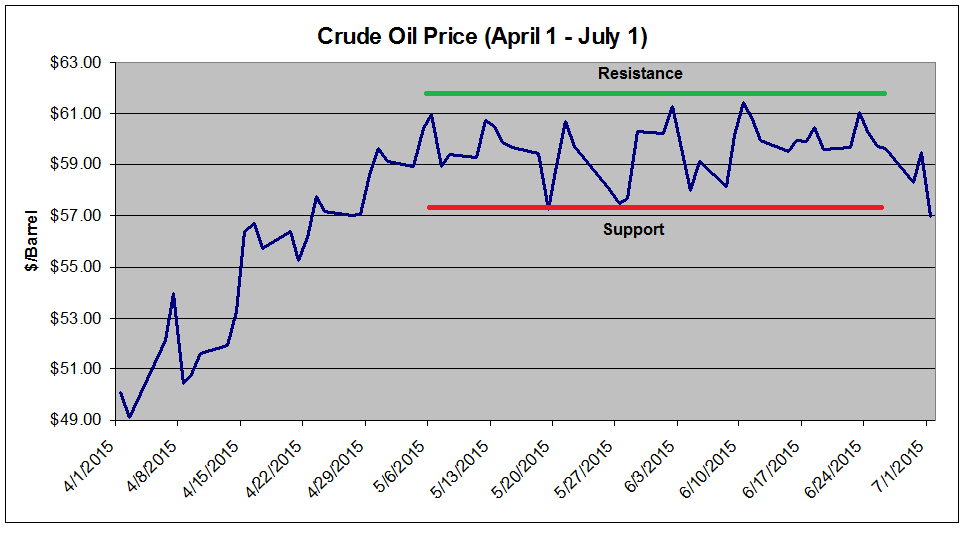

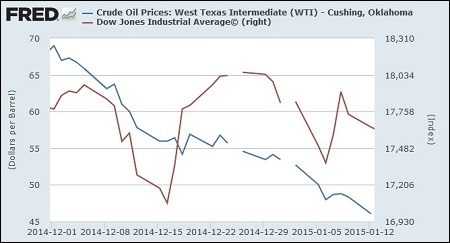

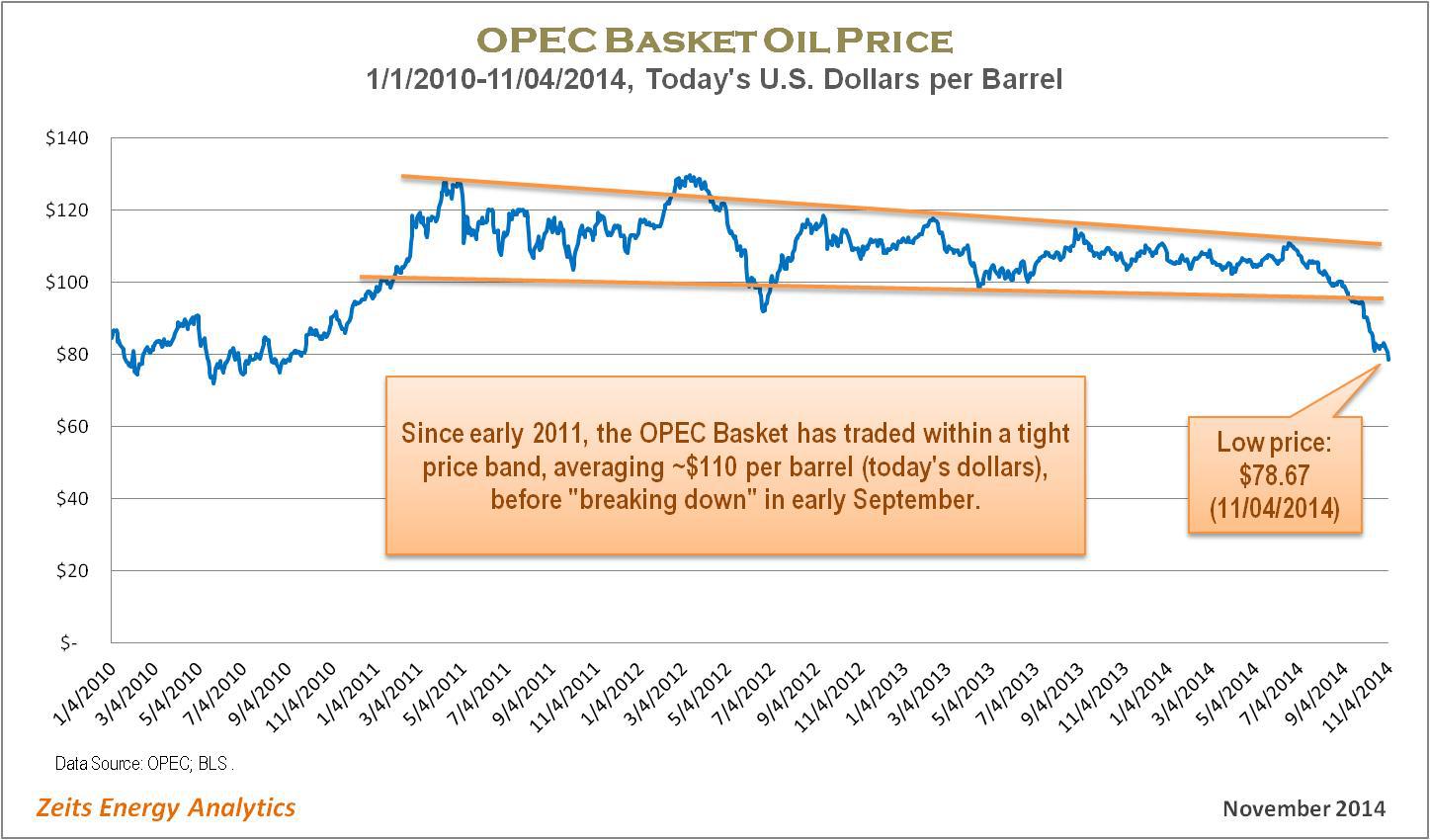

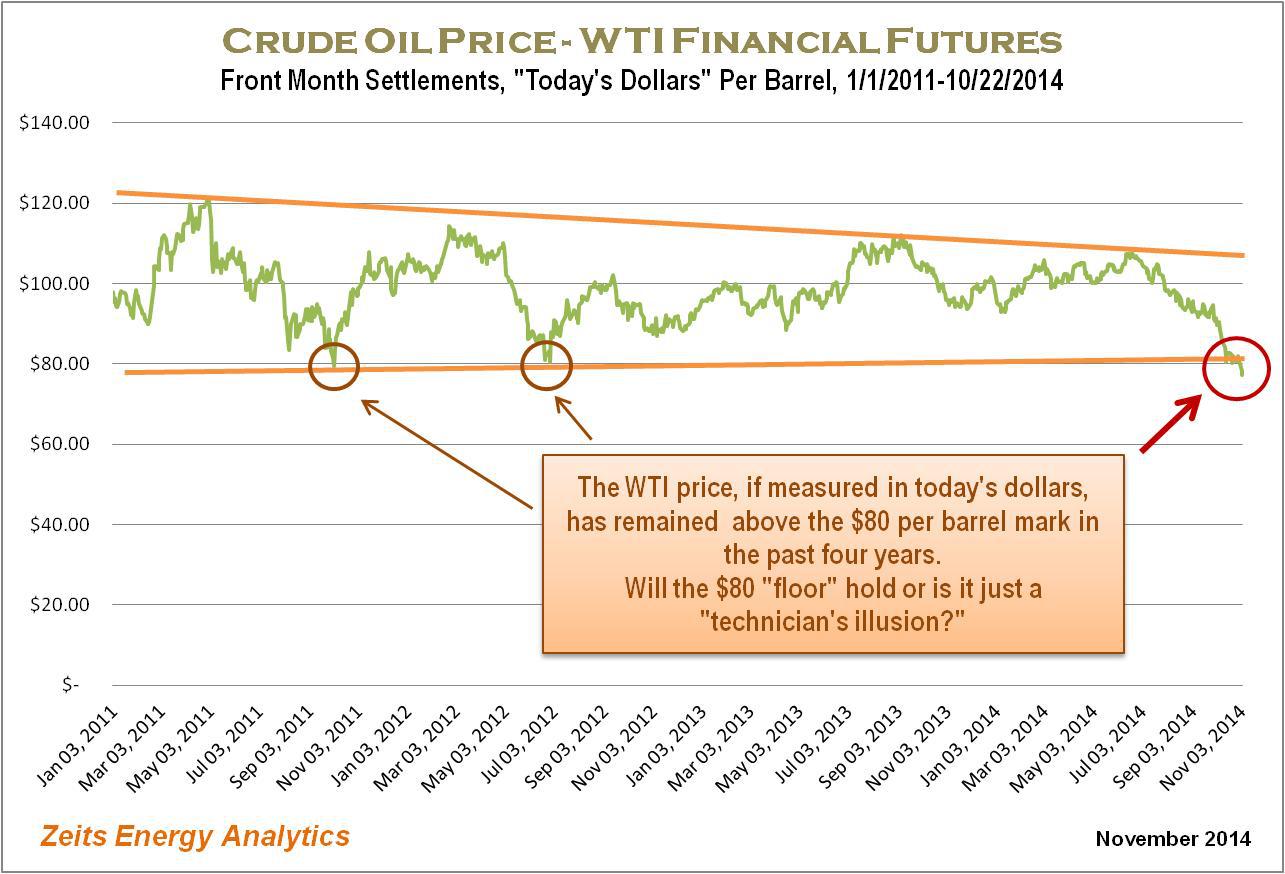

Crude oil prices closed down 4% yesterday, breaking through a 2-month support level at $57/barrel, after an EIA report showed an unexpected build in inventories.

I argue that the domestic supply/demand balance has not improved and is just as bearish now as it was last winter when oil was in free fall.

Based on my analysis of supply/demand data presented in this article, I believe crude oil has further to fall.

My trading strategy, including holdings, price targets, and entry/exit points are discussed in detail.

After trading tightly range-bound between $58/barrel and $61/barrel since mid-April, crude oil finally broke down yesterday, after an EIA Petroleum report showed that crude oil inventories increased more than expected. The commodity slid 4.2% – its largest single-day loss since April 8 – to a 9-week low closing price of $56.92/barrel. The commodity is down 6.6% since recording a peak of $61/barrel one week ago on Tuesday. Further weighing on prices were unclear reports of a draft of an Iranian nuclear deal that would relax sanctions and permit a resumption of exports, as well as continued fears over Greece’s exit from the eurozone. This article will discuss yesterday’s EIA inventory report and use this data to support my argument that crude oil supply and demand remain just as unbalanced presently as when oil was trading at $45 per share, justifying my continued bearish position on the commodity.

In yesterday’s Petroleum Report for the week ending June 26, the EIA announced that crude oil inventories increased by 2.4 million barrels, versus the analyst consensus for a 2-million barrel storage withdrawal. The storage build was also markedly bearish compared to last week’s 4.9 million barrel withdrawal, last year’s 3.2 million barrel withdrawal and the 5-year average 4.1 million barrel withdrawal. It was the first storage injection in 9 weeks since the week ending April 24. Storage injections during the final week of June are highly unusual, and last week’s build was the first storage injection during the last week of June since the week ending June 29, 2007, and only the third this millennium.

