CCP Fosun Pharma has been involved in making the Pfizer Vaccine and now will make pills for Pfizer in America as well.

Author Archives: Bone Fish

70% of 10-Year-Olds Cannot Read After Lockdowns

400,000 Chinese Lose Their Life Savings Instantly

Remember that Western leaders under WEF tutelage are in the process of transforming our societies to be run exactly like China.

How a Complete Lock Up of The System Will Occur

(Gregory Mannarino) Why is the world awash in never ending and inflating debt? Moreover, why does global debt keep expanding relentlessly every day, every month, and every year, in what seems like some kind of twisted mass insanity?

What is THE REAL TRUTH behind all this?

Supply Chain Crisis: 70,000 Self-Employed Truckers in California Forced Off The Road Under New Democrat State Law

(Pamela Geller) The Democrats war on hard working Americans just ratcheted up another unimaginable notch. But this time, it not only puts the small businessman out of business, it throws in massive shortages (food, energy, supplies etc.), supply chain issues etc. It’s a catastrophe

Sadly, the U.S. Supreme Court denied a review on whether California Assembly Bill 5 (AB-5) violates the Federal Aviation Administration Authorization Act of 1994 as it applies to self-employed truck drivers.

Will The Fed Reverse Course?

CRYPTO CONTAGION: Three Arrows Capital Defaults After Failing To Make Required Payment On Loan Of 15,250 Bitcoins

(Ethan Huff) Voyager Digital LLC just issued a notice of default to Three Arrows Capital (3AC) after the latter failed to make the required payments on a loan of 15,250 bitcoins (BTC) and $350 million of USD Coin (USDC).

Sharp Decline in Pending Sales, Inventory Surges In California

“Real Estate Tech” in Existential Crisis

“Real Estate Tech” in Existential Crisis as Housing Sours, Stocks Plunge, New Money Out of Reach: Redfin & Compass Try to Survive by Cutting Staff. Opendoor, Zillow Sag

In short, the party ran out of bamboozle.

Game Over, They’re Pulling the Plug – Bill Holter

It’s Hammer Time

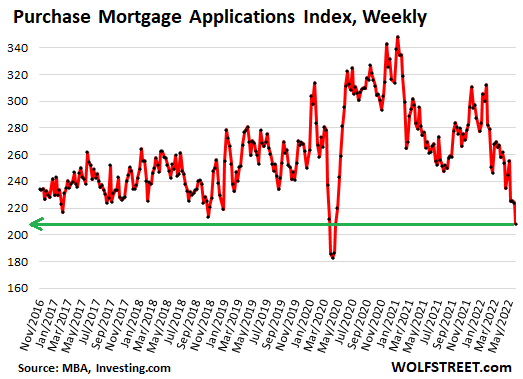

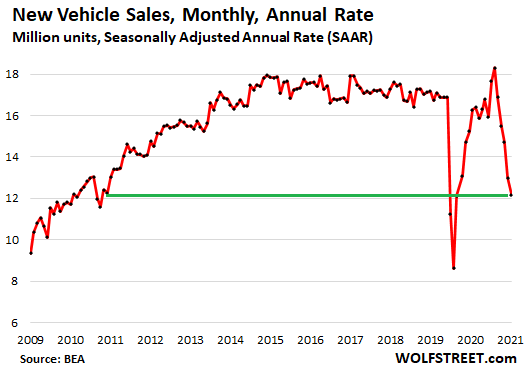

Housing Bubble Getting Ready to Pop: Mortgage Applications to Purchase a Home Drop to Lockdown Lows, “Bad Time to Buy” Hits Record amid Sky-High Prices, Spiking Mortgage Rates

(Wolf Richter) This just keeps getting worse: Applications for mortgages to purchase a home dropped 7% for the week, and were down 21% from a year ago, the Mortgage Bankers Association reported today. An indicator of future home sales: Potential homebuyers try to get pre-approved for a mortgage, lock in a mortgage rate, and then start house-hunting.

Mortgage rates have soared this year, and home prices have soared for years to ridiculous levels, causing layers and layers of potential buyers to abandon the market, amid “worsening affordability challenges,” as the MBA called it. And these applications to purchase a home hit the lowest point since the depth of the lockdown in April 2020 (data via Investing.com):

The MBA’s Purchase Mortgage Applications Index has now dropped below the lows of late 2018. By November 2018, the Fed had been hiking rates for years (slowly), and its QT was in full swing, and mortgage rates had edged above 5%, which was enough to begin shaking up the housing market. Home sales volume slowed, prices began to come down in some markets, and stocks were selling off. But with inflation below the Fed’s target, and with Trump, who’d taken ownership of the Dow, constantly throwing darts at Powell, the Fed signaled in December 2018 that it would cave, and instantly mortgage rates began to fall, and volume and prices took off again.

Today, raging inflation is the #1 economic issue, and the Fed is chasing after it, with backing from the White House, and so this issue in the housing market is just going to have to play out.

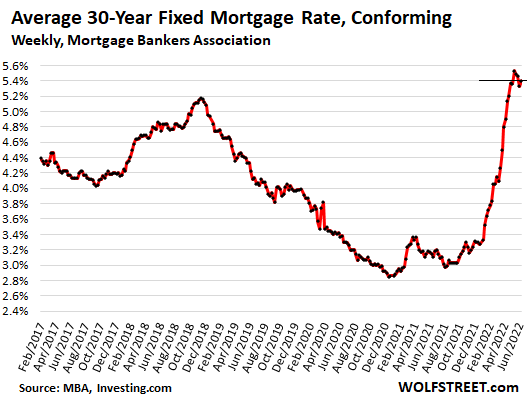

Holy-Moly Mortgage Rates.

The average 30-year fixed mortgage rate with conforming balances and 20% down rose to 5.40% this week, according to the MBA today, having been in this 5.4% range, plus or minus a little, since the end of April, the highest since 2009.

I call them holy-moly mortgage rates because that’s the reaction you get when you apply this rate to figure a mortgage payment for a home at current prices and then accidentally look at the resulting mortgage payment (data via Investing.com):

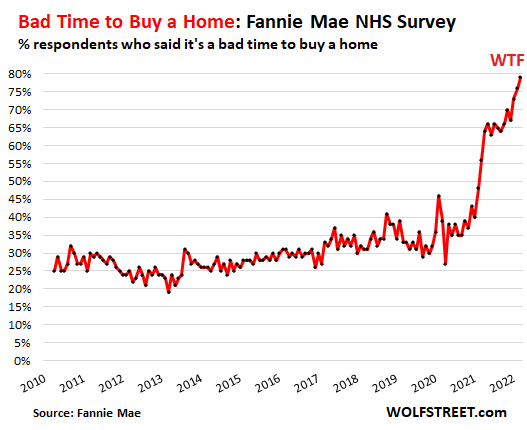

“Bad time to buy a home.”

Turns out, sky-high home prices to be financed with holy-moly mortgage rates, plus uncertainty about the economy, dropping stock prices, and inflation eating everyone’s lunch make a toxic mix for homebuyers.

The percentage of people who said that now is a “bad time to buy” a home jumped to 79%, another record-worst in the data going back to 2010, according to Fannie Mae’s National Housing Survey for May. Sentiment has been deteriorating since February 2021:

“Consumers’ expectations that their personal financial situations will worsen over the next year reached an all-time high in the May survey, and they expressed greater concern about job security,” according to Fannie Mae’s report.

“These results suggest to us that increased mortgage rates, high home prices, and inflation will likely continue to squeeze would-be home buyers – as well as those potential sellers with lower, locked-in mortgage rates – out of the market, supporting our forecast that home sales will slow meaningfully through the rest of this year and into next,” said Fannie Mae.

Sagging stock prices keep getting blamed.

The stock market is on the front pages every day. Only a small percentage of Americans own any significant amount of equities, but that doesn’t matter. Stock market declines, with many high-flying stocks plunging 70% or 80% or even 90% since February 2021, have rattled a lot of nerves. Which is in part why Fannie Mae pointed out, “consumers’ expectations that their personal financial situations will worsen over the next year reached an all-time high.”

The MBA also had previously pointed at the financial markets as one of the reasons for the plunge in purchase mortgage applications.

In the tech and social media sector, the big declines in stock prices have now triggered the first hiring freezes and a few layoffs. And this too – just the idea of nirvana being somehow over – is shaking up some folks.