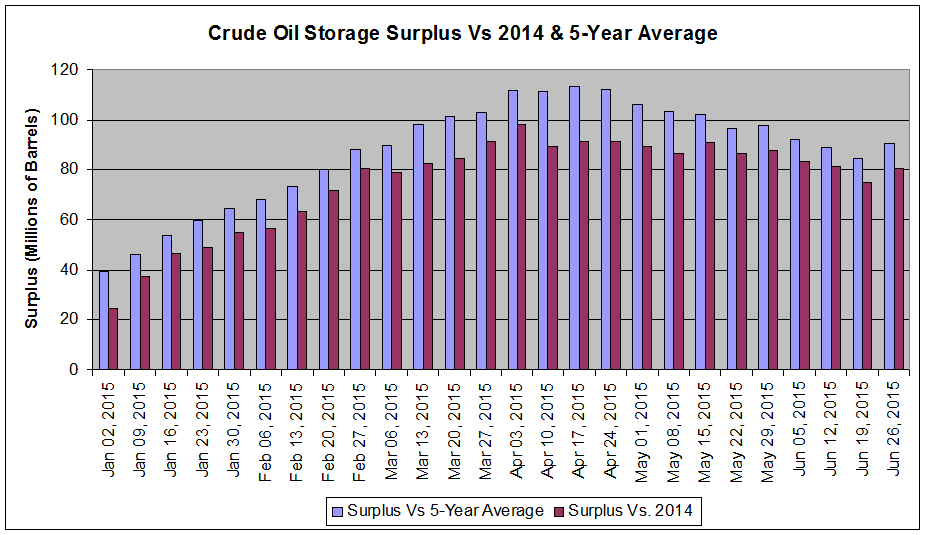

At 480 million barrels, total crude oil storage is 90 million barrels above the five-year average inventory level and 80 million barrels above last year’s level, versus a 84 and 75 million barrel surplus last week, respectively. The increase in crude oil surplus is a sharp departure from the past two months which had seen surpluses, versus the five-year average decline in 8 of the past 9 weeks from a peak of over 113 million barrels. Figure 1 below shows the storage surplus versus the five-year average and 2014 over the past year.

(click to enlarge)

Figure 1: Crude oil storage surplus versus 2014 and the 5-year average showing an increase in the surplus after several weeks of decline. [Source: Chart is my own, data from the EIA.]

What happened over the past week that led to such an abrupt change in crude oil supply/demand balance?

Not much, I argue. And that is the problem.

There are three components of US supply/demand balance – domestic production, demand (measured by refinery inputs), and imports.

Domestic production was largely unchanged last week, declining by 9,000 barrels per day, from 9.604 million barrels per day the previous week to 9.595 million barrels last week. Domestic production remains at record highs, despite an oil rig count that has fallen 60% since October. Production is up 1.2 million barrels year-over-year.

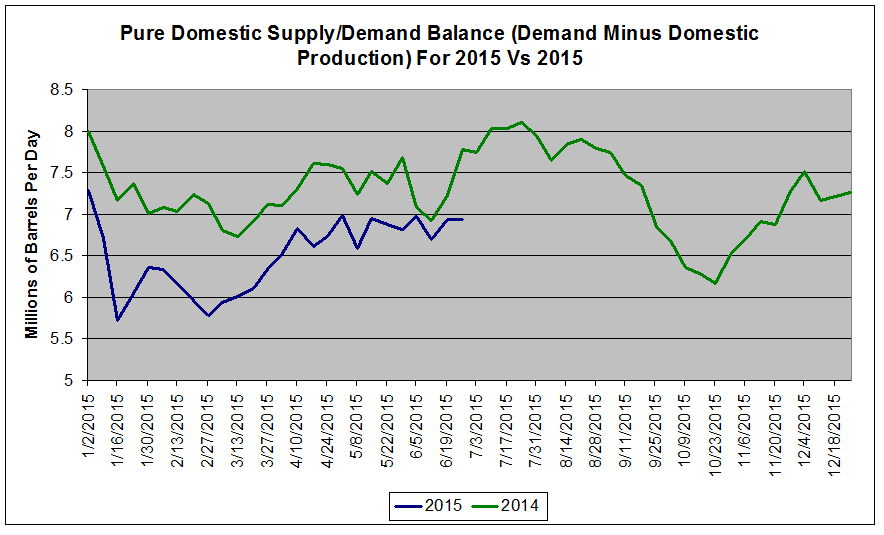

Crude oil demand was likewise flat week-over-week, declining a negligible 1,000 barrels per day last week to 16.531 million barrels per day. Demand is up 313,000 barrels per day year-over-year. Note that this is well shy of the 1.2 million barrel per day year-over-year increase in production. As a result, the purely domestic supply/demand picture – demand minus US production – is markedly loose compared to last year. Figure 2 below compares the purely domestic supply/demand picture for 2015 versus 2014.

(click to enlarge)

Figure 2: Purely domestic crude oil supply/demand balance equal to demand minus domestic production. Supply/demand remains loose to 2014 and has been flat over the past 2 months, indicating minimal tightening of the market. [Source: Chart is my own, data from the EIA.]

Note that last year at this time, demand exceeded domestic production by 7.8 million barrels per day, while last week, this spread was just 6.9 million barrels. Further, despite all of the hullabaloo over record demand and declining domestic production, this spread is sitting near the 2015-to-date average of 6.6 million barrels, and has been essentially flat since late April.

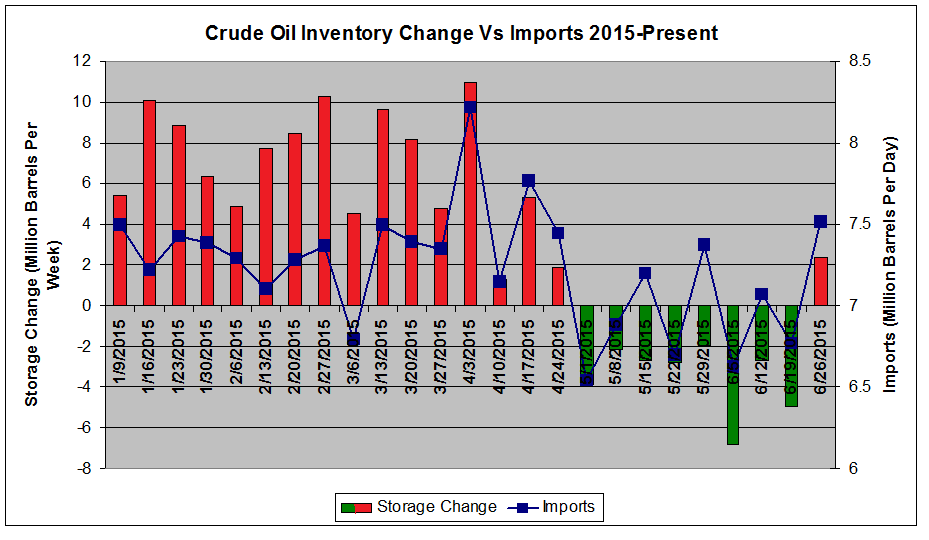

It is the third component of the US supply/demand picture – imports – that drove last week’s bearish storage build and had been masking the persistent supply/demand mismatch shown above in Figure 2 that allowed crude oil to rally more than 30% off the March lows. Imports increased by 748,000 barrels per day last week to 7.513 million barrels per day. It was the largest week-over-week increase since the week ending April 3rd and the largest daily average since the week of April 17th. Nevertheless, the 7.5 million barrel per day tally was a mere 170,000 barrels per day above the 1-year average import level. Figure 3 below plots crude oil imports versus the 1-year average over the last 12 months.

(click to enlarge)

Figure 3: Crude oil imports versus the 1-year average. After 2 months well below the 1-year average, crude oil demand rebounded last week. [Source: Chart is my own, data from the EIA.]

Note that after hovering in the 6.75-7.25 million barrel per day range since late April, last week’s imports were merely a return to the baseline. Furthermore, imports have room to go even higher. Figure 4 below shows the week-over-week change and the departure from 2015-to-date average imports by country.

(click to enlarge)

Figure 4: Crude oil imports by nation with week-over-week and departure versus the 2015 average included. While imports from Canada rebounded last week, large deficits versus the 2015 average remain in Canada, Saudi Arabia, and Mexico. [Source: Chart is my own, data from the EIA.]

Note that the second-largest weekly increase in imports last week came from our biggest oil trading partner, Canada, where imports increased by 142,000 barrels per day. However, thanks to persistent wildfires in Alberta’s prolific oil sands, imports are still 187,000 barrels per day below their 2015 average. As these wildfires have largely diminished, I expect Canadian imports will continue to increase, from 2.8 million barrels per day last week back to their 3.0 million barrel per day 2015 average in coming weeks. An even more impressive departure versus the 2015 average was seen in Saudi Arabia, where imports remained flat at 700,000 barrels per day last week, more than 250,000 barrels below their 2015 average of 992,000 barrels per day. Saudi Arabia is a country whose rig count is at record highs and which is spearheading the effort to destroy the US shale oil industry, so I expect these imports will recover rapidly over the next month. Finally, our third-largest trading partner, Mexico, saw its imports slide 290,000 barrels per day last week, and currently sit 215,000 barrels per day below its 2015 average – likely another short-term anomaly. Were just these three countries to have had their imports at 2015 baseline levels, last week’s storage build would have been a massive 7.1 million barrels. The gains seen in Venezuela, Kuwait, and other smaller trading partners that sent tallies above their 2015 averages may be at least partially attributable to a surge in Gulf Coast imports following delays caused by Tropical Storm Bill, and therefore, may decline in coming weeks. However, I expect the net change in imports to be upwards over the next month, putting further pressure on the supply/demand balance.

My rationale for emphasizing imports compared to US production and demand is that I believe that they have been artificially creating the appearance of a tightening supply/demand balance. Thanks to wildfires in Canada, Tropical Storm Bill interrupting shipments in the Gulf of Mexico, and unrest in the Middle East, imports during April, May, and early June (as shown in Figure 3) were depressed below the five-year average. This correlated strongly with a transition to storage withdrawals that helped to fuel the back-end of crude oil’s 30% rally from the March low of $43/barrel to $61/barrel. Figure 5 below compares crude oil weekly storage injections/withdrawals to imports.

(click to enlarge)

Figure 5: Crude oil storage changes versus imports. There is a strong correlation between storage withdrawals between May and late June and a decline in imports. Storage injections resumed last week, following a surge in imports. This supports imports being the major driver of the domestic supply/demand balance over the past few months. [Source: Chart is my own, data from the EIA.]

During this same period (as shown in Figure 2), domestic production and demand remained relatively unchanged. As a result, I firmly believe that the decline in imports hoodwinked many investors into thinking that the supply/demand balance was permanently tightening, due either to increasing demand from cheap oil or declining production from the declining rig count, when it was really a temporary drop in imports. Now that imports have returned to a baseline level, this “masking” of the supply/demand balance has been lifted, and the result was a bearish injection similar to those seen during oil’s springtime free fall – but during a time when the market expects withdrawals. It is therefore unsurprising that oil retreated to the tune of 4% yesterday.

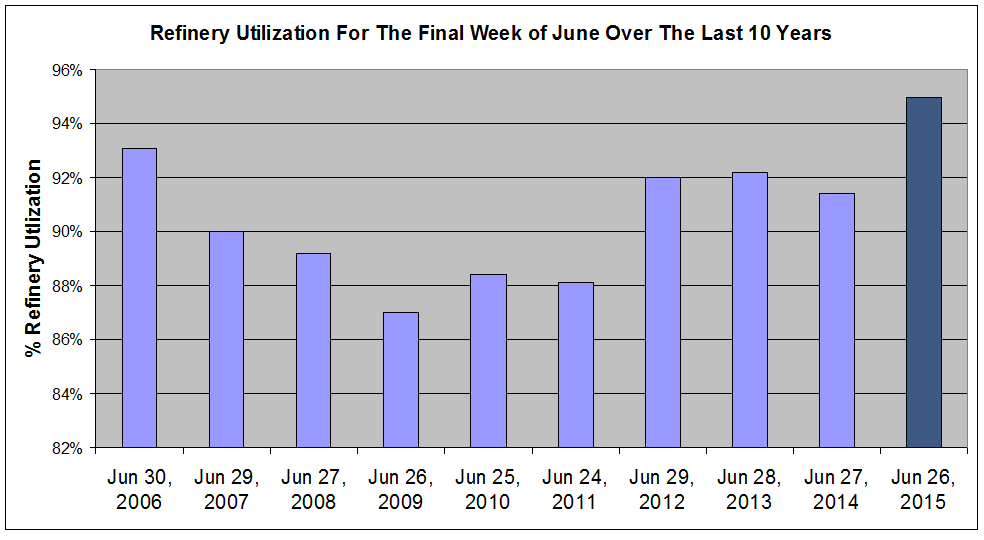

What I believe to be even more concerning is that there is little room to go higher on the demand front. Refinery utilization – the percentage of US refinery capacity that is being utilized to convert crude oil to gasoline and other finished products – was at 95.0% last week. This is the highest refinery utilization during the final week of June over the last 10 years. Figure 6 below shows refinery utilization for the last week of June from 2006 to the present.