Sharp increases in stock portfolios, stock options from employers, or cryptos empowered potential homebuyers and enabled many to borrow against their portfolios to come up with down payments. This option has either vanished or is looking very shaky for many.

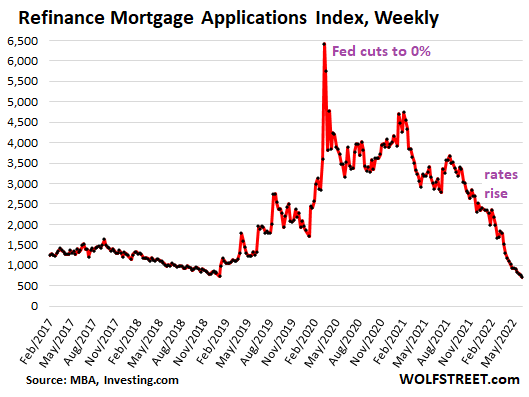

Refi applications collapsed to lowest since year 2000.

Applications for mortgages to refinance an existing mortgage dropped another 6% for the week, and have collapsed by 75% from a year ago, to the lowest level since the year 2000, according to the MBA’s Refinance Mortgage Applications Index. The MBA obtains this data from a weekly survey of mortgage bankers.

With these holy-moly mortgage rates, just about the only reason to refinance is to extract cash from the home via a cash-out refi (data via Investing.com):

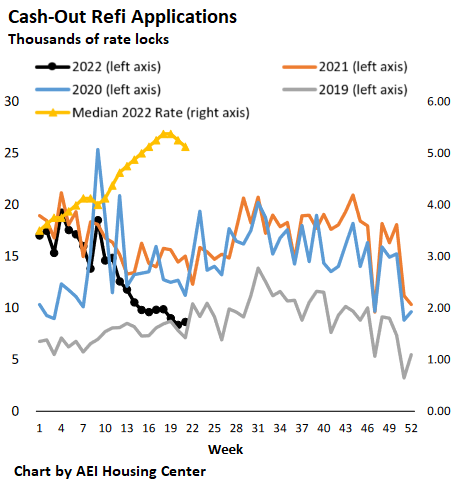

Cash-Out Refi mortgage applications.

According to the AEI Housing Center, which tracks mortgage applications by the number of rate locks, no-cash-out refi applications have collapsed by 92% from a year ago. But cash-out refi applications are primarily driven by the desire to extract cash from a home, with mortgage rates being a secondary issue – and so they continue but a slower pace.

Cash out refi applications in week through May 30 (black line) plunged by 42% from the same week in 2021 and have stabilized roughly level with 2019:

A cash-out refi provides a big lump sum for the homeowner to spend on all kinds of things, from cars to home improvement projects. They are also used to pay off high-cost debts, such as credit cards so that these credit cards can then be used for more purchases. The plunge in cash-out refi reduces the availability of these lump-sums, and therefore reduces the stimulus to the economy they provide.

No-cash-out refi mortgages at lower mortgage rates also boost consumer spending, as the lower rates reduce payments that then leave some extra every month to spend on other stuff. But the spike in mortgage rates, and the subsequent 92% collapse of no-cash-out refi mortgage applications ends this program.

Source: by Wolf Richter | Wolf Street

***

George Gammon: Thinking of buying a house? Stop and watch this first – MS

US housing implosion about to start – Market Sanity

Bank of America declares ‘technical recession’ – NTD

Inflation, consumer woe add to worries that recession is already here – CNBC

“Warning flags are everywhere” – ECB, inflation and U.S. stocks – QTR

Bond market rout so severe double-digit losses are the norm – Yahoo!

Get ready for currency collapses – King World News

Housing Market: Could This Be Worse Than 2008?

“Conditions are changing really fast”

Nick Gerli, in his interview with Wealthion, alludes to a number of figures which spell trouble for the residential market. If you own real estate or we’re considering entering the market soon, it’s worth checking out:

Mortgage Demand Falls To 22 Year Low Amid Rising Rates And Slowing Home Sales

- The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 5.40% from 5.33%.

- Applications for a mortgage to purchase a home fell 7% for the week and were 21% lower than the same week one year ago.

- Refinance demand dropped 6% for the week and was down 75% year over year.

“Major Turning Point” – US Housing Inventory Rises For First Time Since 2019

“Sellers are fueling this turnaround in inventory, with newly listed homes entering the market at a rate not seen since 2019.”

JP Morgan CEO Says A ‘Hurricane’ Is Coming For The U.S. Economy: ‘Brace Yourself’ (VIDEO)

Code Brown: Get out of the pool.

Demand For American Gold Eagles Explodes

Demand for American Gold Eagles exploded in May according to the latest data from the US Mint.

USDA Food Price Forecast Highest Since 1980

(Sundance) Have you ever seen egg prices at $1 per egg range, or $12/doz? Hold on a few months and perhaps you will. That is the context for the scale of food price increases the USDA is now starting to predict. The highest predicted change in food costs in well over 40 years, that’s the USDA warning in their revised May “Food Price Outlook”. [DATA HERE]

Gregory Mannarino Tells Mike Adams How To Protect Yourself From The Eventual Global Debt Implosion

Sometimes the only thing you can do is shine a light.

U.S. Retailers’ Ballooning Inventories Set Stage For Deep Discounts

(Reuters) – Major U.S. retailers that recently scrambled to restock shelves amid product shortages disclosed this week that their stores are now packed with too much merchandise, and some are even doing what was unthinkable just a few months ago: discounting unsold goods.

The Smoking Crack Spread

Biden Admits Sky Rocketing Energy Prices Are Part Of Green “Transition”

Joe Biden let the veil slip Monday, telling reporters gathered at a press conference in Tokyo that unaffordable gas prices in the U.S. are part of a deliberate “transition” to green energy.

Suddenly, Vladimir Putin isn’t to blame anymore as a reporter asked if a U.S. recession is unavoidable.

Are Real Estate Prices About To Crash?

No however, difficult is the way, narrow is the gate and in service to each other we will remain free.

Why $20 Gas Is Coming

‘My God… This Shuts It Down!’: Manchin Confronts Sec. of the Interior Haaland With Statement From Her Dept On Drilling.

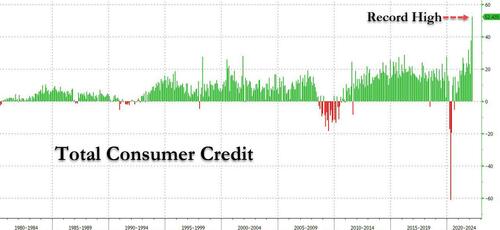

Goldman Economist Warns US Consumers Maxing Out Credit Cards Will Lead To Late 2022 Spending Collapse

A little over a week ago, when looking at the latest consumer credit data from the Federal Reserve, we were shocked to learn that in March, credit card debt soared by a record $52.4 billion, the biggest monthly increase on record and more than double the expected change.

AKA, the American consumer is approaching maximum credit saturation.

Ravaged Consumers Push Back On Biden-Pelosi-McConnell Inflation

Target down 25% TODAY. Walmart down 14% between YESTERDAY and TODAY, represents the single largest drops for these companies since the market crash of 1987.

Working class Americans have never been hammered this hard by government fiscal policy.

“2nd CIVIL WAR… The Republicrats, the globalists are raging an ALL OUT WAR against us… Continue reading

The United States Will Suffer Serious Consequences From China’s Failing Economy

Steve Cortes was on Steve Bannon’s War Room Monday. He discussed growing evidence of China’s failing economy which impacts the US economy greatly. To put it mildly, China’s economy is falling apart.

Goldman Sachs-Backed Funds Buy Up Entire Florida Neighborhood for $45 Million

(Abby Liebing) In the midst of a growing housing and economic crisis, Wall Street investors are using this as an opportunity to purchase rental properties. Two investment funds backed by Goldman Sachs bought a community of Florida homes for $45 million, WFLA reported. The development is Cypress Bay, which is located in Brevard County in Palm Bay, Florida. It is a community of 87 single-family rental homes.

Seller Freaks After Flashy Bel Air Mansion Listed For $87.8 Million Flopped At Auction

(Ray Parisi) An over-the-top modern mansion in Bel Air was listed for $87.8 million for an auction this week. But the highest bid came in just under $45.8 million, according to the home’s seller, dermatologist-turned-developer Alex Khadavi.