(click to enlarge)

Figure 6: Refinery utilization during the final week of June for the past 10 years showing that, at 95%, 2015’s utilization is the highest of the decade. [Source: Chart is my own, data from the EIA.]

Furthermore, the maximum refinery utilization during any week in the last 10 years was 95.4%, recorded several times, most recently last December. As a result, at 95.0% refinery, utilization is nearly at its maximum capacity. The fact that we saw a 2.4 million barrel storage injection, with demand near its maximal level pulling hard at crude oil inventories and with imports still with room to run higher, suggests to me that oil still has room to fall.

Oil’s 4% decline to under $57/barrel represented a major breakdown not only from a fundamental level, as discussed above, but from a technical level. During the 44-day period from April 29 to June 30, crude oil had traded within a tight $4.17 range between $61.43/barrel and $57.26/barrel, the narrowest range since March 2004. Oil broke out of that range yesterday. Figure 7 plots the price of crude oil over the last 3 months, showing the rally, range-bound action, and the breakdown yesterday.

(click to enlarge)

Figure 7: Crude oil prices over the last 2 months showing range-bound trading largely between $58/barrel and $61/barrel. followed by a breakdown yesterday. [Source: Chart is my own, data from the EIA.]

Now that oil has fallen below its 2-month support level, I would not be surprised if more investors head for the exits.

I continue to hold three positions betting on a continued downtrend in crude oil prices. I own a 10% short position in the popular United States Oil ETF (NYSEARCA:USO) – increased from 5% last week – a large 15% short position in the leveraged VelocityShares 3x Long Crude Oil ETN (NYSEARCA:UWTI), and a 5% short position in the Market Vectors Russia ETF (NYSEARCA:RSX). The latter provides short exposure to an oil-driven economy, as well as the turmoil encompassing Europe. The short UWTI position is a higher-risk play on leverage-induced decay due to choppy trading. USO, of course, is a safer direct play on declining oil prices.

Should oil drop to $55/barrel – which has long been my short-term price target – I will begin to aggressively cover my UWTI short position to protect profits in a highly volatile trade, which is currently up 20% and would likely be pushing 35% if oil reaches $55/barrel. I will likewise plan to close out my RSX short around the same level to lock in profits, should the European crisis appear to be resolving.

However, I plan to hold USO for the foreseeable future. Following yesterday’s decline, contango in the oil futures market is again rising, with the 4-month spread up to $1.21, or 2.2%, after bottoming out at $0.86 last week. Should oil continue to fall, the contango will likely widen further, and I could easily see contango-generated returns topping 5% on a position held through the Fall. I feel USO is a safer, less volatile long-term hold than UWTI (despite the fact that UWTI triples the contango-generated gains and also benefits from leverage-induced decay). My price target to close out my USO position is currently $50/barrel. Factors that would likely cause me to cover sooner would include any socioeconomic forces that look like they would suppress imports for an extended period, or if US production (finally) begins declining in a meaningful way. As a result, my “stop” is a fundamental stop, and I do not have a specific stop price. Should oil rally in the face of the current bearish fundamentals, I will even consider adding to my USO short position up to 15%. If I had no crude oil short exposure, I would be reluctant to open a position here with oil down 7% in a week. Rather, I would wait for a bounce before initiating any position.

In conclusion, I believe that US crude oil demand and production remain in a stable, bearish pattern. Instead, the fundamental supply/demand picture is, and has been, dictated by fluctuations in crude oil imports. I do not believe that the underlying fundamental picture has changed since March, and that a return to baseline import levels last week following months of temporary suppression unmasked this persistent supply/demand imbalance. With crude oil demand unlikely to go higher with refineries near peak capacity, domestic production stable, and crude oil imports with room to go even higher, particularly from Canada and Saudi Arabia, I expect continued weakness in crude oil in the months to come. Once the summer driving season fades and demand declines, I would not be surprised to see the domestic oil surplus climb back above 100 million barrels over the next 1-3 months. Further exacerbating bearish sentiment are the possible resumption of Iranian exports and continued anxiety over Greece and the eurozone, although I believe these fears to be secondary to the ongoing domestic storage glut. My 1-3 month price target is $55/barrel, with a potential to drop as low as $50/barrel during this time. As a result, I plan to hold my large basket of crude oil short positions in USO, UWTI, and RSX.

Additional disclosure: As noted in the article, I am also short RSX and UWTI.

“Today is Day 1 of Year 7 of the ‘recovery’, and yet economists everywhere proclaims 3% growth is just around the corner,” rages Jim Bianco as he addresses what ‘bugs him’, exclaiming “that ship has sailed.” Bianco and Santelli go on to slay Keynesian big government dragons and the incessant bullshit from officials like Jack Lew who opine on Greece and other potential systemic risks as being a non-event – “what is priced in is that everything will work itself out at the 11th hour,” leaving a huge asymmetric risk.

California’s massive housing market is slowing down in almost every way imaginable, according to the latest California Real Property Report from PropertyRadar.

California single-family home and condominium sales dropped 3.5% to 36,912 in May from 38,249 in April.

However, the report explained that what is unusual this month is that the decrease in sales was due to a decline in both distressed and non-distressed property sales that fell 8.6% and 2.5%, respectively. The monthly decline in non-distressed sales is the first May decline since 2005.

On a yearly basis, sales were up slightly, gaining 2.3% from 36,096 in May 2014.

“With the exception of a few counties, price increases have slowed considerably,” said Madeline Schnapp, director of economic research for PropertyRadar. “You cannot defy gravity.”

“The environment of rising prices on lower sales volumes was destined not to last. Higher borrowing costs since the beginning of the year and decreased affordability was bound to impact sales sooner or later. We may also be seeing the fourth year in a row where prices jumped early in the year, only to roll-over and head lower later the rest of the year,” Schnapp continued.

Back in March, PropertyRadar’s report showed California was finally ramping up for the spring homebuying season, posting that March single-family home and condominium sales surged to 31,989, a 33.1% jump from 24,031 in February. It was the biggest March increase in three years.

Meanwhile, May’s median price of a California home was nearly unchanged at $396,750 in May, down 1.8% from $404,000 in April.

Within California’s 26 largest counties, most experienced slight increases in median home prices, edging higher in 21 of California’s largest 26 counties.

Year-over-year, the median price of a California home was nearly unchanged, up 0.4% from $395,000 dollars in April 2014.

While at the county level most of California’s 26 largest counties exhibited slower price increases, four counties continued to post double digit gains.