“Horrible, Horrible, Horrible!” was how Khadavi characterized the auction results to CNBC. He filed for Chapter 11 bankruptcy protection two weeks after putting the home on the market last year.

Curveballs In The Housing Bubble Bust

All these curveballs will further fragment the housing market.

Bill To Vaxx Minors Without Parental Consent Passes Cali Senate

(Press California) It’s Sen. Scott Wiener’s legislation. More background on SB866 here. We guess SB666 wasn’t available.

The bill removing parental consent for 12-year-olds to get vaccinated just passed the Senate by a single vote. We will stop this obscene legislation in the Assembly.

— Kevin Kiley (@KevinKileyCA) May 12, 2022

Coinbase Earnings Were Bad. Warning That Bankruptcy Could Wipe Out User Funds

(Nicholas Gordon) Hidden away in Coinbase Global’s disappointing first-quarter earnings report—in which the U.S.’s largest cryptocurrency exchange reported a quarterly loss of $430 million and a 19% drop in monthly users—is an update on the risks of using Coinbase’s service that may come as a surprise to its millions of users.

In the event the crypto exchange goes bankrupt, Coinbase says, its users might lose all the cryptocurrency stored in their accounts too.

Is Housing a Bubble That’s About to Crash?

(Charles Hugh Smith) We are all prone to believing the recent past is a reliable guide to the future. But in times of dynamic reversals, the past is an anchor thwarting our progress, not a forecast.

Are we heading into another real estate bubble / crash? Those who say “no” see the housing shortage as real, while those who say “yes” see the demand as a reflection of the Federal Reserve’s artificial goosing of the housing market via its unprecedented purchases of mortgage-backed securities and “easy money” financial conditions.

Trojan Condom Maker Cautions About Potential Recession Risk

Even Trojan Condoms Are Smarter Than The Fed…

(Daniela Sirtori-Cortina) The maker of Arm & Hammer baking soda and Trojan condoms cautioned about a possible recession in its first-quarter earnings report.

UK ‘Sleepwalking’ Towards Food Shortages, Farmers Warn

A tractor cultivates the ground for rapeseed oil crops at the Westons Farm, in Itchingfield (AFP via Getty Images)

Farmers have warned the UK is “sleepwalking into food shortages” because of the rising costs of fuel, fertilizer and feed.

“We’ve got absolutely ridiculous fertilizer prices and we can’t forget that half the food produced in this world comes from artificial fertilizer.” – Farmer from UK

This is not limited to the UK. This is happening everywhere.

Property Taxes EXPLODE. Owners Forced to SELL (especially in TEXAS)

Property Taxes are SURGING across the 2022 US Housing Market. Especially in Texas, where both homeowners and real estate investors could be forced to sell.

Union Pacific Rail Line Begins Restricting U.S. Fertilizer Distribution

(Sundance) This is layers of odd. As many readers are aware, the prices of fertilizer have skyrocketed as supplies have been heavily impacted by increased energy costs and supply chain issues. Many people have worried if a shortage of fertilizer may impact farm yields this year.

China’s Lockdown of Nearly 400 Million Set to Impact Global Economy

People in protective suits prepare to disinfect a residential compound in Huangpu district in Shanghai on April 14, 2022. (China Daily via Reuters)

(Dorothy Li) Factories have suspended production. Truckers are stuck on highways. Containers are piling up at ports. Shipping vessels have been waiting to unload.

China’s economy is set to pay a price as the communist regime’s determination to stamp out the COVID-19 outbreak through harsh lockdowns have brought its manufacturing and commercial hubs, like Shanghai, to a halt.

The Curious Case Of California’s Disappearing Children

“We just aren’t sure where they’ve gone.”

JPMorgan Predicts That Global Commodities Prices May Rise By 40%… Or More

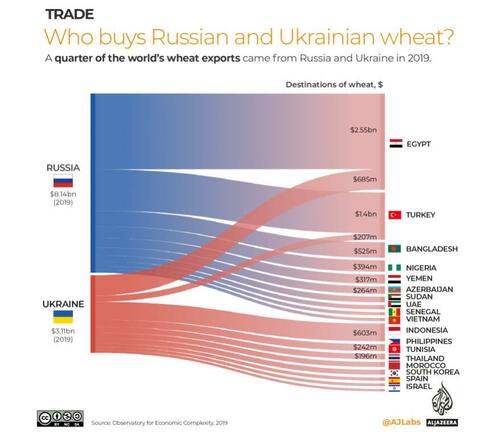

(Bryan Jung) Commodities prices could rise by 40 percent and will likely continue to go higher, according to a note from JPMorgan Chase from April 7, as raw materials hit a record high last month following Western sanctions on Russia due to its invasion of Ukraine.

Russia is a main supplier for up to 10 percent of global energy production and about 20 percent of global wheat production.

The Commodity Currency Revolution Begins

(Alasdiar Macleod) We will look back at current events and realize that they marked the change from a dollar-based global economy underwritten by financial assets to commodity-backed currencies. We face a change from collateral being purely financial in nature to becoming commodity based. It is collateral that underwrites the whole financial system.

Cracks Appear In Housing Market As Sellers Begin To Lower Asking Prices

Over the last several weeks, readers have become aware of an emerging housing affordability crisis as US mortgage rates continued their near-vertical ascent, risks jeopardizing the housing market boom. The 30 Year fixed mortgage rate has jumped a staggering 177bps this year, reaching the highest since 1Q10, with Bankrate data showing mortgage rates are above 5%.

Shocking Consumer Credit Numbers: Credit Card Debt Soars With Savings Long Gone

While it is traditionally viewed as a B-grade indicator, the February consumer credit report from the Federal Reserve was an absolute stunner and confirmed what we have been saying for month: any excess savings accumulated by the US middle class are long gone, and in their place Americans have unleashed a credit-card fueled spending spree.

Here are the shocking numbers: in November, consumer credit exploded by a whopping $41.8 billion, more than double the expected $18.1 billion print, nearly five times more than the upward revised $8.9 billion January number (revised from $6.8 billion), the highest on record!

‘This Raises Serious Questions’ – BLM Paid $5.8 Million For LA Mansion From BLM-Linked Developer Who Paid $3.1 Million For It 6 Days Earlier

Say you’re laundering money, without saying you’re laundering money.

As previously reported, the Black Lives Matter Global Network Foundation spent approximately $6 million on a lavish Southern Californian mansion using donor cash and then took measures to keep the purchase a secret, according to a report Monday.

Washington State Is BANNING Non-Electric Cars by 2030

(Jeff Thompson) As 1984 gains a firmer grasp on the modern world, one recent bill has caused it to spread its reach even further: a bill inserted within Washington state’s $16.9 billion “Move Aside Ahead Washington” package. This new piece of paper, signed by Washington governor Jay Inslee on March 25, now makes it so that police will enforce all vehicles sold, purchased, or registered within the state to be electric vehicles by 2030.

German Retailers To Increase Food Prices By 20-50% On Monday

Just days after Germany reported the highest inflation in generation (with February headline CPI soaring at a 7.6% annual pace and blowing away all expectations), giving locals a distinctly unpleasant deja vu feeling even before the Russian invasion of Ukraine broke what few supply chains remained and sent prices even higher into the stratosphere…

Rate Hikes Jeopardize Much More Than Just American Home Ownership

(J.G. Collins) Someone once said that you never actually “buy” a home. Instead, you merely commit to paying an annuity: the mortgage.

That’s largely true. The price and “value” of homes for the overwhelming majority of homeowners is a function of home buyers’ ability to make payments.

And with the Federal Reserve signaling further interest rate hikes, home buyers and sellers—and assorted others who use credit—will incur knock-on effects from those increases.

Biggest Housing Affordability Shock In History Incoming

30 Year fixed mortgage rates have jumped 160bp this year, reaching the highest since November 2018, with the latest Freddie Mac data showing an acceleration in mortgage rates which jumped a quarter point in just the past week, from 4.42% to 4.67%. This is an even bigger increase than we discussed in our recent housing comment.

And while the benchmark 10y Treasury yield has also risen, the increase is “only” 94bp. In other words, there has also been a significant widening in mortgage spreads, by 66bp to 243bp. This could be explained by the Fed’s accelerated pivot from QE to QT, the latter of which we expect will be announced at the next FOMC meeting in May.

As discussed one week ago in “Housing Affordability Is About To Crash The Most On Record“, the move higher in rates means that an already record affordability shock will be even worse! Continue reading

JPMorgan Admits Central Banks Need A Recession “To Cure Inflation”

Over the past few months we have repeated a statement which – because it is controversial and because it is true – sparked feigned outrage among the financially illiterate macrotourists (which these days is the vast majority of the financial commentariat): we said that in light of the galloping inflation which has crushed BIden’s approval ratings and has ensured a landslide loss for Democrats in the midterms, the Fed desperately wants to create a recession (and, at this rate, it will get it).

Fed wants recession. It will get it in a few months.

— zerohedge (@zerohedge) March 16, 2022

Today, our tinfoil conspiratorial theories once again were validated today when none other than JPMorgan’s European economists admitted that…

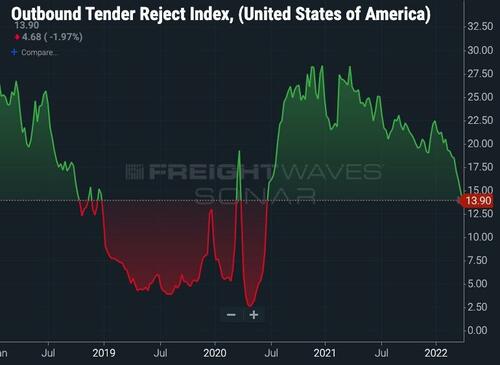

Trucker Stocks Plunge After First Post-COVID Job-Losses As Freight Recession Looms

Tender rejections are the best indicator into real-time supply/demand in the truckload sector.

Just wait for April…

https://www.zerohedge.com/markets/why-freight-recession-imminent

***

Yield Curve Inverts Dramatically As Goldman Sees Recession Risks Soaring

..2s30s just inverted for the first time since 2007…

Russia, In The Interim Agrees to Accept Euros for Energy Payment, Which Will be Transacted into Rubles by Gazprombank

(Sundance) Russian President Vladimir Putin and German Chancellor Olaf Scholz will hold further discussions on the purchase of Russian energy products in rubles according to TASS (Russian News) and western media. However, in the interim Russia will continue accepting payment in euros which will be exchanged for Rubles by Gazprom bank.

Which Major Currency Will Be The First To Fall?

…Could the euro beat the Yen in the race to the graveyard?

(Bruce Wilds) Before saying anything else, it is important to note, when it comes to the major currencies, it is safe to assume they are manipulated by central banks. It is in the best interest of Central Bankers to keep them trading in a rather tight pattern as so not to rock the foundation of the global financial system. On top of the stress being placed upon economies due to the war in Ukraine, the one thing bankers don’t want to deal with is the growing fear the fiat monetary system is about to fail.

Biden Regime Crushes Home Ownership For Young Americans

The policies of Joe Biden exclude an entire wave of young citizens from a critical component of the American Dream.

As America descends into oligarchy, conglomerates and their affiliated political stooges manipulate markets and public policy to centralize power and disenfranchise the historic drivers of social cohesion in America, especially vibrant churches, prosperous small businesses, and thriving families. Regarding families, a pillar of family formation and lasting generational strength in America long revolved around private property, the creation and sustenance of ownership over single-family housing.

Blackstone Gives Up On One Of Its Midtown Manhattan Office Buildings, Hands Keys To Lender

Blackstone is giving up on one of its Midtown Manhattan office buildings, the latest sign yet that distress is beginning to hit the office sector.

The world’s largest owner of commercial real estate, Blackstone has turned over the keys of 1740 Broadway, a 26-story office tower a block from Carnegie Hall, to the special servicer on its $308M commercial mortgage-backed security, Commercial Observer reports.

Kremlin Threatens To Halt Supplies As G7 Ministers Reject “Unacceptable” Demand To Pay For Gas In Rubles

https://www.zerohedge.com/markets/here-are-all-latest-news-and-developments-ukraine-war-march-28

“You must pay in Rubles now.”

“That wasn’t the deal!”

“I have altered the deal. Pray I do not alter it any further.”

President Putin Says ‘Unfriendly Countries’ Must Switch To Its Currency By March 31

Putin Declares May 9th As End Of War In Ukraine

…Same Date Russia Defeated Nazis In WW2

Welcome to the Death Zone

Do you own a house? Do you rent?

It All Comes Together: Hunter, Burisma, Kolomoisky, Zelensky and the “Children Burned Alive in Donetsk”

Is the US being drawn into WW 3 over the corruption of the Biden crime family? Burisma Holdings is owned by oligarch Ihor Kolomoisky, who backed the campaign of President Volodymyr Zelensky and funded the neo-Nazi Azov Battalion, writes blogger Kanekoa the Great. The profound corruption of Hunter Biden and The Big Guy in Ukraine may also explain Hunter’s mysterious reference to “children burned alive in Donetsk.”

BlackRock’s Fink Says Ukraine Invasion “Accelerates” Shift To ESG and Digital Currencies

BlackRock CEO Larry Fink’s annual letter to shareholders has become heavily scrutinized as ones from Berkshire Hathaway chief Warren Buffett and JP Morgan chief Jamie Dimon. Fink is the boss of a $10 trillion asset manager, the world’s largest and oversees more money than the Fed, told shareholders Russia’s invasion of Ukraine would fundamentally reshape the world economy and drive up inflation as supply chains are reconfigured.

Yikes!

Millions to Develop AIDS from Vax by Fall – Dr. Elizabeth Eads

Dr. Elizabeth Eads is on the front line of medicine, treating patients who have been injected with the experimental CV19 so-called “vaccines.” Dr. Eads is now seeing first-hand Acquired Immunodeficiency Syndrome, commonly referred to as AIDS. Let that sink in. Dr. Eads explains, “Yes, we are seeing vaccine related acquired immunodeficiency in the hospital now from the triple vaxed. . . . It is a vax injury, and we are not really certain how to treat this. We are throwing the kitchen sink at it.”

Afghanistan’s Last Finance Minister, Now a DC Uber Driver, Ponders What Went Wrong

(Greg Jaffe) WOODBRIDGE, Va. — Until last summer, Khalid Payenda was Afghanistan’s finance minister, overseeing a $6 billion budget — the lifeblood of a government fighting for its survival in a war that had long been at the center of U.S. foreign policy.

Now, seven months after Kabul had fallen to the Taliban, he was at the wheel of his Honda Accord, headed north on I-95 from his home in Woodbridge, Va., toward Washington, D.C. Payenda swiped at his phone and opened the Uber app, which offered his “quest” for the weekend. For now his success was measured in hundreds of dollars rather than billions.

Inflation Stings Most If You Earn Less Than $300K. Here’s How to Deal.

Petrodollar Cracks: Saudi Arabia Considers Accepting Yuan For Chinese Oil Sales

One of the core staples of the past 40 years, and an anchor propping up the dollar’s reserve status, was a global financial system based on the petrodollar – this was a world in which oil producers would sell their product to the US (and the rest of the world) for dollars, which they would then recycle the proceeds in dollar-denominated assets and while investing in dollar-denominated markets, explicitly prop up the USD as the world reserve currency, and in the process backstop the standing of the US as the world’s undisputed financial superpower.

Those days are coming to an end.

This Is Big: Naomi Wolf Confirms Big Pharma Was Adding Varying Amounts of Active Ingredient to Batches of COVID Vaccine (VIDEO)

(Jim Hoft) Former Clinton adviser and COVID Vaccine critic Naomi Wolf joined Steve Bannon on The War Room on Monday morning. Naomi shared her latest bombshell from her investigation into the Pfizer vaccine documents released by the US government on their COVID vaccine testing. Naomi’s team of investigators, doctors and attorneys identified several US government documents that confirm that Pfizer was adding varying amounts of active ingredient to their experimental COVID vaccines. According to the data, the range of dangerous active ingredient went from 3μg, to 10μg, to 30μg, to 100μg depending on the batch they happened to inject you with.

U.S. Commodity Crisis Giving Rise to New World Order, Says Credit Suisse’s Zoltan Pozsar

Credit Suisse short-term rate strategist Zoltan Pozsar also said the new order would weaken the US dollar and create higher inflation in the western world.