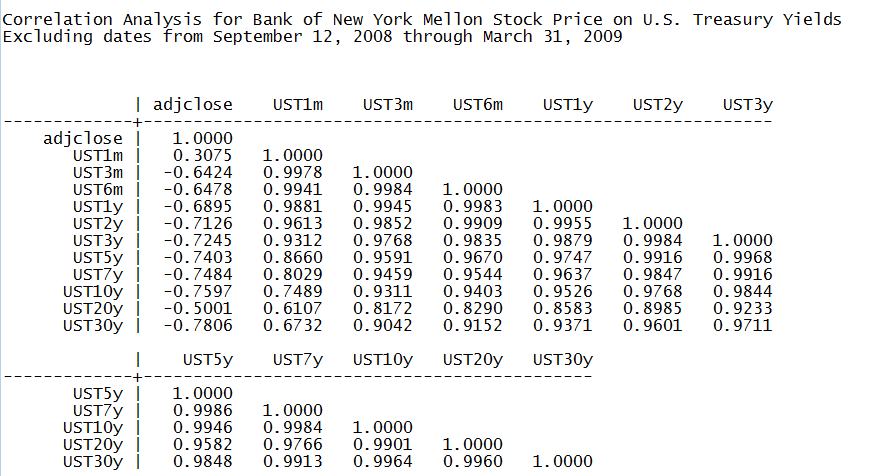

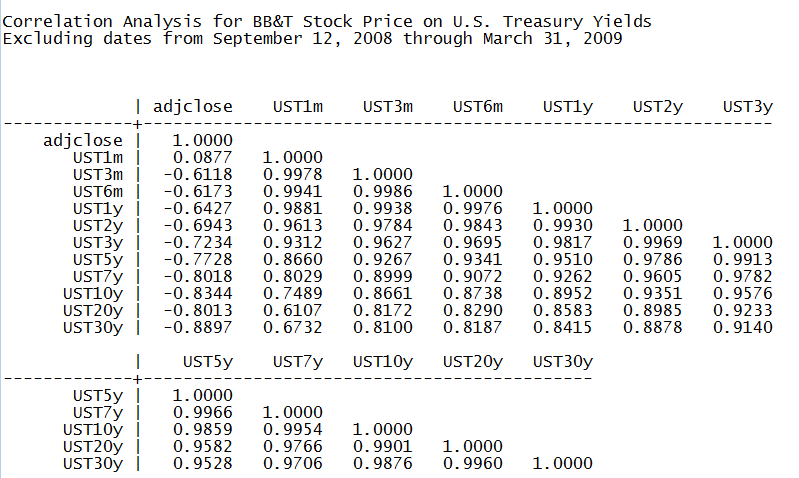

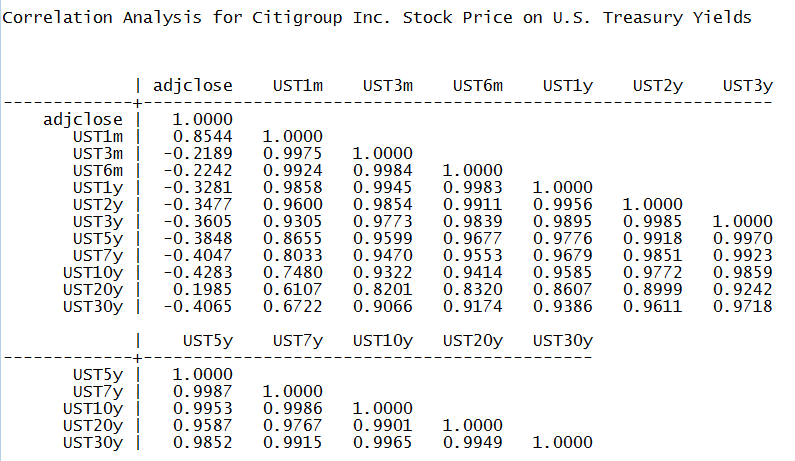

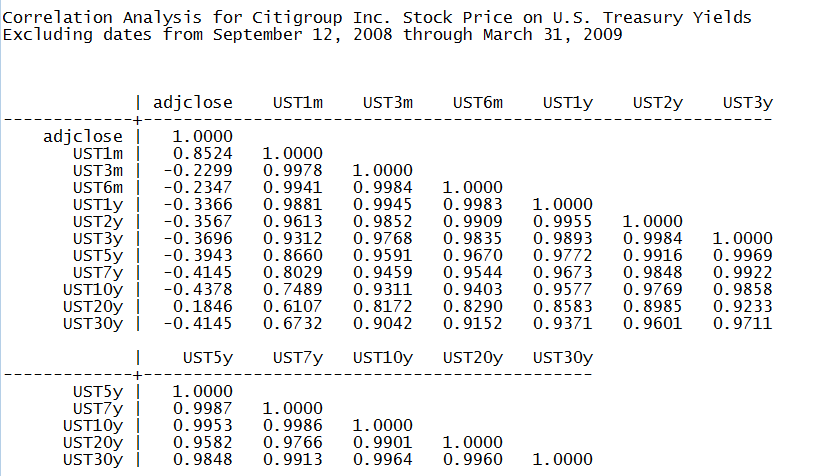

Wm. Mack Terry explained the basics of how rates impact bank stocks at Bank of America in 1974. Net income goes up, margins go up, and stock price goes down.

We value a bank by replication, assembling a series of Treasury securities with the same financial characteristics as a bank. All of Mr. Terry’s conclusions are correct.