(Jocelyn Fernandez) Credit Suisse short-term rate strategist Zoltan Pozsar, a former United States Federal Reserve and US Treasury Department official, in a report said the US is in a commodity crisis and this will give rise to a new world order that will weaken the US dollar and create higher inflation in the western world.

Phoenix’s Tent City Expands To Nearly 1,000 As Housing Affordability Crisis Worsens

A massive homeless encampment in downtown Phoenix, Arizona, known as the “Zone,” raises eyebrows as the shelter’s population swells to more than 900 people.

The Zone is located on 9th Avenue, Jackson Street, 13th Avenue, and Jefferson Street in Phoenix, down the street from the Arizona State Capitol complex.

SARS-COV-2 Vaccines and Neurodegenerative Disease

(Stephanie Seneff and GreenMedInfo) Since December 2020, when several novel unprecedented vaccines against SARS-CoV-2 began to be approved for emergency use, there has been a worldwide effort to get these vaccines into the arms of as many people as possible as fast as possible. These vaccines have been developed “at warp speed,” given the urgency of the situation with the COVID-19 pandemic. Most governments have embraced the notion that these vaccines are the only path towards resolution of this pandemic, which is crippling the economies of many countries.

U.S. Historic Ban on Russian Oil Creates Ripples in The Global Economy

(Autumn Spreademann) Attempting to further sequester Russia’s economy U.S. President Joe Biden announced on March 8 the ban of all Russian oil imports as part of a multi-faceted response to the eastern nation’s military invasion of Ukraine.

While strict sanctions on Russian exports remain a cornerstone of Western efforts to stop President Vladimir Putin’s attack, it comes with a hefty price tag already felt by global consumers.

Crisis Actors Pretending to be Dead Ukrainians Can’t Keep Still and Fox News Talking Heads Can’t Stop Lying

(Paul Craig Roberts) As you can see from the short video, anti-Russian psyops is in full operation: video/fVxGiHParDAC/ It tells us nothing about Russia, but much about ourselves. Western presstitutes have no morality, no integrity, and will lie for money even when the lies lead to nuclear war.

https://www.bitchute.com/video/fVxGiHParDAC/

This video above is not Ukraine, it was a climate change protest in Vienna on 4 February, 2022, weeks before Russia invaded Ukraine. Convenient that the guy talking has a mask so you can’t read his lips. Watch the original: https://www.youtube.com/watch?v=2o3Rph8DcUY

Unintended Consequences of mRNA Vaccines Against COVID-19 Are Undeniable

(Joseph Mercola) MIT scientist Stephanie Seneff’s paper, “Worse Than the Disease: Reviewing Some Possible Unintended Consequences of mRNA Vaccines Against COVID-19,” published in the International Journal of Vaccine Theory, Practice and Research in collaboration with Dr. Greg Nigh, is still one of the best, most comprehensive descriptions of the many possible unintended consequences of the mRNA gene transfer technologies incorrectly referred to as “COVID vaccines.”

Russia “Recommends” Fertilizer Makers To Halt All Exports

This morning ZeroHedge listed some of the countries that are dangerously (and almost exclusively) reliant on Russia and Ukraine for their wheat imports, highlighting Turkey, Egypt, Tunisia and others…

… which are facing an “Arab Spring” style food crisis (and potential uprising) in the coming weeks unless the Ukraine conflict is resolved.

ISM Services Index Decreased to 56.5% From 59.9 In February

The ISM® Services index was at 56.5%, down from 59.9% last month. The employment index decreased to 48.5%, from 52.3%. Note: Above 50 indicates expansion, below 50 in contraction.

Bernie Madoff’s Sister And Husband Found Dead In Apparent Murder Suicide

Palm Beach County Sheriff’s Office announced that they would inquire into the deaths of Sondra Wiener, 87, and Marvin Wiener, 90

2/20/22 Bernie Madoff’s sister and her husband died from gunshot wounds at their home, authorities said today. They added that the case was being investigated as a murder-suicide.

More Vaccinated Than Unvaccinated Proportionately Caught Covid Last Week According to LA County Health Department Data

(Santa Monica Observer) February 24, 2022 – Data from the Los Angeles County Department of Public Health show that last week the vaccinated were 6.3% more likely to catch Covid-19 than the unvaccinated. This is at least the second week in which numbers dipped the wrong direction for proponents of the idea that it is the unvaccinated who are the main transmitters of the virus.

Here are the raw numbers:

China’s Property Bubble Collapse Gets Worse

An aerial view shows the 39 buildings developed by China Evergrande Group that authorities have issued a demolition order on in Hainan Province, China, on Jan. 6, 2022. (Aly Song/Reuters)

Kim Iversen: GREAT RESET Has INFILTRATED Cabinets Around The World With Young Leaders Like Trudeau

The Hill’s Kim Iversen details the prestigious class of the World Economic Forum’s Young Global Leaders (tyrants) program and speculates how their group think may have led to Covid-19 lock downs.

Blackrock Whistleblower Who Predicted The Crash of Moderna Breaks Bombshell Information

Edward Dowd of @DowdEdward joins The Alex Jones Show to break down evidence of fraudulent clinical data along with the plunge in Big Pharma stocks. Dowd also delivers groundbreaking analysis on how globalists operate.

“This Pandemic Won’t Have a Defined End” – Newsom Proclaims California’s Permanent ‘Endemic’ Virus Policy (VIDEO)

(Cristina Laila) Governor Gavin Newsom on Thursday unveiled California’s “endemic” virus policy – and it’s going to cost billions and billions, and billions of dollars in pork spending.

U.S. Accuses Zero Hedge Of Spreading Russian Propaganda

(Nomann Merchant) U.S. intelligence officials on Tuesday accused a conservative financial news website with a significant American readership of amplifying Kremlin propaganda and alleged five media outlets targeting Ukrainians have taken direction from Russian spies.

The officials said Zero Hedge, which has 1.2 million Twitter followers, published articles created by Moscow-controlled media that were then shared by outlets and people unaware of their nexus to Russian intelligence. The officials did not say whether they thought Zero Hedge knew of any links to spy agencies and did not allege direct links between the website and Russia.

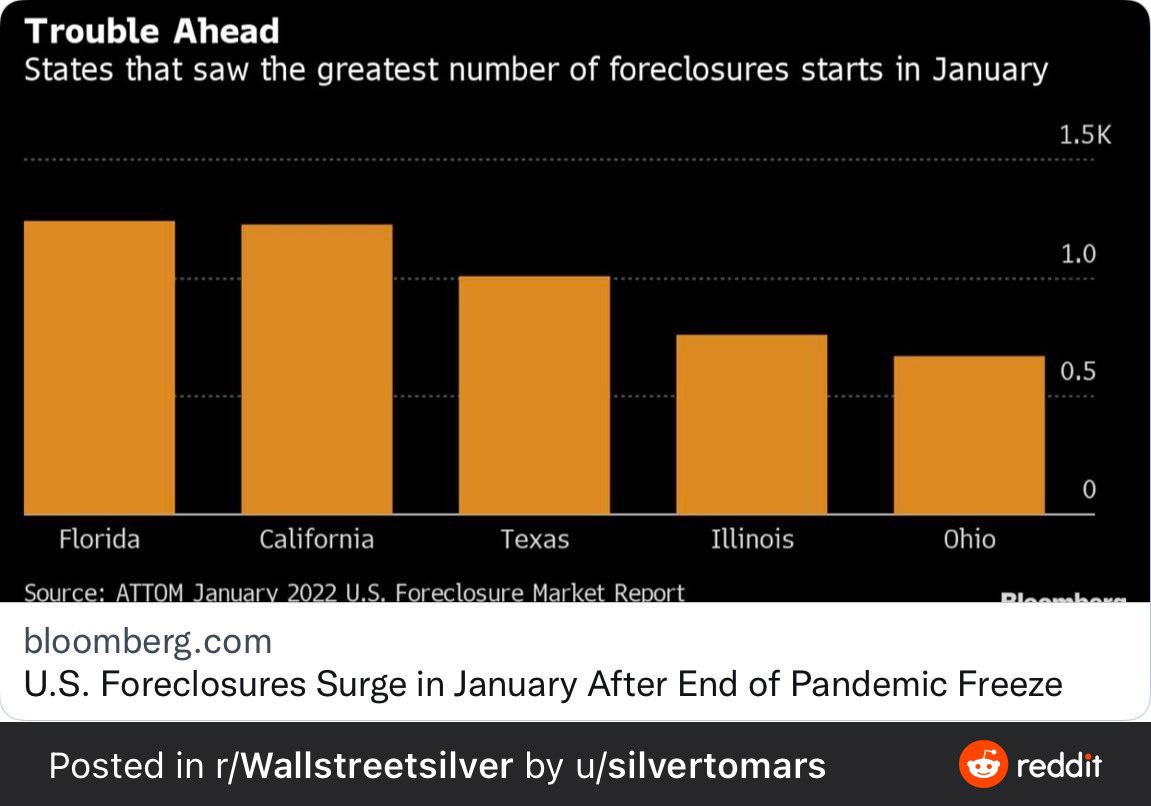

U.S. Foreclosures Surge in January After End of Pandemic Freeze

(Alexandre Tanzi) Foreclosures on homes in the U.S. surged in January after a pandemic moratorium ended, though they remained well below pre-Covid levels, according to new data from RealtyTrac.

Fed Blocks Release Of Documents On Pandemic Insider Trading By Policymakers

(Howard Schneider) – The U.S. Federal Reserve, responding to a Freedom of Information Act request by Reuters, said there are about 60 pages of correspondence between its ethics officials and policymakers regarding financial transactions conducted during the pandemic year 2020.

But it “denied in full” to release the documents, citing exemptions under the information act that it said applied in this case.

Why 42 States Have Removed Taxes From The Purchase of Gold and Silver

(Jp Cortez) Last year was a good year for state-level sound money legislation across the United States. 2022 could be even better.

Long Funeral Homes, Short Life Insurers? Ex-Blackrock Fund Manager Discovers Disturbing Trends In Mortality

Four weeks ago, OneAmerica insurance company CEO Scott Davison revealed that they had witnessed ‘the highest death rates in the history of this business – not just at OneAmerica’ with a jump of ‘40% over what they were pre-pandemic.‘ Interestingly, Davison noted that the majority of deaths are not classified as due to Covid-19. Continue reading

Scottsdale School Board – “You’ve Been Served”

Leigh Dundas and Miki Klann speak to the Scottsdale Unified School District in Arizona. During the meeting, Miki declares her intention to file a claim against the Governor’s surety bond on behalf of the SUSD board members. Each member of the board will be charged with practicing medicine without a license, child abuse, segregation and inappropriate sexual material in the school libraries.

Watch

Miki served each board member with 10 letters of intent by 10 different parents. Each claim carriesa liability of up to 100K – this means each board $carries a total liability of $1 million in the event that the claims are filed. Now the board members have 5 days to rectify the situation or the parents of SUSD will file the claim.

How to destroy your local School Board (from 11:57)

Bondsforthewin.com

Bombshell: CDC Admits Natural Immunity Superior to Vaccinated Immunity Alone at Preventing COVID-19 Hospitalizations & Deaths

The Centers for Disease Control has finally admitted that natural immunity from prior infection exists. But it’s even worse than that for the COVID-19 narrative: The CDC also admits that natural immunity from prior infections is superior to vaccinated immunity alone.

Defend The Billionaire’s Bubble Or The U.S. Dollar And Empire – You Can Only Choose One

The Empire is striking back, protecting what really counts, and the Billionaire Bubble sideshow is folding its tents.

CDC Finally Admits Cloth Masks Were Always Political Theater (Jan 2022)

CDC Update: Cloth masks don’t [never] work[ed] and advise against using respirators “if it’s hard to breath while wearing them.”

Ivermectin ‘Works Throughout All Phases’ Of COVID According To Leaked Military Documents

As more and more information pours out of the Project Veritas leaked military documents, there appears to be a damning section in support of Ivermectin as a Covid-19 treatment.

California Will Double Income Taxes to Pay For Proposed Single-Payer Health Care System, Including Coverage For Illegal Aliens

(Cristina Laila) California lawmakers are weighing DOUBLING taxes to pay for a single-payer health care system that would cover all illegal aliens – For The Greater Good.

Headed for a Digital Concentration Camp – Catherine Austin Fitts

Catherine Austin Fitts reminds viewers why the ‘vaccine passports’ and ‘central bank digital currencies’ (CBDC) are so dangerous, and what we must all do in solidarity to save ourselves.

Simply Put: The pandemic is to mandate an experimental gene therapy that the CDC and FDA like to refer to as a “vaccine.” That “vaccine” is for purposes of getting everyone onto a vaccine ID passport. The passport is to force everyone into the new global social credit system. That system is to bring the global population to full obedience, as the globalists control everyone’s access and spending to anything and everything in life, through the use of the new CBDC (central bank digital currency) system they are building toward. And, the icing on the cake for the globalists who orchestrated this – is depopulation.

Some Good News: Rents Have Finally Peaked As Rental Market Enters “Widespread Cool Down”

Drilling into the December data, 61 of the nation’s 100 largest cities saw rents fall this month, indicating a widespread rental market cool down.

Fauci Discourages COVID Vaccinated Americans From Eating At Restaurants

And though the forest was shrinking, the trees kept voting for the axe, for the axe was clever and convinced the trees that since his handle was made of wood, he was one of them.

(Pam Key) National Institute of Allergy and Infectious Diseases director Dr. Anthony Fauci said Sunday on CNN’s “State of the Union” that he would not recommend the fully vaccinated go to restaurants during the Omicron surge of COVID.

Life Insurance CEO Says Deaths Up 40% Among Those Aged 18-64

The death rate for those aged 18-64 has risen an astonishing 40% over pre-pandemic levels, according to the CEO of Indianapolis-based insurance company OneAmerica.

Bank Of Mexico Announces Its Own Central Bank Digital Currency By 2024

End of Easy Money: Global Tightening in Full Swing, While the Fed Promises to Wake Up in Time Next Year

Central banks jacked up rates to catch up with run-away inflation, but most fell further behind; only Russia caught up. The Fed didn’t even try.

Why New York’s Billionaires’ Row Is Half Empty

(Jaden Urbi) Billionaires’ Row in New York City set off a super-slender skyscraper revolution. Today, the towers are an astounding display of wealth, prestige and engineering firsts. But they’re also kind of empty.

Response to Collapse of Build Back Better Legislation Highlights Originating Motive And Timing For The COVID-19 Plandemic

(Sundance) The apoplectic response to Joe Manchin’s rebuke of Biden’s Build Back Better deal in general, and specifically, their reaction to losing the climate change agenda within it, points toward the original intent of COVID-19 in the first place. Continue reading

Sixth Circuit Court Of Appeals Reinstates Biden’s Vax Mandate Setting Stage For Supreme Court Battle

Businesses Have Until January 10 Before Facing Penalties For Noncompliance With Biden’s COVID-19 Vaxx Mandate: OSHA

(Tom Ozimek) The Occupational Health and Safety Administration (OSHA) on Saturday announced a six-day grace period beyond the Jan. 4 deadline for compliance with its COVID-19 vaccine mandate for private employers, saying that it would not issue citations to give employers more time to adjust. Continue reading

Steve Bannon’s Full Interview With ‘The Real Anthony Fauci’ author, Robert Kennedy Jr.

Most decent people comply with the onset of tyranny because they just want it to end. Thinking it will stop, here. Not seeing that by complying, it goes there. That it never ends. Indeed, it is just beginning.

best played at 1.75X

They have no rules, they have no limits on their desire for power and they have no concern for your welfare or that of your family. They will lie, cheat and use whatever means necessary to destroy you.

There is nothing more they can threaten us with that is worse than what they demand we acquiesce too. We’ve got nothing left to lose. Resist.

California Residents Flee Amid COVID Restrictions And Skyrocketing Crime

A recent study performed by the California Police Lab shows that 38 percent fewer people are moving into California since the start of the pandemic and 12 percent are moving out.

Jim Cramer At CNBC Today Said Crypto Is A Better Hedge Than Gold…

Here is Jim Cramer’s track-record on his stock picks this year… 🤡

Jim Cramer also has some medical advise for you too…

China’s Economy Has Collapsed, And It’s About To Bring The US Economy Down With It

(Daily Veracity) Similar to Japan’s devastating 80% market crash in the 1990s, China’s economy is about to experience the biggest crash in history that will take decades to recover from.