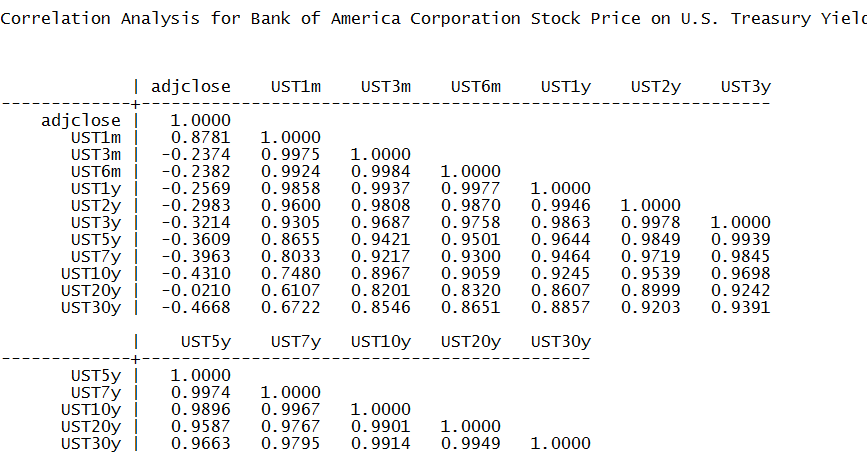

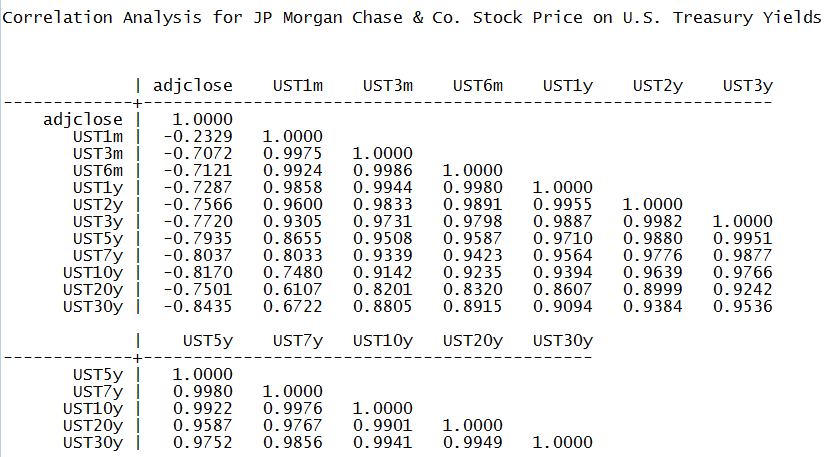

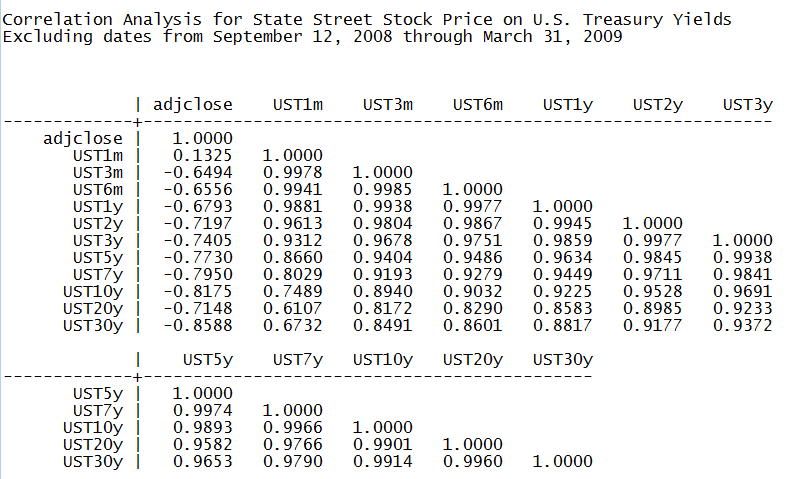

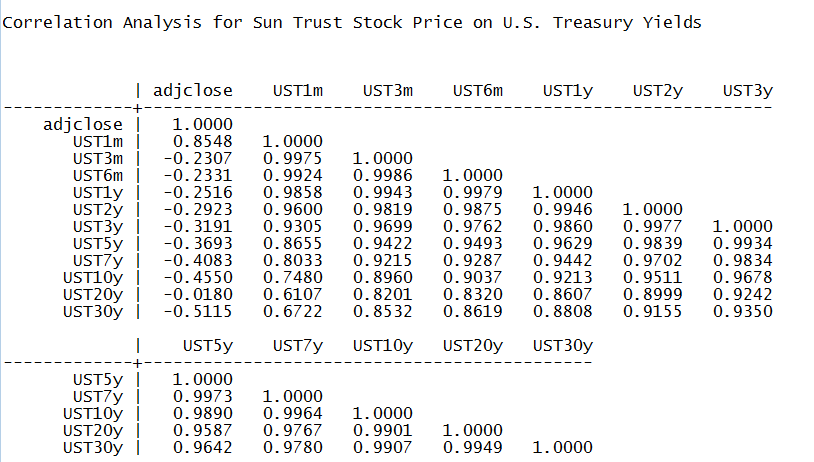

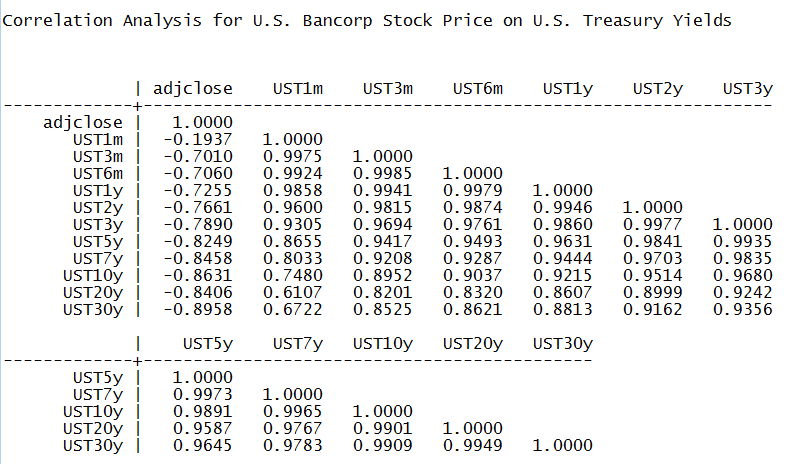

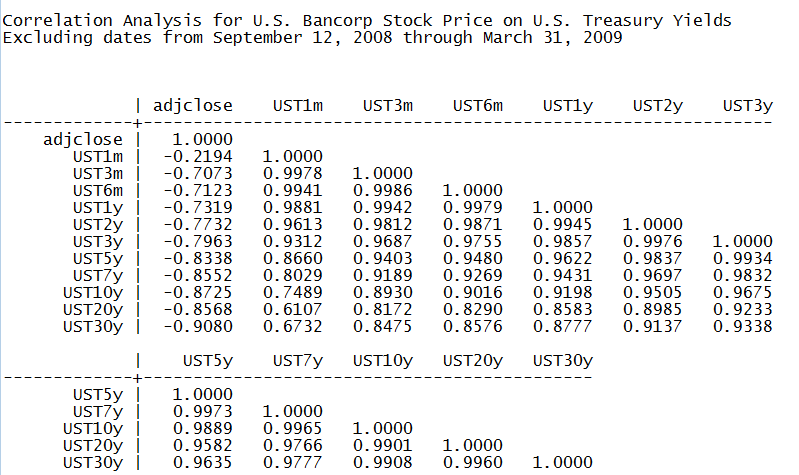

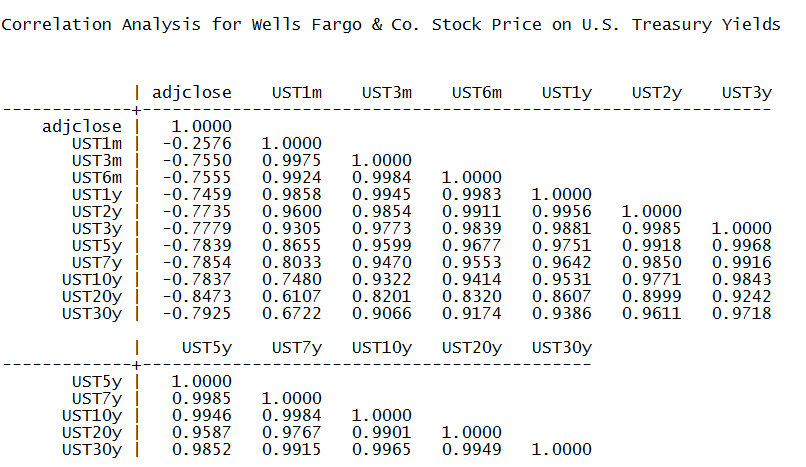

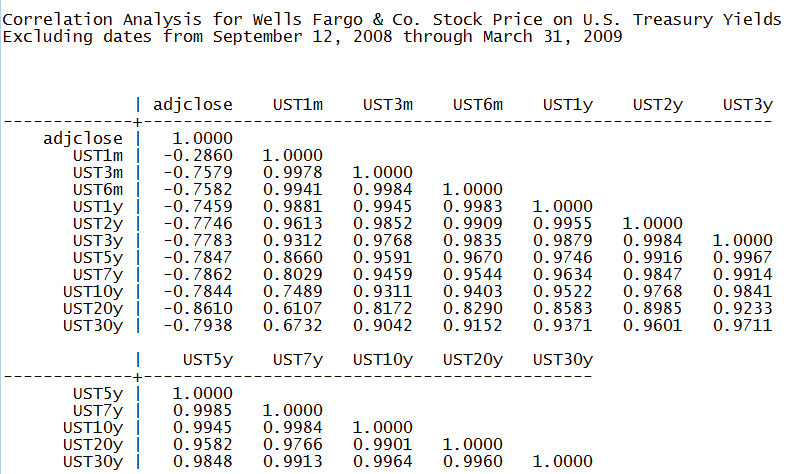

A more technical analysis and references are provided. Correlations with 11 different Treasury yields are added in Appendix A. Finally, a worked example is given in Appendix B.