No Way Does China Save Us From The Next Bust

Hawaii’s Ultra-Luxury Real Estate Market Smashes Records, As Sales Soar 600%

- In Hawaii, an average of 16 luxury homes sold per week every single week for 39 weeks straight, according to data from Hawaii Life’s Luxury Market Report.

- For the first three quarters of the year, deal volume hit a record-breaking $3.698 billion, and many of these transactions were done in cash.

- There was staggering growth in the ultra-luxury market, which includes homes priced above $10 million, as well.

This $23.5 million mansion in Kauai recently sold to guitarist Carlos Santana (PanaViz).

Evergrande Officially DEFAULTS: Contagion Risk Will Spread to Institutional Investors, Pension Funds, Crypto And More Throughout 2022

Deep Report

(Mike Adams) Evergrande, China’s Ponzi property developer, is now officially in default as Fitch has confirmed the indebted company has missed interest payments on bonds, with over $300 billion in bonds outstanding. Property developer Kaisa is also named in the default decision, and there are nearly a dozen other Chinese property developers that are widely believed to be on the path to default.

Miami Jury Rules In Favor Of Craig Wright, Who Claimed To Invent Bitcoin

(MacKenzie Sigalos) A man who has claimed to be the inventor of bitcoin just won a major U.S. court case, saving him from paying a former business partner tens of billions of dollars in the cryptocurrency.

Nevada Becomes First State To Impose Surcharge On Unvaccinated Workers

(Zachary Stieber) Nevada on Thursday became the first U.S. state to impose a surcharge on workers who have not gotten a COVID-19 vaccine, though the penalty doesn’t take effect until the middle of next year.

What Do They Know? Insiders Are Dumping Stocks At The Fastest Pace In History

(Michael Snyder) Why are CEOs and corporate insiders selling their stocks at a far faster rate than we have ever seen before? Do they know something that the rest of us do not? If stock prices are going to continue soaring into the stratosphere like many in the mainstream media are suggesting, these insiders that are dumping stocks like there is no tomorrow will miss out on some absolutely enormous profits. On the other hand, if a colossal market crash is coming in 2022, then 2021 was absolutely the perfect time to get out. As I have said countless times before, you only make money in the stock market if you get out in time. Could it be possible that many of the richest people in the world have picked the absolutely perfect moment to pull the trigger?

Cali Zeros Water Allocation For Valley Farmers, Caps Valley Cities To The Minimum For 2022

California water regulators will be delivering the bare minimum of water supplies to the state’s municipalities via the State Water Project, the Department of Water Resources announced to water users on Wednesday.

For Valley farmers, who hoped for an ounce of good news related to water supplies heading into 2022, they will see a zero-percent water allocation from state water agencies to start the year.

Black Friday Shopping Down 28% Over 2019 Levels Despite Improvement Over Last Year

The good news: Black Friday retail traffic was up 47.5% over last year. The bad news: It was still 28.3% lower vs. 2019 levels, according to CNBC, citing preliminary data from Sensormatic Solutions.

Inside The Most Expensive Listing Ever In Weston, FL | Mansion Tour

Go inside the most expensive home to ever hit the market in Weston, FL. The $14,000,000 mansion is located around 20 miles west of Fort Lauderdale. The residence is called the Monarch Estate. It unfolds over 12,323 sq ft with 7 bedrooms, 11 baths, and a 93 foot infinity pool all situated on a gorgeous lake. Take the exclusive mansion tour with CNBC’s Ray Parisi and real estate broker Senada Adzem. Take a look.

CEO of American Trucking Association Reveals 37% of Truckers Will Not Comply With Vaccine Mandate – The Consequences Would Collapse Supply Chains and Civic Society

(Sundance) A very interesting interview with Chris Spear, president and CEO of the American Trucking Association.

During a House Transportation Committee hearing on supply chain issues, CEO Chris Spear shares an internal survey showing that 37% of truck drivers “not only said no, but said hell no” to the Biden vaccine mandates.

5th District Federal Court Upholds Ban on Biden’s Vaxx Mandate For Firms With 100+ Workers

Biden’s mandate strategy was always based upon coerced consent, which is RAPE.

- A federal court upheld a ban on Biden’s vaccine mandate for firms with 100 or more workers.

- The 5th US District court called the rules ‘staggeringly over broad’ in an opinion published Friday.

- ‘The mandate is a one-size-fits-all sledgehammer,’ the ruling said.

Zillow Layoffs Tell More About Real Estate Market Than Most Think

Fertilizer Shortage Forcing Farmers To Plant Less

(Elizabeth Elkin) A shortage of nitrogen fertilizer is getting so bad that farmers won’t be able to get what they need for their fields in the near future.

Why China Switched to the New QBZ-191 Primary Weapon

Bond Traders Grounded By Violent Curve Flattening Losses

Over the weekend,ZeroHedge reported that in the aftermath of last week’s staggering, 6-sigma bond moves which saw unprecedented surges in short-term rates everywhere from Australia, to Canada and the U.K. amid growing speculation that the world’s central banks will accelerate plans for raising interest rates in the face of persistent inflation…

Zillow Fires 25% Of Workforce, Scraps Robo-Flipping Program After Huge Loss

On Monday we reported that Zillow Group had ‘halted‘ it’s AI-powered house-flipping operation after 93% of homes listed in their Phoenix portfolio are underwater, and is scrambling to unload 7,000 homes for $2.8 billion.

Today, the company announced during earnings that it’s going to reduce its workforce by 25% and completely scrap its home-flipping operation which began buying homes in December 2019.

Zillow Caught Holding The Bag As 93% Of Phoenix ‘Flipping’ Portfolio Listed At Loss

Two weeks ago Zerohedge reported that Zillow’s electronic house flipping operation had been underperforming – as the real estate company had been buying houses at inflated prices and flipping them for a loss.

Did Mainstream Media Lie About Evergrande Having Made a USD ($47.5M) Interest Payment Friday?

Dr. Marco Metzler: Evergrande Missed Second Past Due Interest Payment In A Week-Is Bankrupt-Could Drag Down Real Estate Sector/HSBC & World Financial System

This past Tuesday I reported that Dr. Marco Metzler, former Fitch analyst and now of DMSA (Deutche Mrkt Screening Agentur GmbH) has announced that the past due interest payment on China Evergrande Group’s offshore international bonds that all of the western media reported as supposedly paid by Evergrande could not be confirmed. Today, he is stating that a second interest payment ($47.5 Million) allegedly made by Evergrande according to the western media last night has not been paid, once again contradicting mainstream media reports.

Largest Private U.S. Landlord Jacking Rents As Purchasing Power Of Blown USD Evaporates

Demand for single-family rental homes is off the charts and shows no signs of abating anytime soon, and that is pushing rents sky-high. This has allowed the largest owner of houses in the U.S. to raise rents.

Criminal Couponers Receive Long Prison Sentences For $31.8 Million Fraud Scheme

The FBI is revealing new details about a $31.8 million counterfeit coupon scheme that landed a Virginia Beach couple in prison for nearly 20 years, combined.

During a search of Lori Ann Talens’ home, agents found thousands of counterfeit coupons, rolls of coupon paper, and coupon designs for more than 13,000 products on her computer. (Courtesy of FBI)

Cushing Storage Approaching Critical Low Level

Traders say that Cushing stockpiles might fall to critical levels within weeks; the last time that happened was in 2014.

/cloudfront-us-east-2.images.arcpublishing.com/reuters/ZRTUGWC57VJETDQH27TGNQRQWY.jpg)

(Devika Krishna Kumar) Stockpiles at the biggest U.S. crude depot are quickly approaching critically low levels. The last time that happened, crude cost more than $100 a barrel.

ANOTHER In-N-Out Burger Shut Down For Refusing To Be ‘Vaccine Police’

The Burger chains are being punished by the state for refusing to ‘segregate’ their customers.

A second chain of In-N-Out Burger has been closed down by county authorities in California after it refused to go along with enforcing proof of vaccination orders.

California Port Worker Exposes Labor Union for Exacerbating Supply Chain Crisis, ‘Keeps Cutting The Work’

I don’t buy this. .Gov would not allow a union to blockade our national economy if they didn’t want it to be blockaded. What’s your take?

A California longshoreman, who works at California’s San Pedro Bay Port Complex, reportedly said the labor unions are exacerbating the supply chain crisis.