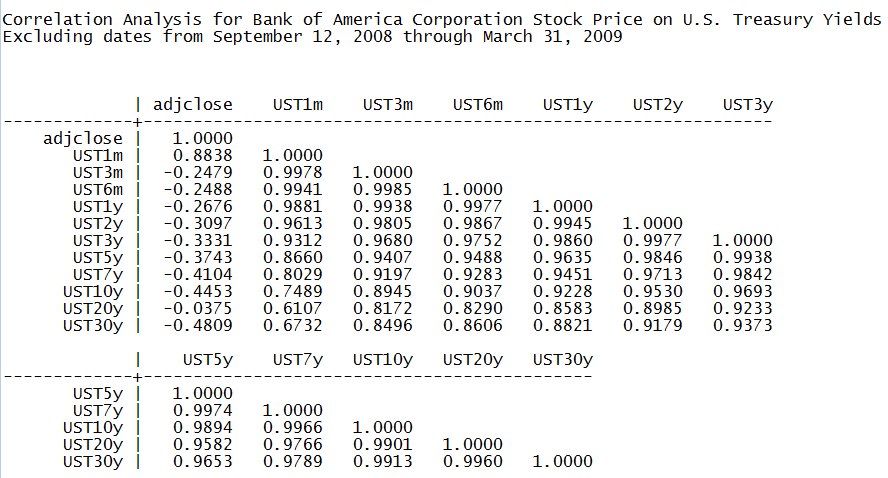

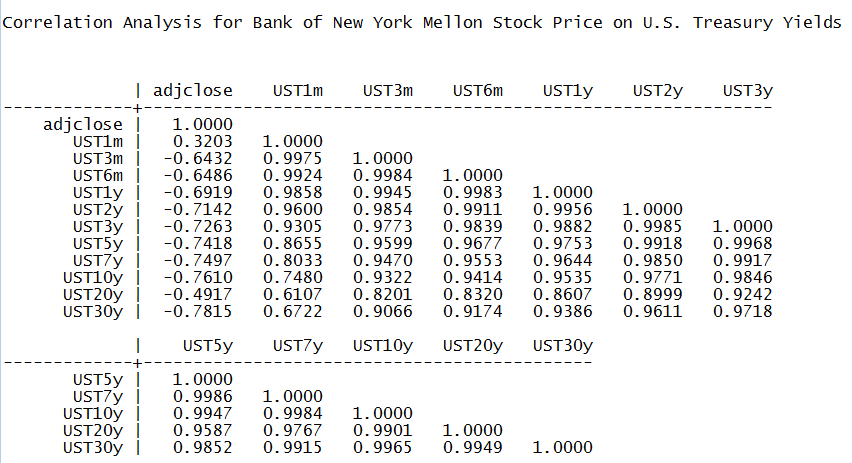

We want to thank our readers for the very strong response to our June 17, 2015, note “Bank Stock Prices and Higher Interest Rates: Lessons from History.” For those readers who asked “is the correlation between Treasury yields and bank stock prices negative at other maturities besides the 10 year maturity?” – we include Appendix A. Appendix A shows that for all nine bank holding companies studied, there is negative correlation between the bank’s stock price and Treasuries for all maturities but two. One exception is the 1-month Treasury bill yield, which is the shortest time series reported by the U.S. Department of the Treasury. The 1-month Treasury bill yield has only been reported since July 31, 2001. The correlation between the longer 3-month Treasury bill yield series and the stock prices of all nine bank holding companies is negative. The other series that occasionally has positive correlations is the 20 year U.S. Treasury yield, which is the second shortest yield series provided by the U.S. Department of the Treasury.

In this note, we use modern “no arbitrage” finance and a story from 1974 to explain why there is and there should be a negative correlation between bank stock prices and interest rates. We finish with recommendations for further reading for readers with a very strong math background.

Wm. Mack Terry and Lessons from the Bank of America, 1974

In the summer of 1974 I began the first of two internships with the Financial Analysis and Planning group at Bank of America (NYSE:BAC) in San Francisco. My boss was Wm. Mack Terry, an eccentric genius from MIT and one of the smartest people ever to work at the Bank of America. One day he came to me and made a prediction. This is roughly what he said:

“Interest rates are going to go up, and two things are going to happen. Our net income and our net interest margins are going to go up, and our senior management is going to claim credit for this. But they’ll be wrong when they do so. Our income will only go up because we don’t pay interest on our capital. Shareholders are smart and recognize this. When they discount our free cash flow at higher interest rates, even with the increase on capital, our stock price is going to go down.”

Put another way, higher rates never increase the value of investments of capital funds, and the hedged interest rate spread is a long term fixed rate security that drops in value when rates rise. That is unless the leading researchers are completely wrong in their finding that credit spreads narrow when rates rise.

Everything Mack predicted came true. The 1-year U.S. Treasury yield was in the 8 percent range in the summer of 1974. It ultimately peaked at 17.31% on September 3, 1981. The short run impact of the rate rise was positive at Bank of America, but the long run impact was devastating. By the mid-1980s, the bank was in such distress that my then employer First Interstate Bancorp launched a hostile tender to buy Bank of America.

Their biggest problem was an interest rate mismatch, funding 30 year fixed rate mortgages with newly deregulated consumer deposits when rates went up.

The point of the story is not the anecdote about Bank of America per se. Why was Mack’s prediction correct? We give the formal academic references below, but we can use modern “no arbitrage” financial logic to understand what happened. We model a bank that’s assumed to have no credit risk by replication, assembling the bank piece by piece from traded securities. This was the approach taken by Black and Scholes in their famous options model, and it’s a common one in modern “no arbitrage” finance. We take a more complex approach in the “Technical Notes” section. For now, let’s make these assumptions to get at the heart of the issue:

We assume the bank has no assets that are at risk of default.

All of its profits come from investing at rates higher than U.S. Treasuries and by taking money from depositors at rates lower than U.S. Treasury yields

We assume that the bank borrows money in such a way that all assets financed with borrowed money have no interest rate risk: the credit spread is locked in. We assume the net interest margin is locked in at a constant dollar amount that works out to $3 per share per quarter.

We assume this constant dollar amount lasts for 30 years.

With the bank’s capital, we assume the bank either buys 3-month Treasury bills or 30-year fixed rate Treasury bonds. We analyze both cases.

We assume taxes are zero and that 100% of the credit spread cash flow is paid out as dividends to keep things simple.

We assume the earnings on capital are retained and grow like the proceeds of a money market fund.