TSMC’s $100 Billion American Plan To Fix The Chip Shortage

Taiwan Semiconductor Manufacturing Company makes 24% of all the world’s chips, and 92% of the most advanced ones found in today’s iPhones, fighter jets and supercomputers. Now TSMC is building America’s first 5-nanometer fabrication plant, hoping to reverse a decades-long trend of the U.S. losing chip manufacturing to Asia. CNBC got an exclusive tour of the $12 billion fab that will start production in 2024.

Beijing Orders Evergrande’s Multi-Billionaire Founder To Repay The Insolvent Company’s Debts

Hui Ka Yan, founder of China Evergrande Group, had once amassed a fortune of $42.5 billion, placing him at the top of the wealth rankings for all of Asia. But 73% of that immense fortune has now evaporated, and the tycoon will almost certainly lose even more as anxious creditors, suppliers and homebuyers besiege Evergrande’s offices.

But that’s not nearly enough for Beijing.

Newsom Signs Executive Order Aimed at Alleviating Port Congestion

As California’s shipping ports congestion persists, Gov. Gavin Newsom issued an executive order on Oct. 20 intended to alleviate the crisis.

Food Producer Warns Major Food Shortages Are Imminent

Below are four short news clips outlining a global problem that has been building for a year and a half. Take some time to put back extra frozen, dry and canned foods this week.

The Impending Mass Firing of America’s Unvaccinated Essential Workforce And Ensuing Chaos

The government isn’t allowing natural immunity exemptions to their vaccine mandates because that’s what keeps you alive, healthy, strong and free.

Here’s The Truth Behind Biden’s 24/7 Port Operations Pledge

A guy that burns out after a couple hours of work calls for 24/7 port operations?

King Dollar’s Purchasing Power Plunges Further, as Housing CPI Begins to Climb, Food & Energy Soar, New Vehicle Prices Spike

CPI inflation highest since 2008 and 1991.

The CCP Is Trapped: China Producer Prices Surge At Fastest Pace In 26 Years

China’s factory-gate prices grew at the fastest pace in almost 26 years in September, adding to global inflation risks and putting pressure on local businesses to start passing on higher costs to consumers.

Trans Secretary Buttigieg Tells Us Supply Chain Nightmares Could Last For Years

The truth is starting to come out, and a lot of people aren’t going to like it. When the supply chain problems and the shortages began, government officials repeatedly assured us that they would just be temporary, and most of us believed them. But now it has become clear that they aren’t going to be temporary at all. In fact, during a recent interview with Bloomberg, U.S. Transportation Secretary Pete Buttigieg admitted that some of the supply chain problems that we are currently facing could last for “years and years”. I don’t know about you, but to me “years and years” sounds like a really long time.

“Catastrophic” Property Sales Mean China’s Worst Case Scenario Is Now In Play

Explaining The Logistics Crunch Crisis

Why Evergrande Collapsed – Our Chinese Houses Crumbled

We explore our Chinese apartments, and how the downfall of Evergrande was written on the wall of every tofu building in China. This is only the beginning.

***

Default Of Second Chinese Developer Sparks China Junk Bond Meltdown As Contagion Explodes

New Vehicle Sales Plunge As Prices Soar Amid Supply Chain Chaos, Chip Shortages, & Depleted Inventories

Total new vehicle sales in September dropped to 1.01 million vehicles, down 37% from 1.6 million vehicles in March, when there were still enough new vehicles to sell.

Dr. Richard Fleming Updates on COVID, Antibody Dependent Enhancement and Criminal Proceedings

(October 02, 2021) Renowned scientist Dr. Richard Fleming visits Infowars to give a powerful, in-depth Power Point presentation exposing what’s really happening with Covid-19 and vaccine induced ADE (Antibody-dependent Enhancement) as well as legal proceedings being pursued in international criminal court to hold responsible parties accountable for development of this virus and dissemination of these vaccines.

Cargo Ships Anchored Near Los Angeles and New York Ports Face a 4-Week Delay To Dock, Raising Further Fears Over The Global Supply Chain

The shipping industry is dealing with immense challenges in the run-up to Christmas. Associated Press

Workers Who Maintain Supply Chains Warn of Worldwide ‘System Collapse’

(Jack Phillips) Several industry groups have warned world leaders of a worldwide supply-chain “system collapse” due to pandemic restrictions, coming as Federal Reserve Chairman Jerome Powell suggested that the current period of higher inflation will last until 2022.

California Becomes First State To Require Students Be COVID Vaccinated To Attend Public & Private School

Fresh off his victory in the gubernatorial runoff, California Gov. Gavin Newsom just announced that California’s schools will soon require all eligible public and private school students in 7th grade and higher in the Golden State to be vaccinated against COVID, a first-in-the-nation policy that Newsom says will impact millions of students by fall 2022, or possibly sooner.

Biden Nominates Unabashed Communist For Top Bank Regulator Position

Biden’s Nominee For Comptroller of the Currency, Saule Omarova Earned “Lenin” Award, Praised USSR’s “Equality”, And Wants To “End Banking As We Know It”

China Panics: Beijing Orders Energy Firms To “Secure Supplies At All Costs”, Oil Soars

China officially panicked.

Now that the global energy crisis has slammed China’s economy, leading to the first contractionary PMI since March 2020 as a result of widespread shutdowns of factory and manufacturing, not to mention hundreds of millions of Chinese residents suffering from periodic blackouts, Bloomberg reports that China’s central government officials “ordered the country’s top state-owned energy companies to secure supplies for this winter at all costs.”

Japan Lifts Corona Virus State of Emergency to Rejuvenate Their Economy

TOKYO (AP) — Japan’s government announced Tuesday that the coronavirus state of emergency will end this week to help rejuvenate their economy as infections slow.

China’s Belt and Road Initiative Is Losing Momentum as Opposition and Debt Mount

SHANGHAI, Sept 29 (Reuters) – China’s vast Belt and Road Initiative (BRI) is in danger of losing momentum as opposition in targeted countries rises and debts mount, paving the way for rival schemes to squeeze Beijing out, a new study showed on Wednesday.

Pictured are travelers walking past a map displaying CCP targets of conquest

Pictured are travelers walking past a map displaying CCP targets of conquest

Another Month, Another Record Surge in U.S. Rents To a New All Time High

General Mark Milley Admits Trump Was Being Managed By Administrative State Group Who Run Government, Mike Pompeo and Mark Meadows Assisted

(Sundance) Years of agonizing and frustrating reviews and analysis of the Trump administration activity in real-time are reconciling today. During Senate testimony today before the Armed Services Committee, Joint Chiefs of Staff Chairman, General Mark Milley, clarified some very painful issues to accept. President Trump was being heavily managed by operatives of the Senior Executive Service (SES), and his inner circle was willfully participating.

Italy Orders Companies Not To Pay Unvaccinated Workers

Unjabbed employees face large fines if they show up to work…

The Italian government has passed a decree applying to both the private and public sector ordering companies to withhold pay from workers who refuse to take the COVID-19 vaccine.

The decree mandates that all employees get the vaccine ‘green pass’, which led to questions about what would happen to the millions of Italians who remain unvaccinated.

U.S. Congress Quietly Sneaks In Crypto-Bill Amendment Authorizing Central Bank Digital Currency

The future of money is here; will the Federal Reserve Board be authorized to use distributed ledger technology for the creation, distribution and “recordation” of all the transactions of a Digital Dollar?

(Wesley Thysse) On July 28, 2021, a new bill was introduced in the US House of Representatives. This bill, sponsored by Congressman Don Beyer,1) aims to regulate crypto-currencies. But it does more…

The bill is called the “Digital Asset Market Structure and Investor Protection Act”2) (“Digital Asset Bill”). And for the majority, it sets out future rules for crypto. However, hidden in this bill, changes to the foundation of the Dollar are proposed.

FDA Agrees With Advisors, Limiting Emergency Authorized Booster Jabs To Older & Immunocompromised Americans

Following last Friday’s decision by the FDA’s vaccine advisory panel to only recommend the use of boosters for patients who are a) immunocompromised, b) overweight or c) both, Bloomberg reports that the FDA has decided to accept the advisory panel’s conclusions, as expected – representing a major victory for “the science” over President Biden’s political priorities.

You must be logged in to post a comment.