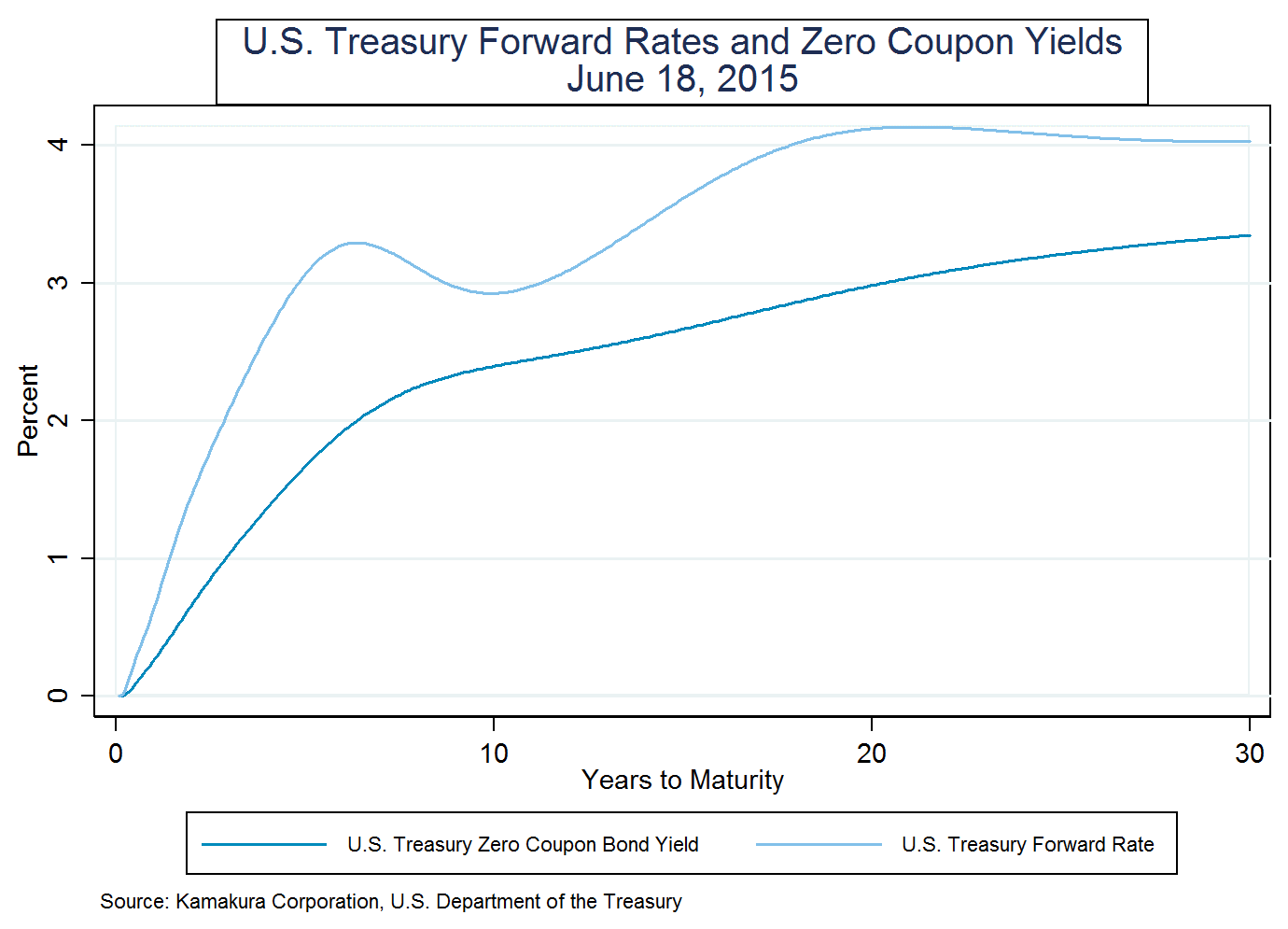

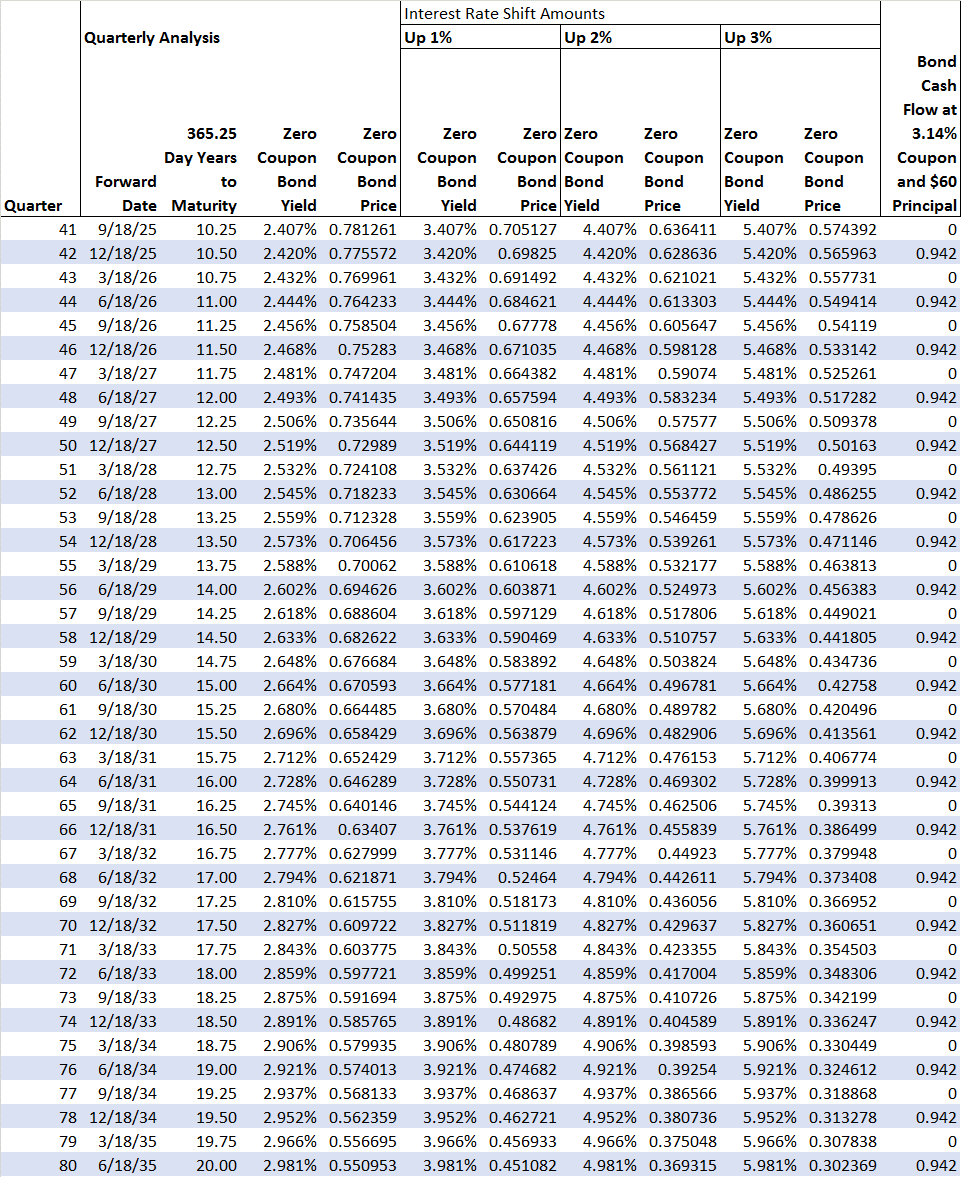

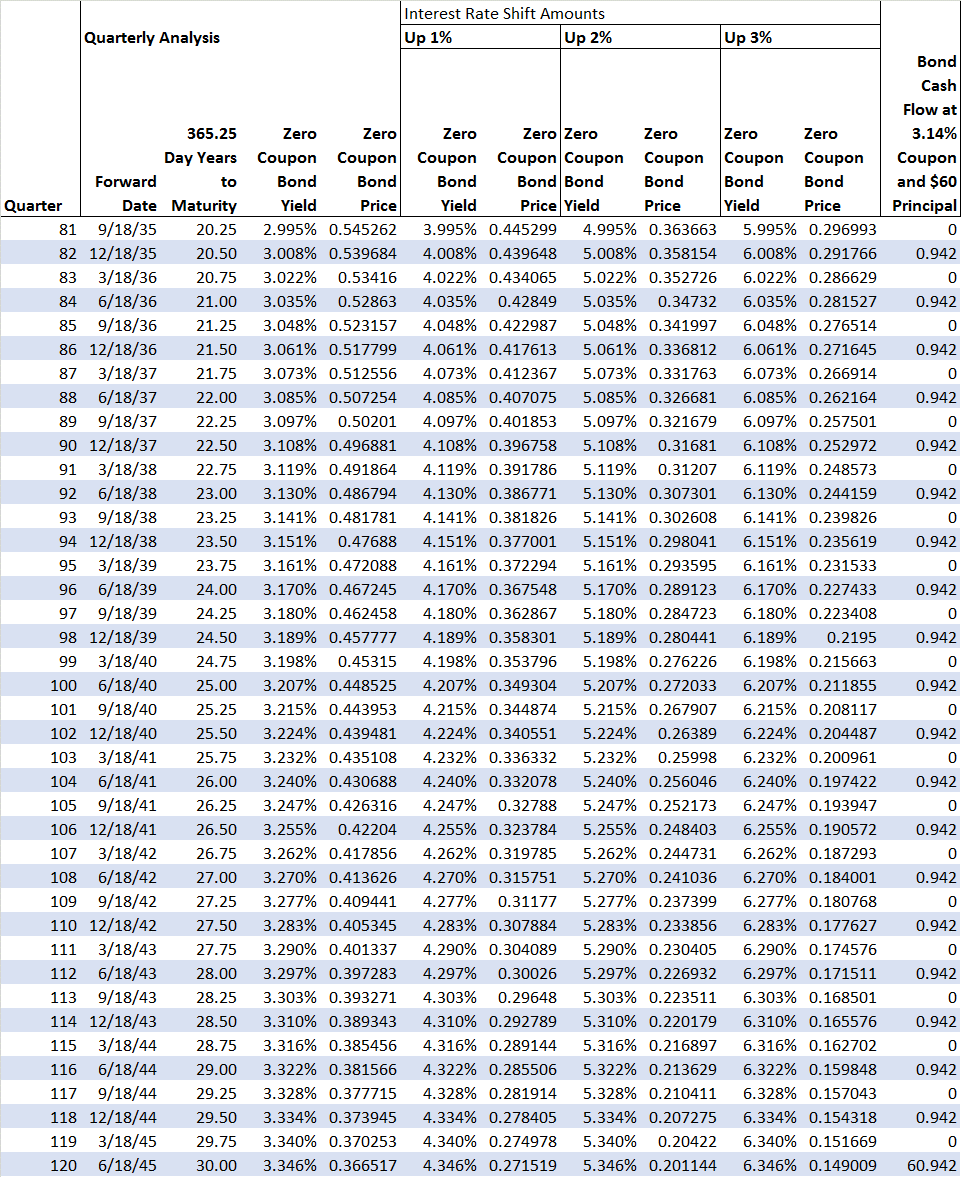

We use the U.S. Treasury curve of June 18 to analyze our simple bank. The present value of a dollar received in 3 months, 6 months, 9 months, etc. out to 30 years can be calculated using U.S. Treasury strips (zero coupon bonds) whose yields are shown here:

(click to enlarge)

We write the present value of a dollar received at time tj as P(tj). The first quarter is when j is 1. The last quarter is when j is 120. The cash flow thrown off to shareholders from the hedged borrowing and lending is the sum of $3 per quarter times the correct discount factors out to 30 years.